We hope you had a better weather weekend than we did in MD. Rain, rain and more rain. I can’t complain, though. I finished one of my newest favorite books: Amarillo Slim in a World Full of Fat People.

If you haven’t read it, buy a copy. Brad Hathaway (you can find his podcast here) turned me on to the book. He even bought me a copy. Great dude — can’t thank him enough.

Next on my to-read list is Creating Shareholder Value and The Bond Book. What’s on your reading list?

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- A Framework For Understanding Financial Companies

- Investing in Cloud Computing

- Alta Fox’s Latest Activist Position

- Why IPOs are Rip-offs

Ooo I’m excited for this one! Let’s get after it.

—

June 25th, 2020

Chart Of The Week: This week’s chart was featured in a prior Breakout Alerts report. So far it’s working in our favor (I have a position). Profit target is around $59-$60/share. Here’s what I like about it:

-

- Breakout from horizontal boundaries

- Established uptrend

- Continuation pattern from bullish inverse H&S breakout

__________________________________________________________________________

Investor Spotlight: Alta Fox Raises Voice in Activist Campaign

GIFs by tenor

GIFs by tenor

Alta Fox Capital went activist last Friday. Connor Haley, managing partner of Alta Fox, disclosed an activist position in Collector’s Universe (CLCT). You can read the letter here.

Connor is one of the sharpest investors in the game. I read his letters like religion. This public activist stance got FinTwit’s attention real quick.

Before diving into the letter, let’s take a look at CLCT.

CLCT By The Numbers

-

- Market Cap: $305M

- Enterprise Value: $296M

- Gross Margins: 60%

- Unlevered FCF Margin: 19%

We can see why Connor would like CLCT. A durable, high FCF generating business with a strong competitive moat.

Armed with our figures, let’s breakdown Connor’s letter.

Not Your Typical Activist Stake

Alta Fox didn’t initiate its CLCT investment with the intention of going activist. The fund bought shares because CLCT displayed common characteristics found in many Alta Fox investments (from the letter):

-

- Strong competitive advantages

- Long runway for growth

- Attractive reinvestment opportunities

- Low investor awareness

But after talking with past executives, employees, customers, etc. Alta Fox smelled an untapped value creation opportunity.

The activist campaign centered on one company problem (from the letter, emphasis mine):

“In our opinion, CLCT’s lack of innovation and margin improvement is primarily attributable to a complacent and disengaged Board that has not demonstrated or executed on a thoughtful capital allocation plan.”

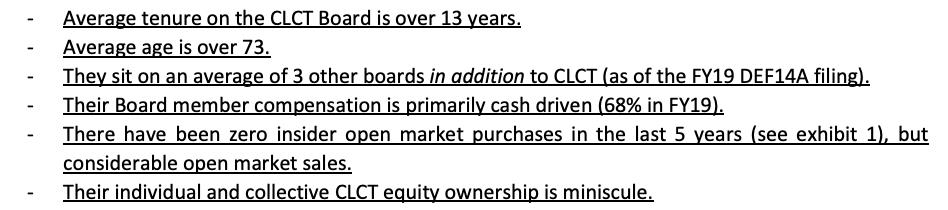

Not The Best Board

Reading further, we see why Alta Fox wants to change CLCT’s board. Take a look at the current board’s rap sheet (from the letter):

That’s a recipe for complacency and lackluster capital allocation. And when Alta says the board’s equity ownership is minimal — they mean it. The board owns (a collective) 1.5% of common stock.

Three Ways Out

Alta Fox sees three paths for CLCT’s future (from the letter):

-

- Bring in a new and rejuvenated Board to work with current management in improving the core business (Alta Fox’s preferred plan)

- Slash public company costs and go private

- Maintain the status quo (which the board has elected to do)

Alta’s Final Thoughts

Alta Fox sums up its thesis in the following paragraph (emphasis mine):

“With reasonable growth and margin expansion assumptions, CLCT’s base grading business is severely undervalued by the market today. Furthermore, the market today is assigning CLCT no credit for any digital efforts. Our nominees would work tirelessly with management to fix the bottlenecks in the core grading business, introduce valuable new digital services, and bring increased transparency to both investors and customers …

We believe our nominees have the experience and track record to work collaboratively with management to deliver $100/share in value to CLCT’s shareholders within the next 3 years ($50/share in core business + $50/share in new digital initiatives).”

__________________________________________________________________________

Movers & Shakers: Frameworks For Financials

GIFs by tenor

GIFs by tenor

I struggle analyzing financial companies. In fact, I have yet to invest a dollar into financials or insurance businesses. Not because I don’t think they’re good businesses. But because I don’t understand them. I want to change that. That’s why we’re covering Marc Rubinstein’s newsletter post, Front Book, Back Book: A Framework for Understanding Financial Companies.

The Benefits of A Large Back Book

Banks and insurance companies have “old” assets on the balance sheet. Each year, those assets grow because you can’t replace the duration of those assets today, with the returns you’ve generated from the old asset until now.

In short, a long-tail premium written decades in the past has had time to accumulate decades of premiums. That’s not the case for newer premiums.

Here’s Marc’s take on the benefits of a large back book (emphasis mine):

“A financial company doesn’t have to start all over again on 1 January each year. Before it even opens its doors it can bank on a stream of income coming in (although a stream of charge offs or claims could very well go the other way). Unlike other businesses a back book makes money during the night and over the weekend. It’s a melting ice cube of course, the asset won’t stick around forever, but as long as it was priced correctly, the back book can provide a stable stream of earnings to finance new business growth.”

Did you catch that last part? “As long as it was priced correctly …”

That’s critical. Marc explains why (emphasis mine):

“Just as no-one priced in the possibility of large-scale terrorism losses in 2001, no-one priced in the possibility of pandemic losses in 2020. Lloyd’s of London estimates that insurance industry losses will exceed US$100 billion this year. That’s around twice what 9/11 cost (US$40 billion or US$55 billion in today’s money).”

What does this mean for financial companies’ business models? They become quite capital intensive enterprises.

That makes sense. The back book of business took a lot of expense to win upfront. But after that, it’s an annuity stream until losses and claims come in. It’s at this point we find the distinction between front and back books.

Front vs. Back Books

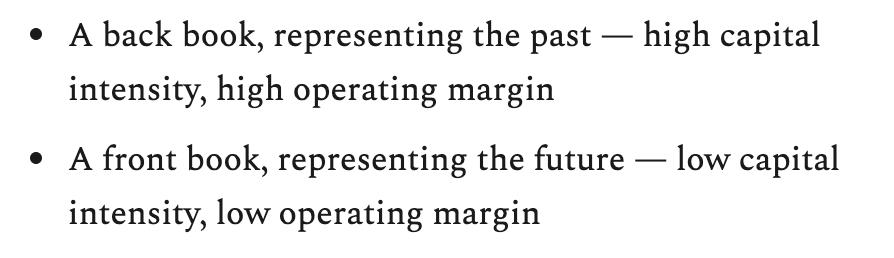

I love the way Marc bifurcates financial companies’ two main business segments (from the article):

This creates a problem for newer financial companies, like insurance. Take Lemonade, Inc. for instance. We covered them in last week’s Value Hive. Marc notes an important distinction in their business model that allows Lemonade to eliminate the need for a back book (emphasis mine):

“Lemonade details in its S-1 prospectus how beginning 1 July it will cede 75% of its business to reinsurers. Like most fintechs it does not have the capital to cultivate a back book.”

Again, this makes sense. The back book is a highly capital intensive operation (but with high margins). What new company wants to go through the trouble of developing a back book of business when they can offload it to reinsurance companies?

A major problem with doing that is lack of skin in the game. Marc explains (emphasis mine):

“The problem of course is that it removes skin in the game. If you’re not going to retain some interest in the long-term performance of the book, there is little incentive to underwrite it properly at the outset.”

Benefits of Having Two Books

The newsletter ends with a defense for two books of business (emphasis mine):

“When capital is abundant, pricing goes down. At times like those, a well-underwritten back book can sustain the business until the cycle turns. If the entire business is built around flow it’s harder to withstand competitive forces … But when capital is depleted, like it is after large losses and pricing goes up — that’s really the time to dance.”

Marc observes two ways to make money with both books:

-

- Front book: follow the pricing higher (works best in a consolidated industry

- Back book: Value the book higher than the market

__________________________________________________________________________

IPO Of The Week: IPOs are (actually) Rip-offs

Last week we covered Lemonade, Inc. LMND wants to go public via IPO. Bill Gurley thinks that’s a terrible idea. And we should listen to him. Gurley’s a GOAT in the venture capital space. He’s invested (via Benchmark) in companies like Uber, Zillow and Stitch Fix (to name a few).

What makes IPOs such a rip-off? Simple: it’s all about the underwriters making money. Gurley elaborates with a story on Elastic’s public offering (emphasis mine):

“We suddenly realized that the investment banks were way underpricing the shares, and that the market cap would jump by $70 [million] to $80 million the first day.”

When investment banks underprice a company’s shares, there’s usually one direction the stock trades post IPO. Up. Gurley noted that in Elastic’s case, the underwriters took home a cool $200M in gains from the share price increase. None of that went to original investors (like Benchmark) nor the company’s bank accounts.

A 2019 CNBC article revealed the largest underpricers in the underwriting game (Hint: it’s who you think it is).

What’s the solution? Gurley suggests direct listing.

Benefits (and Drawdowns) of Direct Listing

The main benefit of a direct listing is insiders and employees retain most of the equity ownership in the company. There’s less dilution and you remove the underpricing with investment banks.

It’s also never been easier to directly list on a stock exchange. The article notes, “There’s no technical reason why companies can’t list themselves. The technology already exists. Companies can essentially plug right into the stock exchanges, and the share price gets determined by a standard market-matching process.”

There are clear drawdowns with direct listings. IPOs are an easy way to raise cash for a business. Direct listings don’t have a clear way to raise capital (if companies need it). Another common drawdown people mention about direct listings is there’s little/no momentum going into the listing.

I don’t see that as a big issue with social media and digitization of road shows.

If you’re interested in learning more about direct listing vs. IPOs, Patrick O’Shaughnessy did a great podcast with Gurley. You can find that here.

__________________________________________________________________________

Whitepaper Of The Week: Investing in Cloud Computing in 2020

GIFs bytenor

GIFs bytenor

JPM released a 106-page CIO survey on IT investment spend. It’s a great primer for understanding where chief allocators put their money in that space.

Here’s the TL;DR if you’re pressed for time:

-

- IT budgets remain cloudy (see what I did there) amidst COVID-19 uncertainties

- Microsoft dominates the cloud game (commands 3x mindshare as #2 opponent)

- Spending on cloud computing remains robust

- Top five companies include: Microsoft, Amazon (w/ AWS), Google, salesforce, and ServiceNow.

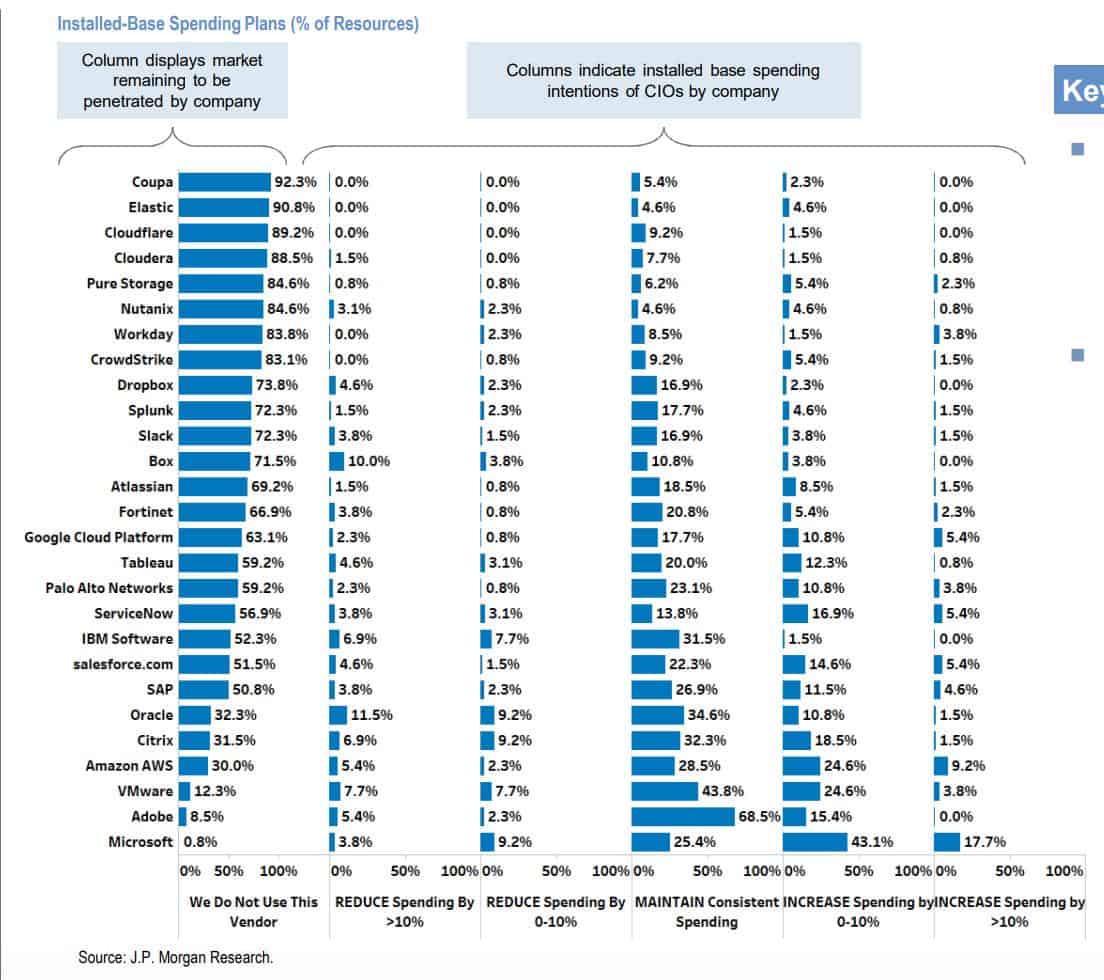

Spending Plans For CIO’s in 2020

One of the coolest parts about the survey was seeing how CIO’s planned to spend their IT budget. And more importantly, which product companies CIO’s plan to invest in. Check out the graph below:

There’s a few things to notice from this graph:

-

- Microsoft only has 0.8% of the market left to conquer

- CIOs plan to maintain investment in Adobe

- Almost 50% of CIOs plan to invest more in Microsoft products

Also not a huge fan of Slack’s numbers in this report. Looks like deterioration of the bull thesis.

Let’s take a look at another graph (warning to Box.com shareholders):

Almost 50% of CIOs expect to increase their spending in Microsoft products/services. On the other hand, CIOs plan to spend 10% less on Box.com and 4.6% less on Dropbox. But don’t tell that to DBX and BOX shares. Both companies’ stock prices are hitting new highs.

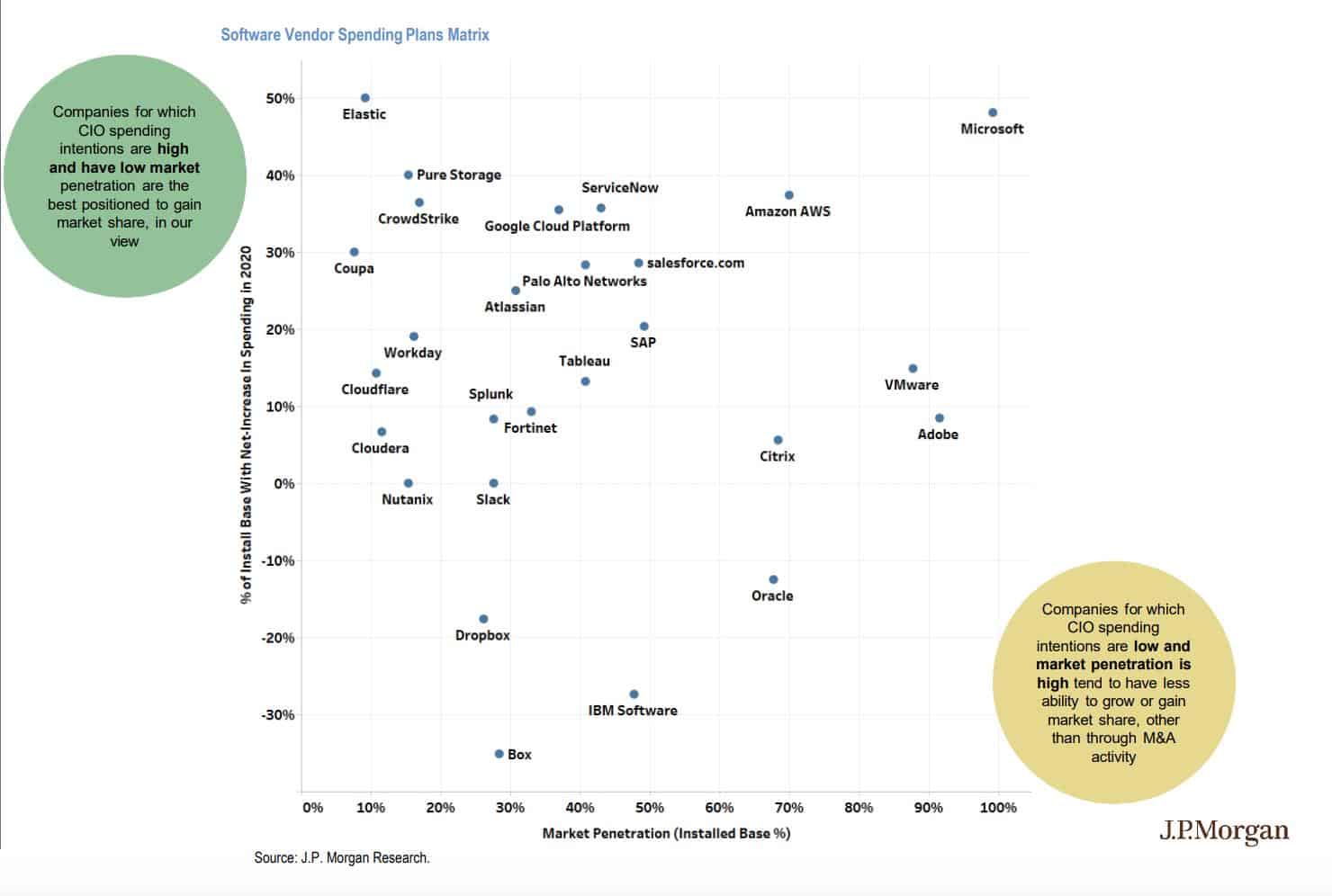

Next is one of my favorite charts in the survey. If you’re looking for actionable investment ideas this is your chart:

Take a look at the top left of the chart. It shows companies which CIOs spending intentions are high and company market penetration remains low. In other words, there’s a lot of demand for these products with long runways for growth.

That’s not a bad combination.

If you don’t want to squint your eyes, here’s the list:

-

- Elastic (ESTC)

- Pure Storage (PSTG)

- CrowdStrike (CRWD)

- Coupa (COUP)

Find a hour to read the entire report. You’ll get smarter and learn about a few businesses you might not otherwise.

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!