“In the United States problems of economic understanding have been compounded by the effect of economic prosperity. The Japanese in World War II spoke ruefully of shoribyo or ‘victory disease.’ The Greeks called it hubris, and thought that it always ended in the intervention of the goddess Nemesis. That lady makes her appearance when wave-riders begin to believe that they are wave-makers, at the moment when the great wave breaks and begins to gather its energy again.” ~ David Fischer, via The Great Wave

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at Friday’s reversal, dive into the inflation outlook, cover positioning in bonds and equities, discuss beaten-down gold miners, chat about the strong underlying action in semis, and end with a housing play with a large breakout, plus more…

Let’s dive in.

***click charts to enlarge***

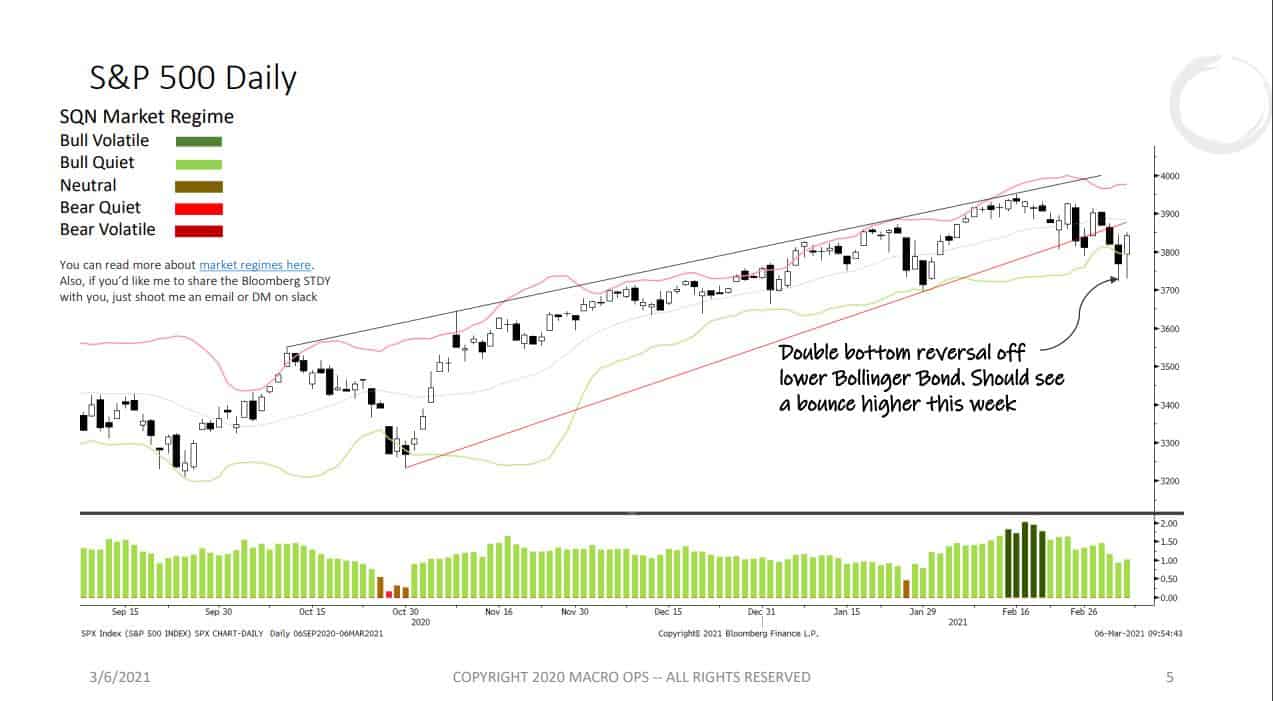

- The market put in a face-ripper or a bullish reversal Friday afternoon, surprising many, including your author who nearly managed to bottom tick the day on a short entry (fun stuff!).

This gives us a double bottom false breakout off the lower band on the daily timeframe. We should see further upside follow-through this week but stay on your toes cause if bonds don’t cooperate, things could continue to get squirrely!

- Our broader market take is the same as it has been for the last few months. Sentiment and positioning are stretched, trend fragility is high so expect occasional chop and vol like we’ve seen over the last couple of weeks. But, fiscal and economic recovery dominate so the path of least resistance is up.

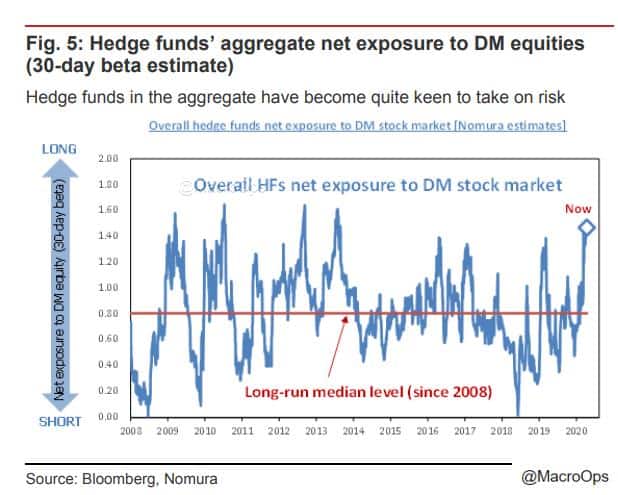

Nomura shows that hedge funds are starting to pile back into stocks after sitting on the sidelines for much of the last 10-months.

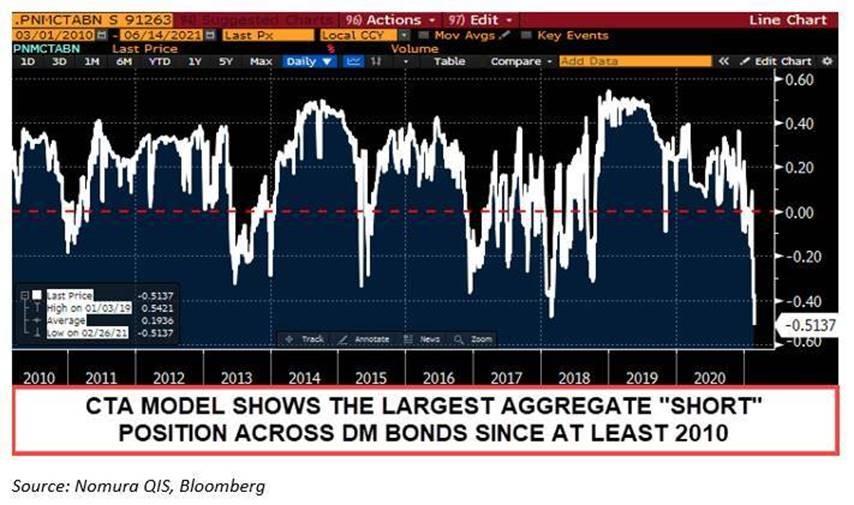

- Their CTA Model also shows the largest aggregate short position across DM bonds since at least 2010 (h/t @DriehausCapital).

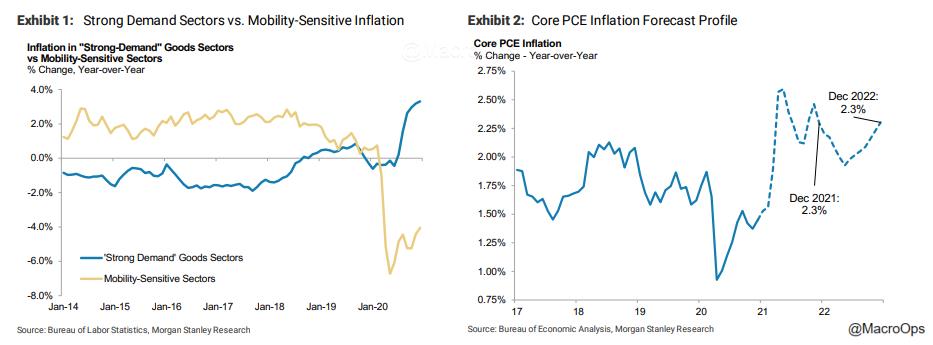

- Considering we expect both growth and inflation to run above consensus this year, the CTAs are probably right. Here’s Morgan Stanley summarizing their inflation forecast for the year, which we agree with.

“As reopening progresses, there are significant price adjustments to come in mobility-linked sectors of inflation, and that should come alongside goods inflation that remains elevated through mid-year as inventories and supply chains remain constrained. Not all pressures in 2021 are transient, and in 2022 inflation intensifies on a tightening labor market and robust levels of demand.”

- Continued: “The bulk of inflationary pressures this year will reflect transient developments driven by Covid-related distortions as economic activity begins to normalize. Multiple rounds of fiscal stimulus and excess savings provide a powerful tailwind of buying power that has been building among US households – ready to be deployed as the economy is reopening.”

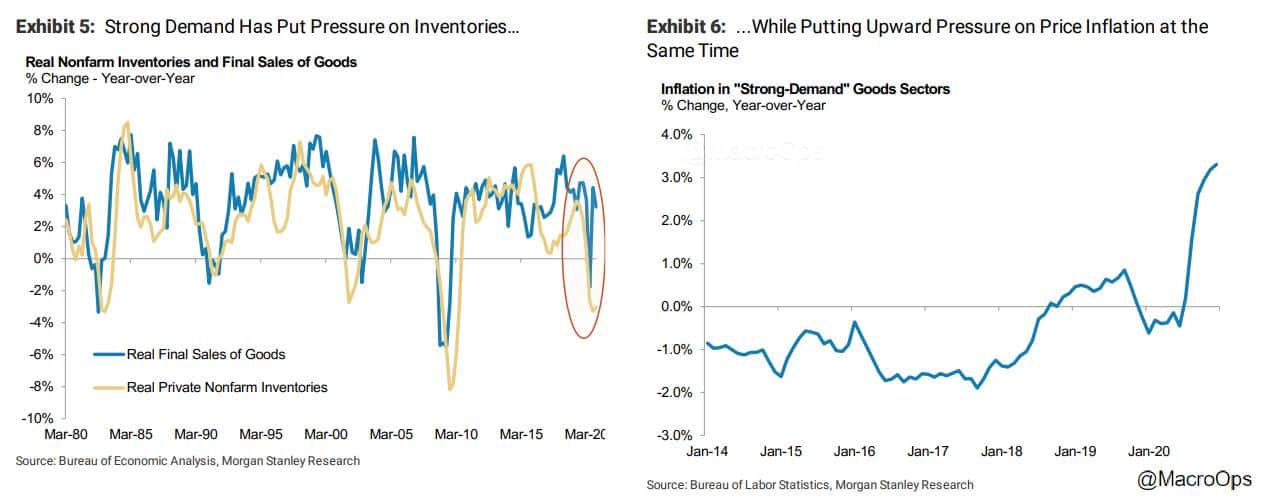

- And… “One Covid effect on activity has been to shift spending away from services and into goods sectors. As a consequence, in those areas where demand has accelerated, inflation has also accelerated. That has been exacerbated by the fact that strong demand for goods has led to lean inventories – evidenced by the fact that over the four quarters through 4Q20, the level of real nonfarm inventories was down 3%, while real final sales of goods were up 3.2% from a year earlier.”

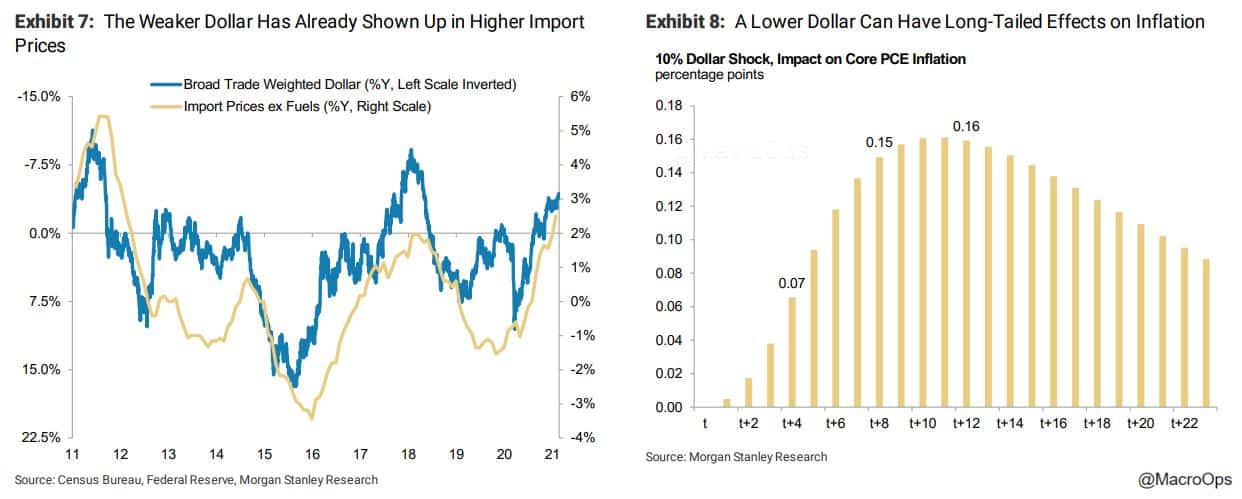

- Lastly, “In addition to inventory imbalances and demand shifts creating inflationary pressures in the goods space, there are additional tailwinds to inflation emanating from a lower foreign exchange value of the US dollar. Already the depreciation in the dollar over the last year has shown up in higher import prices, which will likely pass through the inflationary pipeline into consumer prices as well. While dollar impacts on inflation may also be seen as transient, they can have longer tails – a simple simulation of the effects of a 10% depreciation in the value of the dollar shows these effects can remain in place for a number of quarters.”

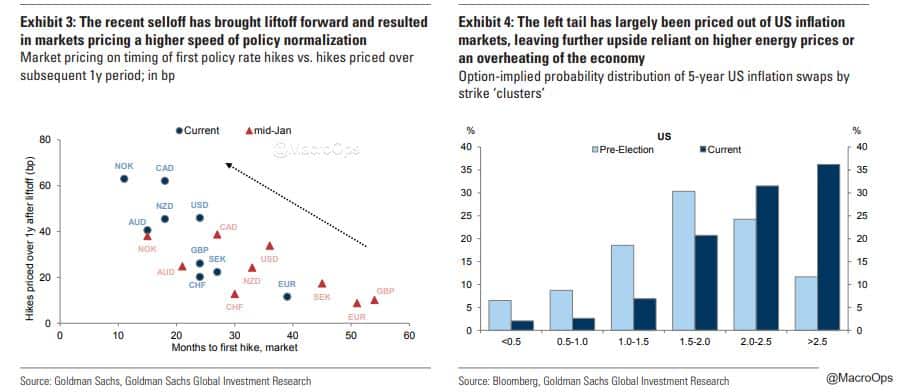

- The market is revising its Fed policy expectations by pricing in hikes earlier than what the Fed has communicated. This is creating a communication challenge for Powell and will eventually lead to increased market vol and/or force the Fed to make some changes to its messaging (chart via GS).

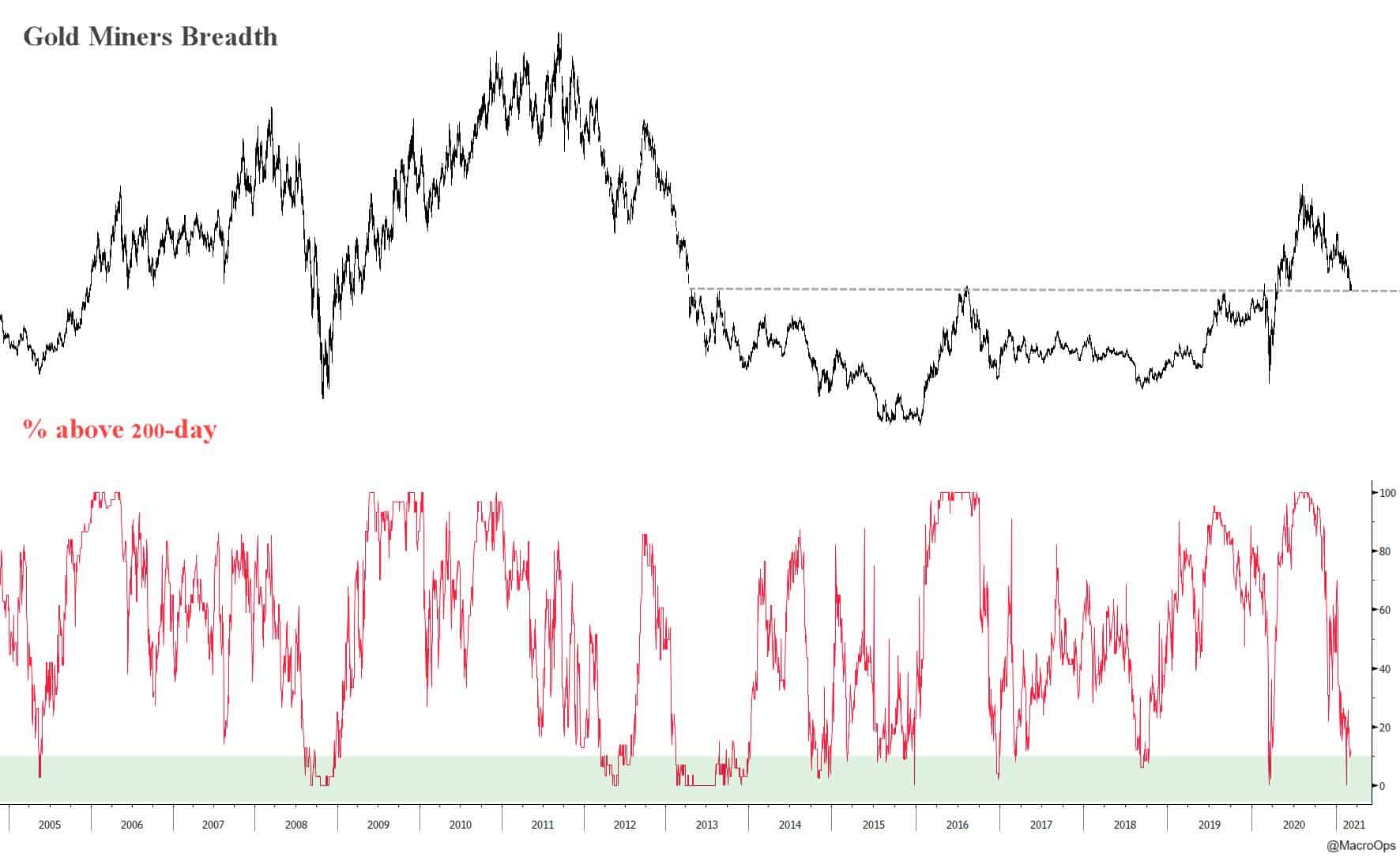

- With slightly above-trend inflation coming, it may soon be time to revisit precious metals, which have been hammered over the last 6-months. Only 12% of gold miners are trading above their 200-day moving averages currently. Breadth this bad tends to precede bottoms.

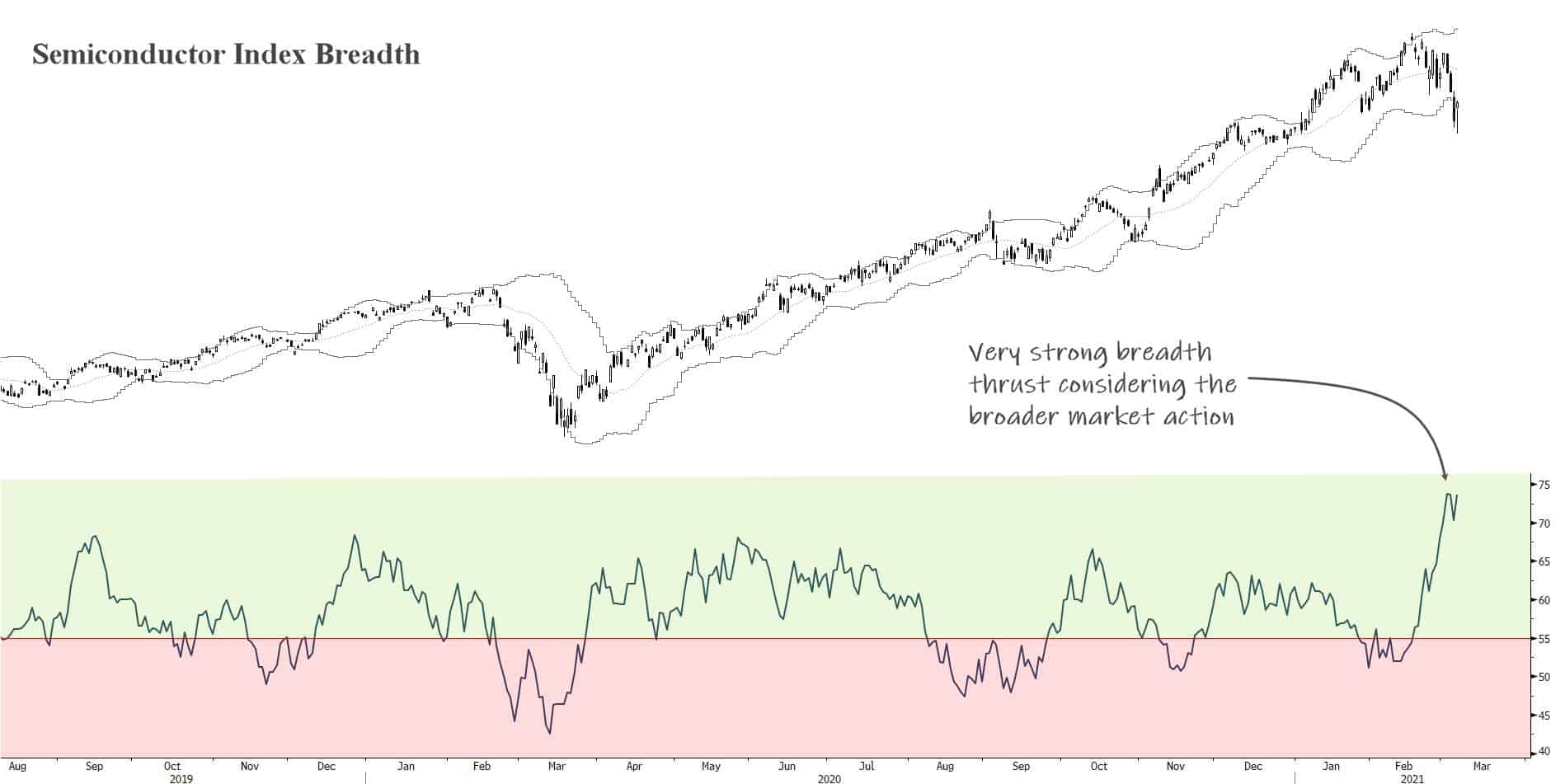

- Conversely, breadth in semis remains incredibly strong, especially considering the broader market action over the past few weeks.

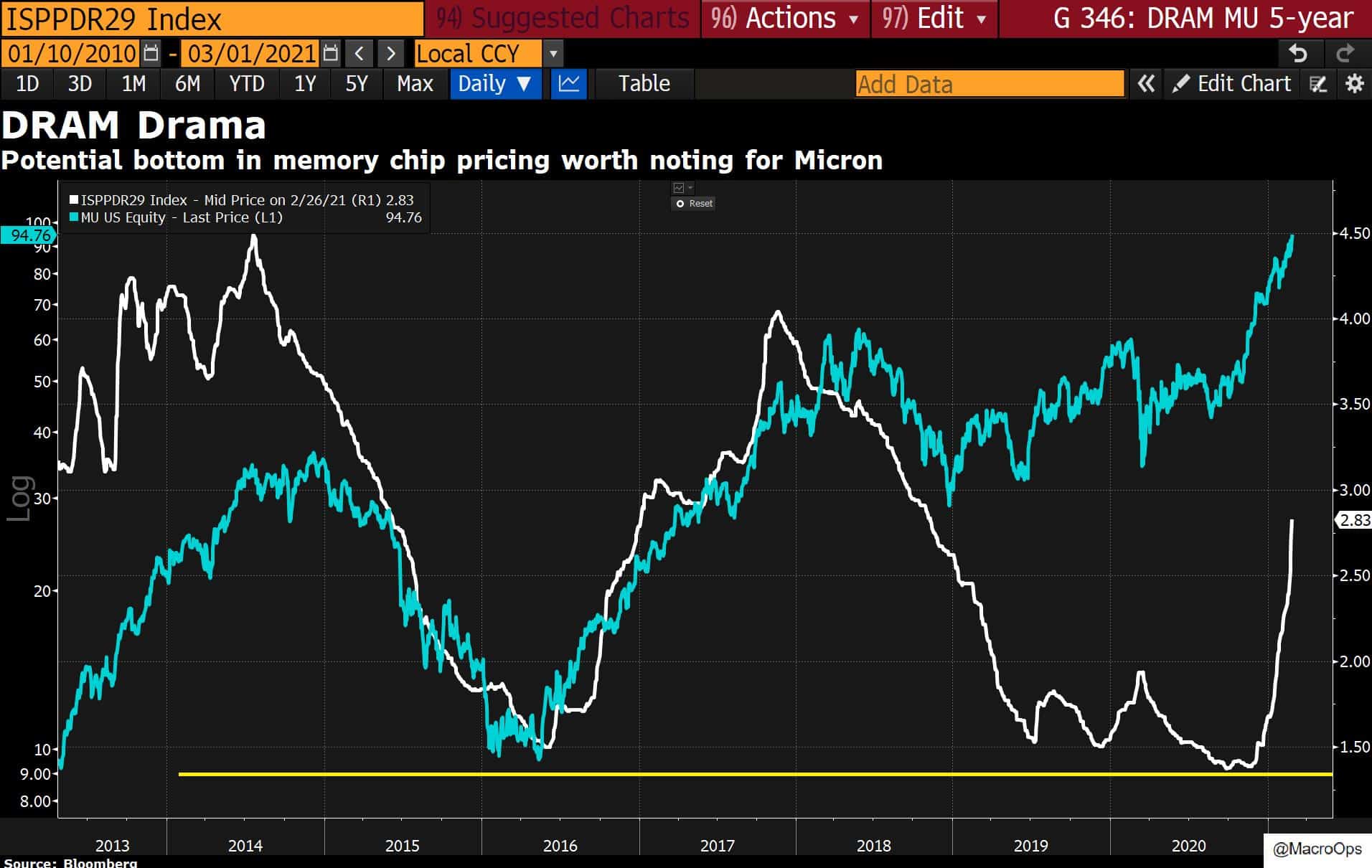

- I shared this chart months ago making the point that we’d likely seen the bottom in DRAM prices for the cycle. DRAM has gone vertical since and with the industry’s secular tailwinds, this trend is only getting started… You can read our secular bull semiconductor & MU thesis here.

- We continue to like the housing sector at MO. Cavco Industries is an interesting play on this theme. The company produces manufactured homes as well as providing financing. Its chart is a beaut with the stock breaking out of a 3-year wedge.

Collective members can find the bullish housing report we wrote up last year in the library.

Stay safe out there and keep your head on a swivel.