Alex here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.

Recent Articles/Videos —

Lessons From Stanley Druckenmiller — AK discusses Druck’s advice on betting big, going anywhere, and gaming market scenarios.

The Commodity Boom of 2018 — Our call on oil has been spot on so far. Here’s what we think happens next.

Articles I’m reading —

Mark Dow shared an older but excellent post where he lays out the actual impact of central bank QE on markets and economies. And he explains where credit creation really comes from. This is a must-read for those of you interested in learning what mechanisms drive credit creation and why things like QE induced hyperinflation never materialized following the GFC. Here’s the link and an excerpt.

The truth is the Fed’s monetary policy can influence only the price at which lending transacts. The main determinant of credit growth, therefore, really just boils down to risk appetite: whether banks and shadow banks want to lend and whether others want to borrow. Do they feel secure in their wealth and their jobs? Do they see others around them making money? Do they see other banks gaining market share?

These questions drive money growth more than the interest rate and base money. And the fact that it is less about the price of money and more about the mental state of borrowers and lenders is something many people have a hard time wrapping their heads around–in large part because of what Econ 101 misguidedly taught us about the primacy of price, incentives and rational behavior. If you answer the behavioral questions and ignore the endless misinformation about base money—even when it’s coming from the titans of finance—as an investor you’ll be much better off.

Oh, also, here’s a great primer from Bear Stearns on using return on invested capital (ROIC) as a valuation metric. Some of the slides are sideways so you might want to print it out. Here’s the link.

Plus, here’s a list of the 20 best investment papers of 2017. Some good reading in there.

Video I’m watching —

Buffett did a long (60 min) interview on CNBC this week. I’m more of a Munger fan but this interview was pretty good. If you don’t watch the whole thing, at least check out the section where he explains the market impact of tax reform (starts at about the 15:50 mark). It’s the most succinct explanation of the bill and its impact that I’ve come across. Hint: it’s a huge positive for markets. Here’s the link.

Also, someone (sorry, I don’t remember who) posted to twitter this talk that Mauboussin gave a while back, titled Why You Don’t Understand Luck. It’s focused on luck in sports but could just as easily be about investing. You can find the video here (it’s under 30 mins) and the slides to the lecture here. The three takeaways are (1) We overweight results (2) We rely too much on perception and (3) We make risk-averse choices.

It’s a great talk, check it out.

Book I’m reading —

This week I read One-Way Pockets: The Book of Books on Wall Street Speculation by Don Guyon. I wanna say I ordered this book after Felix Zulauf recommend it in an interview he did a few weeks ago with Barry Ritholtz on the MIB podcast (which was a fantastic interview and you should listen to it if you already haven’t).

Anyways, it’s a fun book. I should admit I’m biased towards old trading books (this one was published in 1917). I love older market books because you find that as much as things have changed, everything kinda stays the same — the most powerful market force, human nature, hasn’t evolved one bit…

In this short book (only 64 pages long) the author shares the results of an in depth study he conducted into the trading habits of the very few successful speculators as well as the money losing public, who were clients of his brokerage firm. And from this study, he teases out lessons and trading rules that are as relevant today as they were 100 years ago. You can read the book in one sitting and it’s worth picking up. Here’s an excerpt.

The few who make money in the stock market await what they consider exceptional opportunities and then play for profits that are worthwhile. They look ahead a week or a month or a year, as the case may be, and disregard the changes that occur in the price movement in each daily session, which to the daily trader assume exaggerated proportions.

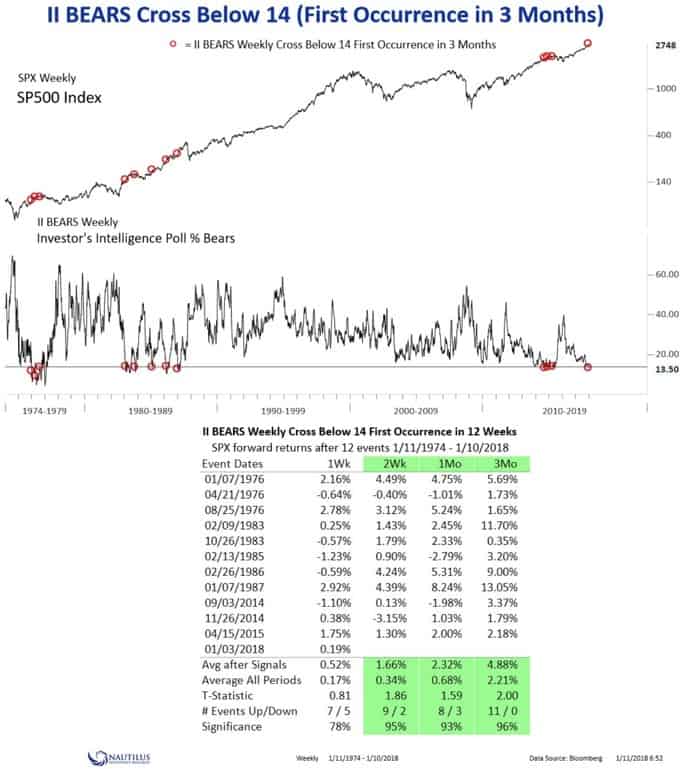

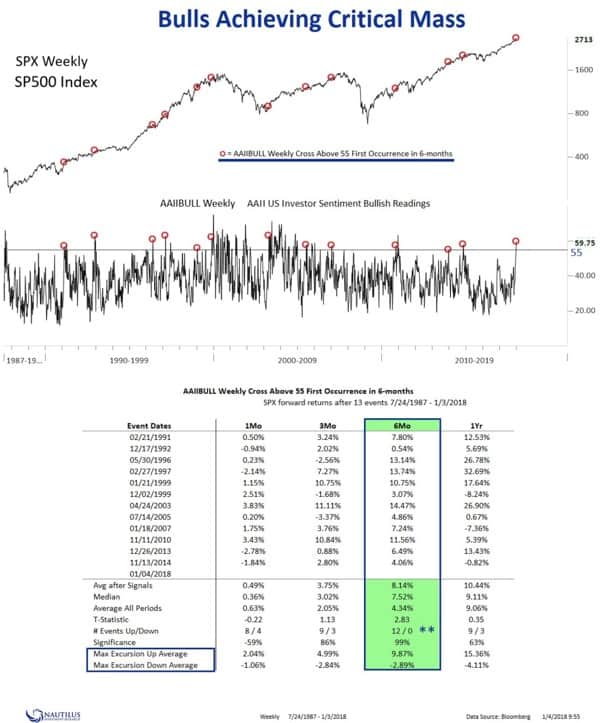

Chart(s) I’m looking at —

Market sentiment is stretched by nearly every measure.

But similar to valuation, gauges of sentiment are not that useful from a timing standpoint, at least not by themselves. I’ve always found sentiment to be a much more useful tool for indicating bottoms than I have for picking tops.

These two charts/studies via Nautilus are a great example of how excessive optimism (as noted by the AAII survey) doesn’t necessarily indicate a coming selloff — at least not in the short to intermediate term.

According to Nautilus, each time the AAII numbers have reached these extreme levels of bullishness, the market has shown a positive return on average over the following 1, 3, and 6-months. And the average returns are pretty high.

I believe it’s likely we’re in the early stages of a “melt-up”, where sentiment will increasingly drive accelerating upward trends, which will further boost sentiment, forming a powerful feedback loop. Jeremy Grantham, of GMO, wrote a great piece on the possibility for this, just the other week. It’s worth a read, here’s the link.

Trade I’m looking at —

This is a beautiful chart of Overstock (OSTK) on a weekly basis. A great long-term technical setup that preceded it’s monster run which began earlier last year.

I almost bought some shares of OSTK towards the end of 2016 because it was very cheap on a comp basis.

I didn’t because I thought the CEO Patrick Bryne is nuts (I still do) and I didn’t think the hype around cryptos would amount to anything. This was of course the worst take imaginable. I never gave the potential for a crypto mania any serious thought. Lesson learned….

Anyways, moving on. OSTK is up 400+% from when I last considered buying and I’ve been digging into the company again. A number of smart HF managers, like Mark Cohodes, are bulled up on the stock. You can watch the pitch he gave for OSTK at a Grant’s Pub conference last October here, and here’s the slides.

The basis of Cohode’s thesis is simple. It’s that OSTK is a valuable strategic e-commerce asset which trades at low multiples relative to peers, has high insider ownership, and has the first and only SEC approved stock loan exchange on a blockchain. The company also has sole ownership of Medici Ventures, which has become a kind of VC arm of OSTK that invests in blockchain/crypto technology.

The stock has risen considerably since he gave that presentation, so the valuation argument is less relevant now. The stock still trades at only 1x revenues, which is lower than its peers (Wayfair trades at 1.6x and Amazon 3.6x), but both companies are seeing revenue growth in the 30+% y/y range while OSTK’s sales are declining.

Cohodes recently tweeted that he thinks OSTK will be a $200+ stock. And Bryne, the CEO, has hinted that he’s looking to potentially sell the company.

As a pure e-commerce play, I think the company is a melting ice cube. Go on Glassdoor and read what many of Overstock’s software engineers have to say about the company and its product. It’s not good.

But, because of the speculative times we’re in. I can see OSTK continue to go vertical from here. It’s almost a perfect Zeitgeist stock, with all its unique investments in the crypto space. It’s trading platform Tzero, which utilizes blockchain technology, is pretty interesting. It could end up actually becoming something someday — which is more than I can say about a lot of these crypto companies sprouting up like weeds.

So if you think the crypto bull market has more room to run, and I think it does. Then a small long position in OSTK may actually be one of the safer ways to play it. The company has a tiny float, only 16M shares, and has a short interest of 32.8%! That’s a lot of fuel to drive the stock even higher.

And if I’ve learned one thing from studying bubbles… it’s that things can, and often do, go to a level of stupid that nobody could imagine.

Quote I’m pondering —

Here’s some thoughts on risk, from market wizard Larry Hite.

I have a friend who has amassed a fortune in excess of $100 million. He taught me two basic lessons. First, if you never bet your lifestyle, from a trading standpoint, nothing bad will ever happen to you. Second, if you know what the worst possible outcome is, it gives you tremendous freedom. The truth is that, while you can’t quantify reward, you can quantify risk.

Risk is a no-fooling-around game; it does not allow for mistakes. If you do not manage the risk, eventually they will carry you out.

I have two basic rules about winning in trading as well as in life: (1) If you don’t bet, you can’t win. (2) If you lose all your chips, you can’t bet.

Most retail traders are focused on trying to make profits. This is the wrong approach.

In markets, as in many complex endeavors, it helps to follow Carl Gustav Jacobi’s advice and, “Invert, always invert.” The successful speculator focuses on risk; how to spot it, how to measure it, and above all, how to manage it.

Focus on risk, and profits will come. Focus on profits, and risk will blindside you like a frying pan to the face.

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. I post my mindless drivel there daily.