Alex here with your latest Friday Macro Musings…

Special Announcement —

Chris D. our resident systems trader has just launched his new course Backtesting Mastery: Build Consistently Profitable Trading Systems Forever.

In this course Chris details the exact steps he uses to create his consistently profitable trading systems from scratch. And the best part about it is that his method requires zero coding experience.

Enroll before this Sunday, July 21st at 11:59PM. After that the special discounted launch price will expire.

Click here to check out Backtesting Mastery!

All purchases come with a 30-day money back guarantee, so there’s no risk to checking this out!

Latest Articles —

A Monday Dozen — Charts, Charts, and some more Charts; 12 to be exact. There’s all sorts of stuff in this edition: liquidity, sentiment, monetary policy, the peso and more.

Rough Seas Ahead — I explain why we just went to over 50% cash and share the indicators/data points that tell us there’s a high probability of a market selloff in the coming weeks.

Articles I’m reading —

MoonTowerMeta put together some good notes on @Patrick_Oshag’s interview with @Jesse_Livermore (here’s the link). One of the more interesting takeaways from that chat, in my opinion, was Jesse’s theory that markets may permanently become more expensive. Here’s a cut from the notes explaining his point.

Why is it plausible that markets get permanently more expensive?

- Valuation is a function of the required rate of return to which liquidity is an input. Imagine a pre-Fed wildcat bank. You would not accept such meager real rates of return because you do not have the confidence in the liquidity of your deposit. So much of our required rates of return come down to confidence. The progress of finance has been towards greater networks levels confidence which creates downward pressure on required rates of return. The Fed put is an example of this.

- With low growth and inflation (demographics follow Japan, Europe), volatility will be to the downside but the Fed can also act more aggressively without fear of inflation. Higher structural valuations may be reflecting this market understanding.

I don’t necessarily agree but I don’t disagree either. It’s possible and some good food for thought as we move into this next decade which will almost assuredly look nothing like the last.

Ray Dalio published a paper this week titled “Paradigm Shifts” where he talks about the major economic transition points throughout history along with the one we’re approaching now. It’s a good article and I’m sympathetic to much of what he has to say. Like Dylan said “the times are a changin’” and what’s worked well in the current paradigm is unlikely to work well in the next.

Dalio, in reference to equity and equity-like investments, wrote: “ I think these are unlikely to be good real returning investments and that those that will most likely do best will be those that do well when the value of money is being depreciated and domestic and international conflicts are significant, such as gold.” Again, I agree. Here’s the link to the piece, it’s worth a read, along with an excerpt.

I have found that the consensus view is typically more heavily influenced by what has happened relatively recently (i.e., over the past few years) than it is by what is most likely. It tends to assume that the paradigms that have existed will persist and it fails to anticipate the paradigm shifts, which is why we have such big market and economic shifts. These shifts, more often than not, lead to markets and economies behaving more opposite than similar to how they behaved in the prior paradigm.

Lastly, if you’ve got time I suggest giving this Chuck Akre speech titled “An Investor’s Odyssey: The Search for Outstanding Investments” a read. It’s an oldie but goodie. I’ve mentioned Chuck in these here pages a number of times. He’s a value investing OG and spits salty wisdom befitting of his long and successful career in markets. Here’s the link and a cut:

At our firm we have this quaint notion that in certain economic environments and in certain stock market environments both of which we have an abysmal record of predicting, we are well served by owning things which were a modest valuation, at least to start. There’s an old Wall Street ad agent attributed to Goldman Sachs…which says, “Something well bought is half-sold.” Taking a completely different tact, if we had properly identified the compounding in machines and had bought them at modest valuations, we would be set up for the famous Davis double play. That is, the business… will compound our capital at an above-average rate, and we’re in line for an increase in market valuation, but double play indeed.

Charts I’m looking at—

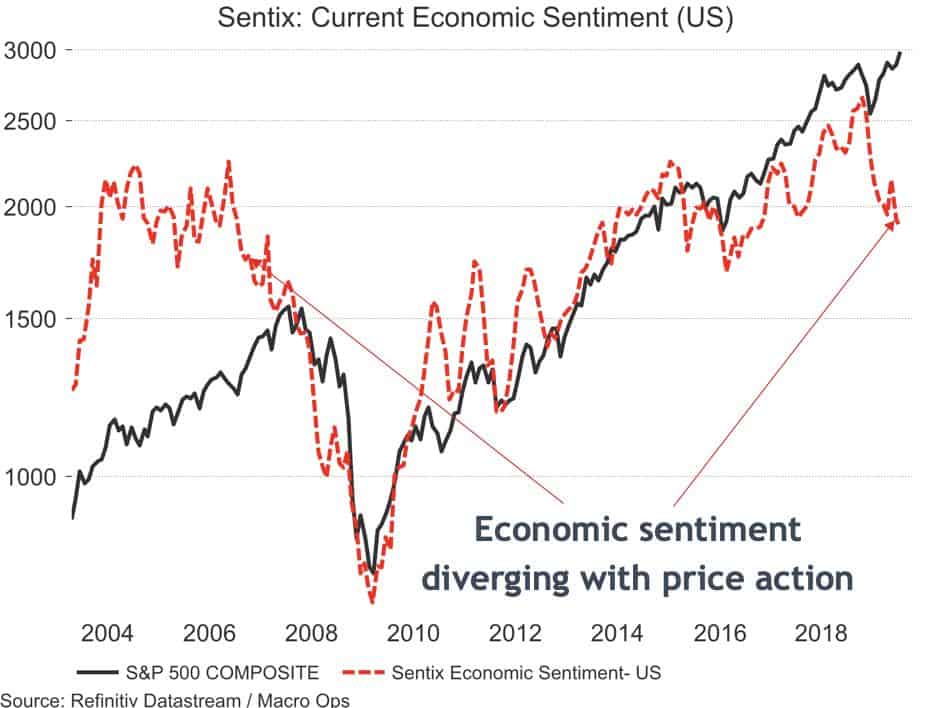

Check out the following chart showing Sentix’s “Current Economic Sentiment” on US data (dotted red line) and the S&P 500 in black. Sentix’s survey data comprises the opinions of over 5,000 investors around the world. Typically, survey data like this should be viewed from a contrarian’s perspective. But, the economic sentiment data is a little different. It usually follows the market, which makes sense, people buy risk assets when they’re optimistic on the economy and vice versa.

What’s concerning is the growing divergence between the survey data and the market itself. The last time there was a divergence like this was in the run-up to the GFC. I’m not saying a crash is around the corner, but we did just recently turn a lot more defensive (over 50% in cash). This market is being propped up by buybacks and passive inflows while the marginal investor is taking his money out as the deteriorating macro data accelerates.

More food for thought…

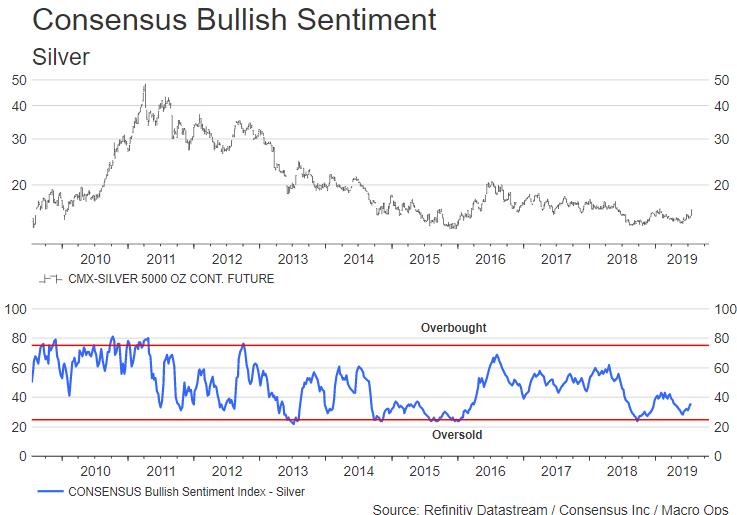

We at MO have been pounding the table about precious metals for the last two months, saying a major regime change was afoot. And I’ve been noting (aka: tweeting) over the last two weeks about the fantastic looking technical bottom setting up in silver. Well, this week the market finally gave us an answer and it looks like this cyclical bull in precious metals is just getting started.

Even sweeter, is that sentiment for silver is kicking off from really low levels (meaning people have been very bearish on it). So there’s plenty of positioning fuel to boost this trend higher. On a side note, the above chart is from Consensus Inc.

Consensus Inc. has been in the game since 1971. Their sentiment/charting data is similar to DSI but works on a longer time horizon and their subscriptions are a fraction of the price. If you’re interested in checking out their offerings then just follow this link. My friend Richard, who runs the show at Consensus is offering all MO readers a free 4-week trial. The data is also available for those of you with terminals (Bloomberg and Reuters).

I get no monetary benefit from pitching their wares. I’m just a fan of the service and want to get their name out, so check them out!

Video I’m watching —

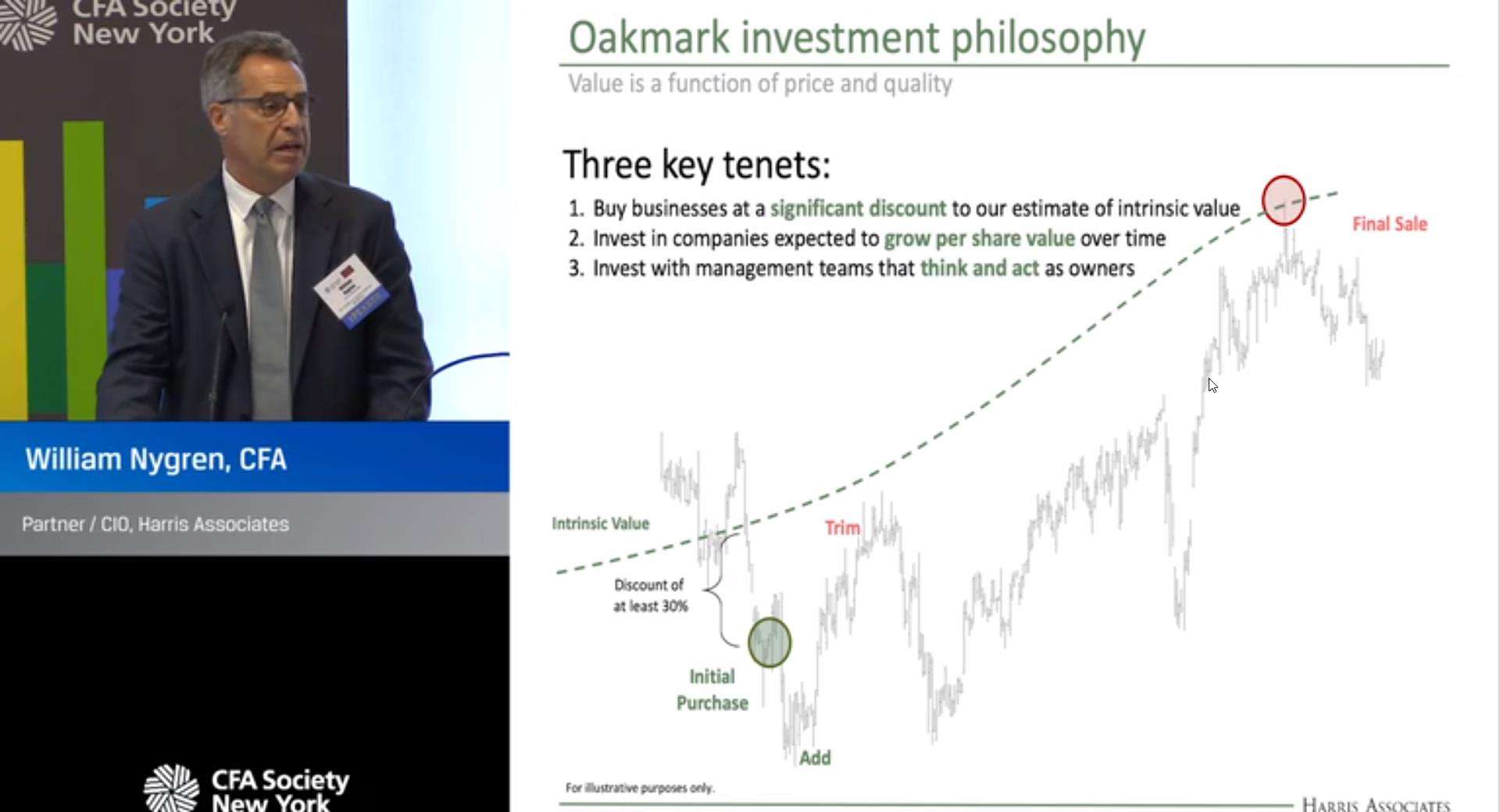

This is a good and short (18 minutes) presentation from Bill Nygren, CIO of Oakmark. Bill gives an overview of his investment process and talks about the evolving value investing landscape. Here’s the link.

Trade I’m Considering —

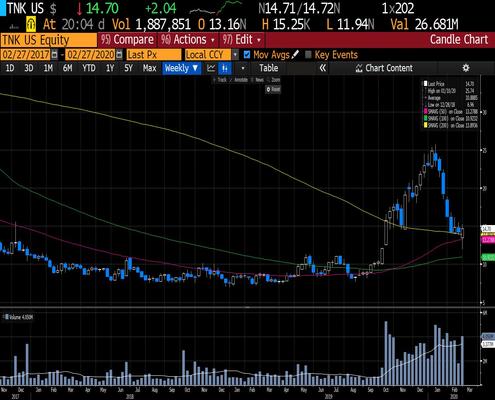

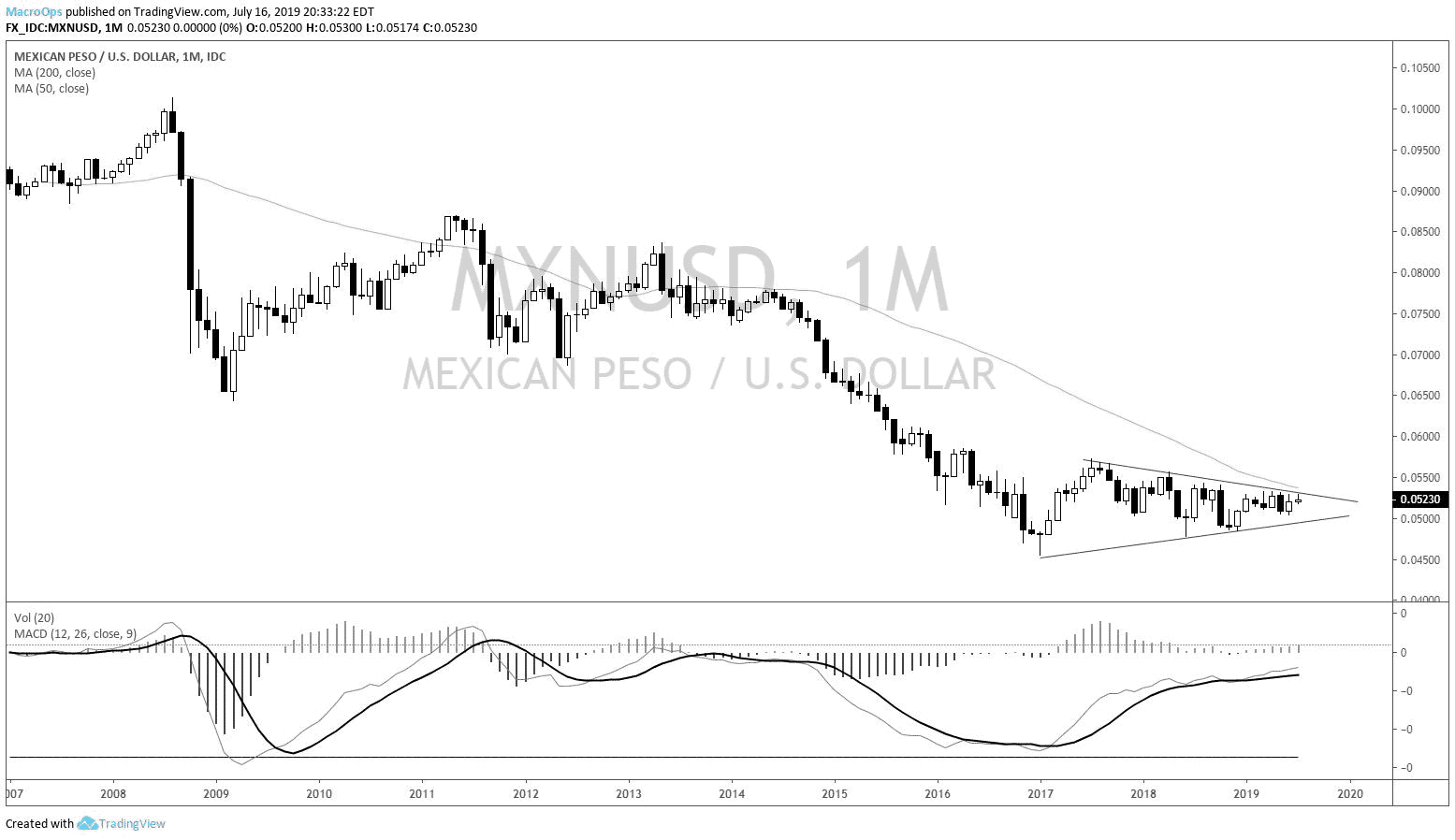

This is one of the best looking charts in macro at the moment. It’s a monthly of the Mexican peso. I’m a dollar bear who’s already short USD versus CAD and CHF but will be adding this to my basket very soon. The peso is one of the highest yielding currencies right now. I’ll probably be long by the time this goes out.

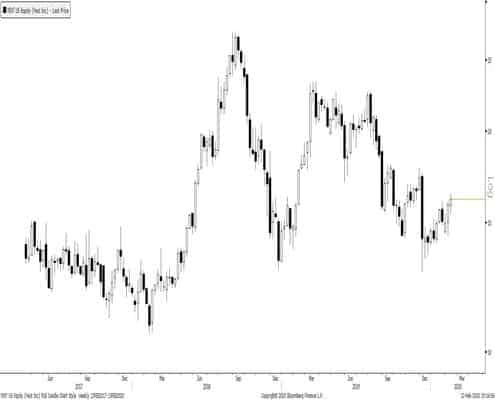

Evan Tindell put together a good writeup laying out the bull case for French holding company, Bollore (BOL). I know a number of smart value-focused fund managers who really like this name. I haven’t taken a deep look at it yet myself, but the thesis is compelling and the chart is bien fait.

Book I’m reading —

This week I found myself rereading some passages from Schwager’s Hedge Fund Market Wizards. The entire Market Wizards series is a must read for anybody serious about the game of speculation.

Here’s one of my many highlighted passages from the book (this is from the chapter with hedge fund manager Colm O’Shea in response to what 90% of profitable trading comes down to):

Implementation and flexibility. You need to implement a trade in a way that limits your losses when you are wrong, and you also need to be able to recognize when a trade is wrong. George Soros has the least regret of anyone I have ever met. Even though he will sometimes play up to his public image as a guru who knows what is going on, it is in no sense what he does as a money manager. He has no emotional attachment to an idea. When a trade is wrong, he will just cut it, move on, and do something else. I remember one time he had this huge FX position. He made something like $250 million on it one day. He was quoted in the financial press talking about the position. It sounded like a major strategic veiw he had. Then the market went the other way, and the position just disappeared. It was gone. He didn’t like the price action, so he got out. He doesn’t let his structural views on how he believes the market will play out get in the way of his trading. That is what strikes me about really good money managers —- they don’t get attached to their ideas.

Watch out for the fintwit proselytizers who use ten-dollar words and complex intelligent sounding narratives to tell you why something has to happen. Nobody knows anything, we’re all just playing a game of possibilities. Manage your money accordingly.

Quote I’m pondering —

While the M.P.C. continued to talk about traders in terms of their specialties, most of our traders were becoming generalists, which meant they followed and traded a wide variety of commodities. This type of trading made sense because a trader could shift his attention to the commodities that were active and offered the opportunity for profitable trades. A generalist had to know something about the fundamental aspects of each commodity and combine that knowledge with the appropriate use of technical analysis, which meant that he had to have the ability to interpret chart patterns of the price movements of each commodity. The ability to read charts is more an art than a science. I began to realize that trading was an intuitive process rather than an intellectual one. All traders were privy to the same information. Some had more sophisticated methods of analyzing the markets, but that didn’t seem to make a difference. The people who made the most money had the best money management skills and a good sense of market timing. ~ Irwin Rosenblum, from his book “Up, Down, Up: My Career At Commodities Corporation”

Be a fox, not a hedgehog… If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.