At any moment of time there are myriads of feedback loops at work, some of which are positive, others negative. They interact with each other, producing the irregular price patterns that prevail most of the time; but on the rare occasions that bubbles develop to their full potential, they tend to overshadow all other influences. ~ Soros

Markets, like much of nature, are composed of infinite feedback loops.

Understanding these feedback loops was one of Soros’ big analytical edges back in his prime. They’re a critical component of his theory on Reflexivity and also formed the foundation of his framework for analyzing currencies.

In this note, we’re going to explore the primary feedback loops at work in the US dollar. We’ll do this using Soros’ “currency equation”. And in doing so, we’ll see how the long-term USD bull trend is near the end of an unsustainable Core Domination paradigm. One that is ripe for reversion to the mean…

Let’s start with a review of the basics.

Like all markets, exchange rates are driven by supply and demand. Currency supply and demand can be separated into two broad categories: fundamental and speculative.

Fundamentals are things like the trade and balance sheet of the currency issuer and its fiscal and monetary policies, such as its budget deficits and its control of the money supply.

Speculative demand is centered around expectations of the relative and future value of the currency. Think exchange rate trends, interest rate differentials, and relative market opportunities.

To simplify even further. Currency supply and demand is comprised of three things:

-

- Trade

- Non-speculative capital transactions

- Speculative capital flows

Trade affects exchange rates through the balance of trade. Countries sell goods in their home currency. For other countries to buy those goods, they have to exchange their currency for the seller’s (exporter’s) currency. And vice-versa for when the country wants to import goods. This differential is referred to as the balance of trade. A trade surplus is an appreciating force on a currency and a deficit is a depreciating one.

Speculative capital flows are the buying and selling of currencies with no attached underlying asset.

Speculative capital moves in search of the highest total return. The total return is made up of:

-

- Exchange rate differentials

- Interest rate differentials,

- Local currency capital appreciation.

Of the three, exchange rates are the most important because they tend to fluctuate more than interest rates or relative market returns. It doesn’t take much of an exchange rate decline/increase to completely overshadow the return on interest rates or capital appreciation.

In the short-term (months to a few years) exchange rates are driven by speculative flows. In the long-term, economic fundamentals (trade + non-speculative capital transactions) dominate exchange rate movements. It’s the dynamic tension between these two that comprise the trends and fluctuations of currency markets.

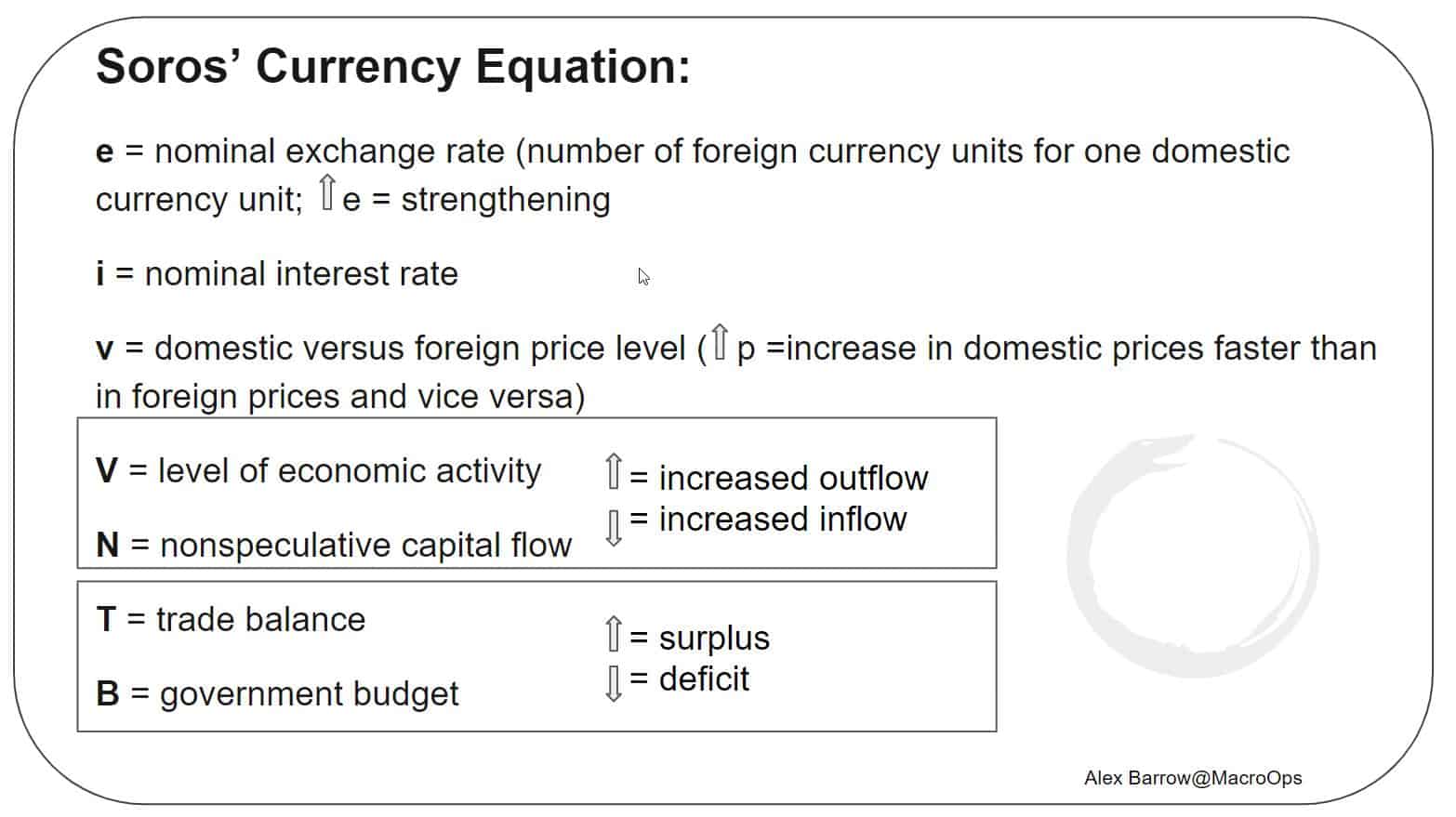

Soros broke these factors down so he could turn them into simple logic statements (the below example is taken from his book The Alchemy of Finance). He did this in an effort to gain a better understanding of the drivers of a trend and the sustainability of that trend.

The importance of these drivers shifts over time, from regime to regime. This is one of the reasons why the FX markets are notably hard to forecast. Players are often keying off the thing that worked during the last cycle while unaware of what’s driving the current one.

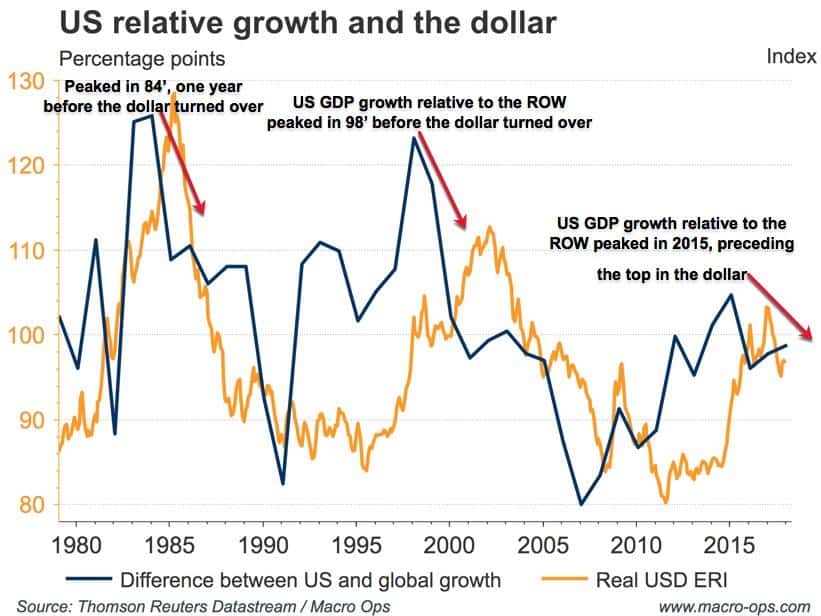

The most recent USD bull market that kicked off in 11’ was driven by an equation that looked something like this.

DXY = US V > RoW V (rest-of-world) = ↑(i+e+m) → s↓ → e↑

Where US growth was stronger on a relative basis (accounting for the US safety premium) than growth in the RoW (US V > RoW V). This led to positive interest rate differentials for the dollar which drove exchange rate appreciation and brought in speculative flows (s) into US assets (stocks + bonds). This drove relative US market outperformance (m).

As a result, the dollar benefited from numerous positive feedback loops that boosted its Total Return Equation, which again, is the most important factor in driving speculative flows.

But here’s the thing… A number of these factors are no longer supportive of the positive USD feedback loop; such as relative growth, yield spreads, and recently, the trend in the exchange rate itself.

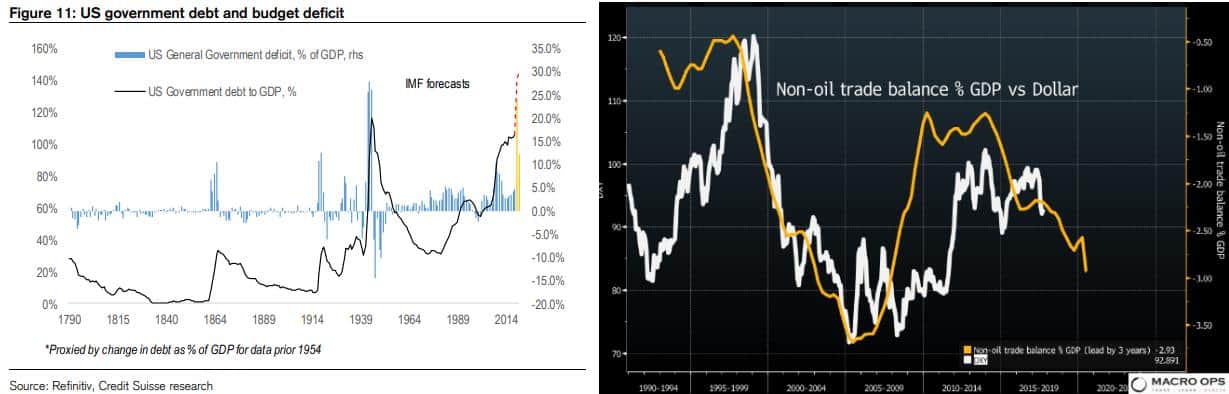

In addition, there are a number of longer-term fundamental factors, such as a deteriorating trade balance (T↓) and widening budget deficit (B↓) that are actively working against it.

So now the DXY equation looks something a little more like this:

DXY = ↕(i+e)+↑(m)→ s↕ → e↕

Where the now dollar only has relative market performance (m) working in its favor.

Reflexive processes tend to follow a certain pattern. In the early stages, the trend has to be self-reinforcing, otherwise the process aborts. As the trend extends, it becomes increasingly vulnerable because the fundamentals such as trade and interest payments move against the trend, in accordance with the precepts of classical analysis, and the trend becomes increasingly dependent on the prevailing bias. Eventually, a turning point is reached and, in a full-fledged sequence, a self-reinforcing process starts operating in the opposite direction. ~ Soros

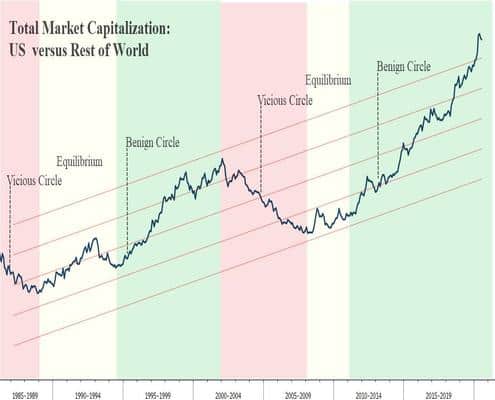

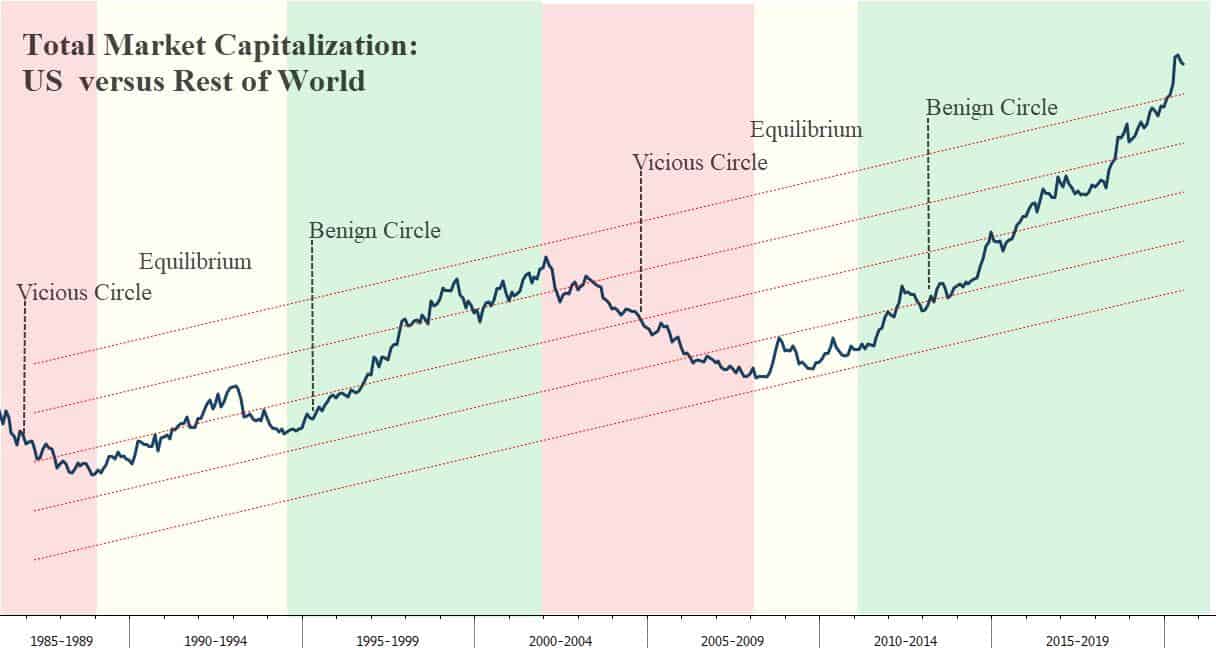

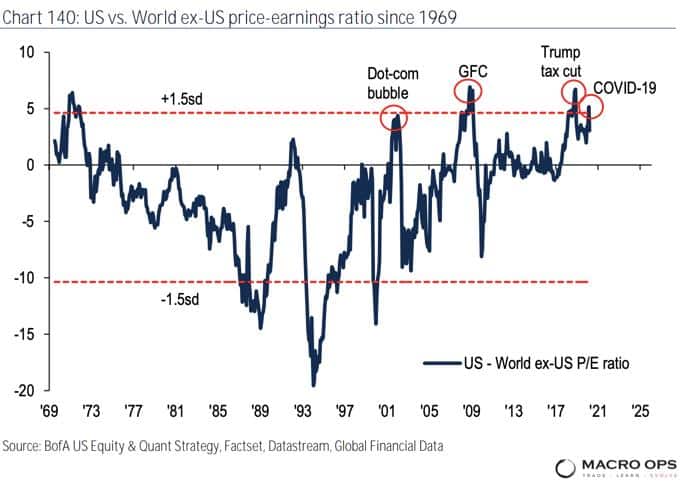

And as we can see in the chart below, this sole-remaining USD bull pillar of relative market performance is historically stretched.

(Note: Benign Circles in the US are characterized by low inflation, an easy Fed, a strong dollar, and US outperformance. While US Vicious Circles are marked by above-trend inflation, a weak dollar, and US underperformance.)

This is one of those things that means little in the short-term but a lot in the long-term.

The fact is that capital concentration is likely near its zenith here in the US. The valuation premium placed on US financial assets is over 1.5std above its long-term average. And it now no longer has the supportive tailwinds of positive growth, yield, or exchange rate differentials.

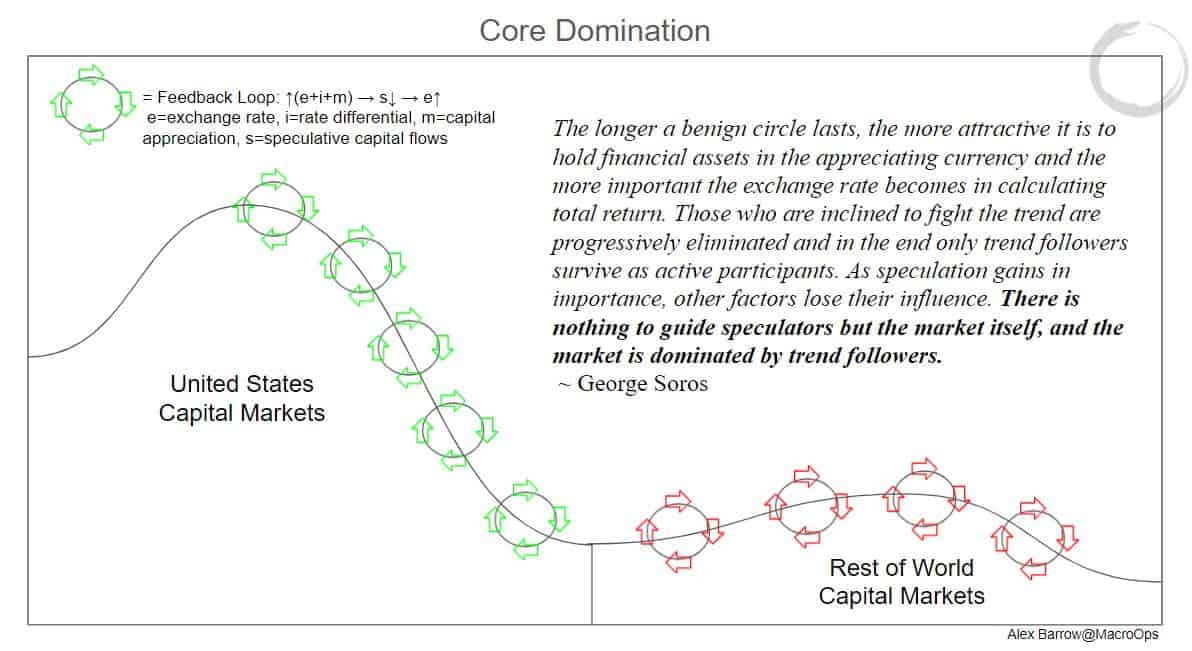

So at this point, the primary thing preventing the dollar from completely tipping over is relative US asset outperformance, or rather the bullish trend in tech. And this speculative trend that has driven Domination by the Core is itself being driven by stimulus-funded trend followers.

Understanding this, we’ll know the time is ripe for the real start of the USD bear market when the trend in US tech begins to bend — which I suspect will come sooner rather than later. That will mark the extinguishment of the final bullish USD supportive leg and the start of a new regime. One balanced by capital flows back to the periphery (RoW) and a Vicious Circle for the US.

This new regime will be led by commodities, emerging markets, cyclicals, value, etc… And it will kickstart a number of monster cyclical trends.

Finally, I should note that this will just be a standard cyclical turn in the dollar. And in no way does it reflect the greenback’s status as the world’s reserve currency. I’ll write in a follow-up note about why that’s not a serious risk.

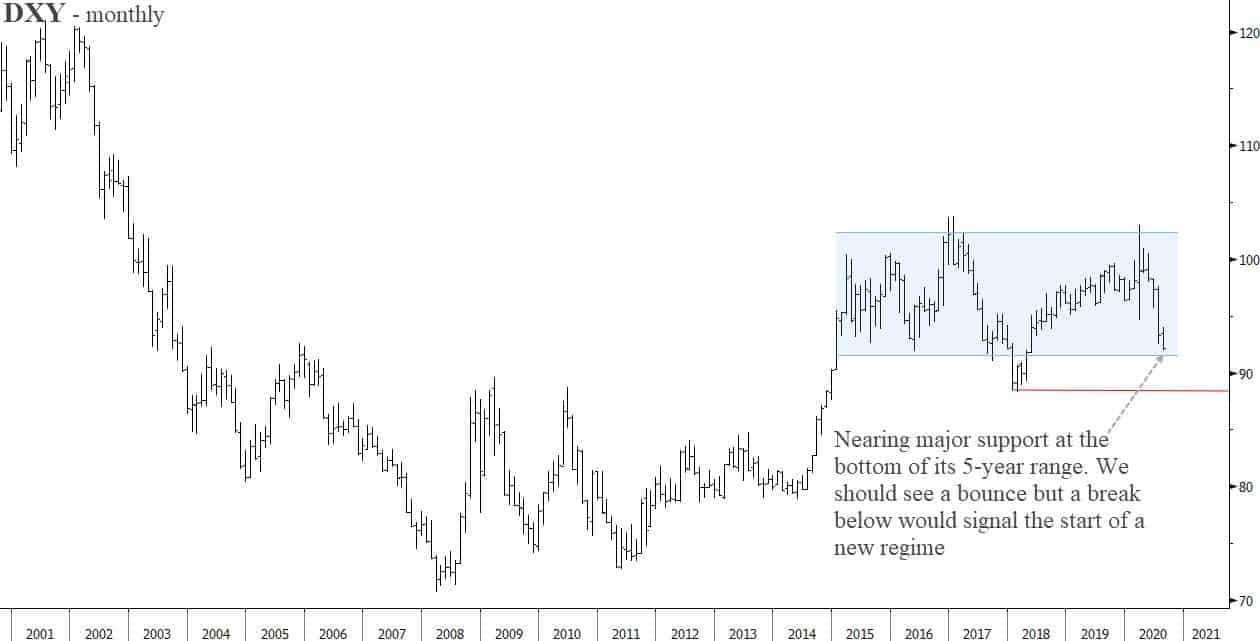

In the meantime, DXY is nearing significant resistance and technical extension. We should see a reversal soon — failure to do so would be an important signal. So we need to wait for the tape to confirm.

Stay safe out there and keep your head on a swivel.