When a new bull market is launched it is *not* typically widely accepted or believed at the outset. A new bull market needs a “wall of worry” to climb. So rather than cheering for a Fed Pivot, sentiment should turn deeply skeptical of the Fed’s efforts: “The Fed will be pushing on a string” rather than “Yippee; the Fed Pivot is just around the corner.” ~ Legendary technician Walter Deemer via this thread.

In this week’s Dirty Dozen [CHART PACK], we look at an overly optimistic consensus, the best seasonality indicator, a bad macro regime = bad forward equity returns but a spike in put/call = a short-term bounce, a cyclical peak in the US dollar and a decade long pattern in gold, plus more…

**Note: Due to a number of you shooting us emails post enrollment close we’ve decided to extend our enrollment to the Macro Ops Collective for another week until Sunday, January 8th. Don’t hesitate to shoot any Qs my way. Looking forward to seeing you in the slack!

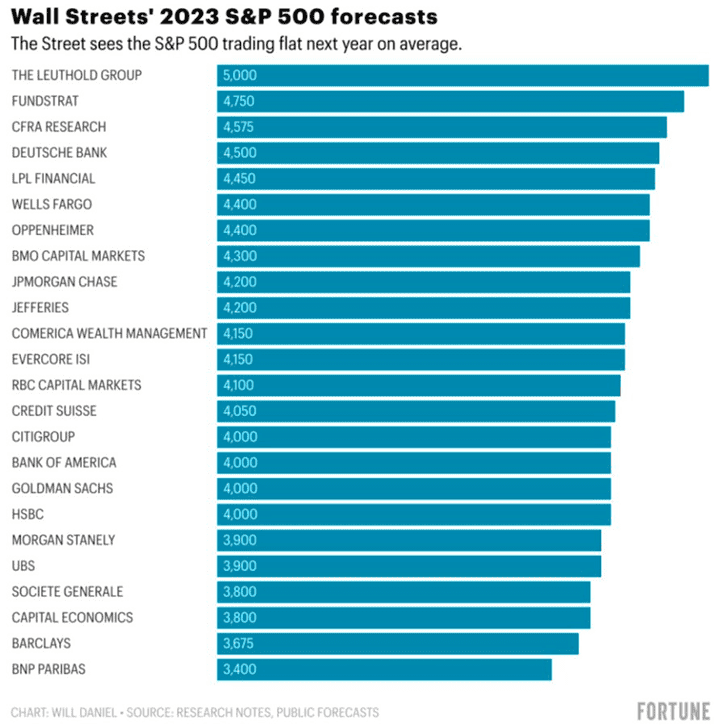

- 20 out of 24 shops are predicting a bullish year for the SPX in 2023. The four that are bearish are only mildly so.

Reminder: In 22’ the median end of year target for the SPX was 4950…

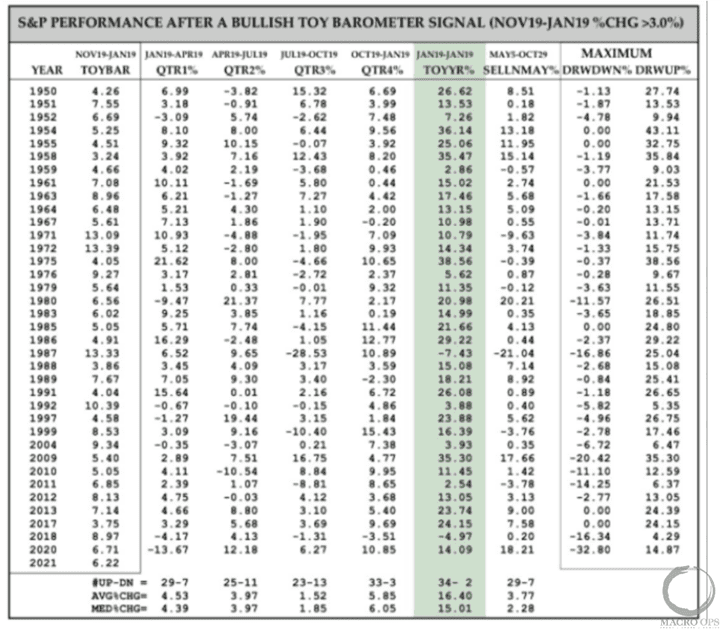

- The TOY seasonality indicator built by the OG quant Wayne Waley via Finom Group (link here):

“He considers the TOY Barometer to be the single most reliable seasonality barometer of forward stock market returns, so much so that he’s said if he could only make one trade/year based on one indicator, this is the indicator he would use. TOY is an acronym for Turn. Of. Year. The seasonal dates it tracks is from November 19 to January 19 of a new calendar year, hence turn of year.

“What he found was there was a high correlation between the S&P 500’s returns between November 19th and the following January 19th and the S&P’s performance the 12 months following January 19… The 36 completed bullish signals have led to gains 34 times the following 12 months.”

Let’s see what the next two weeks bring, shall we?

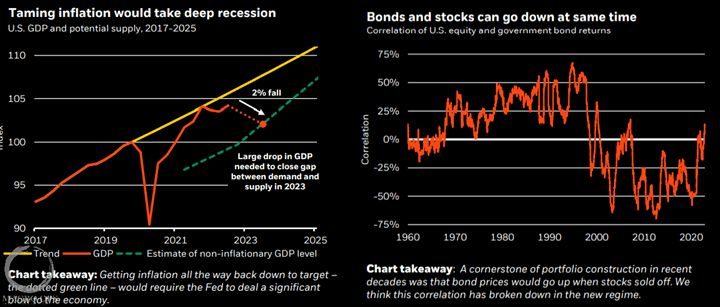

- Two very important charts from BlackRock’s 2023 markets preview (link here). Here’s some color from the report with emphasis by me:

“Central bank policy rates are not the tool to resolve production constraints; they can only influence demand in their economies. That leaves them with a brutal trade-off. Either get inflation back to 2% targets by crushing demand down to what the economy can comfortably produce now (dotted green line in the chart), or live with more inflation.

“For now, they’re all in on the first option. So recession is foretold.” And “the negative correlation between stock and bond returns has already flipped, as the chart shows, meaning they can both go down at the same time. Why? Central banks are unlikely to come to the rescue with rapid rate cuts in recessions they engineered to bring down inflation to policy targets. If anything, policy rates may stay higher for longer than the market is expecting.”

We are in agreement with the above.

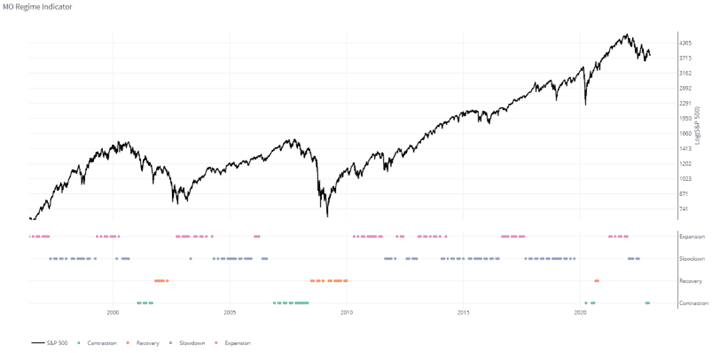

- Our spanking new Macro Regime Indicator (a measure of the slope and RoC of 11 different econ, market, financial data points) has been in a Contraction regime since the start of October and a Slowdown regime since Jan 1st. Contraction regimes have the worst historical equity returns by far. Recessionary bear markets occur in Contraction regimes. Our Liquidity indicator tells us that we should expect this regime to last another 6-months

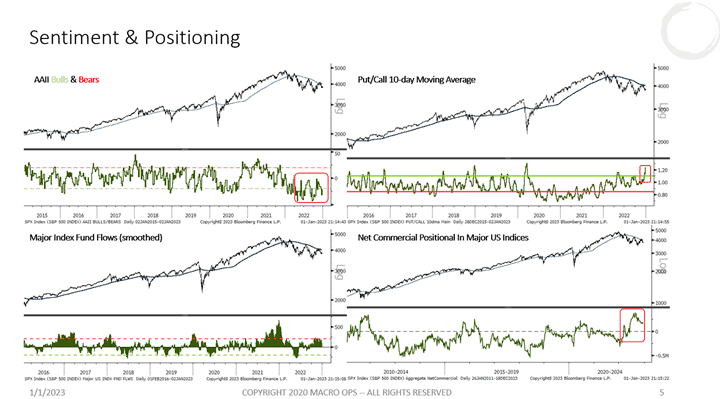

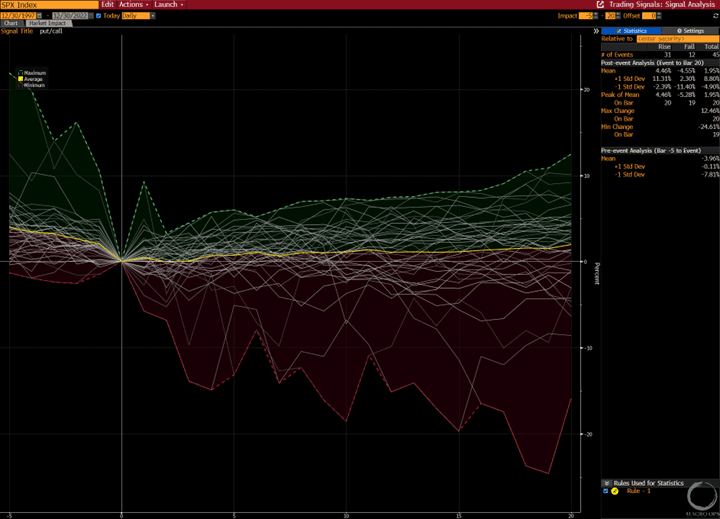

- But if you’re looking for tactical longs then we’ve got a decent setup here with a large spike in the Put/Call 10dma (top right chart), high commercial long positioning, and a bearish AAII.

- There have been 45 of these setups over the past 25-years. 31 ended up positive over following 20 trading days with an average gain of +4.46% versus an average loss of -4.55%.

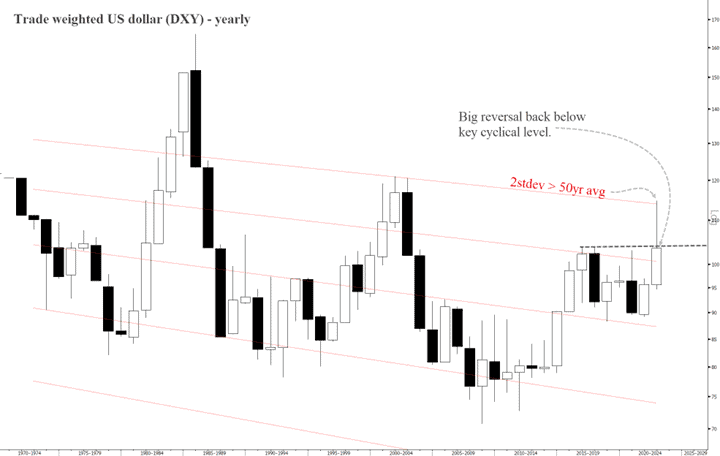

- I like to routinely pull back and look at the long-term charts, the monthly, quarterlies, and yearlies to get a good visual on where the broader trends are pointing.

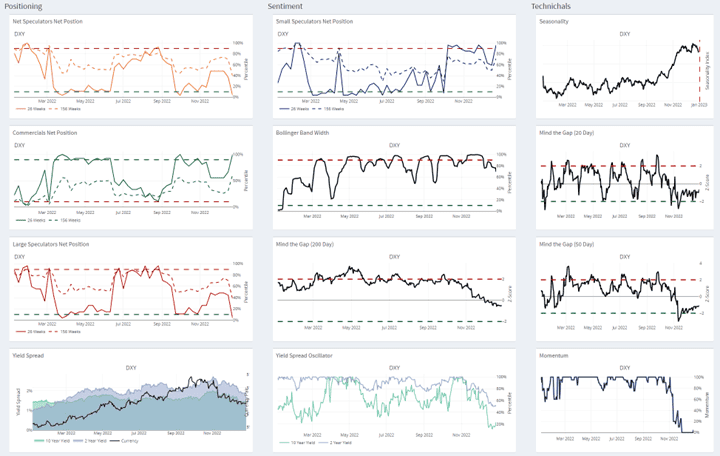

Here’s a yearly chart of the trade weighted dollar (DXY). At the start of the year we saw the DXY spike 2std above its 50-year average, before sharply reversing back below its significantly cyclical high level. This is a large bear trap and suggests the cyclical top is in on DXY.

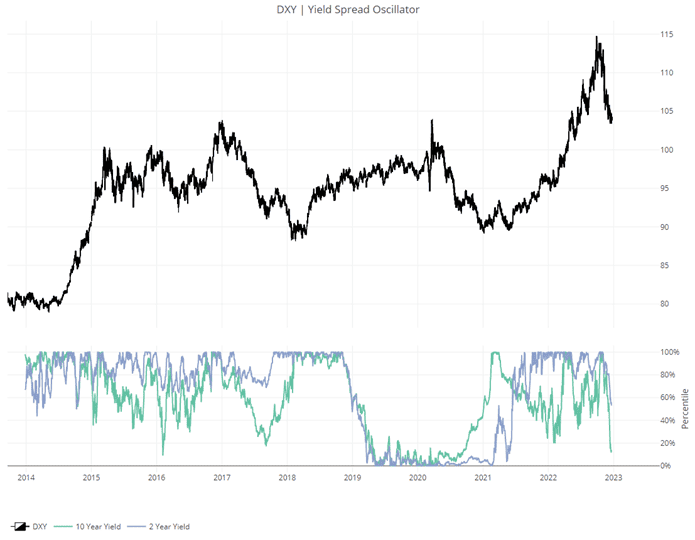

- The reason for this strong reversal? Two things (1) we saw yield spreads reverse against the USD. Below is our Yield Spread Oscillator which tracks the DXY’s aggregate yield spread momentum. It flipped negative in the Fall and (2) high capital concentration in the US megacap techs that is now reversing, causing money to flow from the Core back out to the Periphery. We wrote about why this was inevitable here.

- Using our mutlichart tool for DXY, we can see that long-term net spec positioning is neutral, momentum is in its lowest percentile, it’s just now entering its worse 2-months of seasonality. But, on the bright side, it’s close to 2std below its 20 and 50 day moving averages, so we should see some reversion/consolidation soon.

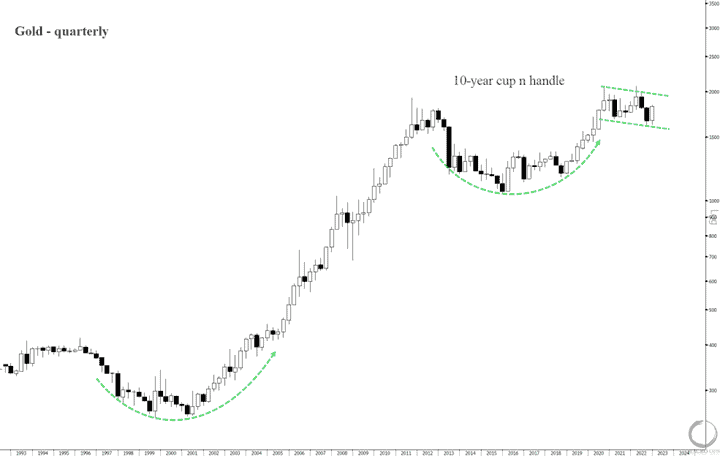

- You know what macro asset has the best historical returns in a Contraction regime? That’s right, gold and silver. Bullish PMs continue to be our highest conviction bet looking out over the next 1-2 years.

Here’s a quarterly chart showing the decade long cup n handle pattern for gold.

- Net spec positioning is in the 14% percentile (it hit the 1st %tile in Nov). And it’s entering is strongest period of seasonality right now.

- A large cap miner with one of the strongest momentum profiles throughout 2022 is Eldorado Gold (EGO). The chart below is a monthly.

We’ll continue to add to our PM basket as technical opportunities arise.

**Note: Make sure to sign up for the Macro Ops Collective today. The Collective is our premium service that offers institutional-level research, proprietary quant tools, actionable investment strategies, and a killer community of dedicated investors and fund managers from around the world. Enrollment will remain open until Sunday, January 8th at midnight.

Thanks for reading.

Stay frosty and keep your head on a swivel.