“The object of skilled investment should be to defeat the dark forces of time and ignorance which envelop our future. The actual, private object of the most skilled investment today is ‘to beat the gun’, as the Americans so well express it, to outwit the crowd, to pass the bad, or depreciating half-crown to the other fellow.

“This battle of wits to anticipate the basis of conventional valuation a few months hence … does not even require gulls amongst the public to feed the maws of the professional; it can be played amongst the professionals themselves. Nor is it necessary that anyone should keep his simple faith in the conventional basis of valuation having any genuine long-term validity. For it is, so to speak, a game of Snap, of Old Maid, of Musical Chairs — a pastime in which he is victor who says Snap neither too soon nor too late, who passes the Old Maid to his neighbor before the game is over, who secures a chair for himself when the music stops. The game can be played with zest and enjoyment, though all the players know that it is the Old Maid which is circulating, or that when the music stops some of the players will be unseated.” ~ John Maynard Keynes (h/t DerivativeMusings)

Good morning!

In this week’s Dirty Dozen [CHART PACK] we discuss the implications of more fiscal on the market, then talk some inflation and what it may mean for the highly valued tech sector, before going over the continued outperformance of value over growth and end with an auto and Ag-tech play, plus more…

Let’s dive in.

***click charts to enlarge***

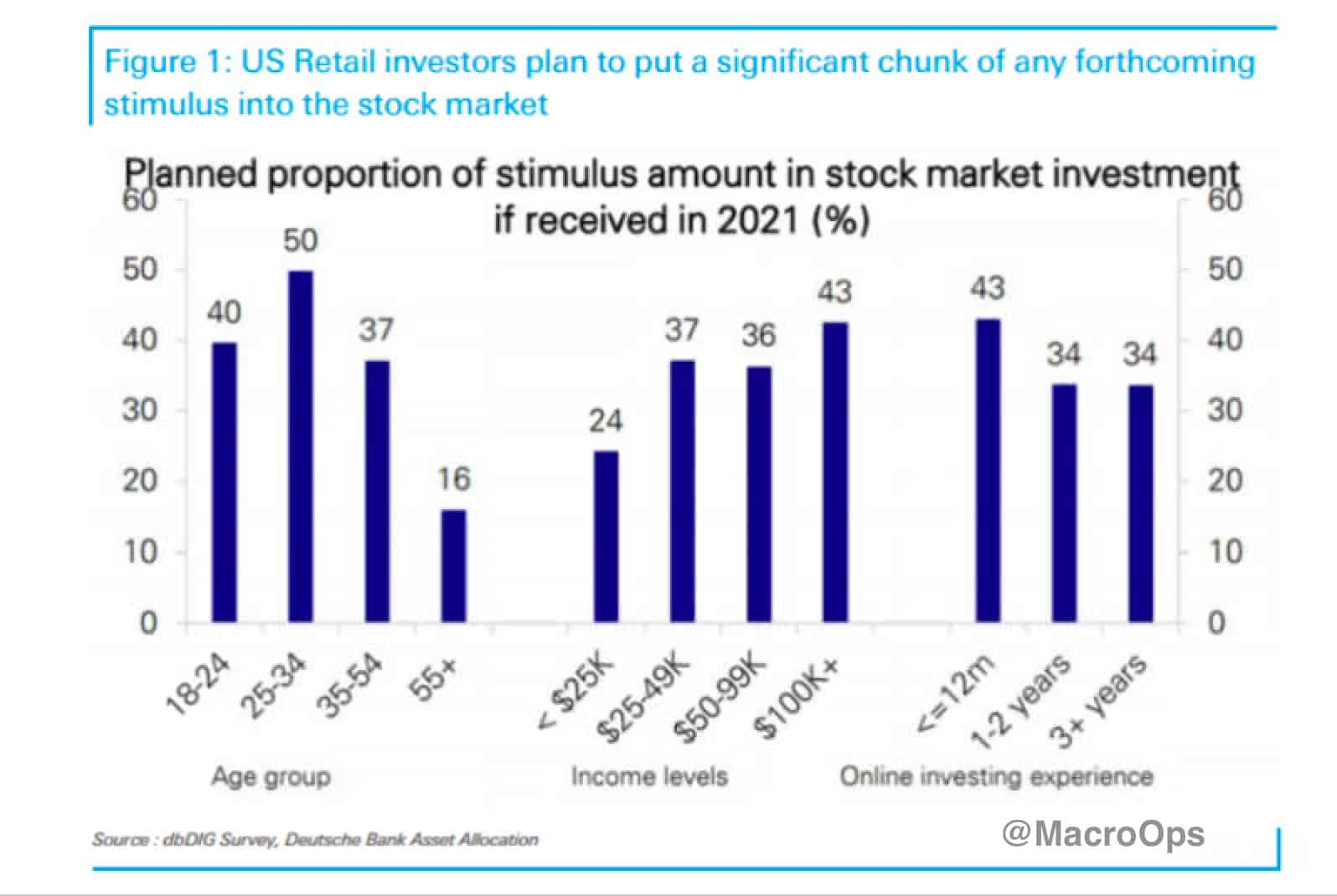

1.Stimulus will be hitting the checking accounts of the Redditt Brigade in the near future. According to a survey by Deutsche Bank and noted by Bloomberg, “Individuals age 25 to 34 with online brokerage accounts plan to use about 50% of their stimulus to buy stocks.”

As I wrote back in early Jan, fiscal is the ultimate cheat code for the economy and markets. This is a structural wave that we want to surf, not swim against. With that said, I expect there to be wide dispersion in returns across the market so pick your stocks wisely.

- The inflationistas who approach the “analyses” of inflation with a religious zeal that would make the most truculent extremist blush, are back at it again… They’re calling for more inflation, of course. Nevermind the fact that these people have been wrong year in and year out for the last decade, or that they haven’t changed their framework for analyzing why this time will be different (if they have a framework at all). Some people just can’t help themselves it seems…

We at MO expect somewhat higher inflation later this year due to transitory effects. And it’s possible these transitory drivers are replaced with stickier cyclical ones next year. But… when analyzing something as complex as longer-term inflation dynamics it’s ridiculous to make high-conviction predictions, especially when structural disinflationary dynamics persist.

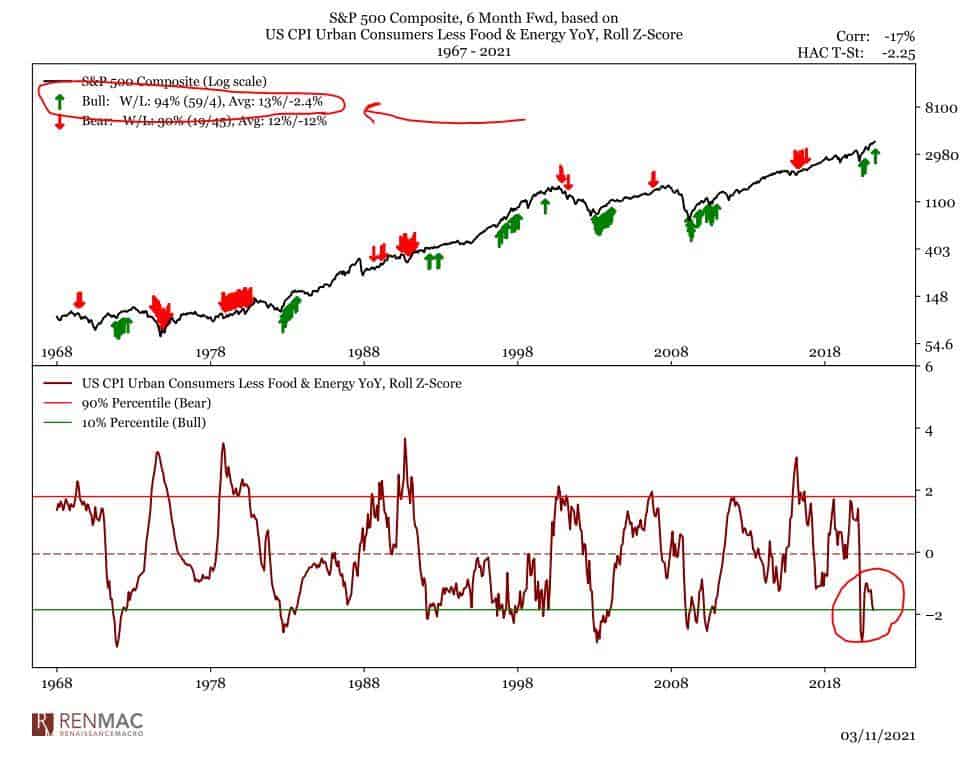

@RenMacLLC tweeted similar thoughts last week, saying “The importance of inflation on equity performance can’t be over-emphasized. Yes it’s a daisy-chain, yes it will be noisy in the interim, but the data remains supportive, and importantly the expectations for higher inflation are so (can we say?) ‘inflated’.”

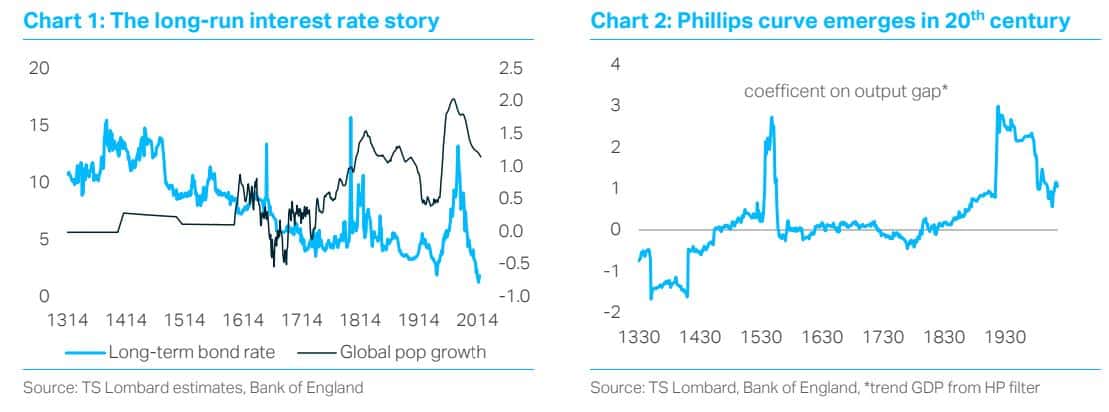

- TS Lombard tackles the inflation question in this recent post. Here’s a clip and a chart.

“The Fed, ECB, etc. can all desire higher inflation – a welcome shift from their deflation bias of the last 30 years – but unless there is a secular increase in r*, they will struggle to achieve this outcome. The problem today is that it’s not entirely clear how those secular inflation forces will evolve. Demographics are changing, with an inflection point in the share of the population who are spenders rather than savers. Older people save less. But the “militancy” of the late-1960s/1970s isn’t going to return…”

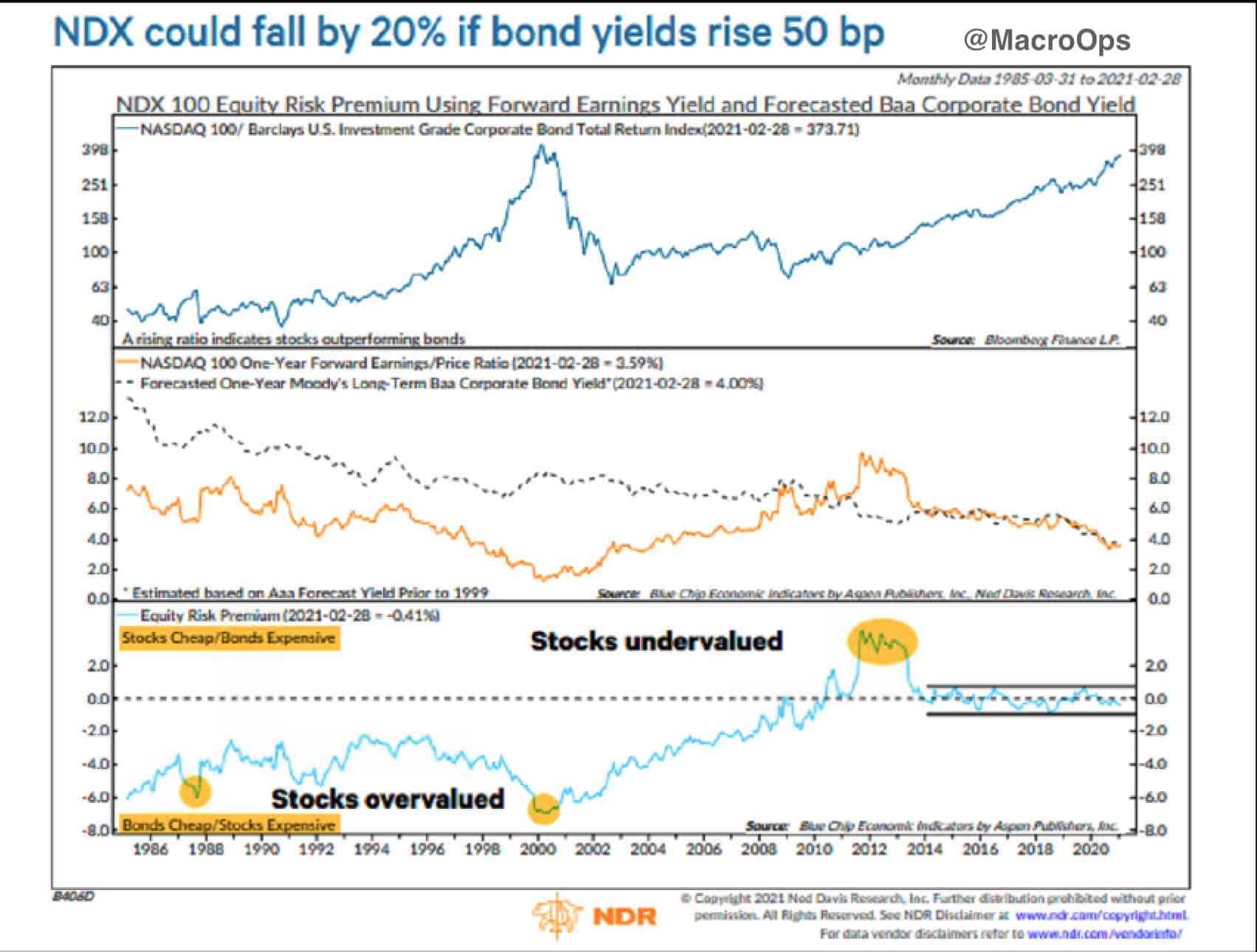

- The inflation question matters for many reasons, one of them being its impact on yields. Bloomberg writes “Joe Kalish, chief global macro strategist at Ned Davis Research, found that since 2014, the Nasdaq 100’s forward earnings yield — the inverse of its price-earnings ratio where the higher it is, the cheaper stocks are — has moved almost in lockstep with forecast corporate bond rates.

“In his model, if 10-year Treasury yields rise to 2% this year, that in turn could drive long-term Baa-rated bond rates to 4.5%, a scenario where the Nasdaq 100 would have to drop as much as 20% to stay attractive, all else equal. If yields climbed but the Nasdaq didn’t move, this would indicate over-valuation, Kalish said, adding his model correctly flashed warnings in 1987 and 2000.”

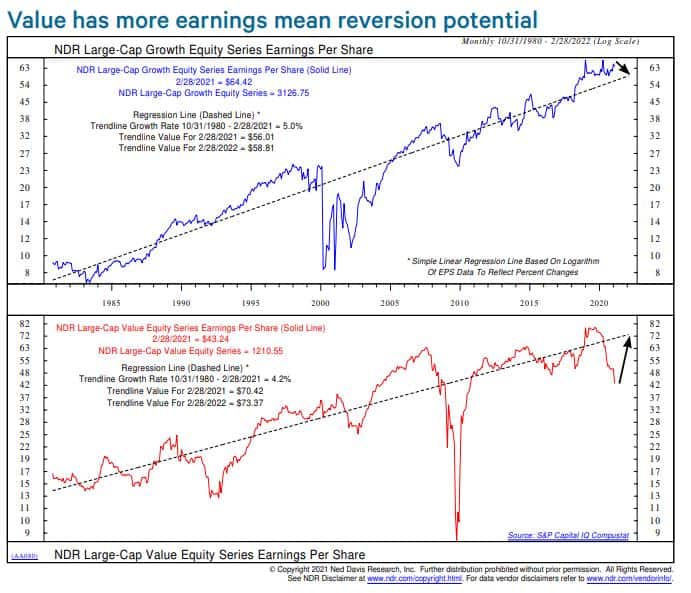

- I believe the recent outperformance of value over growth is just the start of a cyclical trend, and there’s a plenty long runway for this to continue to play out. @edclissold shared the following last week.

“The EPS recovery is in 2021 should be the fastest since 2010, and it’s driven by Value. Our Growth index’s EPS is 15% above trend-line, while Value is 38% below.”

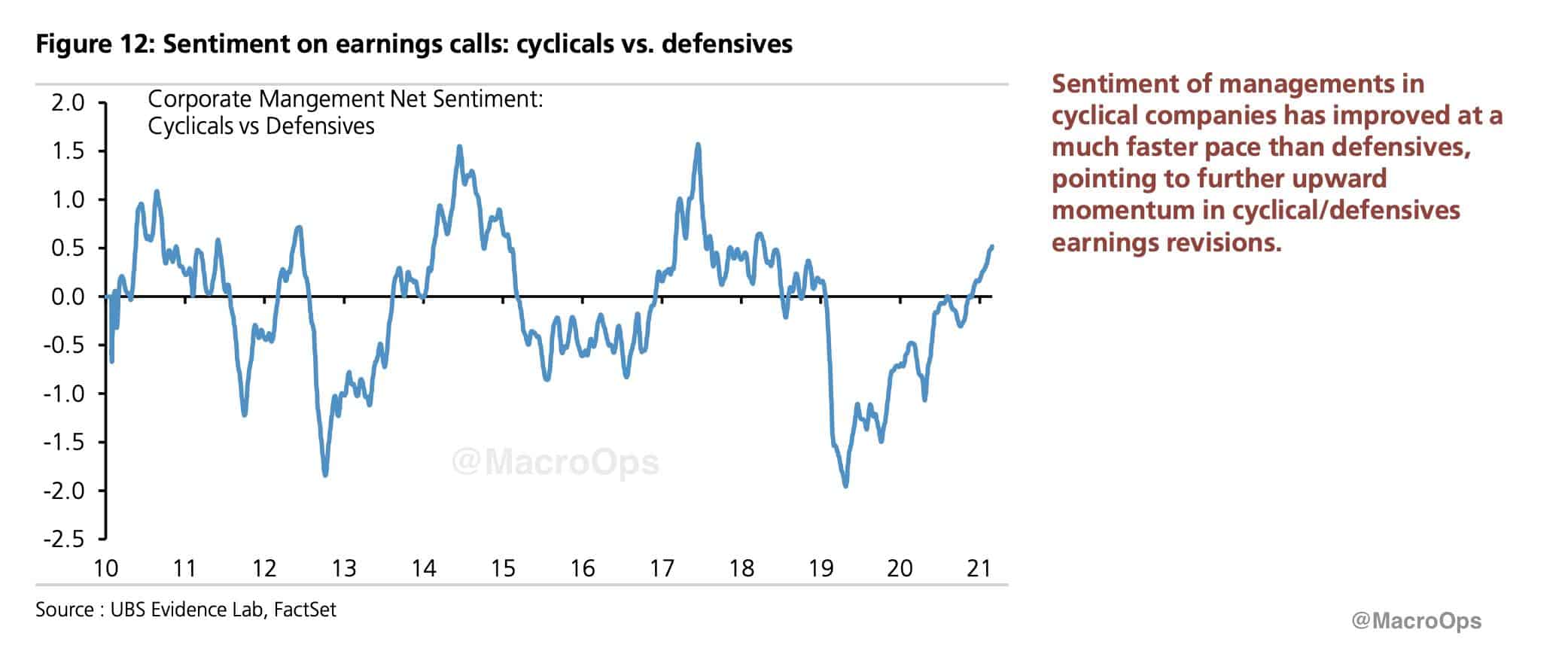

- The following few charts from UBS’s Evidence Lab also support the continued outperformance of the cyclical/value trade.

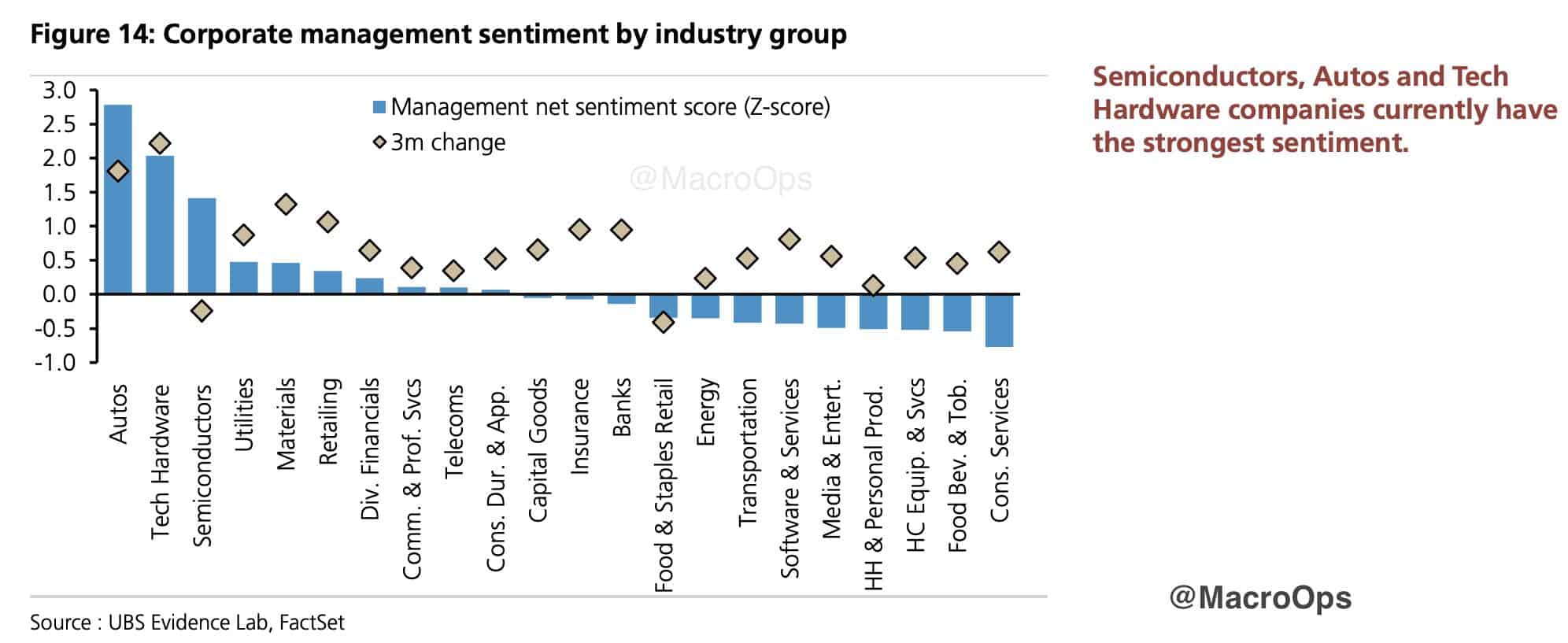

- Here’s the breakdown in corporate management sentiment by industry.

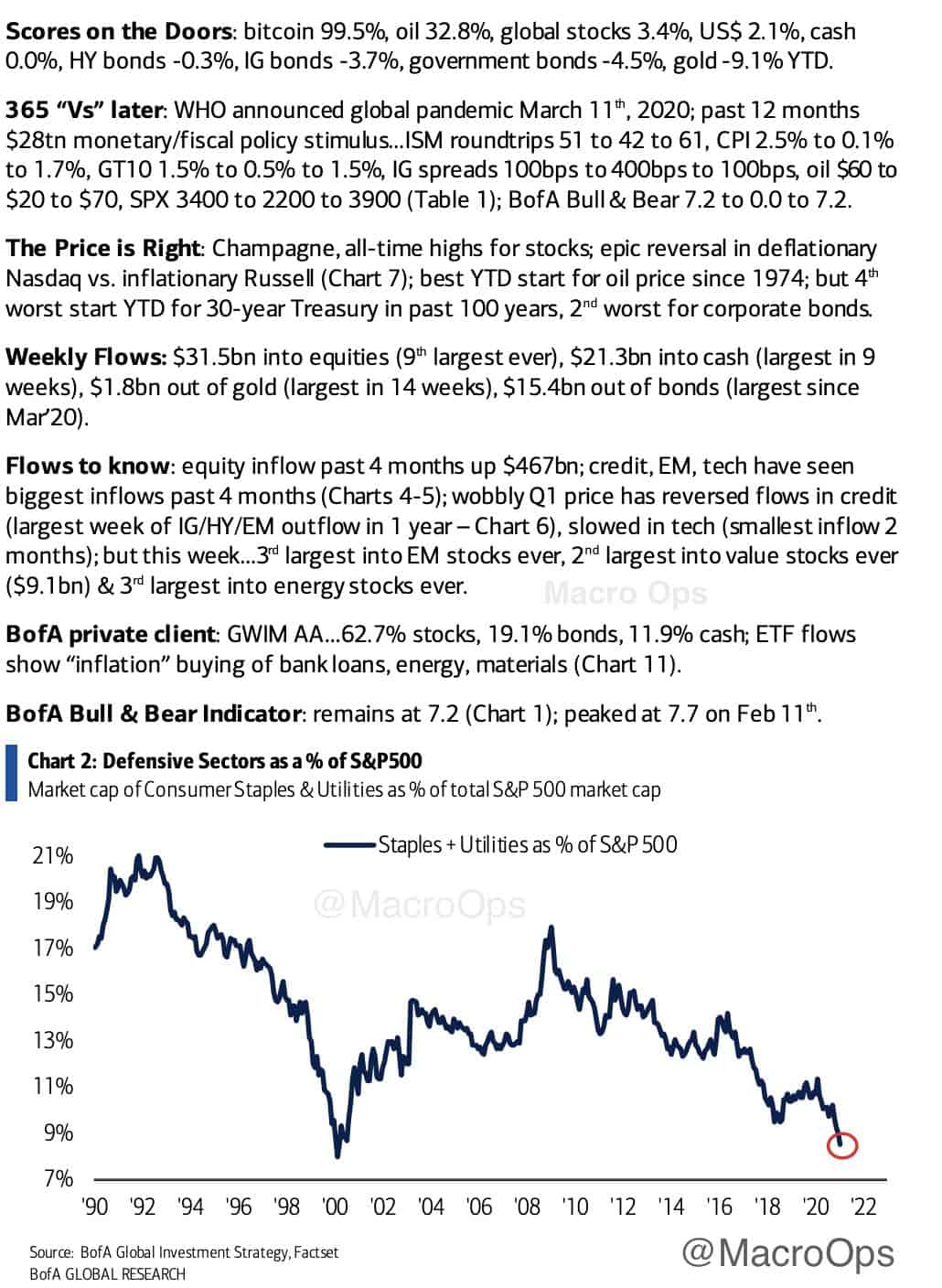

- Here’s BofA’s Flow Show highlights from last week. Standouts: “best YTD start for oil since 1974” and “4th worst start YTD for 30-year Treasury in past 100-years”.

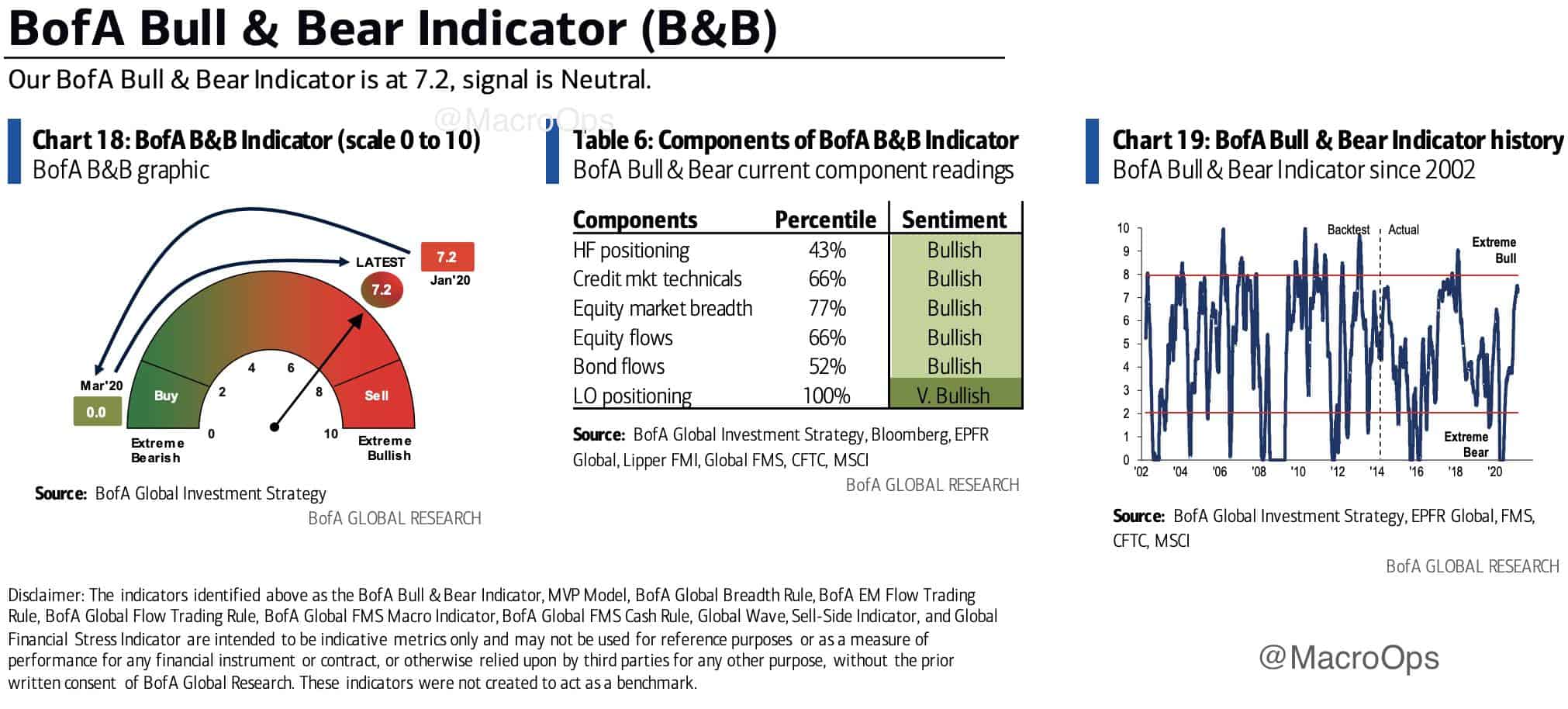

- The Bull & Bear Indicator remains elevated but still below an official sell signal.

- Here’s Sentix with some color on the dollar.

“The US dollar should remain sought after. At least, this is indicated by the strategic bias of EUR-USD, which continues to decline significantly, i.e. it works in favour of the US dollar. We have measured a similar decline in the bias over 6 weeks 14 times. In almost 80% of the cases, EURUSD was lower 8 weeks later. On average by 2.3%.”

If the US dollar is going to retrace it needs to do it soon and convincingly so or else that’ll just speak to the strength of the cyclical USD bear trend.

- Speaking of value, have you looked at GM’s chart lately? It’d been a while since I had and I was a bit surprised to see such bullish technicals.

This is one of my favorite patterns. A massive false bear trap — allowing some whale(s) to accumulate a large position — followed by a face-ripping rally. GM is a leader in self-driving tech and electrification. They’re trading at 0.69x Price-to-Sales. Now, if we just apply a multiple half that of Tesla’s 21x sales then… I kid. But, in all honesty, I’d be interested in maybe playing this on a pullback.

- I pitched this stock back in January when it was trading sub $6.50. It’s an Argentinian Ag-tech play. I’m bullish on the Ag space as a whole and I continue to like this chart.

The company recently received regulatory approval for the company’s “proprietary drought-tolerant HB4 wheat from the Ministry of Agriculture in Argentina, Latin America’s largest wheat producing country”. Which is apparently the world’s first and only drought-tolerant wheat to receive regulatory approval.

Stay safe out there and keep your head on a swivel.