The pendulum of the mind alternates between sense and nonsense. ~ Carl Jung

Politics is a pendulum whose swings between anarchy and tyranny are fueled by perennially rejuvenated illusions. ~ Einstein

Stephen Buhner wrote in his book “The Secret Teachings of Plants” the following:

The physical Universe is an aggregate of frequencies. – Buckminster Fuller

All living organisms receive electromagnetic signals all the time. And like the signals received by our radios, many of them contain extremely large amounts of information, which can be used for a great many things. These range from regulating the opening of little doors in cells to let food in and waste out, to healing, to the beating of the heart, to birds orienting themselves to the magnetic lines of the Earth when migrating, to the communication between pollinators and their flowers, to the communications between members of the same family who have bonded with each other — and, of course, a great deal more.

Electromagnetic spectrum signals, like those we know as a particular radio station, can and do contain very large amounts of information… Every time life flows through a frequency in the electromagnetic spectrum, it fractalizes that wave differently, because the flow of life is always nonlinear. What is interesting is that unique information is always embedded or encoded within the way the oscillating sine wave is fractalized.

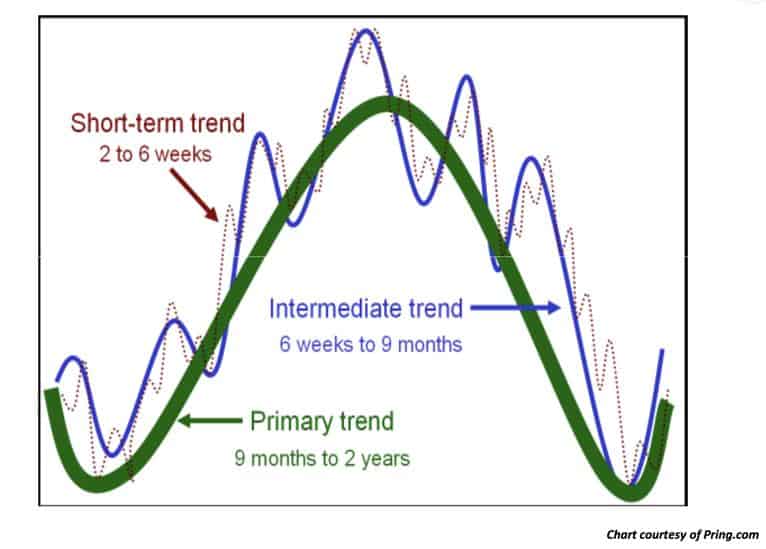

Fractalized sine waves seem to be encoded into the very fabric of our reality; like the Golden Ratio and the second law of thermodynamics. They appear throughout the universe on nearly every level of scale and function. It’s no surprise then that they underlie the very structure of our market, which is just fractalized sine waves overlaid on fractalized sine waves of various temporal scales.

This makes intuitive sense because a sine wave is just a continuous pendulum swing. And crowd dynamics naturally follow the path of a pendulum, swinging from one local extreme to another.

The market is in effect a large complex information transmission system. All acting participants make bets using their particular knowledge set which then in aggregate moves the market, providing new information for the actors to incorporate into their decision-making process where they then make new bets. Creating a neverending information feedback loop.

The infinite feedback loops in the structure of the market, not to mention the way group psychology evolves, necessitate this constant back and forth, like that found in every natural system.

Every rally sows the seeds for a reversal and every reversal sows the seeds for a rally. Ad infinitum.

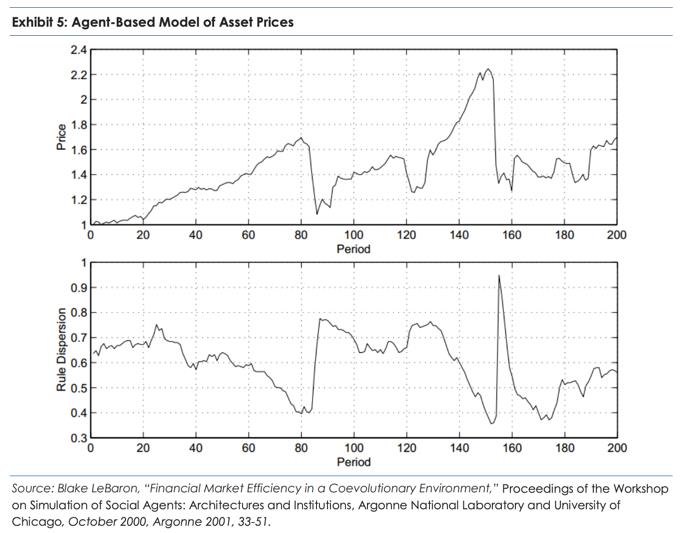

Michael Mauboussin discussed a critical driver behind why this process plays out in his recent paper titled “Who is on the other Side?”. In it, he shares work done by economist Blake LeBaron which animates this concept using an agent-based model (here’s a link to the original paper).

The model is computer generated and the “agents” are imbued with decision-making rules and objectives similar to those that drive market participants (i.e., make money, try not to lose money, don’t underperform the average for long periods, etc…)

Here’s a section from the paper (emphasis by me):

LeBaron’s model replicates many of the empirical features of markets, including clustered volatility, variable trading volumes, and fat tails. For the purpose of this discussion, the crucial observation is that sharp rises in the asset price are preceded by a reduction in the number of rules the traders used (see exhibit 5). LeBaron describes it this way:

During the run-up to a crash, population diversity falls. Agents begin to use very similar trading strategies as their common good performance begins to self-reinforce. This makes the population very brittle, in that a small reduction in the demand for shares could have a strong destabilizing impact on the market. The economic mechanism here is clear. Traders have a hard time finding anyone to sell to in a falling market since everyone else is following very similar strategies. In the Walrasian setup used here, this forces the price to drop by a large magnitude to clear the market. The population homogeneity translates into a reduction in market liquidity.

Because the traders were using the same rules, diversity dropped and they pushed the asset price into bubble territory. At the same time, the market’s fragility rose.

Mauboussin goes on to note the important lessons this model underscores about our market structure, which can be broken down into three primary points.

- Falling agent diversity initially leads to agents making more money which creates a feedback loop of higher prices -> agents in the ‘herd’ make more money -> less agent diversity -> higher prices… This is why fighting trends, even ones based on faulty prepositions, can be so dangerous over a short timescale.

- A reduction in agent diversity is non-linear. Meaning, as diversity falls, market fragility rises exponentially. This is more often than not initially obscured by rising market prices. But, as Mauboussin points out “crowded trades work until they don’t” and eventually an incremental change in diversity will lead to an outsized drop in market price. This is the age-old liquidity problem. When a large portion of the market is using the same buy and sell rules there conversely becomes a disproportionately small population to sell into and the market needs to drop significantly for prices to clear.

- Lastly, the model highlights the importance of understanding how beliefs propagate across a network. Like a disease, a belief’s level of virality is based on its contagiousness (how compelling it is), its degree of interaction (how many high-density nodes in a network adopt it), and the degree of recovery (how supported is the belief by the unfolding reality).

The Palindrome George Soros was perhaps one of the best at playing the player and identifying these belief-diversity cascades when in his prime. He applied an entirely new vocabulary to financial markets with terms like reflexivity, feedback loops, false trends and so on.

Soros would break down reality into three sub-categories:

- Things that are true

- Things that are untrue

- And things that are reflexive

He said that “Economic history is a never-ending series of episodes based on falsehoods and lies, not truths. It represents the path to big money. The object is to recognize the trend whose premise is false, ride that trend and step off before it is discredited.”

Soros was exceptional at reading where the market was in its pendulum swing (i.e., gauging the level of extremity of consensus narratives and their subsequent positioning) relative to the quality of assumptions in which they are based on (true, untrue, reflexive).

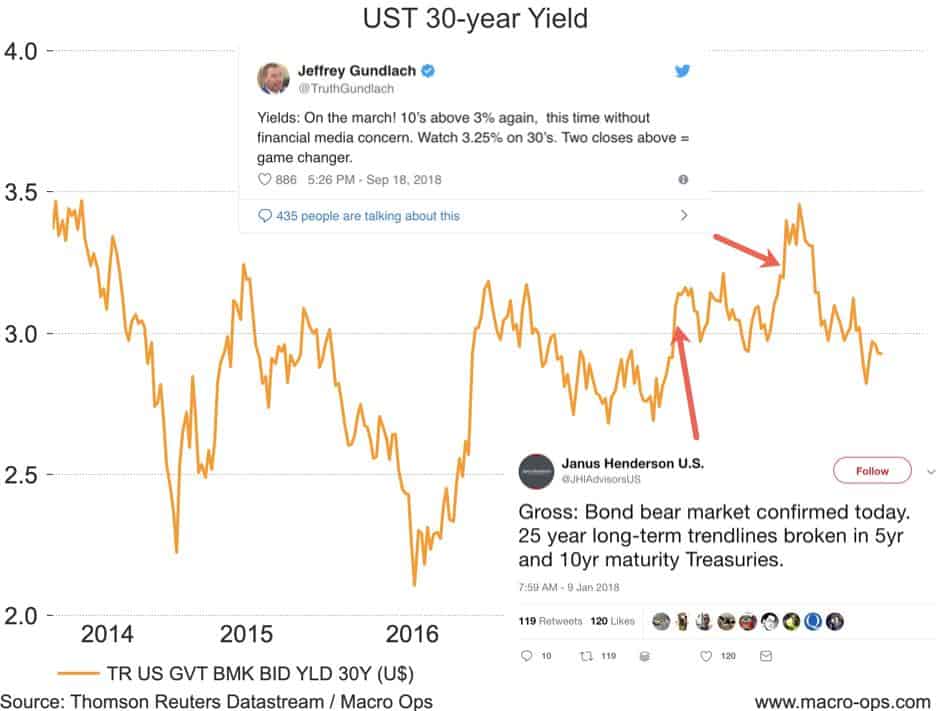

An example of the type of pendulum swing Soros would try to exploit is the clear narrative shift in bonds last year.

Remember back in the middle of 18’ how the popular belief had become that “we’re in a new secular bear market in bonds”.

Both “Bond Kings” we’re shouting about the “game changer” in rates….

Here’s a few excerpts from a Bloomberg article in October of last year when the bearish bond narrative reached its pitch — which also happened to be right when yields peaked. The article is aptly named “Bond Bears Popping Champagne Say U.S. Yields Have Room to Rise”.

Thirty-year Treasury yields pushed above the 3.25 percent level that fixed-income veteran Jeffrey Gundlach identified as a “game changer.”

“Solid data releases, higher oil prices and a technical backdrop that suggests there are not a lot of obstacles for yields to continue to push higher will have many wondering how far this new push higher can go,” said Rodrigo Catril, a Sydney-based strategist at National Australia Bank Ltd.

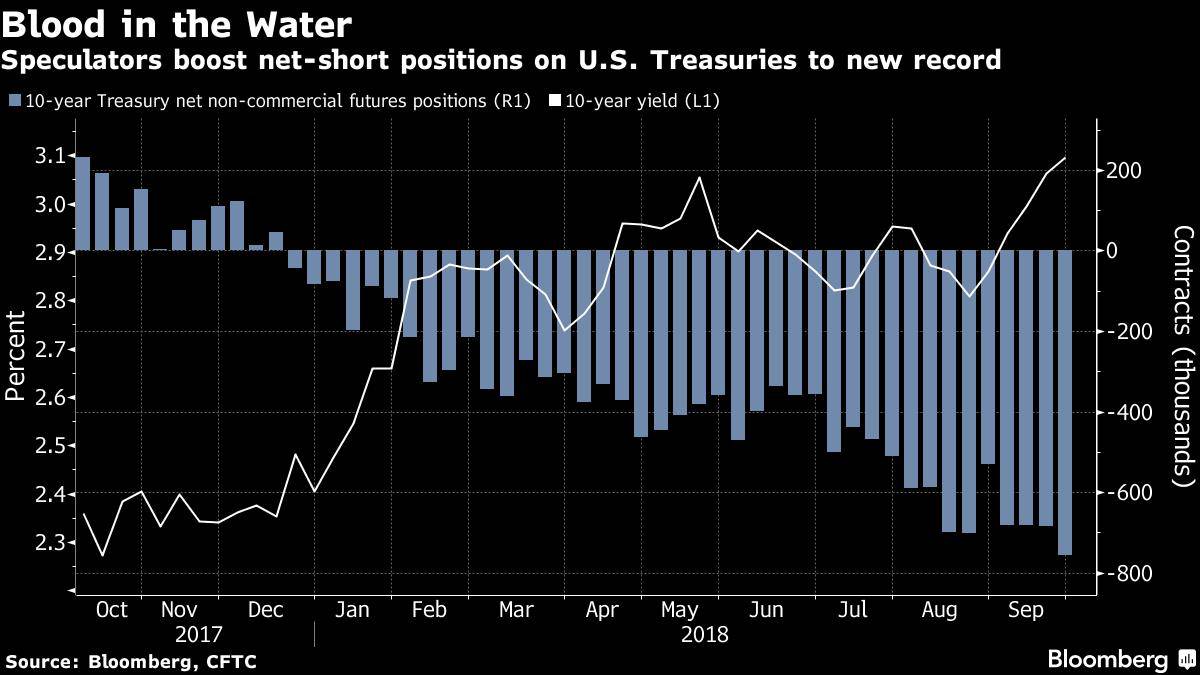

Short sellers were already positioned for more pain in the Treasury market. Speculative net short positions on 10-year notes climbed to a record, the most recent Commodity Futures Trading Commission data showed. An update to those figures comes Friday.

“In hindsight, we wish we were even shorter on U.S. rates,” said Raymond Lee, a fund manager at Kapstream Capital Pty in Sydney.

“That gradual withdrawal of liquidity is causing yields to rise,” Bob Baur, chief global economist at Principal Global Investors, said in an interview with Bloomberg Television in Tokyo Thursday. “We look for 10-year Treasury yields to hit 3.5 percent at some point — later this year, early next year — and I think that’s going to be a real problem for stock markets.”

The famous speculator of the early 20th century, Bernard Baruch, used to say “Something that everyone knows isn’t worth anything.”

The “Bond Bear” narrative was predicated on a false trend. It wasn’t a sustainable move. Our leveraged balance sheets combined with a decelerating China and a responsive Fed ensured it. Crowding in both positioning and narrative combined with a textbook technical breakout in late October made for a perfect buying opportunity — something we pitched in our November MIR at the time.

Not only was the move in bonds not much of a “Game Changer…” but it was also clearly a local extreme on the swing of the pendulum. The narrative was on the front pages of ALL the financial newspapers and shared by nearly ALL the talking heads on CNBC.

And how quickly that narrative pendulum has swung back. It’s now accepted wisdom that yields won’t and can’t rise. The global economy is simply too weak and the Fed too dovish… Subsequently, investors have been stampeding in droves into bonds since the beginning of the year. More on this in a minute.

Something that everyone knows isn’t worth anything…

Equity markets too, have seen a full swing of the pendulum over the last six months. Back at the end of December when we put out a number of reports explaining why it was an excellent time to buy, the dominant belief was that a vicious bear market had started and a recession was around the corner.

I mean, the Yield Curve had inverted!!!! Everybody was fretting about the yield curve and a recent drop in retail sales…

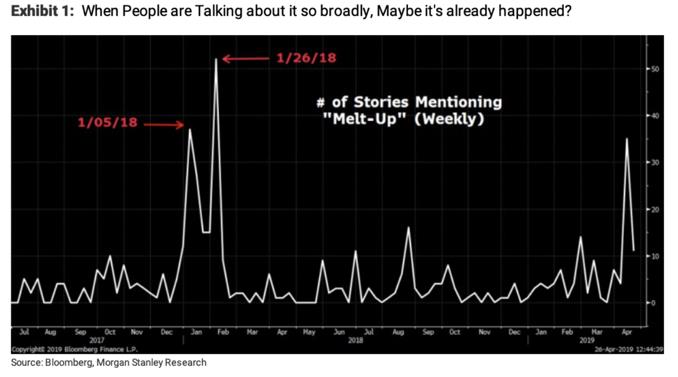

Five months and a vertical runup in stocks later and there’s hardly a whisper of either. Now, the talk is of a Fed Put, a low growth low inflation Goldilocks economy, and a Melt-Up in equities.

One more time: Something that everyone knows isn’t worth anything…

Viewing markets — also history, politics, culture, and on and on — through the lens of a swinging pendulum is a useful heuristic. Look for local extremes and compare it to alternative possible outcomes, ones that aren’t being discounted by the market. Then wait for a break in the technicals and you have yourself a trade.

Doing this, you’ll find that the market, especially when at pendular extremes, is more often than not suffering from acute myopia. It tends to overly discount what’s happening now while not accounting for a future that could look any different than today.

Stanley Druckenmiller (aka The GOAT) put it like this:

[My] job for 30 years was to anticipate changes in the economic trends that were not expected by others, and, therefore not yet reflected in security prices.

Too many investors look at the present; the present is already in the price. You’ve got to think out of the box and visualize 18 to 24 months from now what the world is going to be and what (level) securities might trade at… what a company has been earning doesn’t mean anything, what you’ve got to look at is what people think a company’s going to earn and if you can see something in 2 years that’s going to be entirely different than the conventional wisdom, that’s how you make money.