Alex here with your latest Friday Macro Musings…

As always, if you come across something cool during the week, shoot an email to alex@macro-ops.com and we’ll share it with the group.

Latest Articles/Podcasts/Videos —

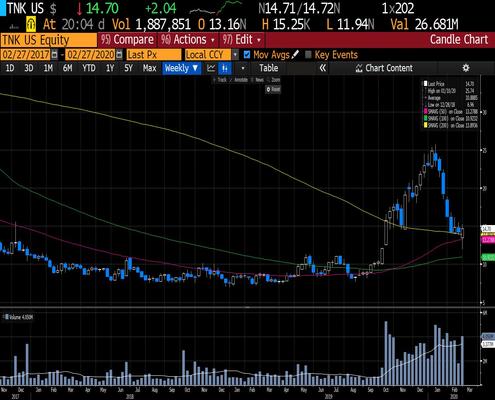

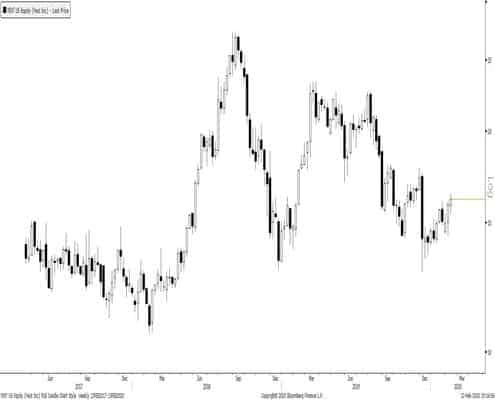

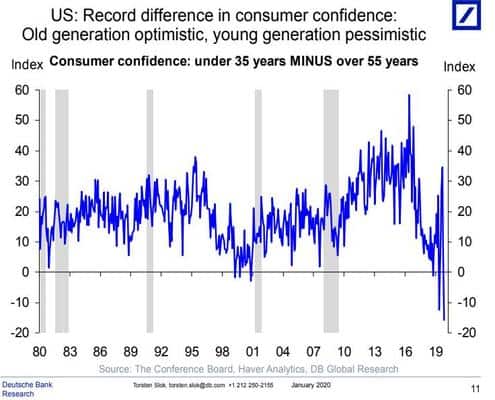

Your Monday Dirty Dozen [CHART PACK] — l look at positioning in the options market versus direct, then we explore the possibility of the SPX entering an extended trading range, followed by good looking charts in precious metals as well as a few stocks, before ending with fiscal and US confidence.

The Perils of Too Much Information — I explore when too much information can be a bad thing and why the market tends to know more than we do.

A Record-Breaking Market — I discuss the big swing in sentiment we’ve seen over the last four months and the increasing signs of wild speculation + my base case for where I believe things are headed.

Articles I’m reading —

Take a few minutes and read through this twitter thread from hedge fund manager Dan McMurtrie talking about the coronavirus and its inevitable impact on the global supply chain. This is an issue I’ve been digging into and Dan does a terrific job of laying out the increasingly real risks that the market and global economy are facing. Here’s the link and a summary of his main points.

-

- We should expect at minimum two-quarters of severe supply chain disruption globally

- This risk increased significantly with news the virus is rapidly spreading across both Japan and Korea

- In China, we’re seeing the largest “containment/effective imprisonment via quarantine” in history. The economic impact of that is nearly impossible to model

- The ubiquity of Just in Time manufacturing and the non-linearity of supply chains mean there’s a leverage downside effect to where the hit to the economy is “not a 1 month hit. It’s not a 1 qtr hit. It’s an annual hit *right now*”.

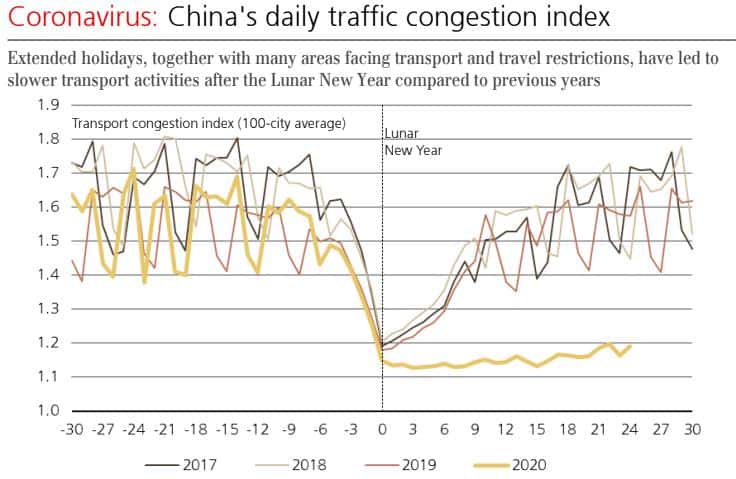

- Chinese rail traffic is still only 1-3% of normal and the widely talked about store reopenings are more forced propaganda than a meaningful change

The virus has now spread to every major continent excluding Antarctica and South America. Here’s a useful tracking app from Johns Hopkins which shows you the latest location, growth, confirmed, and death rates for the virus.

One of the major problems with trying to discount this event is that we have low fidelity data. So while China is reporting a slowing growth rate for the virus, simple statistical analysis shows that the numbers they’re giving us are almost certainly manufactured.

Barron’s pointed out this week that “A statistical analysis of China’s coronavirus casualty data shows a near-perfect prediction model that data analysts say isn’t likely to naturally occur, casting doubt over the reliability of the numbers being reported to the World Health Organization”.

Then there are the issues with testing and identifying the virus. It should be telling when a developed country such as Japan stumbles so badly in getting a jump on this thing, as Nomura’s Richard Koo recently pointed out:

“Despite numerous warnings from experts appearing on Japanese television, the Ministry of Health, Labour and Welfare waited until 14 February to announce a plan to allow those who had not traveled to China’s Hubei province to be tested for COVID-19. All the time, the virus was spreading.

“… Adding to the problems is the fact that the world’s third and fourth-largest economies — Japan and Germany—reported negative economic growth at the end of last year. When coupled with the further slowdowns expected in No. 3 Japan and No. 2 China as a result of COVID-19, the implications for the global economy and global supply chains are likely to be severe.”

Now think about what’s likely already going on in parts of Africa where only two laboratories on the entire continent have the capability to test for the virus.

Here’s some morel numbers:

-

- According to Goldman Sachs “The number of ‘missing workdays’ in China will be roughly equivalent to the entire US workforce taking an unplanned break for two months.”

- The airline industry just announces that it expects to see the first annual decline in global passenger demand in 11-years.

- Foxconn, a major supplier to Apple (AAPL) whom it’s estimated makes up roughly 50% of Foxconn’s numbers, just announced that Q1 revenues may be down by 45%.

The Science Journal Nature noted the extremely wide cone of probabilities that remain around the final damage of this virus, writing:

“Epidemiologists have been trying to estimate roughly when the outbreak will peak, so public-health officials can prepare hospitals and work out when it will be safe to lift travel restrictions in Wuhan and several nearby cities.

“Some models suggest that the climax will happen any time now. Others say that it is months away and that the virus will infect millions — or, in one estimate, hundreds of millions — of people before then. This model assumes that many more people have been infected than is reflected by official counts, but that these people have no symptoms or are not ill enough to seek medical treatment.”

Keep your head on a swivel. COVID-19 isn’t going away anytime soon.

Charts I’m looking at—

The domino effects of this are just beginning (chart via UBS).

Video I’m watching —

Here’s a short couple minute clip of the ever balanced Mohamed El-Erian giving his take on the virus’s impact on markets and the global economy (link here).

His quick take: Markets have been lulled into complacency and this complacency isn’t justified by the data.

Book I’m reading —

I just cracked this one open after I saw that @patrick_oshag recommend it. It’s about animal infections and human pandemics and why we should expect to see a significant rise in both in the coming decades. Fun stuff.

Here’s a cut from the book.

“Make no mistake, they are connected, these disease outbreaks coming one after another. And they are not simply happening to us; they represent the unintended results of things we are doing. They reflect the convergence of two forms of crisis on our planet. The first crisis is ecological, the second is medical. As the two intersect, their joint consequences appear as a pattern of weird and terrible new diseases, emerging from unexpected sources and raising deep concern, deep foreboding, among the scientists who study them.

“How do such diseases and raising deep concern, deep foreboding, among the scientist who study them. How do such diseases leap from nonhuman animals into people, and why do they seem to be leaping more frequently in recent years? To put the matter in its starkest form: Human-caused ecological pressures and disruptions are bringing animal pathogens ever more into contact with human populations, while human technology and behavior are spreading those pathogens ever more widely and quickly. There are three elements to the situation.”

Trade I’m looking at —

Okay, not exactly a trade recommendation. Just something to be aware of if you’re stuffed to the gills with some of the popular tech momo names. The Economist has a pretty good track record of ringing the bell at major turning points. But… and I want to stress this… momentum is still on their side and favors more upside. Don’t step in front of a freight train. Wait for the market to give a signal and a setup.

Quote I’m pondering —

A positive feedback is self-reinforcing. It cannot go on forever because eventually, market prices would become so far removed from reality that market participants would have to recognize them as unrealistic. When that tipping point is reached, the process becomes self-reinforcing in the opposite direction. ~ Geroge Soros

Watch for tipping points.

That’s it for this week’s macro musings.

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.