Markets don’t make sense. The Druck is as confused as the rest of us. Nobody knows why companies with $0 in revenue trade at $20B valuations. And like that, the S&P is back to where it was before the COVID-19 sell-off.

Just as everyone predicted.

If there’s anything we know about markets it’s that we can’t predict. We shouldn’t spend time thinking about predicting them. Nor should we banter over Twitter about where the S&P will trade by the end of the year.

Nobody cares and it doesn’t help us make money on individual stock selection / investment.

Anyways, off my soapbox and on with the regularly scheduled programming.

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- Stock-Based Compensation in Tech Companies

- A DIY S&P 500 Valuation

- GMO Q1 2020 Letter

We get technical in this issue so both hands inside the cart at all times!

—

June 10th, 2020

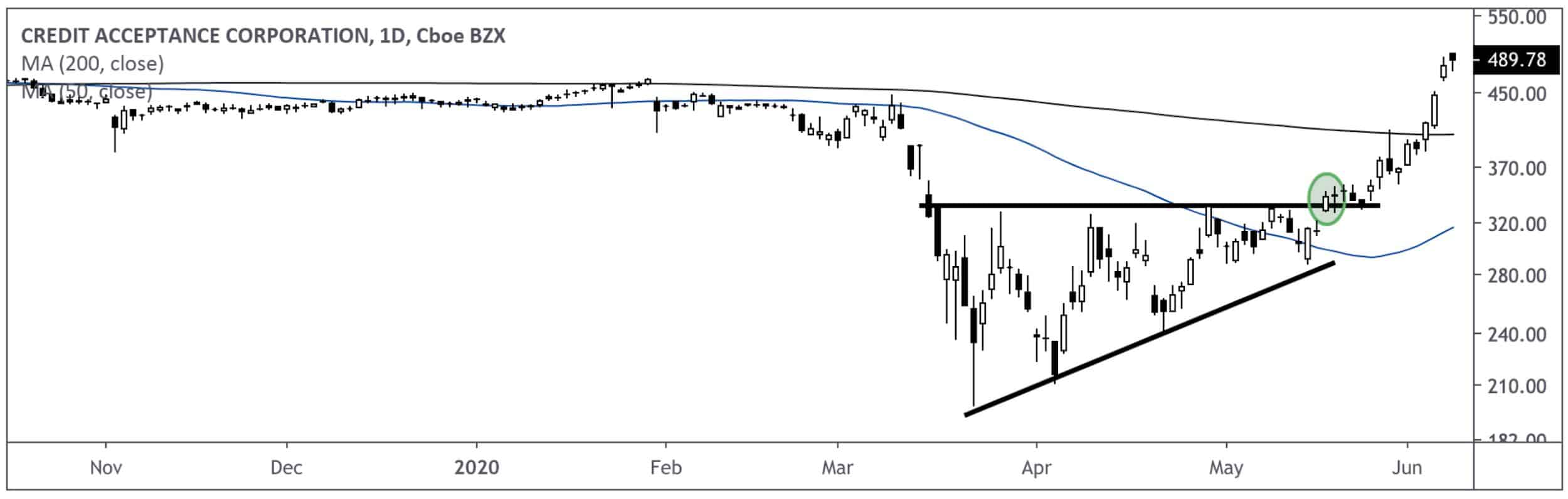

Winner Of The Week: Some of you know I run a premium Breakout Alerts service. Each week we send 6-7 potential breakout trades for the week(s) ahead. We recently closed on our largest winner yet: Credit Acceptance Corp (CACC).

Here’s the chart. Those that took this trade rode it for a near 5R (5% return on risk capital):

I’m sure Robert Vinall of RV Capital is thrilled with how CACC’s played out.

__________________________________________________________________________

Investor Spotlight: GMO Q1 2020 Letter

GIFs by tenor

GIFs by tenor

GMO Capital released their Q1 2020 letter and it’s a doozy. I love their Focused Equity portfolio and their thoughts on global valuations. Here’s the link to read the entire report.

Ben Inker, head of Asset Allocation at GMO starts the letter saying (emphasis mine):

“Our job is to try to understand the impacts of those scenarios on the assets we forecast and put together a portfolio that gives an attractive outcome in as many scenarios as we can manage.”

I can’t stress enough how important it is to ponder alternative realities to the ones we’re currently facing. From there, we can probabilistically weigh those alternative realities and determine how to profit.

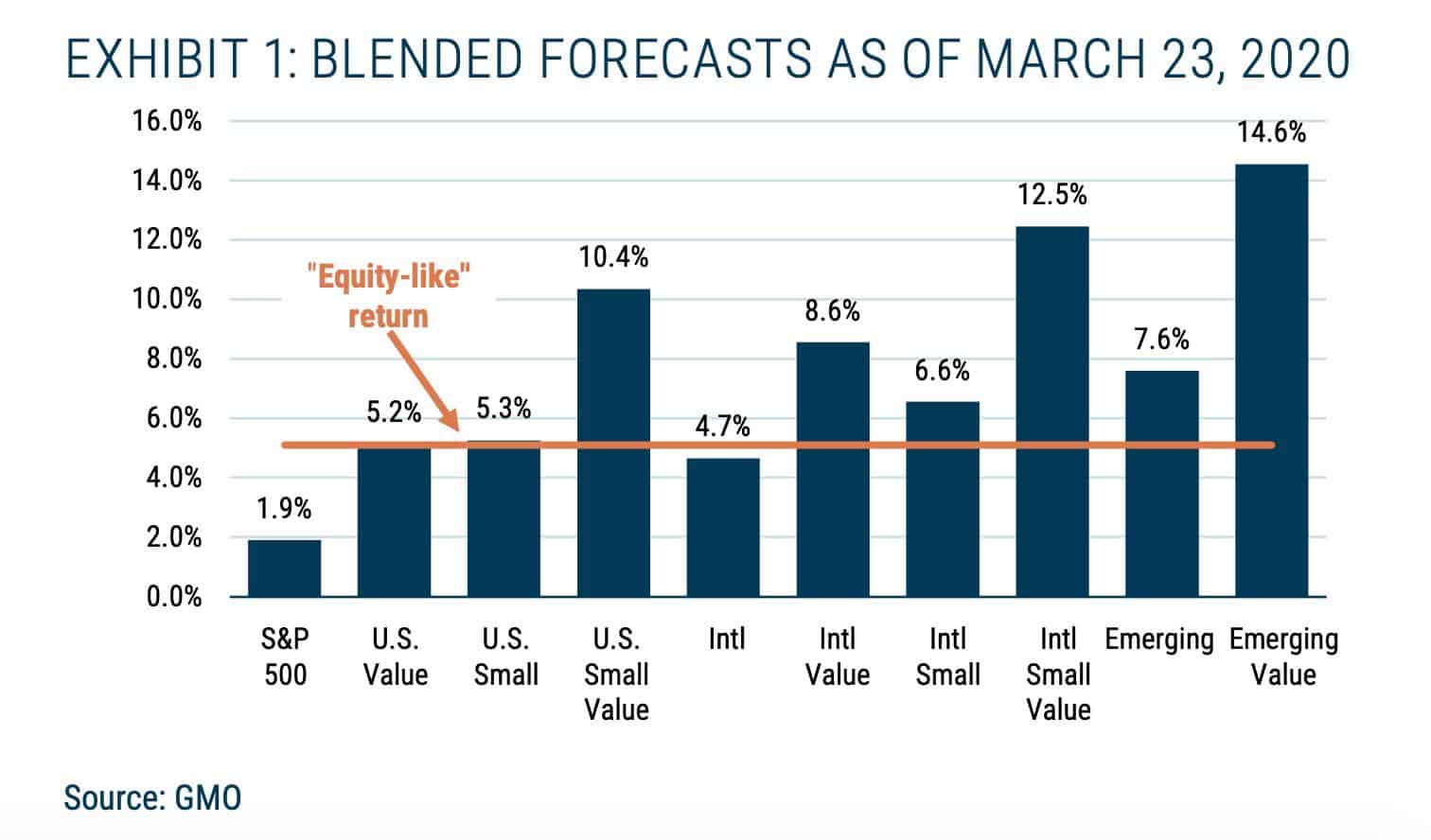

Inker then reveals GMO’s equity forecast from March 23, 2020:

There’s a few things to note:

-

- Emerging stocks look like they’re about to crush it

- S&P 500’s returns going forward look abysmal

- Value-based stocks in all categories should do better than their counterparties

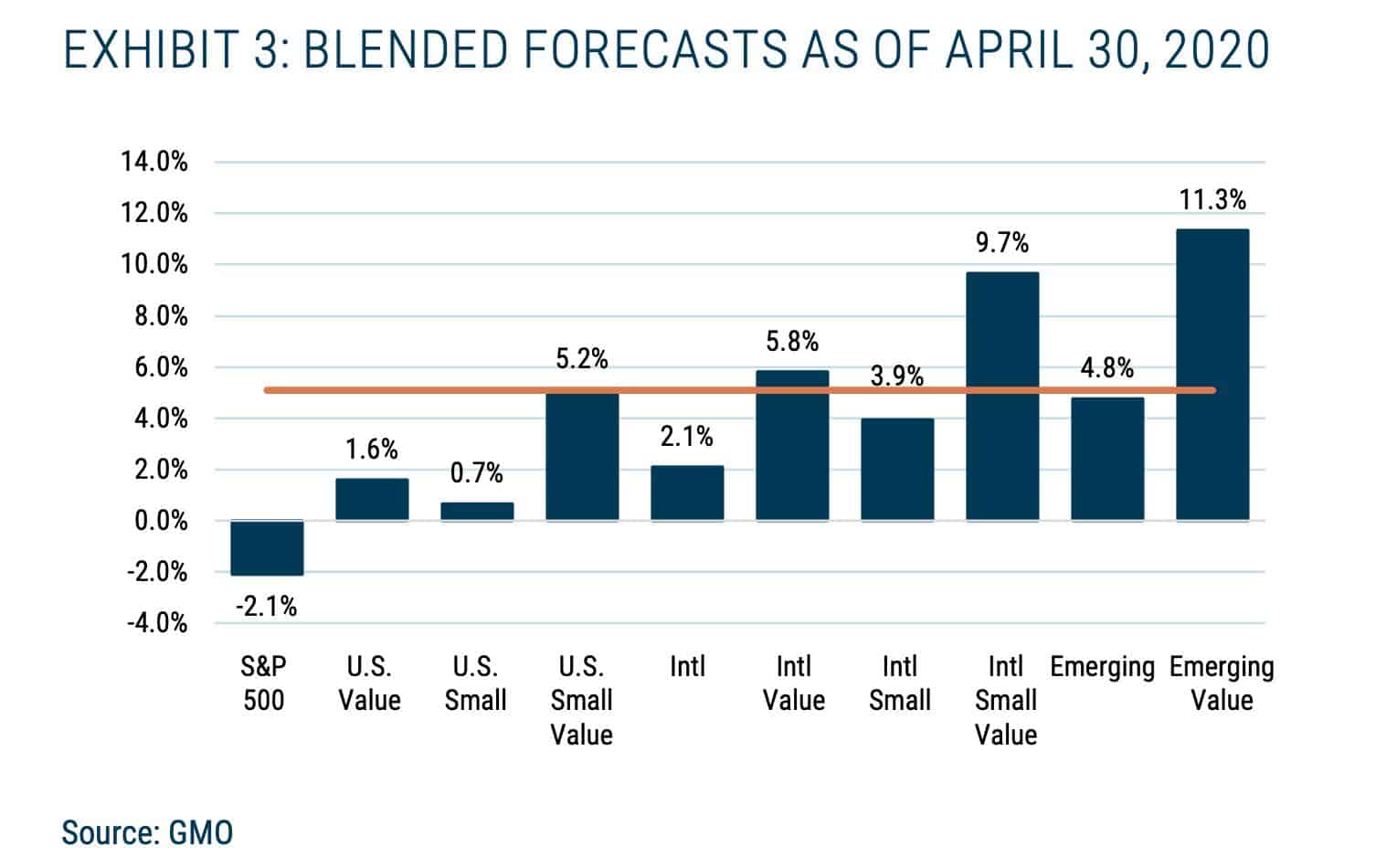

But then the rally came. This recent rally pulled equity returns forward. In some cases almost a decade forward. Inker explains in more detail (emphasis mine):

“To put the rally in perspective, the group that went up the least, International Value stocks, earned the equivalent of 4.4 years of an “equity-like” return for a fair-valued group of stocks. U.S. large and small cap stocks rose the equivalent of 6 years of “equity-like” returns.”

The GMO re-ran the equity projections after the run-up. Check out the difference:

Now we see a few things:

-

- S&P 500 forward returns are negative

- US stocks projected to significantly underperform their global counterparts

- Value stocks should provide decent returns across US, international and emerging markets

Here’s Inker’s thoughts on this (emphasis mine):

“But while the ability of some of these economies to handle the crisis well is helpful, the primary reason we believe emerging stocks should give a higher return is simply that they are trading at much lower valuations, which leaves significant room for normalized earnings to fall while still providing a good return to shareholders. Emerging market value stocks are far cheaper still, and today seem priced to offer a double-digit expected return in a GFCx2.”

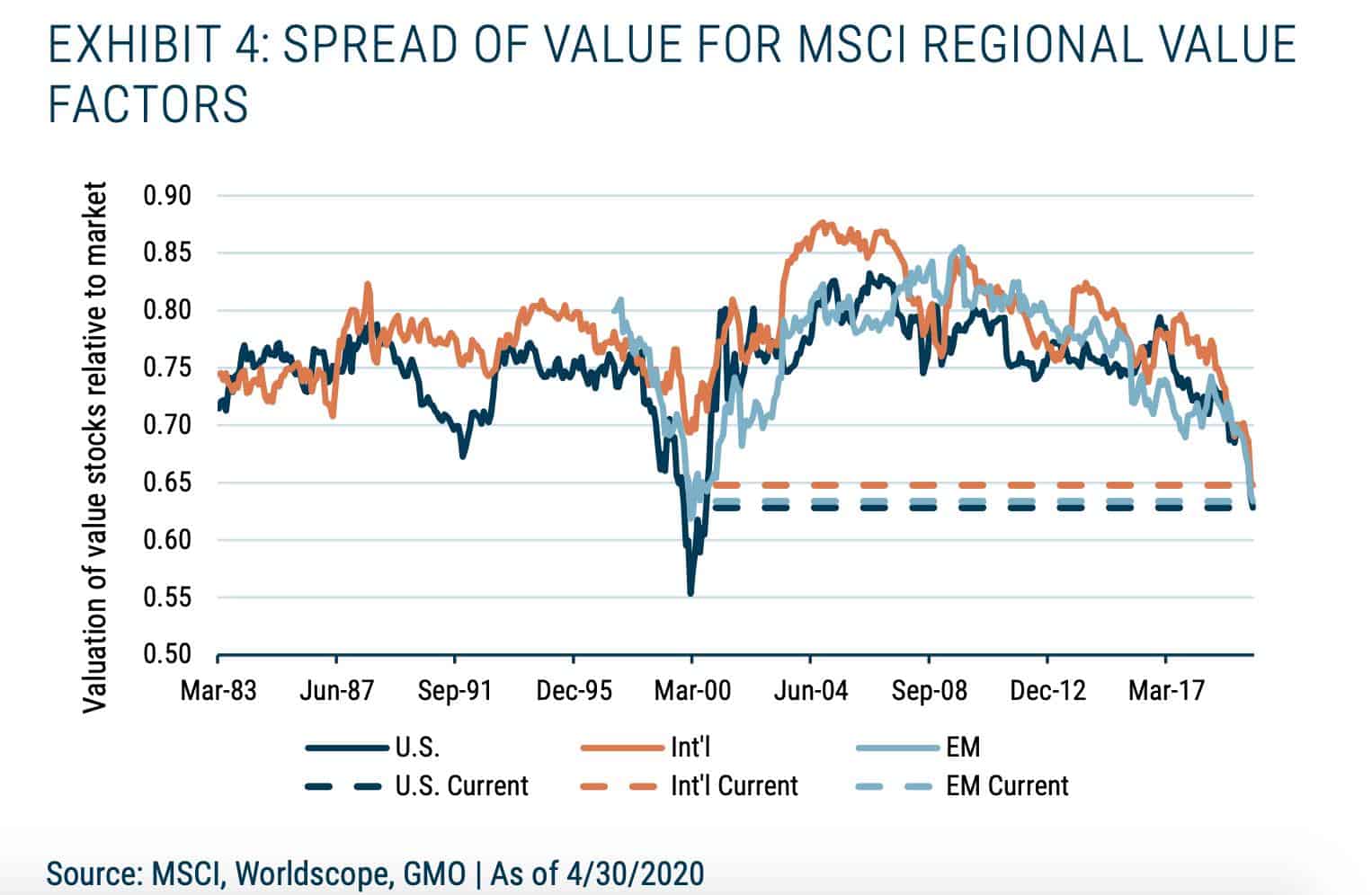

Finally, Inker highlights the massive disconnect between value-based valuations and other indicators:

The above chart shows value stocks at their largest discount relative to the overall market since the 1999-2000 dot-com bubble.

How To Play This:

-

- Look overseas (Italy, Portugal, France, Spain, Poland, etc.)

- Look for value stocks (beaten down YTD returns, cyclicals, left-for-dead)

- Have the stomach to buy them

__________________________________________________________________________

Movers & Shakers: Accounting For Stock-Based Compensation

I stumbled upon Tanay Jaipuria’s Substack this week and I’m glad I did. His newsletter focuses primarily on tech and business/investing. If you’re going to read Tanay’s newsletter, start with his post on stock-based compensation.

Tanay’s Claim: Stock-Based Compensation Hides Unprofitability

For starters, stock-based compensation is simply compensation in the form of options on company stock or restricted stock units (RSU’s). These compensation packages are contingent on certain internal factors like revenue growth, customer growth, etc.

Tanay describes three main benefits of stock-based compensation:

-

- Offer employees and management skin in the game

- Help retain employees since most SBC vests in four years

- Allow cash-poor companies to preserve cash while offering compensation to key employees

To Expense or Not To Expense

It wasn’t until 2004 that GAAP required expensing stock-based compensation. Here’s how the expense works (from the article): Value stock options based on their fair value and record them as an expense on their grant date.

Easy enough. Yet most high-flying tech companies choose to report non-GAAP financials which remove stock-based compensation from the income statement.

Does It Even Matter?

A natural question follows: “Does SBC even matter to overall profitability?” In the case of popular tech-stocks the answer is yes!

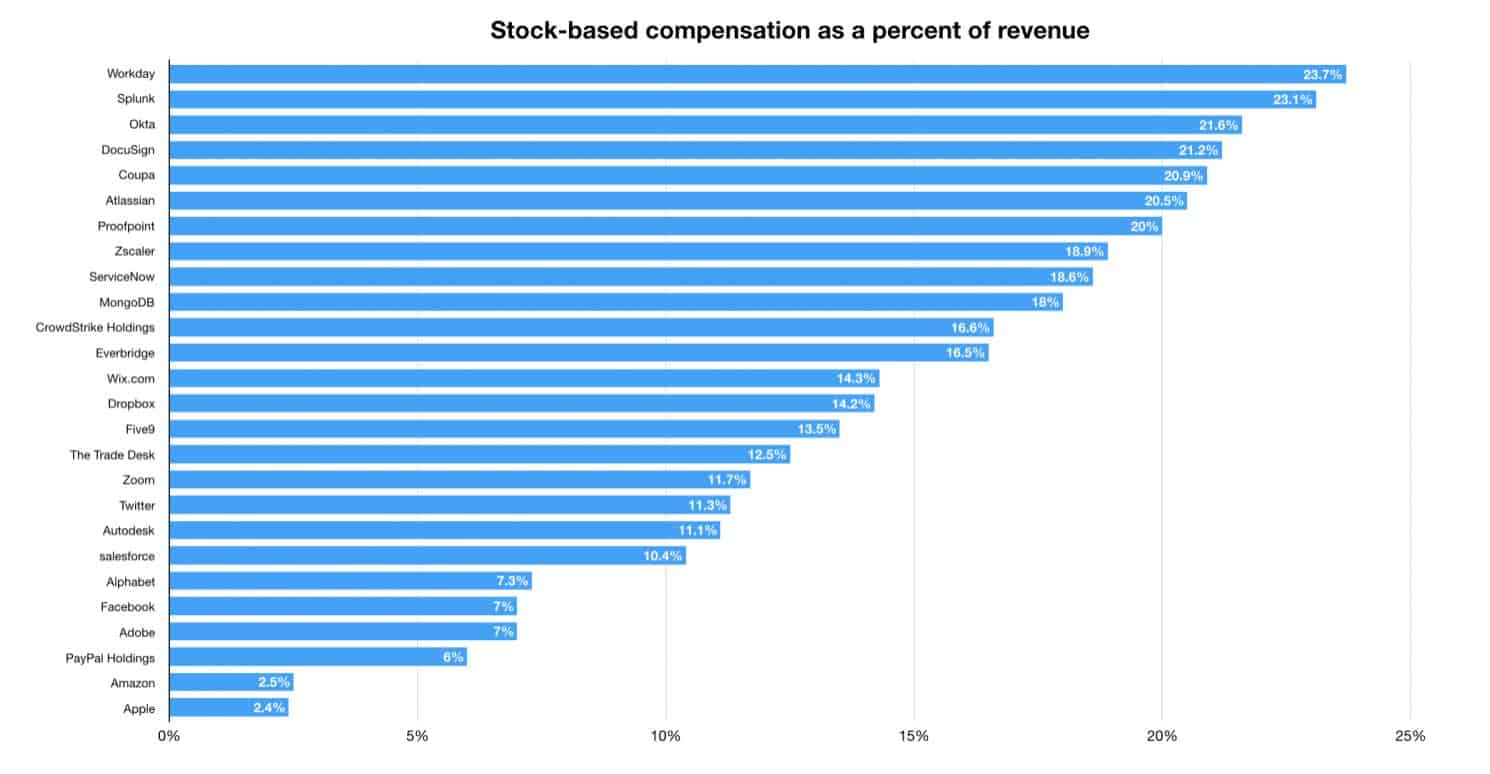

Check out the graph below where Tanay shows the SBC as a % of revenues for various tech companies:

Workday (WDAY), Okta (OKTA), Splunk (SPLK) and Coupa (COUP) all have SBC that’s over 20% of their revenues.

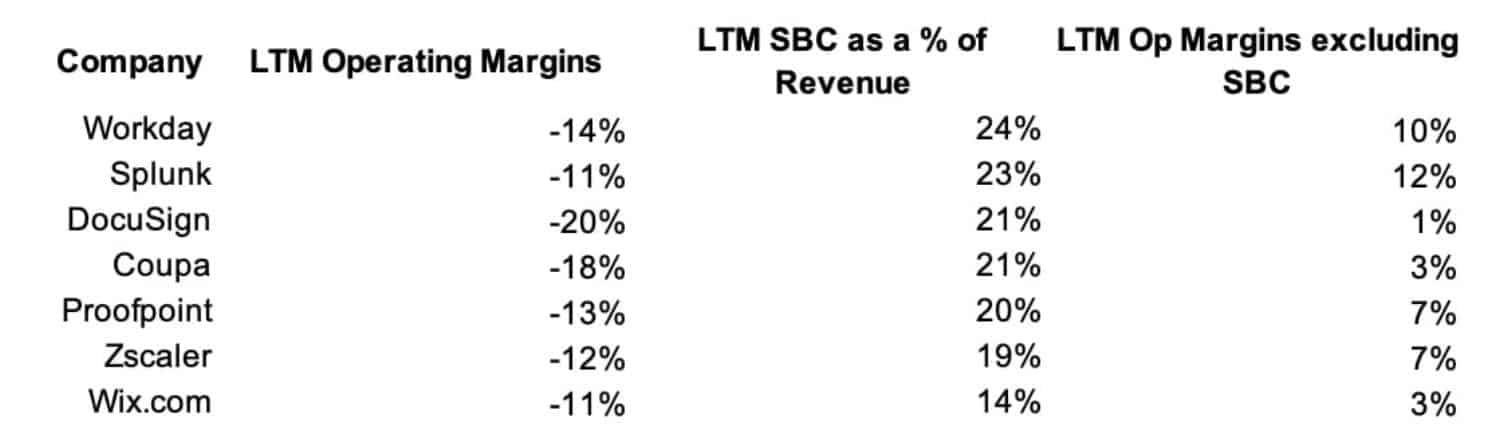

For these companies, SBC inclusion/exclusion is the difference between profitable and not-profitable (from the newsletter):

What Should We Do?

Faced with a value-investing conundrum, I ask myself WWWD? What Would Warren Do? Expense it of course (emphasis mine):

“If options aren’t a form of compensation, what are they? If compensation isn’t an expense, what is it? And, if expenses shouldn’t go into the calculation of earnings, where in the world should they go?”

Tanay includes excerpts from companies like Facebook (FB) and Alphabet (GOOGL) that encourage the use of SBC in their profitability reports.

When in doubt — include the SBC expense. Even if the company doesn’t have to pay the employees options today or issue them restricted stock today, they will at some point. So you might as well start modeling for it.

__________________________________________________________________________

The Weekly Dam: A DIY Valuation of S&P 500

Our valuation OG is back with another great blog post! This week Aswath Damodaran breaks down a do-it-yourself valuation of the S&P 500.

Step 1: Start with earnings

Damodaran starts with the earnings estimates for the S&P over the next two years (see below):

No surprise in 2020’s drop.

Step 2: Focus on Cash Returns

Let’s go back to the blog post (emphasis mine): “As with earnings, this crisis will result in cash flow shocks, and dividends and buybacks will drop this year. Given that dividends tend to be stickier than buybacks, the drop will be lower from the former than the latter. Analysts vary on how much, though, with a range of a drop of 30-70% in buybacks and 10-30% in dividends.”

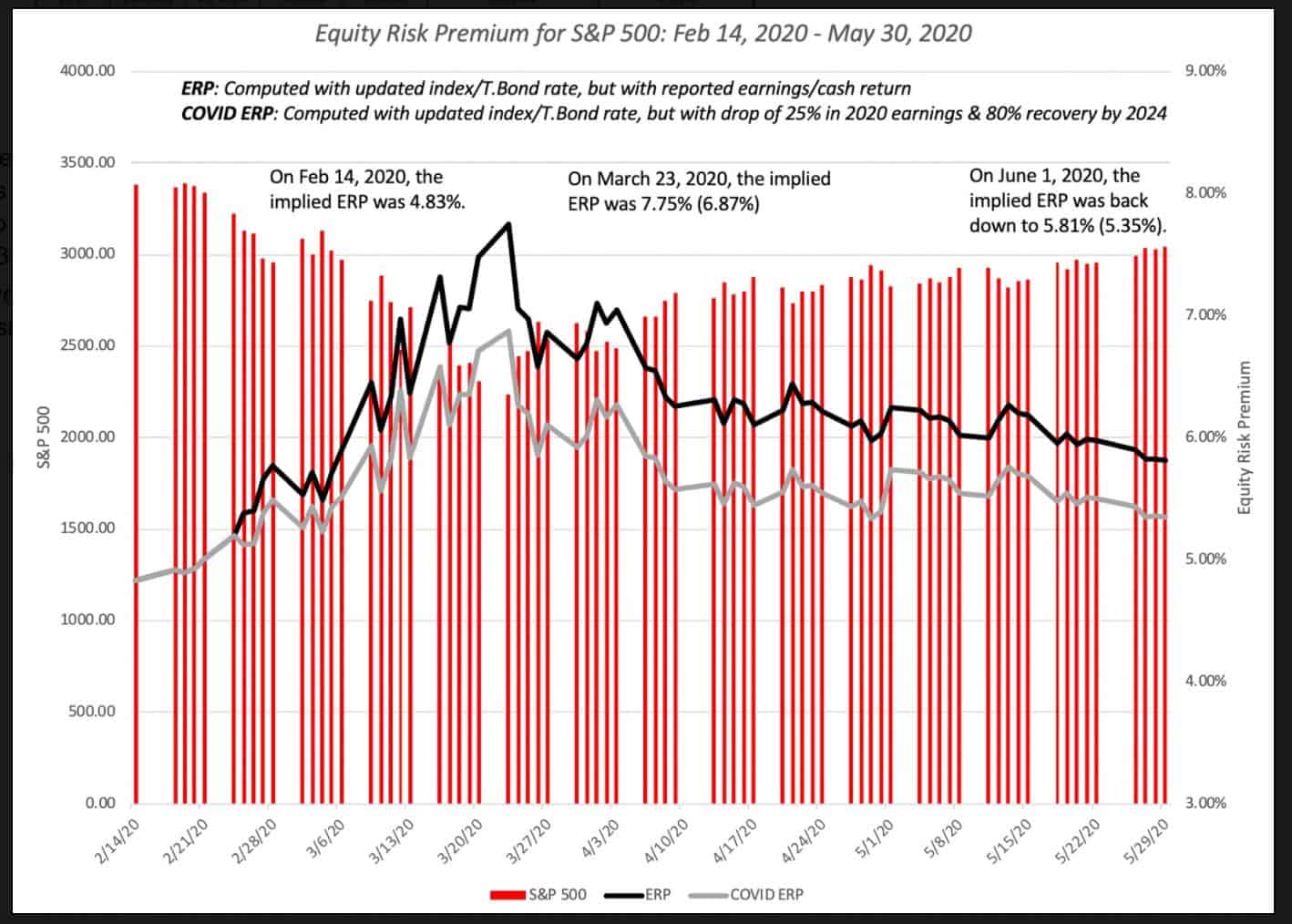

Step 3: Estimate Risk Premium

Check out this graph for risk premium dating back to February 2020 (the beginning of the crisis):

According to Damodaran’s estimates, the equity risk premium is down to 5.81%.

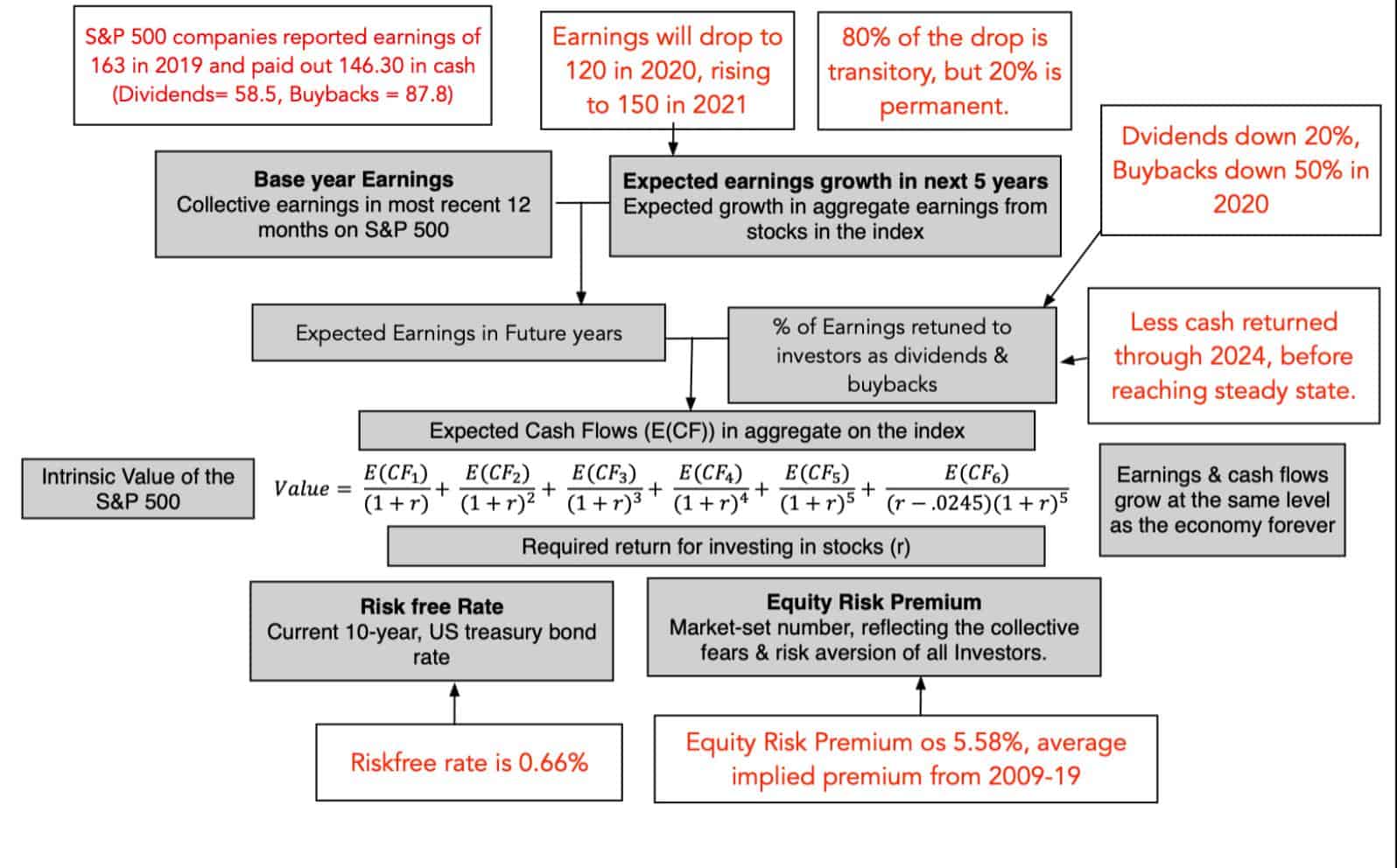

Putting It All Together

The final step is to put numbers behind each part of our story. Damodaran does this for us:

The result: “With these assumptions, I can value the index and I capture the valuation in the picture below. My estimated value for the index is about 2926, which would lead to a judgment that the index was over valued by about 6% (based upon the level on June 1, 2020).”

An overvaluation of ~6% isn’t much. But that was as of June 1st. The market’s risen almost 6% since then. All things equal we’re looking at ~12% overvalued now.

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!