***The following is an excerpt from a recent Market Note that went out to members of our Collective***

Let’s kick this Market Note off with perhaps the best description of the price-sentiment relationship I’ve ever read. It comes by way of one of my favorite trading books “The Way of the Dollar”, by John Percival (note: this book has long been out of print. Collective members can find a link to it in our Vault). Here goes, with emphasis by me.

“In all markets, price extremes are usually attended by a consensus that the trend, be it up or down, will continue; and by a peak of speculation in line with the trend. Hence the excruciating paradox of financial markets, that sentiment is most bullish at the peaks when prices have only one way to go which is down; and most bearish at troughs vice versa: at the top there’s no-one left to buy, and at the bottom no-one left to sell.

“This paradox is absolutely central to the working of all financial markets and we need all the help we can get to understand it so thoroughly that it becomes part of our nature. The more bullish things are, the more bearish they are. Bullishness is born as hope in the midst of despair. Hope swells to confidence and confidence swells to euphoria, and the process contains the seed of its own destruction and the birth of its opposite, fear. Fear is nurtured by falling prices and the two feed on themselves until they swell to despair. And so the cycle is completed and ready to begin again with the birth of hope.

“This is both the way things are and the way they have to be. We haven’t understood the process until we have grasped that. The despair creates the price trough: the price trough creates the despair. The price extreme is the definition of the extreme of despair, which is in turn, by definition the moment when hope comes to prevail; hope feeds and is fed by rising prices until the peak of price and euphoria leave prices with only one way to go, which is down.

“This circular process underlies every price fluctuation in free markets from the smallest one measured in seconds or minutes to the largest measured in years or decades. So it has always been and so it will always be, because it must be. The ancient Chinese symbol called T’Ai-chi T’u or “symbol of the ultimate reality”, more commonly known as the yin yang symbol, is delightfully appropriate to the way markets are — and uncannily appropriate to the way currency markets are.”

Markets, like much of nature, tend to oscillate around a balance point. This creates a constant push-pull, a back and forth, a to and fro that forms the fractalized sine waves of price action.

This is true not only of sentiment swings but also within important Intermarket relationships. The stock-bond relationship being a prime example.

No financial asset exists within a vacuum. The value of everything is a game of relative comparisons. The perceived value of stocks relative to bonds being the most important of these.

This is because stocks and bonds compete for capital. Higher bond yields attract capital. That capital has to come from somewhere, that somewhere is stocks. So stocks sell-off, bonds get bid, and yields fall. Eventually, yields fall to a point where stocks become more attractive and investment flows reverse. That is, until bonds sell-off to the point where they once again become attractive on a relative basis. The process repeats, ad Infinium.

Because of this, we can think of yields as a kind of governor on stocks or risk-taking in general. For those of you not familiar with what a governor is, it’s an electronic device that was put in many older vehicles by car manufacturers. It placed a limit on the car’s engine so it couldn’t go past certain speeds, typically around 100 mph.

Here’s the thing… This market’s governor no longer works… It wasn’t working great before the pandemic hit due to the global structural shift in demand for safe paper and its respective shortage (we talked about this at length here).

And now the relationship appears to have broken down completely. The result, no doubt, due to the Fed projecting zero rate hikes out to at least 2023 as well as signalling they’ll keep the long end from rising too fast if needed.

What does this mean from a practical standpoint?

Well, like a car that’s had its governor ripped out, there’s no longer an effective limit on the speed this market can run. At least, not a traditional one.

Without the limiter of rising yields to decelerate stock prices, equities by default become more speculative… capable of larger swifter rallies… higher valuations… and more volatility in general.

This is one reason why many indicators of sentiment haven’t been working as well as in the past. Extended Put/Call ratios being a perfect example. They’ve kept many smart traders on the sidelines for much of the second half of this year.

Without the back and forth of rising stocks causing falling bonds (rising yields), there’s less relative force on the upward thrust of risk-taking.

The impetus then falls to positioning, which trails sentiment. Investors need to get out over their skis in order to cause a larger selloff. This is the practical effect of “Hope swells to confidence and confidence swells to euphoria, and the process contains the seed of its own destruction and the birth of its opposite, fear.”

…at the top there’s no-one left to buy, and at the bottom no-one left to sell.

But as we’ve been pointing out the last few months, positioning is a ways away from creating instability. Large funds/institutions are still relatively heavy in cash and are lagging the market on the year. And managers of those funds would probably like to keep their jobs… So they’re likely to chase into year’s end to see if they can goose some return.

Now let’s run through some charts so we can show how this malfunctioning governor is showing up under the market’s hood.

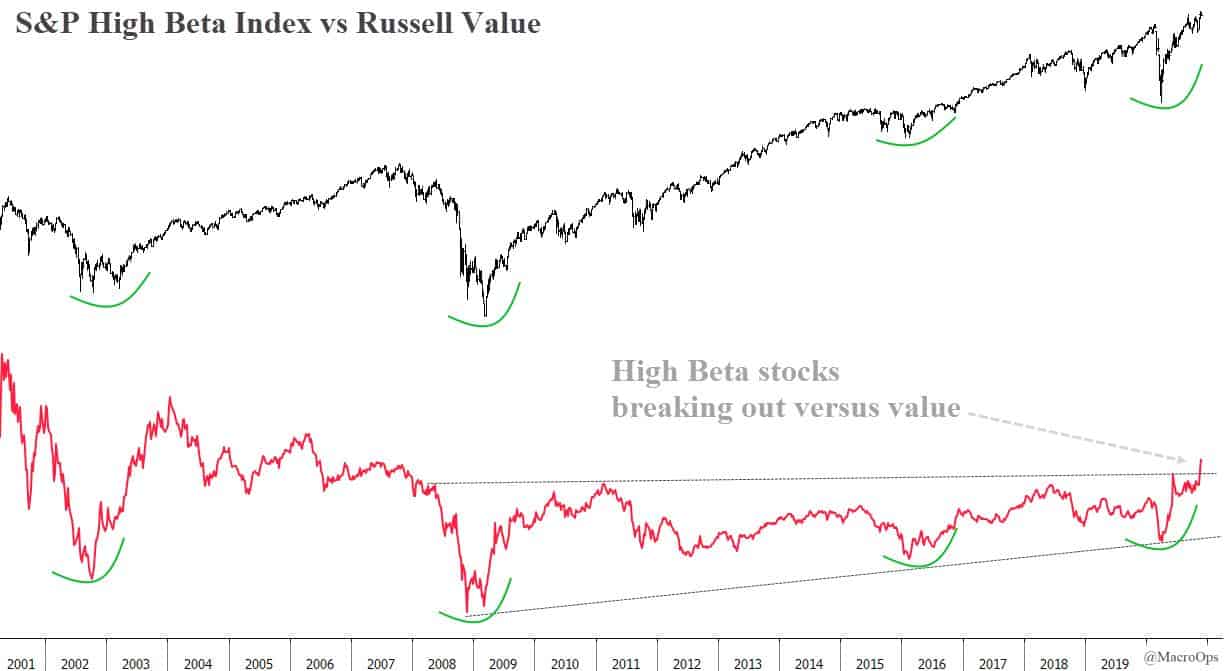

High Beta stocks are breaking out from a long base of relative performance against Value (h/t BofA’s Steve Suttmeier).

Industrials versus the S&P have bottomed and are ripping higher.

Cyclical versus Defensive is on the run following two years of underperformance.

This type of relative action is more indicative of follow-through after a major bottom than it is of a tape preceding a major top. And usually… this kind of Intermarket action would lead to bonds selling off and yields rising, thus sowing the seed of its own destruction.

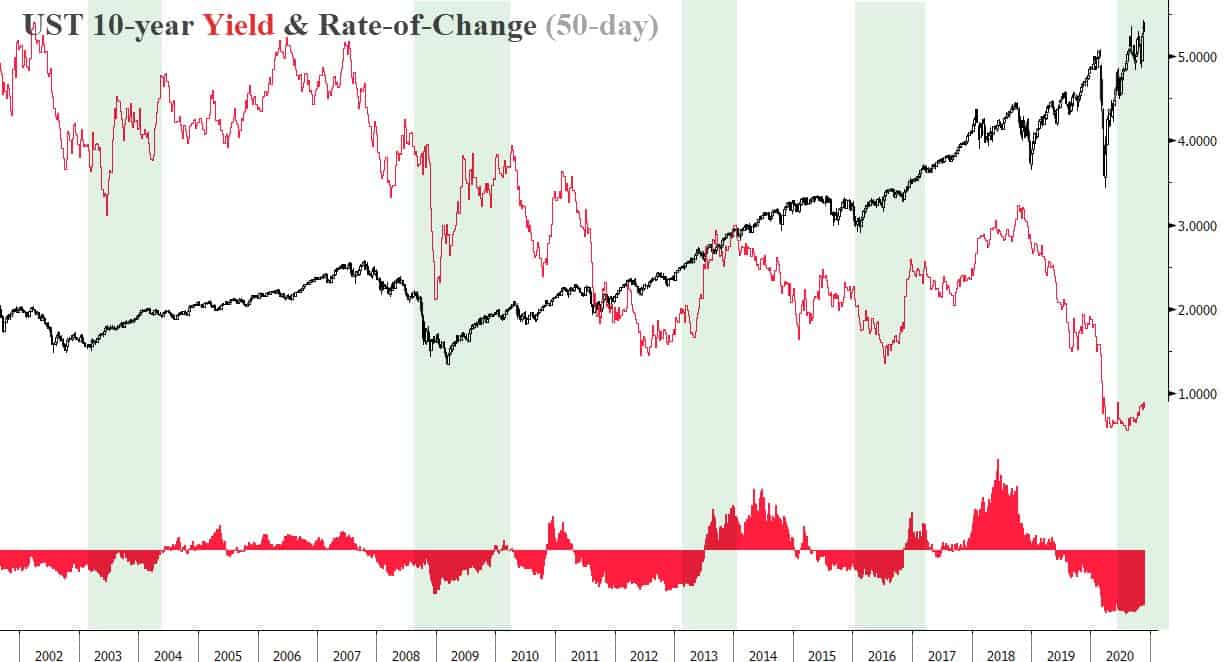

Not this time around though. Take a look at the following charts. The vertical green highlighted areas mark past instances when a major reflation trade was occurring in the market. The red line is the UST 10-year yield and the histogram of the UST’s 50-day rate-of-change.

During past reflation cycles, the UST 10yr yield spiked, usually well over 100bps over a short-period of time. This time around though it’s hardly budged. And that’s exactly why the SPX is within spitting distance of completing the “Greatest Rally of All-Time”.

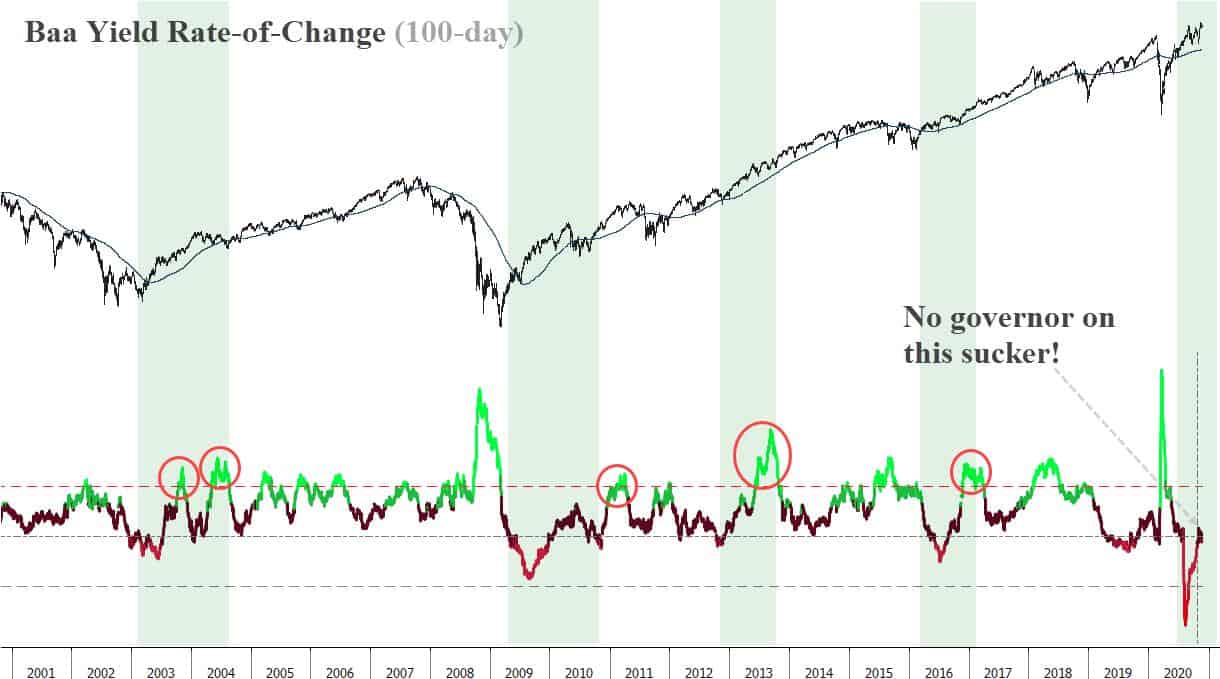

Same with Baa Yields..

The Stock/Bond ratio is a looong way from putting the pinch on risk-taking.

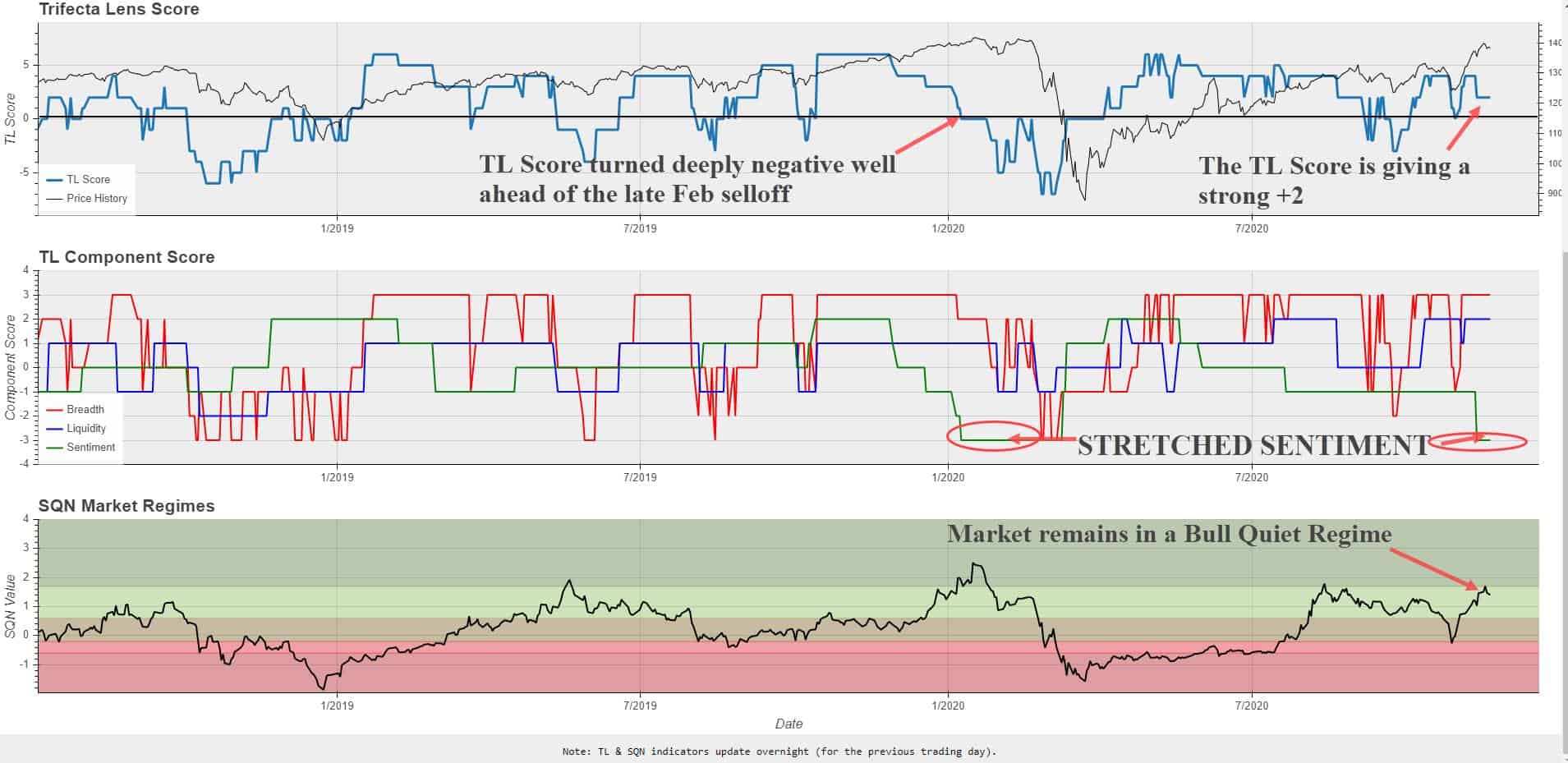

This is why stretched sentiment isn’t yet feeding into wobbly price action. And that’s why the play going forward is to keep doing what we’ve been doing all year. Watch the TL Score, the SQN, and positioning for signs this Tape is tired. And buy the dip and buy rips in the meantime…

The Trifecta Lens Score is giving a strong reading of +2 and the SQN remains firmly in Bull Quiet. Sentiment is the major drag at a full -3 but both breadth and liquidity remain robust.

Brandon and I are digging into a number of reflation plays this week. We’ll be out with some research in the coming days. A few of these names have 5x plus potential. Let’s talk about the one we’re excited about most. It’s a completely under the radar US small-cap that….

***The above was an excerpt from a recent Market Note sent out to members of our Collective***

Stay safe and keep your head on a swivel!