I don’t believe in edge. I think it’s a fairy tale. The world is too competitive. Going back to AI, investing is where chess was in 1996, when there was an enormous race between human grandmasters and algorithms, and Deep Blue started to beat Garry Kasparov by using brute compute force. Welcome to the deep dive on Micron Technologies (MU).

The above is from this interview with Gavin Baker, one of the smartest tech investors in the game. Gavin covers a number of interesting topics: everything from tech’s scale and enduring high returns on invested capital (ROIC), to the increasing efficiency of the market and how that affects one’s ability to generate alpha. Here’s the rest of his remarks on how he thinks about edge in today’s market (emphasis by me).

Today, that’s why value strategies have stopped working: Value investors used to have an edge. They were very quantitative. Maybe, they had a strong stomach and were willing to buy companies because they were cheap no matter how bad it sounded. But the problem is that anything that can be put in a spreadsheet will no longer generate alpha because it has been arbitraged away by quant investors. There is so much quantitative money chasing those same metrics.

To me, all alpha comes from insights. An insight is kind of a differentiated long-term viewpoint about a stock. It’s a differentiated view about the long-term state of the world. Often, these insights are very simple, and a lot of them are right brain: imaginative, being slightly better in seeing the future states of the world. These insights need to be grounded and tested in reality regularly. Also, it pays to boil them down to just a few variables. Like Occam’s razor, the injunction not to make more assumptions than you absolutely need, simple is beautiful when it comes to investing. With electric vehicles for instance, all that matters is efficiency: battery capacity and range to get miles per kWh. You want to focus on the variables that are important instead of the variables that are interesting.

Anything that can be put in a spreadsheet will no longer generate alpha… all alpha comes from insights… an insight is kind of a differentiated long-term viewpoint about a stock [or] about the long-term state of the world… Like Occams’ razor, the injunction not to make more assumptions than you absolutely need…

Let’s go through each of these one by one.

Anything that can be quantified will be arbitraged…

We live in a world of alternative data where satellites provide real-time updates on retail parking lot traffic and detect when manufacturers are adding or reducing shifts… drones beam infrared signals at oil-storage tanks to gauge inventory levels… credit card and point of sales system data tracks consumer spending in the here and now and is available for anybody with the money to pay for it.

The market has become hyper-efficient at correctly pricing in the near future, with iterative changes to prices occurring in nanoseconds as billions of new data points come down the feed and into the brain’s of our silicone overlords.

Knowing this, it’s okay to chuckle when you hear someone pitch the bull case for “company X” because of “their low relative price-to-book and a belief that next quarter’s consensus estimates are a bit low, yada yada yada…”

These peeps are playing the wrong game. They’re up against Deep Blue but think they’re still playing Bud from across the street.

This doesn’t mean the game is over for us simple-minded skin bags. Like Gavin says, we just have to extend our analysis into the future some. Peer beyond that thick veil where quantitative data doesn’t exist. And operate in the space where things must be intuited, gamed out, and probabilistically weighted.

The idea isn’t new. It’s just perhaps more true than before. Legendary hedge fund manager Michael Steinhardt played this game over 30-years ago and talks about it in his book, No Bull (again, emphasis by me):

I defined variant perception as holding a well-founded view that was meaningfully different from market consensus. I often said that the only analytic tool that mattered was an intellectually advantaged disparate view. This included knowing more and perceiving the situation better than others did. It was also critical to have a keen understanding of what the market expectations truly were. Thus, the process by which a disparate perception, when correct, became consensus would almost inevitably lead to meaningful profit. Understanding market expectation was at least as important as, and often different from, fundamental knowledge.

… A summer intern reminded me years later of the advice I had given him on his first day at work. I told him that ideally he should be able to tell me, in 2 minutes, four things: (1) the idea; (2) the consensus view; (3) his variant perception; and (4) a trigger event. No mean feat. In those instances where there was no variant perception – that is, solid growth recommendations within consensus – I generally had no interest and would discourage investing.

I’m reminded of another recent killer interview I listened to. This one being Patrick O’Shaughnessy’s chat with the anonymous twitterer @modestproposal1. Modest Proposal told Patrick about an idea he’d been mulling over for years that had finally begun to crystalize. He refers to it as his Two Different Theories for Investing: Underwriting the past and underwriting the future.

-

- Underwriting the past involved looking quantitatively at historical performance and trying to focus on business fundamentals irrespective of a view on the future. Investors who underwrite the past want as much certainty as possible.

- Underwriting the future is more qualitatively focused and requires an investor to be comfortable with uncertainty as they build a view on the future of a company through strategic analysis. The best-performing investors over the past 20 years belong to this group.

Whatever we choose to call it; a differentiated long-term viewpoint, variant perception, or strategic analysis/underwriting the future, etc… It’s the critical factor in assessing the expected value of a long-term discretionary bet. Forget about what next quarter’s earnings will look like or where margins will be later this year… That game is over. The robots won. Time to move on…

Looking out into the future is hard though. It’s complex. It’s important to not get lost in the sauce. This is why Gavin’s bit about not making more assumptions than you absolutely need is key. Occam’s Razor and keeping your analysis as simple as can be but no simpler… is a concept that’s near and dear to our hearts here at MO.

The Chandler Brothers (the greatest investing duo many have never heard of) are perhaps the best in the world at this. They have an incredible knack for cutting through the web of intellectual mental masturbation that snags most. They know how to go straight to the meat, often employing what they call “creative metrics” in instances when standard data serves as more of a distraction than an informative input.

But getting back to underwriting the future…

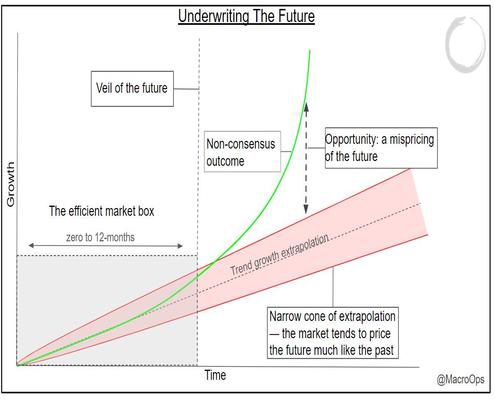

Here’s a nifty illustration of what this looks like.

The market is hyper-efficient within the 0 to 12-month timeframe or what I call the efficient market box. Now, yes, of course, there are exceptions. Efficiency turns to silliness when reflexive processes loop us away from anything resembling a probable outcome. The majority of the time though these feedback loops abort before they can really get started.

Looking out past the veil of the future is where things get interesting. And that’s where we should do most of our thinking.

The market tends to simply extrapolate the present well into the future. Whatever the trajectory of growth, competitive advantages or disadvantages, addressable market size, etc… is today, largely comprises the expectations that are embedded in the price.

This mostly works which is why it’s so. Betting on trend continuation and mean reversion around that trend is statistically a good bet, whether we’re talking about actual market prices or fundamental trends.

Occasionally though, large mispricings occur. The market bets on future trend continuation but instead we see wildly divergent outcomes. Why is this?

Here are a few reasons…

-

- The market is slow to recognize competitive advantages as well as underappreciate its impact on future value creation

- The market tends to underweight the impact of secular macro shifts while overweighting cyclical ones

- The market is inefficient at pricing anything exponential

The stock we’re going to talk about today benefits from all three. The company is Micron Technology (MU). A global supplier of DRAM and NAND semiconductors.

Most people don’t associate a semi company such as Micron Technologies with having a competitive advantage. That’s because the space has long been marked by cyclicality and weak margins. But this is changing due to consolidation and a slowing of Moore’s Law.

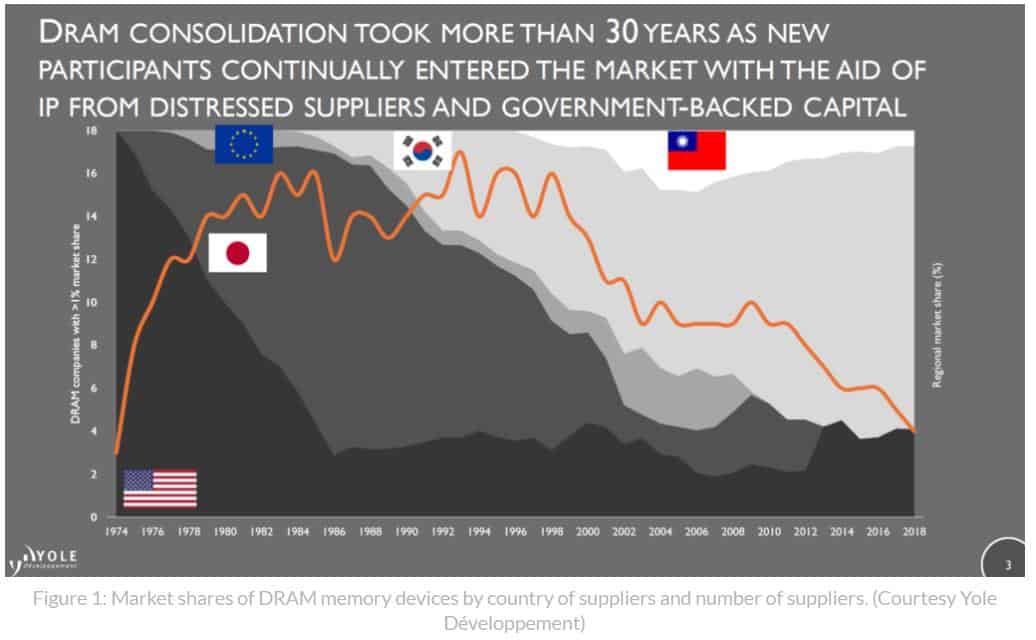

Take the DRAM market for example (approximately 75% of MU’s revenues come from its DRAM business).

Making DRAM used to be a poor business. There was a LOT of competition, with many competitors fueled by cheap government money. This equated to an extreme capital cycle of oversupply leading to painful busts and a firm ceiling on margins.

This competitive landscape has dramatically changed though. Since 2010, the industry has consolidated from 8 large DRAM makers to only 3 today (see orange line).

The DRAM semis oligopoly now consists of just Micron, Samsung, and SK Hynix. A similar consolidation has occurred in the NAND space as well.

This consolidation was driven mostly out of necessity. The reason being is that Moore’s Law — the doubling of transistors on a microchip every two years — has become prohibitively expensive to maintain and may be slowing all-together.

Suppliers were forced to scale to remain competitive. This has improved the industry’s fundamentals. The oligopoly has brought more prudent supply growth along with rising and stable margins.

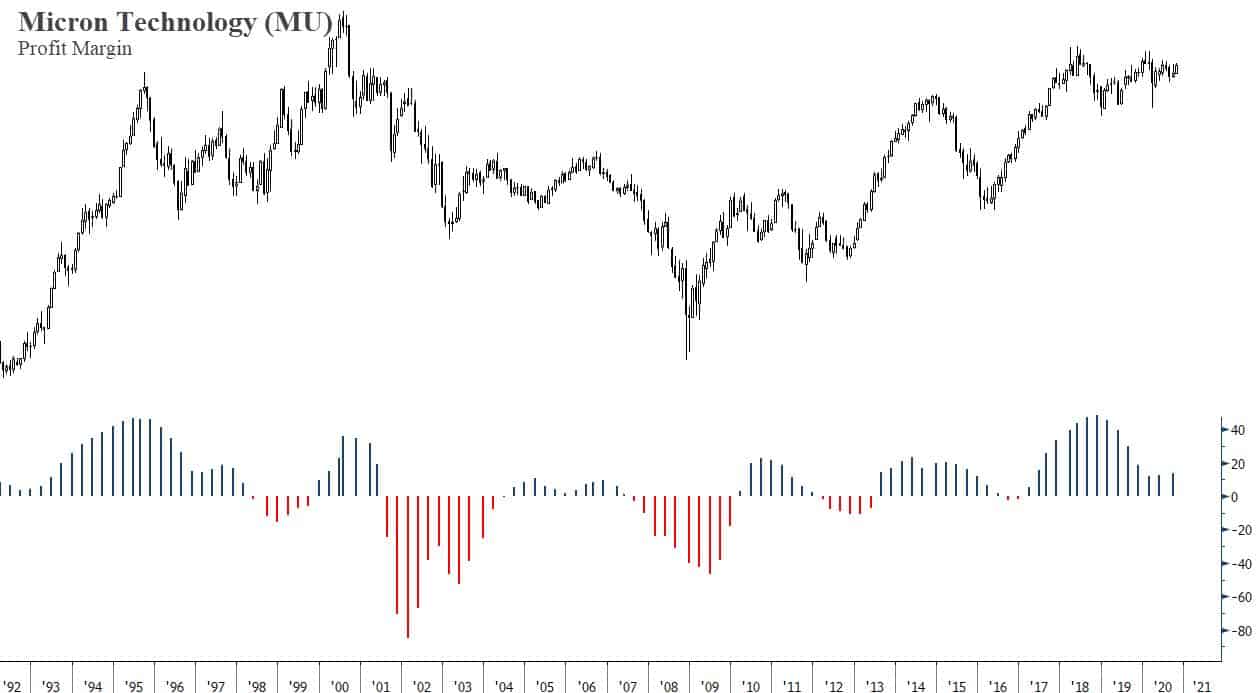

We can see this clearly in the data. Micron was able to remain profitable during the most recent industry downturn that began in 19’ — even amid the pandemic, the company generated a positive $2.83 in EPS. That’s a first in the company’s history.

Due to the above factors, Micron now sees 45% gross margins as an average for itself and the industry over cycles. That’s a significant improvement when compared to the past when the company often saw peak cycle margins in the low to mid-30s.

Secular macro tailwinds.

This is something we’ve been talking about for the last two-plus years and which Brandon has been covering in a recent group of writeups (here and here). So I won’t belabor the point. But suffice it to say, we believe semis are where the oil industry was in the early 2000s. China’s massive leveraging cycle was just getting started and this created a super-cycle for E&Ps.

But instead of a leveraging China, we have the rise of AI/ML, hyper-scale data centers, IoT, AR/VR, autonomous vehicles, etc… driving an increasing secular demand for silicone. As a result, data and compute power are the new black gold.

Here are a few bullet points:

-

- While Moore’s Law scaling challenges have shifted more of the burden (and value) to software, AI changes the paradigm because 1) compute matters again and there are little to no scaling limitations to the problem set (the more data, the better the outcome), and 2) creates a new virtuous demand cycle, much like the combustion engine did for oil. With cloud, compute has been centralized but there are still limited feedback “loops” to PCs and smartphones. AI creates a new feedback “loop” and should push more compute intelligence to the edge for key mobile and automotive applications in particular. ~ UBS

- AI servers will require six times the amount of DRAM and twice the amount of SSDs compared with standard servers. ~ Micron CEO Sanjay Mehortra

- 90% of the data available in the world today was generated in the last 2 years – and it is expected to grow to 180 zettabytes (that is 21 zeros) by 2025. To put a zettabyte into context, storing just one requires 1,000 data centers, or about 20% of the land area of Manhattan. ~ Westfield Capital Management

- Market forecasters estimate the AI-enabled market (defined as direct hardware, software, and services sales) can grow from $6 billion in 2017 to approximately $36 billion by 2025; Micron is well positioned to capitalize on this.

- According to Intel CEO Brian Krzanich, a single autonomous vehicle will generate and consume 40 TB of data for every 8 hours of driving and 1 million autonomous cars will generate as much data as 3 billion people

- According to Gartner, driverless cars contain over 80 GB of DRAM versus 5.5 GB in PCs and 2.5 GB in handsets, exemplifying the sharp increase in the memory demands of these emerging technologies

This can get a bit confusing with all the NAND, DRAM, zettabytes, and such… The key point here is that we are moving into an increasingly compute-heavy world.

In the past, semis ebbed and flowed with the rise and fall of PC and mobile phone demand. But AI and the IoT is going to pervade every aspect of our lives… at an increasing rate. AI works by brute force. The more data it has to train on, the better it becomes. The need for computing power is only going to accelerate from here, exponentially so. The fact there are only a few companies (Micron) in the world, an oligopoly, with the engineering ability to create the foundational tech that’s essential to this growth… and one of them, Micron, trades at just 7x normalized earnings, is mind-blowing…

Below is a monthly chart of Micron. The stock has been coiling tightly for over 2-years. Extreme compression regimes like these tend to precede expansionary regimes (massive trends).

The sentiment and general narrative around the stock are as to be expected. People are focusing on the short-term cycle, worried about narrowing margins over the next quarter or two, as well as the company’s exposure to China.

What they fail to see is that Micron is only one of three companies in the world that’s able to produce a component that’s increasingly critical to the AI stack. And it’s the only one based in the US…

They’re not looking past the veil of the future and seeing that AI and IoT are going to become increasingly integrated into every aspect of our lives. And that this secular shift will support steady exponential demand growth, which will further reduce the cyclicality of a once very cyclical industry, which should lead to a rerating of industry multiples and ipso facto, a significantly higher stock price.

Now, there’s a number of ways to play this. One, we can put on a straight long position in Micron. Or two, we can buy some deep out of the money calls (DOTMs). You can currently find Jan 2022 10-delta calls with a $100 strike trading for a buck.

We’re going to do a combo of the two and will put out a trade alert, likely later this week, when we do.

Stay safe and keep your head on a swivel!