***(The following is an excerpt from a recent note sent to MO Collective Members)***

Markets are about to hit some rough seas in the month(s) ahead. I’m not calling for a bear market or major crash but more expecting some choppy sideways/slightly lower action. We’re going to button down the hatches a bit (ie, reduce equity exposure).

Here’s what I don’t like:

- Numerous measures of sentiment/positioning are now showing excessive bullishness and complacency

- Our indicators suggest US GDP is about to roll over hard and that means lower earnings

- Consensus earnings estimates for Q4 on are way too high considering

- Market valuations are at levels that have acted as a brake on further gains in the past

- I’m expecting earnings beats but bearish guidance this quarter

Starting with sentiment and positioning.

Our Composite Sentiment/Positioning Index is back above the 50 level (red line) which marks excessive bullishness and complacency.

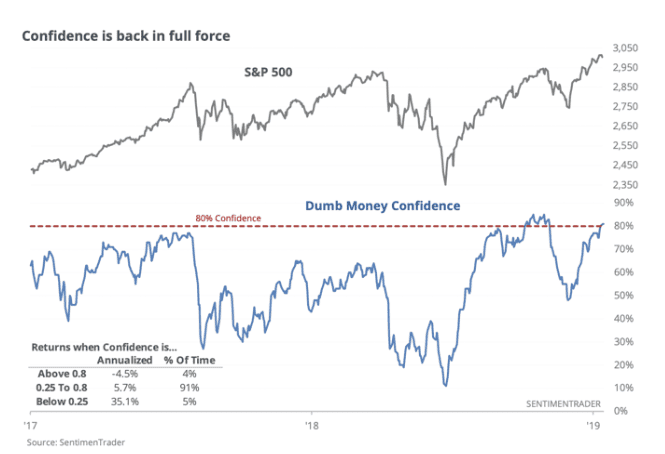

Sentiment Trader’s “Dumb Money Confidence” indicator is near cycle highs. Forward returns for stocks have been weak following similar readings in the past.

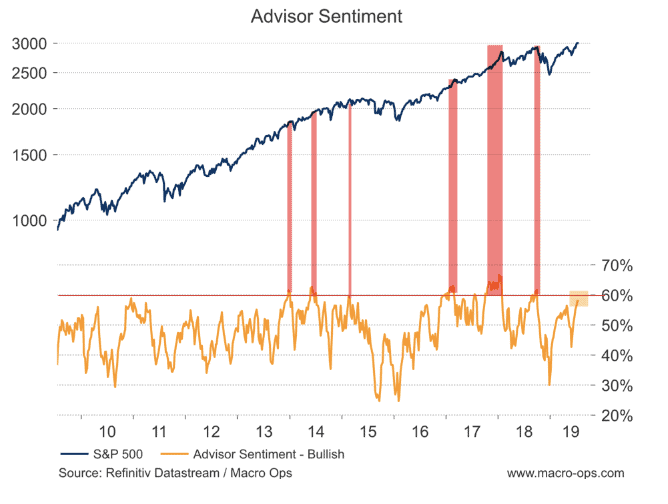

Investors Intelligence Advisor Bullishness is near 60%. The market has dipped or traded sideways over the following month each time this indicator has crossed the 60% mark.

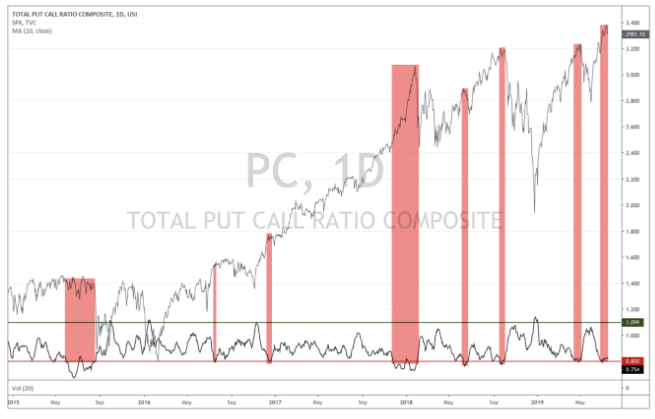

And then our Total Put/Call 10-day moving average indicator shows that investors are complacent and are not hedging their downside relative to their bullish bets.

Now let’s look at economic growth.

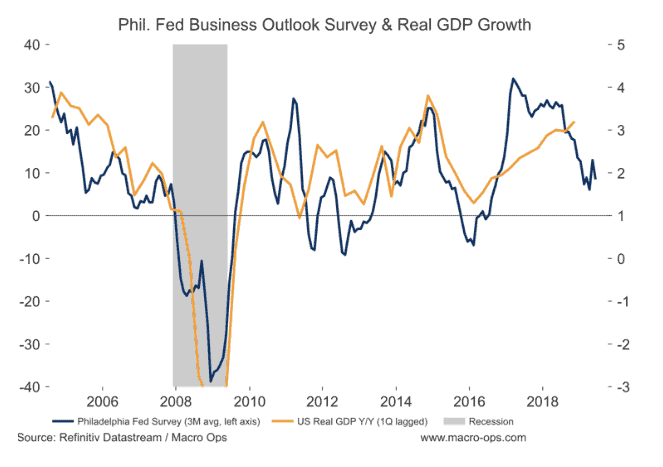

I’ve been talking about this one a lot, but our Philly Fed indicator suggests US GDP growth is headed for sub 2%.

The Atlanta Fed’s GDP Now Forecast is tracking just 1.6% growth.

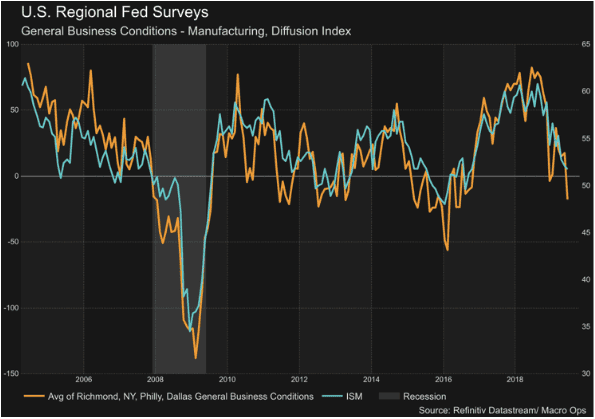

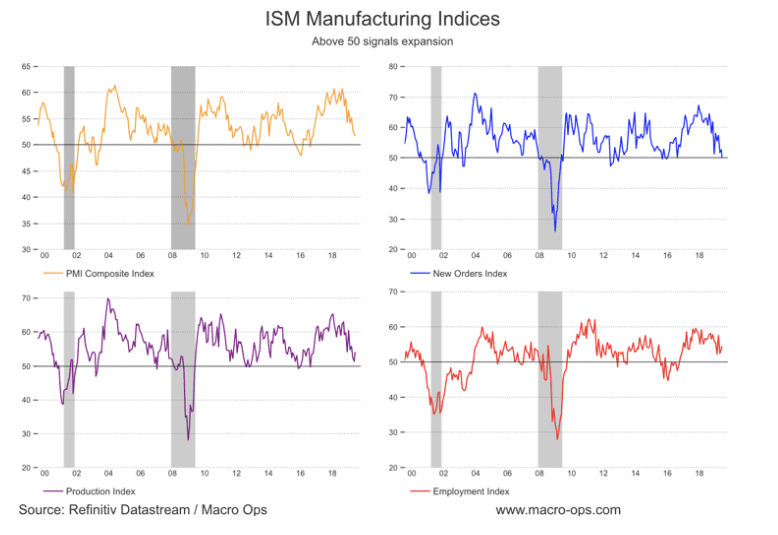

Our Business Conditions Diffusion Index points to the ISM entering contraction territory in the coming months.

The Yardeni Boom-Bust Barometer, which is a composite fundamental indicator, is diverging from the uptrend in stocks.

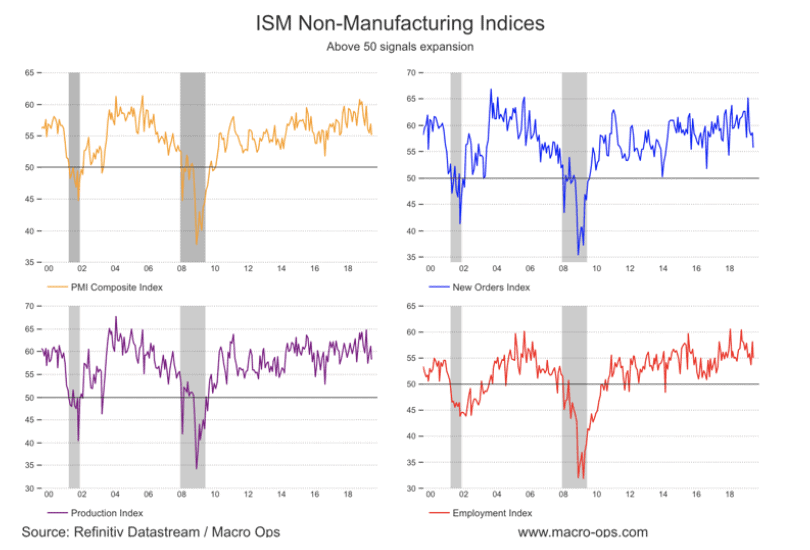

Service’s growth looks like it’s about to follow manufacturing’s lead and trend lower.

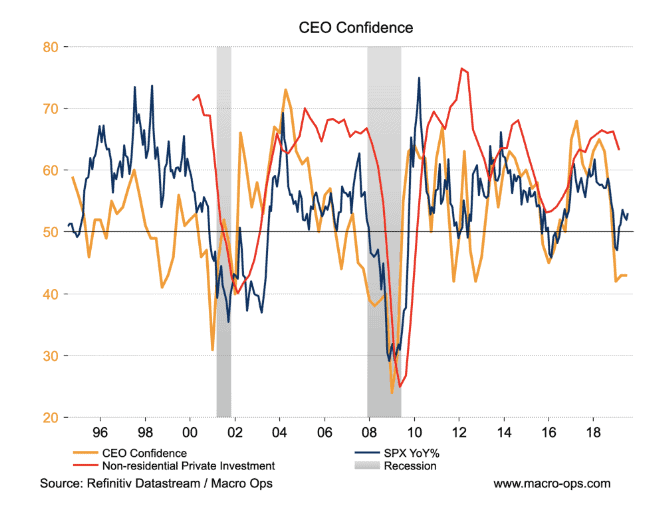

Remember the Levy/Kalecki Profits Equation? Net investment is what drives profits in an economy, which is why capex or non-residential private fixed investment is so important to both economic and earnings growth. This is why the following is no bueno.

The fiscal stimulus in the US is rolling off. What was once a tailwind is becoming a headwind. Growth in the US is now “catching down” with the rest of the world. This is bearish US equities, bullish bonds, bullish precious metals, and bearish the US dollar.

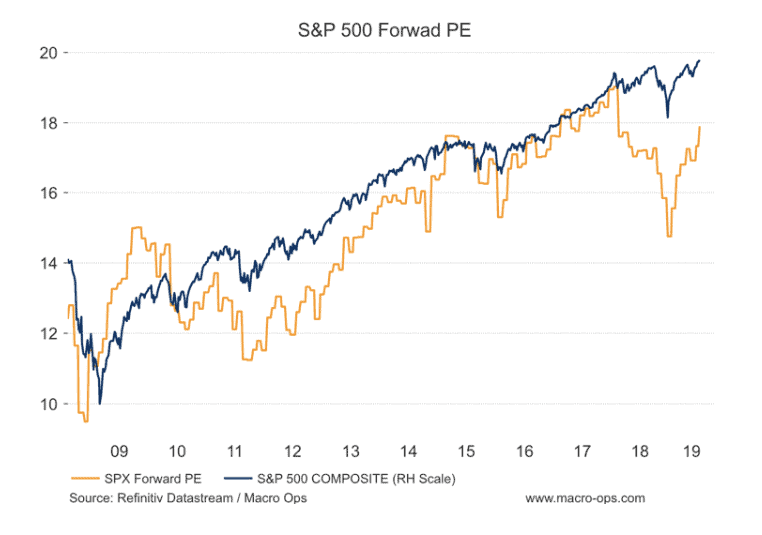

Considering this backdrop, earnings estimates following Q3 onwards are way too optimistic and the current Forward PE for the S&P 500 is too high at just under 18x next year’s earnings.

Consensus earnings estimates for this quarter are low so I’m expecting some easy beats. But we’re likely going to get decent beats coupled with bearish forward guidance and management commentary this quarter, commentary like the following from CSX Corp’s recent earnings release (excerpt via CNBC):

“Both global and U.S. economic conditions have been unusual this year, to say the least, and have impacted our volumes. You see it every week in our reported carloads,” Chief Executive James Foote said on a conference call Tuesday after the earnings report. “The present economic backdrop is one of the most puzzling I have experienced in my career”

Mark Kenneth Wallace, executive vice president of CSX, said on the earnings call. “On the merchandise … there are signs of slowing economic conditions in both IDP and GDP for Q3 and Q4, pointing to a less robust economy in the second half.”

“We’ve obviously seen evidence of this in our own business, and now see a softer industrial environment, with signs in our automotive, chemicals and metals segment,” Wallace said.

Brace yourselves for some higher volatility!