It was just one year ago today that we flattened our equity book and went 200% long bonds… Good times…

Anywho… We’ve been seeing some chatter from the Perma bears (you know the type) who are saying things like “there are a number of parallels between now and then, except this time it’s going to be inflation that kills…” I’m quoting one of the repeat offenders whom I won’t give the honor of calling out by name.

Instead, I’ll use today’s piece to explain what’s really going with the recent vol and where the market is likely headed. So let’s begin.

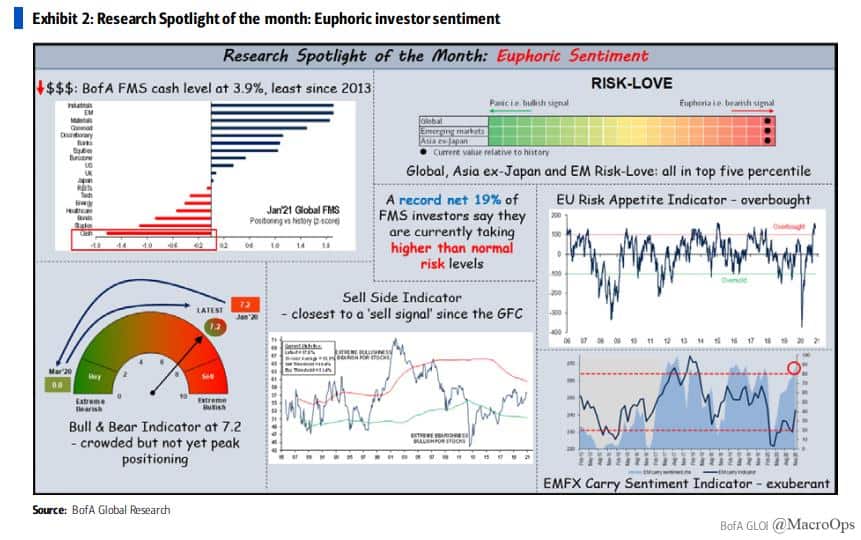

This week’s air pocket market action is a common symptom of “Trend Fragility”. It’s a manifestation of the positioning and sentiment environment we’re in and which I’ve been pointing out for the past few weeks (here’s an excerpt below).

- A record net 19% FMS investors assuming higher than normal risk

- FMS cash level of 3.9% have triggered a ‘sell signal’

- Global Risk-Love indicator is in the 97th percentile of history going back to 1987

- EU Risk Appetite indicator is in overbought territory

- Asia ex-Japan and Emerging Market Risk-Love Indicators are signaling euphoria for the first time since 2015

- The Sell-Side Indicator is at its closest level to a ‘sell signal’ since the GFC

But stretched positioning and sentiment are only a condition, not a catalyst. Both can persist for a long time.

Increasing intraday volatility is what makes a Bull Volatile Regime — the major indices are currently switching back and forth from Bull Quiet to Bull Volatile. This is typical action that defines the latter part of an intermediate trend. But… it doesn’t by itself mean we’re forming a market top.

The market can easily go on to run to new highs over the coming weeks and even months. Furthermore, volatility like that which we’ve seen over the last couple of days actually helps prolong the trend by shaking out weak hands and resetting sentiment some.

What we need to watch how the TL Score develops. It’s currently giving a reading of -2, which is bearish but not horribly so. Remember, it’s readings of -3 or worse that precede larger selloffs. The breakdown of the TL components is as follows.

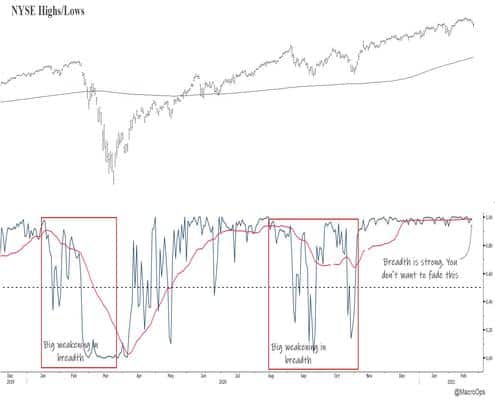

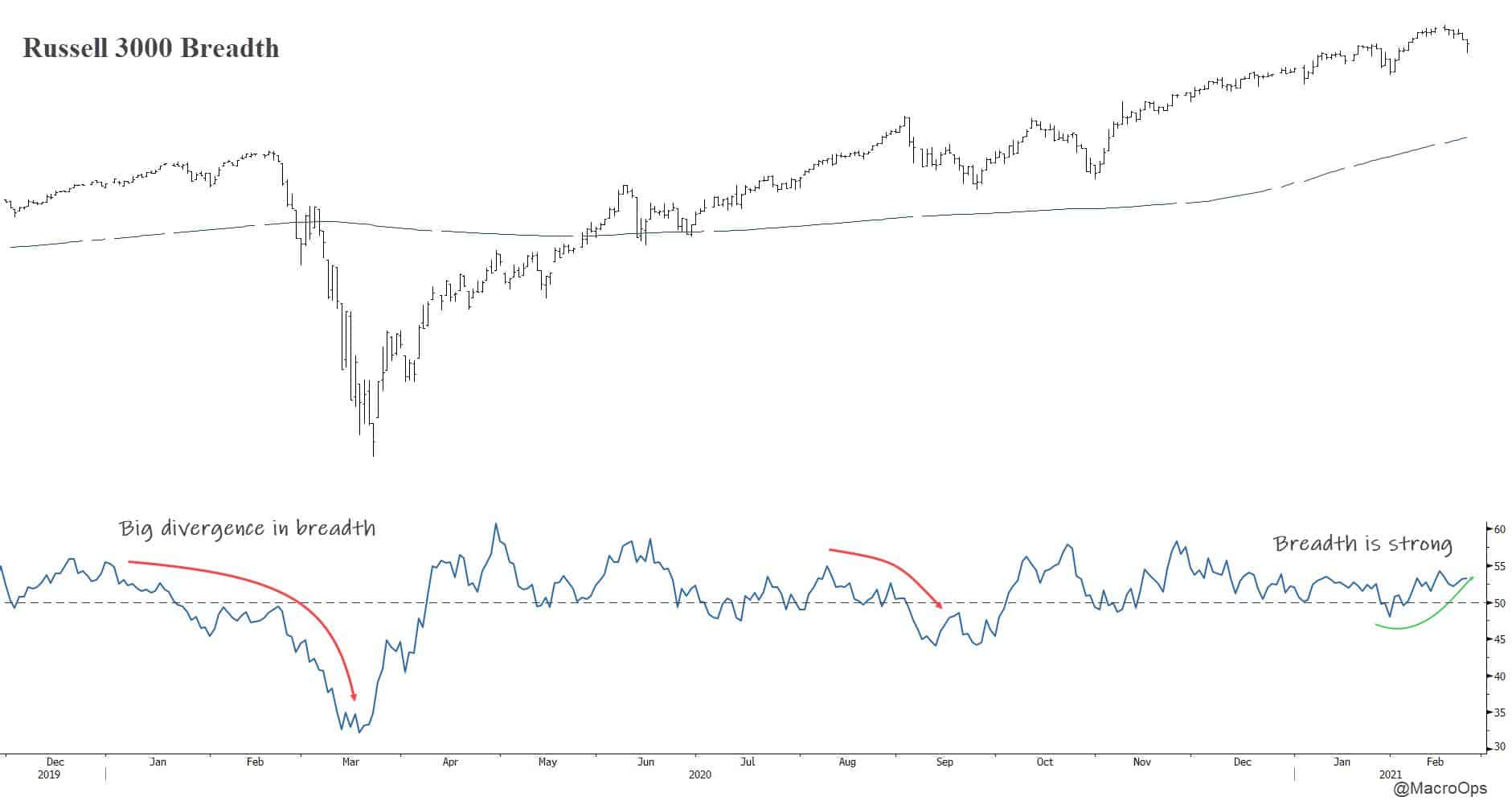

- Breadth: +3

- Sentiment/positioning: -2

- Liquidity: -3

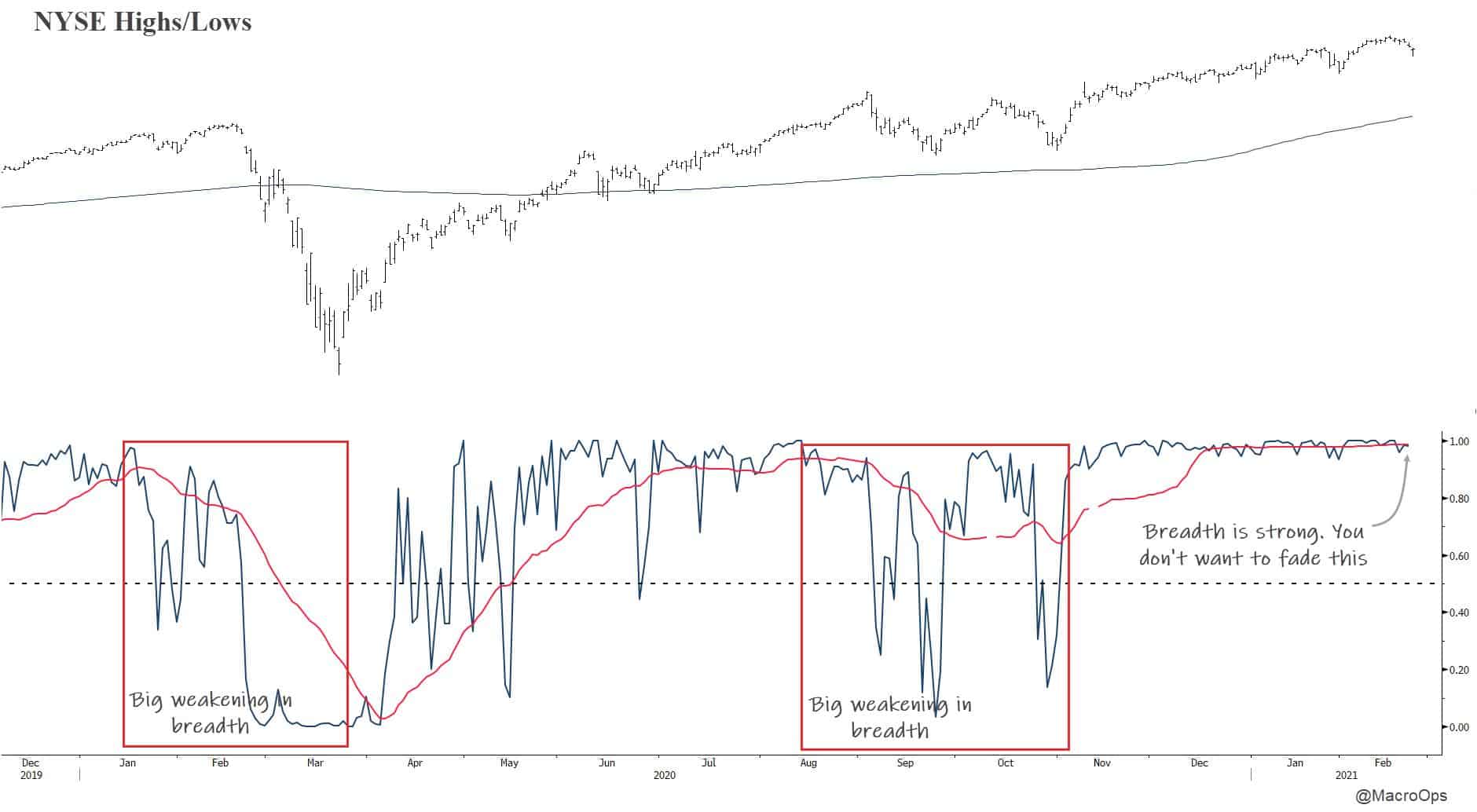

Breadth matters the most over the short-term. And right now it’s holding up very well. This tells me that we should see a continuation in the bounce over the coming days.

Liquidity is the thing to watch to see if this will end up being a bit of a sideways range before the next leg up or if it’ll evolve into a larger selloff.

I’ll explain what’s happening on the liquidity front by starting from the 30,000ft macro view before zooming in for a closer look.

The major market moves right now are being driven by a complete repricing of the macro outlook.

The market is correctly revising its expectations for low growth and low inflation to one of strong growth and above-trend inflation. This is showing up in the repricing of yields which is feeding into a larger rotation out of richly valued tech names and into reflationary assets.

Growth estimates are justifiably being revised from a consensus of around 4% to what will likely be 6%+ GDP growth this year in the US.

This revision of expectations is impacting liquidity conditions in two ways.

First, the market is starting to front-run the Fed by pricing in rate hikes earlier than what the Fed has communicated. We can see this in the chart below where the green line shows the median FOMC dot plot and the purple line shows the OIS forward curve which is diverging higher.

This is creating a bit of a communication challenge for the Fed. And we should expect this front-running to continue until the Fed pushes back and likely implements some form of calendar-based guidance, similar to what the RBA recently did.

Either that or the market throws a fit and we enter a period of risk-off feedback loops which reprice growth/inflation lower… My money is on the former though since the Fed has so far convincingly made the case that they’re operating in a new paradigm.

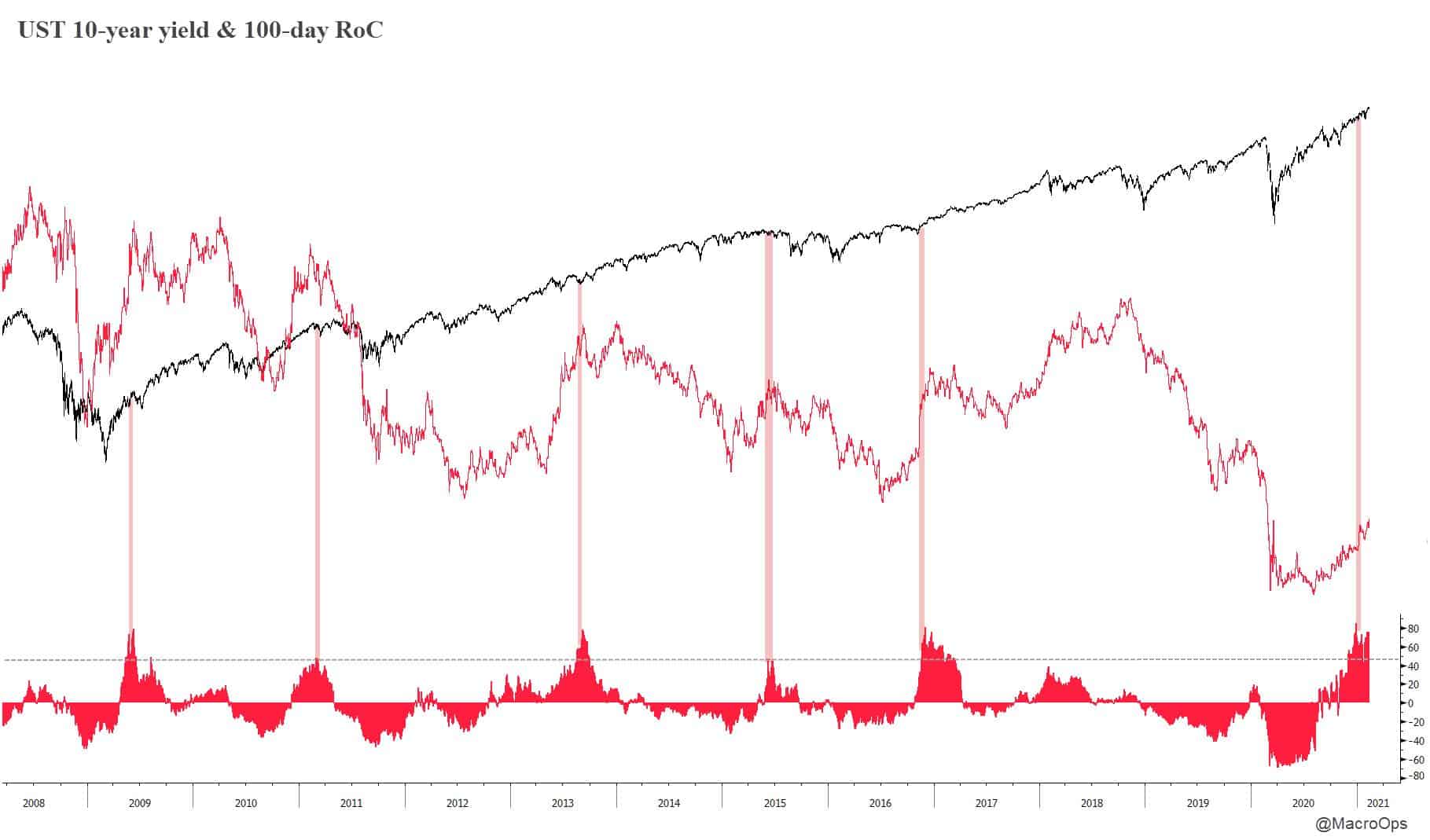

Either way, this front-running is tightening things at the front end and this revising of expectations is also driving the curve to steepen. US 10-year yields have run from a low of 50bps to a recent high of 1.43%.

The chart below shows the 10-year yield (red line) and its 100-day rate-of-change (red histogram). When analyzing yields we’re concerned with not just the level but also the speed at which they rise and fall. We can see that yields have accelerated to the upside at a pace that often leads to increased volatility.

The determining factor in whether a pickup in yields leads to an extended volatile regime or just a short-term correction is whether the move is predicated on a correct or incorrect read of the incoming economic environment (ie, whether it’s a real or false trend as Soros would say).

Let’s look at 2016 and 2018 as examples.

In 2016, the world was thrust out of a global recession and painful commodity shock through the injection of massive amounts of stimulus from the Chinese, as well as a pause by the Fed in its tightening regime.

This drove a quick repricing of growth expectations sending yields on the 10yr from a low of 1.34% to a high of 2.64% in roughly 6-month’s time.

Fast-rising yields caused some bouts of volatility, which you can kinda see on the chart above (I say kinda because they were small and short-lived). All in all, equities were able to digest the rise in rates because the move was predicated on a real trend… growth was accelerating and it was sustainable. Plus, the Game Masters (Central Bankers and Politicians) weren’t interested in raising rates anytime soon since much of the world was coming out of recession.

Towards the end of 17’, yields again started running higher. Growth had long recovered and global equities had been in a low volatile “melt-up” for nearly 18-months. The Fed had resumed its pace of quarterly rate hikes and the 10-year yield jumped from 2% to 3.25% over the course of 15-months.

The market was lulled into a sense of complacency where it began to blindly extrapolate the recent past well into the future as it so often tends to do after a long trend. Here’s a bit from a post titled “Something That Everyone Knows Isn’t Worth Anything” where I share some color on the bond narrative that was being passed around by financial outlets at the time.

The article is aptly named “Bond Bears Popping Champagne Say U.S. Yields Have Room to Rise”.

Thirty-year Treasury yields pushed above the 3.25 percent level that fixed-income veteran Jeffrey Gundlach identified as a “game-changer.”

“Solid data releases, higher oil prices and a technical backdrop that suggests there are not a lot of obstacles for yields to continue to push higher will have many wondering how far this new push higher can go,” said Rodrigo Catril, a Sydney-based strategist at National Australia Bank Ltd.

Short sellers were already positioned for more pain in the Treasury market. Speculative net short positions on 10-year notes climbed to a record, the most recent Commodity Futures Trading Commission data showed. An update to those figures comes Friday.

“In hindsight, we wish we were even shorter on U.S. rates,” said Raymond Lee, a fund manager at Kapstream Capital Pty in Sydney.

As a result, the market sent yields across the curve higher while at the same time the global outlook began to materially deteriorate.

China was doing another Chinese-style deleveraging which was feeding into decelerating growth throughout much of the world. But… the consensus market narrative had become so caught up in the “goldilocks” growth and bond bear market narrative that its collective sense-making abilities turned myopic. It failed to see the dynamics had changed and that the rise in yields was a classic Soros-style false trend — it was untenable.

This toxic combo led to 22-months of volatile sideways chop in equity markets along with another recessionary bear in emerging markets and commodities.

And this brings us to today, where the backdrop is much more like 16’-17’ than it is 18’. With vaccinations ramping, COVID cases dropping, personal savings near record highs, and our Gamemasters leaning heavily into reflationary policies, the incoming macro environment is much more bullish than it was in even 2016/17’.

One bearish distinction is that valuations in the US are much higher now, especially in the popular tech sector, where the average price-to-sales ratio is a heady 7x. We should expect an acceleration of capital flows out of these rich names as the curve continues to steepen.

This is just a change in leadership though, a continuation of a move that’s been playing out over the last year.

Large rotations or regime shifts like these often bring volatility like that which we’ve recently seen. And we should expect more bouts like these as long as the curve is steepening.

Anyways… here’s what we’re watching to see if this correction is the start of something more ominous, the beginning of a sideways range, or just a quick shakeout before another leg up.

As I said, breadth is holding strong.

If we see either of these indicators begin to roll over it’ll tip the TL Score below -3. But as of right now, this type of breadth is more indicative of a pause and minor shakeout than it is of a prelude to a larger selloff — see how both indicators dipped well into negative territory in the runup into last year’s crash.

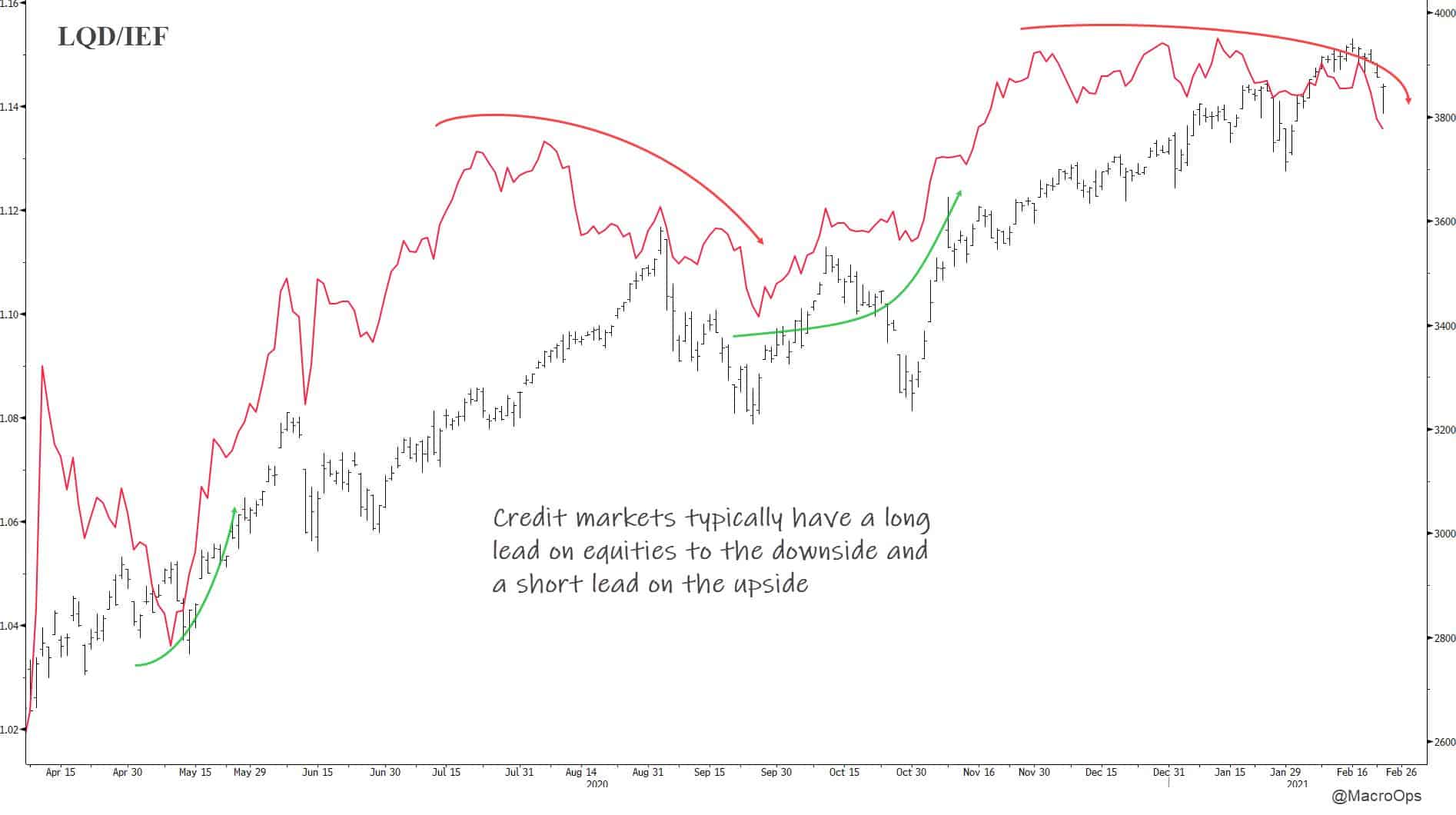

Our credit indicator has been trading sideways-to-down since mid-December giving us notice to expect increasing volatility, which is exactly what we’ve seen over the last month.

This indicator tends to lead on the way down as well as on the way up. So if we’re going to get a sustained move in either direction we’ll want to see it confirmed by LQD/IEF.

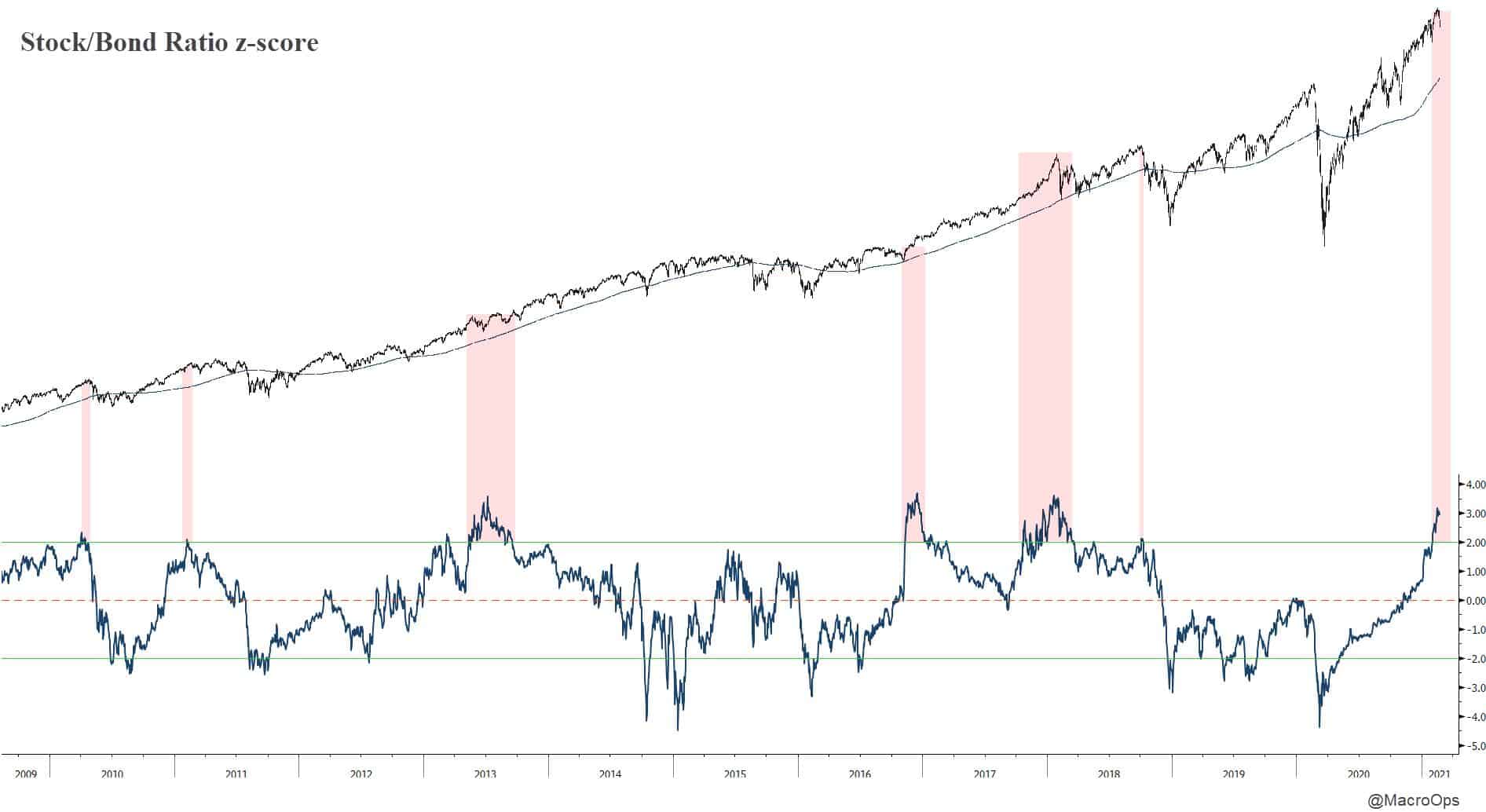

Markets are a game of relativity. Nothing is viewed, valued, or measured in a vacuum. Over the last 12-months, we’ve pointed to the sub -4 stdev move in the stock/bond ratio as one of the many reasons to be extremely bullish. That’s no longer the case today.

The ratio has completely flipped and is now a headwind to risk assets. This isn’t, by itself, a reason to be bearish. We can see in early 17’ that the ratio reset once yields took a pause and equities resumed their climb.

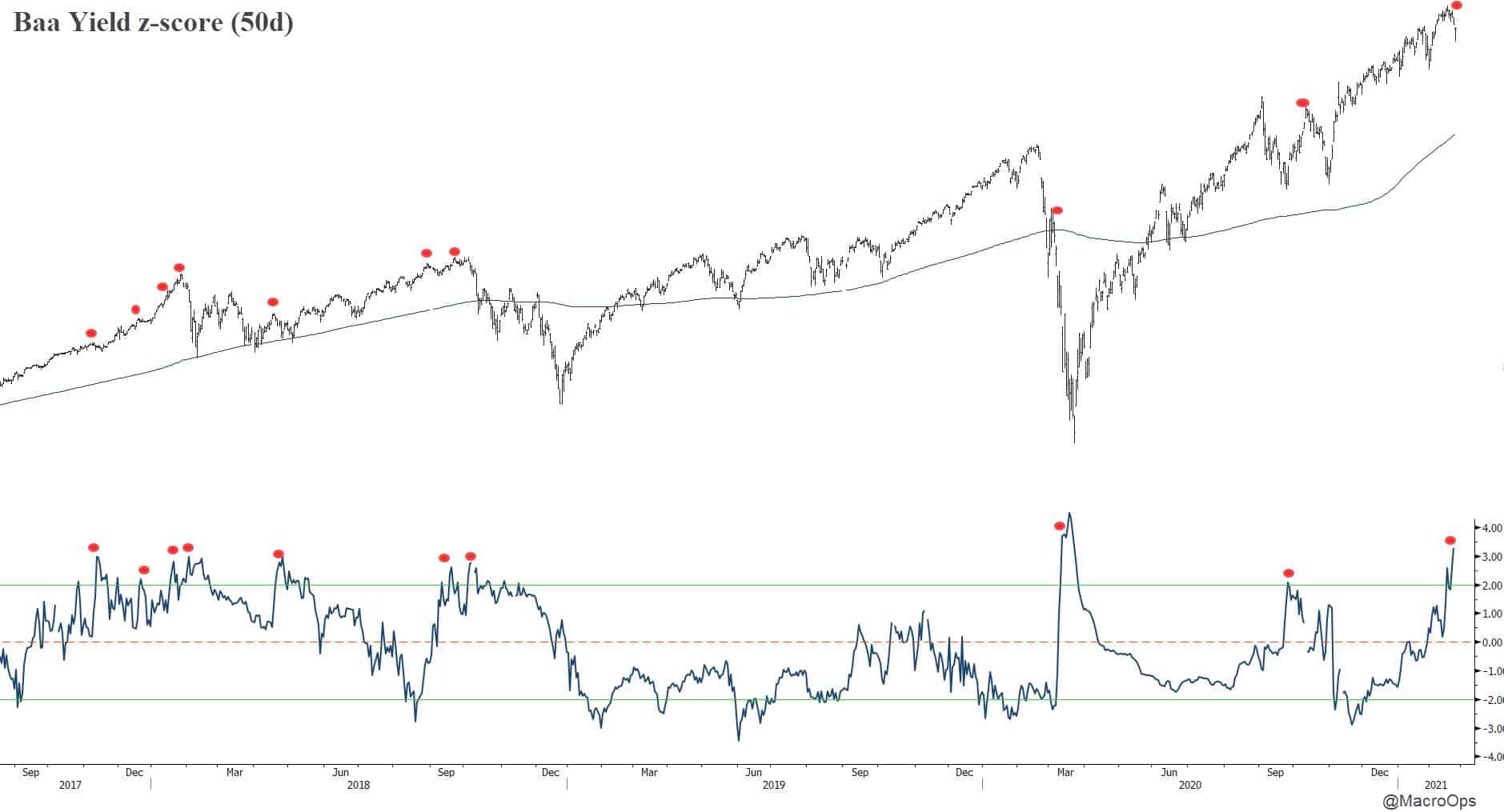

Similarly, Baa yields have seen a 3stdev run higher over the last 50-days. Historically, this leads to some short-term equity weakness like that which we’re experiencing now. We’ll want to see this come down and settle if we’re to see a sustained advance higher.

Finally, we’ll end with the most important input in our Hierarchy of Technicals, the tape itself.

So far, the dip is catching a strong bid. This type of action is reflective of a Bull Quiet regime where the best sell setups fail. When looking at this along with the resiliency of breadth, I’d say the odds favor a short consolidation zone of sideways chop before another leg higher.

Of course, we’ll be watching the Trifecta of inputs and following what the tape and our TL Score tell us… We remain in a market that you want to buy more than sell. But do so with the expectation that as long as positioning and sentiment remain high, and yields continue to climb, Trend Fragility will remain elevated and volatility pockets more frequent.

Stay safe out there and keep your head on a swivel.