Hope you had a great weekend! We’re in the dog-days of Q2 investor letter season. And we love every minute of it. If you haven’t had the chance, check out Part 2 of my series, Cash Flow: It’s All That Matters. Part 2 discusses two cash-flow frameworks that changed my investment process:

-

- Operating Cushion

- Core Growth Profile

You can read it here.

Our Latest Podcast Episodes:

Here’s the letters we cover this week:

-

- Curreen Capital Q2 Letter

- Upslope Capital Q2 Letter

- Silver Ring Value Partners Q2 Letter

We also feature a white-paper on warrants and Michael Mauboussin’s latest podcast interview.

Let’s dive in!

—

July 22nd, 2020

Chart Of The Week: Here’s a great-looking cup-and-handle pattern on a strong, profitable HVAC company. I featured this stock last week’s Breakout Alerts.

I’m diving into the building products space this week. S/O to Harris Kupperman (a.k.a., Kuppy) for tipping me off to this space.

Be on the lookout for a write-up on my favorite companies / set-ups in that space .

__________________________________________________________________________

Investor Spotlight: More & More Q2 Letters!

GIFs by tenor

GIFs by tenor

This week we’re analyzing three investor letters (mentioned above). Let us know if there’s any investor letters you’d want profiled. We’ll include them next week.

Let’s start with Curreen Capital

Curreen Capital: +32.86% Q2 2020

Christian Ryther runs Curreen Captial. The fund returned nearly 33% in Q2 but remains down 26% YTD. Ryther did two things during the most recent quarter:

-

- Sell Garrett Motion (GTX)

- Buy more Kontoor Brands (KTB)

Why Curreen Sold GTX

Anytime an investment has a non-zero chance of going bankrupt, it makes you rethink such an investment. That was the case for Ryther and GTX. Here’s his thoughts (emphasis mine):

“The pandemic-related shutdowns made me reassess my view of Garrett’s ability to overcome its challenges. While I believe that Garrett Motion has an attractive upside-to-downside ratio at current prices, the downside is now bankruptcy, and the probability of that downside has risen.”

Garrett’s asbestos liabilities were always an overhang on the bull thesis. Bulls (myself at the time) concluded that the liability payments weren’t as bad as originally thought. That Honeywell would work with Garrett on those payments to make them affordable.

Throw in COVID and the whole idea of a “not-so-bad asbestos liability” flies out the window.

Curreen sold their remaining stake in GTX for a little over $5/share.

Why Curreen Bought (More) KTB

There were a few reasons Curreen increased their stake in the denim company:

-

- Dynamic CEO making intelligent decisions

- Less-likely chance of bankruptcy

- KTB got covenant relief

- More durable business (people probably won’t stop wearing jeans)

Given the choice between the two investments, Curren concluded the upside/downside ratio was more attractive with KTB. Here’s Ryther’s thoughts (emphasis mine):

“Kontoor does not have quite as much upside if things go as I expect, but there are more ways to lose with Garrett, and losing with Garrett is more likely to involve a wipeout for shareholders. Comparing the two, Kontoor appeared to be a better bet than Garrett, so I sold our Garrett shares and used the proceeds to buy more Kontoor.”

Trusting The Process

Ryther ends the letter with a great reminder for any investor: “I believe that the thing to do in extraordinary times is to stick to our core beliefs and long-term strategy. This means that we continue to look for attractively priced businesses that meet our three key criteria.”

Whatever your own criteria is for stock picking, the important thing is to stick to those tried and true principles. Of course you should confirm those principles are based on sound logic and profitability.

But when crisis strikes and correlations go to 0, there’s a strong desire to throw everything out the window. To follow the “fast-money” and the hottest new trend. Fight that feeling. Stick to your process.

Silver Ring Value Partners: +5.7% Last Twelve Months

Gary Mishuris is the managing partner and CIO of Silver Ring Value Partners (SRVP). The partnership returned 5.7% over the last twelve months. Let’s see what he holds and why. You can read his full Q2 letter here.

Current Holdings

SRVP’s portfolio is a collection of equity, debt and derivative instruments. It’s one of the more unique portfolios I’ve seen and provides insight into the many ways one can make money in markets. Here’s Mishuris’ top five positions (as of Q2 end) as % of portfolio:

-

- Covetrus, Inc. (CVET): 22.4%

- “Undisclosed Position #4”: 13.5%

- Discovery Communications (DISCK): 11.6%

- Charles & Colvard (CTHR): 10.9%

- Owens-Illinois (OI): 10.2%

The fund also has a “Hopes and Dreams” short basket. It’s a collection of long put-options on the following names: TSLA, ROKU, SNAP, WORK, and BYND. The puts expire January 2021.

Investment Thesis Tracker

Mishuris has an Investment Thesis Tracker in Excel that looks real productive. Take look at it below:

![]()

The tracker follows each investment thesis to see if it’s in-tact or defunct. The color-coding goes as follows:

-

- White: thesis is tracking roughly in-line with my base case

- Orange: thesis is tracking somewhat below my base case

- Red: thesis is tracking significantly below my base case

- Dull Green: thesis is tracking somewhat better than my base case

- Bright Green: thesis is tracking significantly better than my base case

- Black: Investment exited

If the base case involves a roughly-right range of intrinsic value, using the daily stock price is a helpful measure.

Extreme Options Discussion

The letter dives deep into “extreme options”. Think of these as lottery tickets. The kind of trades you see on r/WallStreetBets. But in this market scenario, Mishuris thinks certain situations warrant a closer look at these lotto-tickets. One of those times is now.

Mishuris distills options into the following example (emphasis mine):

“So imagine a stock with a price of $100. Picture a vertical line on a chart at the $100 mark on the x-axis. Now imagine that someone draws a normal probability distribution (aka a “bell curve”) around that vertical line. How wide or narrow this bell curve ends up being is determined by how volatile the market perceives the stock to be, which is usually based on how volatile it has been in the past. The wider the curve, the more expensive it is to buy an option at a given strike price. This makes intuitive sense – the more volatile we perceive the stock to be, the more likely it is to reach any price that is not $100.”

Here’s the kicker: bell curves are drawn based on the current price. It doesn’t matter where the stock traded a few weeks (or days) ago. Mishuris explains (emphasis mine):

“What happens if the $100 stock price changes drastically? Let’s say that for some reason the stock price goes from $100 to $20. The option model adjusts by drawing a new bell curve, this time around $20. It could care less that the stock was just at $100. The model assumes random movement around the current price, so if that is now $20, then that’s where the model’s bell curve will be. In most circumstances, the curve will also widen, since option market participants will expect higher future volatility than before the drop from $100 to $20.”

As business analysts, we know a company’s actual value doesn’t change as often as it’s quoted market price. Maybe that $100 to $20 drop in price reflects a mere $20 change in intrinsic value estimations? If that’s the case — and the stock’s worth $80, not $20 — call options look very attractive. Let’s head back to the letter for more clarity:

“Buying such an option can produce [a] 20x-40x return if the price to value gap closes before the option expires. In other words, our fundamental value for such an option based on our intrinsic value estimate for the company is much higher than the market price for that option.”

I’ll leave the options talk with this: Even if intrinsic value is higher than the current stock price, there are many ways to lose in options trading.

Alright, back to more stock talk. The letter offers insight into a few holdings:

-

- Carnival Corp (CCL)

Mishuris’ Take: “We do know that this is an industry leader with ~ 50% market share which has earned slightly more than its cost of capital over the full economic cycle. Structurally the business has not changed, and once demand is restored the industry economics are likely to be similar to the past. If we look at the company’s balance sheet, the replacement cost of its fleet is over $40 per share after taking into account the debt. So as long as this business is a going concern and demand is restored to prior levels, a base case value of around $40 is reasonable. Without any cash burn the business would be worth north of $50, and we can treat the cash burn and the time value of money as getting us to around $40 of equity value.”

How He’s Playing CCL: October 2020 senior unsecured bond, September 2020 $22.50 call option

-

- Covetrus, Inc. (CVET)

Mishuris’ Take: In the depths of the March/April sell-off I was able to add a large number of shares to our CVET position in the $5-$6 price range. This was less than either of the two businesses within the company are worth and a small fraction of my $28 base case value estimate. When the stock tripled quickly and became a very large part of the portfolio I began gradually reducing the position in order to comply with my risk management parameters on position sizing. I did so reluctantly since I think the business is still substantially undervalued and the company remains our largest position.

CVET Presentation: You can watch Mishuris’ CVET pitch at MOI Global Wide Moat 2020 here.

-

- Undisclosed Position #4

Mishuris’ Take: “This has clearly been an unsuccessful investment thus far. What’s more, the company’s business positions it squarely in the path of the economic fallout from the COVID crisis, delaying any progress we might otherwise have seen. Offsetting these facts are the following:

-

- The stock is currently trading at/below cash per share with no debt

- We have a founder-CEO most of whose net worth is in the company’s stock who is working incredibly hard to create value for all of us

Given the events, I re-underwrote the business value from scratch. I believe this presents a very unusual asymmetric value opportunity where the probability of meaningful capital loss from here is small, and it is very easy to see returns in the 100%-300% range from these price levels. I have been gradually moving the position size from medium to large to reflect the opportunity.”

-

- Owens-Illinois (OI)

Mishuris’ Take: “This is still one of the more undervalued companies in the portfolio with very strong upside once the business stabilizes. I know that cheap small-cap companies with leverage are currently extremely out of favor, but as long as I am approximately right on the cash flow stream we should benefit from the company’s substantial free cash stream over time.”

How He’s Playing OI: Reduced equity and increased out-of-the-money call options

-

- Gilead (GILD)

Mishuris’ Take: “The stock rallied to ~ 90% of my Base Case due to optimism for the prospects of revdesimir, the only approved drug for COVID. On a call the CEO was asked multiple times about the economics for the drug and dodged all questions with platitudes. Finally, an analyst asked him point blank if he expects to make a profit for the company on this drug. He dodged that question as well. The combination of these circumstances and the price/value ratio led me to conclude that it is time to move on, and I exited our position during the quarter.”

Upslope Capital: +1.2% Q2 2020

George Livadas runs Upslope Capital and returned 1.2% for Q2. The fund’s roughly breakeven on the year (down 0.7%). Upslope’s ethos is to, “deliver attractive, equity-like returns with significantly reduced market risk and low correlation versus traditional equity strategies.”

You can read his Q2 letter here.

Here’s a snapshot of Upslope’s current portfolio:

Upslope’s a mid-cap focused fund, so its no surprise to see 39% of their portfolio in mid-cap stocks. The remainder of the portfolio includes small-cap stocks (34%), large-cap stocks (24%) and micro-cap stocks (3%).

New Long: Ritchie Bros (RBA)

Upslope’s Take: “Ritchie Bros. is the world’s leading auctioneer and operator of marketplaces for the sale of used heavy equipment (construction, farming, energy, etc.). Through in-person and online auctions, as well as brokered transactions, RBA facilitated the sale of $5+ billion worth of equipment in 2019.”

Their thesis hinges on five key points:

-

- Clear, durable competitive advantages: “As the clear leader in facilitating used heavy equipment sales, RBA enjoys significant competitive advantages – similar to those of a dominant financial exchange (e.g. stock market)”

- Potential inflection point with parallels to financial exchanges: “When financial exchanges have shifted in the past from floor- and/or phone-based trading to purely “electronic” (online) trading, volumes have generally moved higher.”

- Financial results tell a consistent story: “RBA has historically grown GTV (global transaction value, a key metric used to track the health of the business) in the high-single-digit range. Even in the financial crisis, GTV only fell ~8% from peak to trough (over two years).”

- Potential cyclical upside: “RBA has indirect exposure to infrastructure spending (and odds for some kind of stimulus on this front in the next 12 months appear higher than normal) and could be a beneficiary of distress in the energy sector (liquidation auctions).”

- Strong balance sheet: “We may be nearly out of the woods with regards to the COVID-19 crisis (from a market perspective), but a strong balance sheet is still highly desirable today. RBA is levered just 1.0x net and has good access to liquidity.”

- Key Risks: “(A) New, unproven CEO, (B) lumpy quarter-to-quarter performance and (related) potential for losses on inventory deals (i.e. part of RBA’s model involves actually purchasing inventory to be sold in auctions), (C) uncertainty regarding long-term impact of COVID-19, (D) general and unpredictable cyclical nature of the business.”

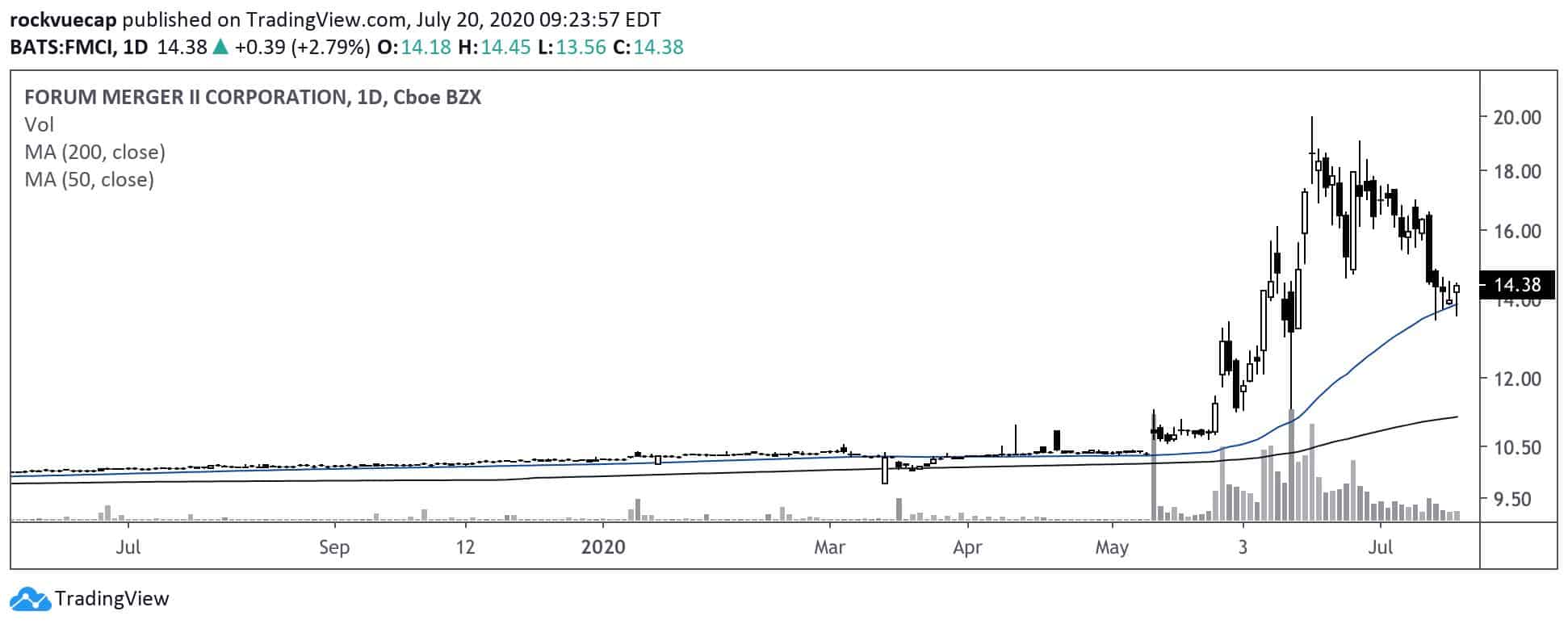

New Short: Basket-o-SPACs

It’s no secret I love the land of SPACs. The financial market wasteland where pump-and-dumpers thrive, Robinhood traders rejoice and fundamental investors get slaughtered.

Livadas discloses a short in Tattooed Chef (FMCI). If you’re like me, the first thing you think of when hearing “Tattooed Chef” is Guy Fieri. Here’s Livadas’ take on the company (emphasis mine):

“FMCI, on the other hand, simply sells pretty standard, “plant-based,” pre-prepared frozen foods. Some examples: $13 bags of frozen vegetables and $16 cauliflower-crust frozen pizza – hardly exciting or unique stuff. Despite an obvious lack of competitive advantages and the long list of typical SPAC headwinds/risks, FMCI shares appear very richly-valued.”

Take a look at the chart below …

Speaking of SPACs … let’s get to our Whitepaper of The Week.

__________________________________________________________________________

Whitepaper of The Week: Stock Warrants & Stock Performance

GIFs by tenor

GIFs by tenor

Soku Byoun wrote the 2014 paper Stock Performance following Seasoned Stock‐Warrant Unit Offerings. In it Byon dives into the world of warrants. Why is this applicable today? Many SPACs (see above) issue warrants plus plus common stock.

There’s a reason companies offer warrants to shareholders, as Byon notes (emphasis mine):

“A desirable feature of warrants in unit offerings is that they generally bring in funds only if they are needed. If the company grows, it will probably need new equity capital. At the same time, growth will cause the price of the stock to rise and the warrants will be exercised at the latest by expiration. The firm will then not need to tap the capital markets through seasoned offerings to complete their financing requirements. The second stage financing should be accomplished by the exercise of the warrants.”

That’s an attractive option for public companies and shareholders.

Warrants are like call options. If the stock reaches its strike price, the company exercises the warrants. Investors in those warrants profit. If the stock doesn’t reach its strike price, investors sit on a fat zero.

Therefore, warrant investors should expect higher return for that investment. Byon expands on this idea, saying, “Therefore, the average long-run performance of unit offerings must be greater than that of share offerings to make up for the higher risk undertaken. This is also consistent with the Chemmanur and Fulghieri (1997) model, which implies that, for a given level of risk, highquality firms use units to signal their quality.”

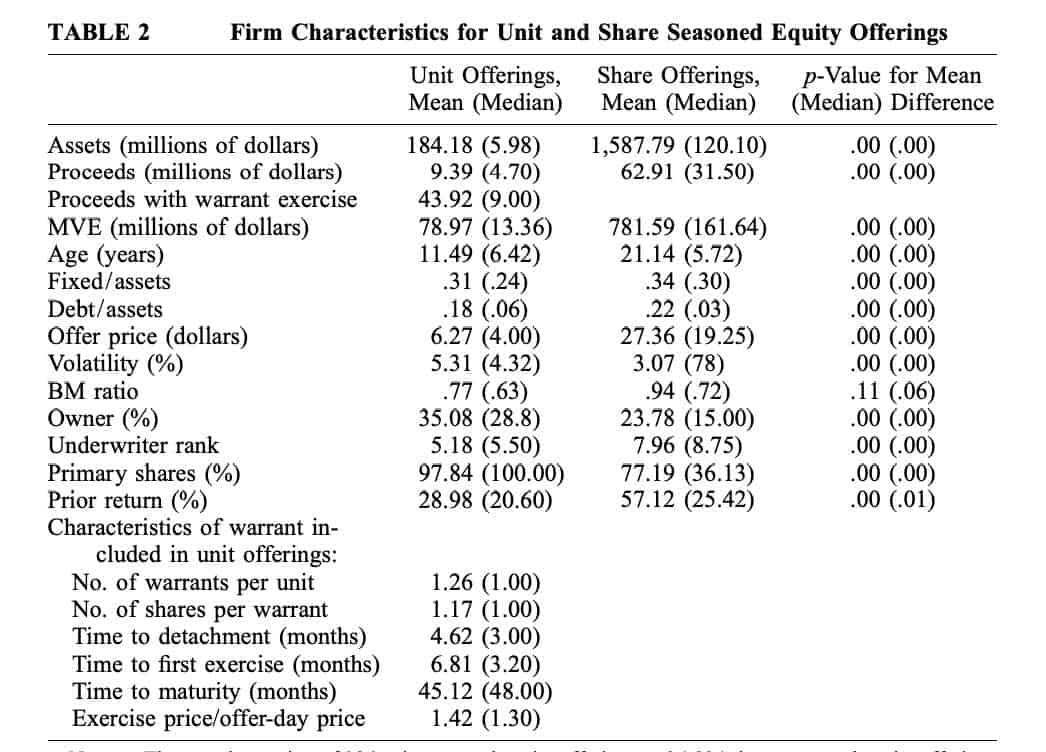

Here’s a rough outline of the average SPAC statistics. It holds clues into what one can reasonably expect from the average SPAC IPO:

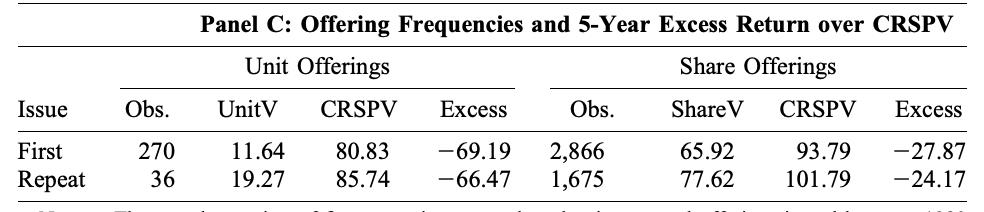

Finally, I’ll leave you with data on excess returns for SPAC-related unit offerings. Spoiler: they’re not good!

__________________________________________________________________________

Podcast of The Week: Michael Mauboussin, What Got You There

GIFs by tenor

GIFs by tenor

As I write this sentence, I’m finishing Michael Mauboussin’s latest podcast on What Got You There. It’s one of his best podcast interviews. Many gems on myriad topics including:

-

- Writing

- Thinking

- Sports and business

- The importance of reading

Give it a listen. You won’t regret it.

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!