“You are—face it—a bunch of emotions, prejudices, and twitches, and this is all very well as long as you know it. Successful speculators do not necessarily have a complete portrait of themselves, warts and all, in their own minds, but they do have the ability to stop abruptly when their own intuition and what is happening Out There are suddenly out of kilter.” ~ Adam Smith, “The Money Game”

In this week’s Dirty Dozen [CHART PACK] we walk through the broader bull case for precious metals. We cover why they’re likely headed lower over the very short term. How this selloff is setting the stage for the next major leg higher. Long with the macro fundamentals that will support the next bull trend, plus more…

- Gold is in a 2-year rectangle consolidation within a broader uptrend. Over the last few weeks, we’ve started to become interested in precious metals, for the reasons I’m about to outline. The technicals aren’t there yet. The chart still needs time to develop. But we’re of the belief that PMs are gearing up for their next major leg higher.

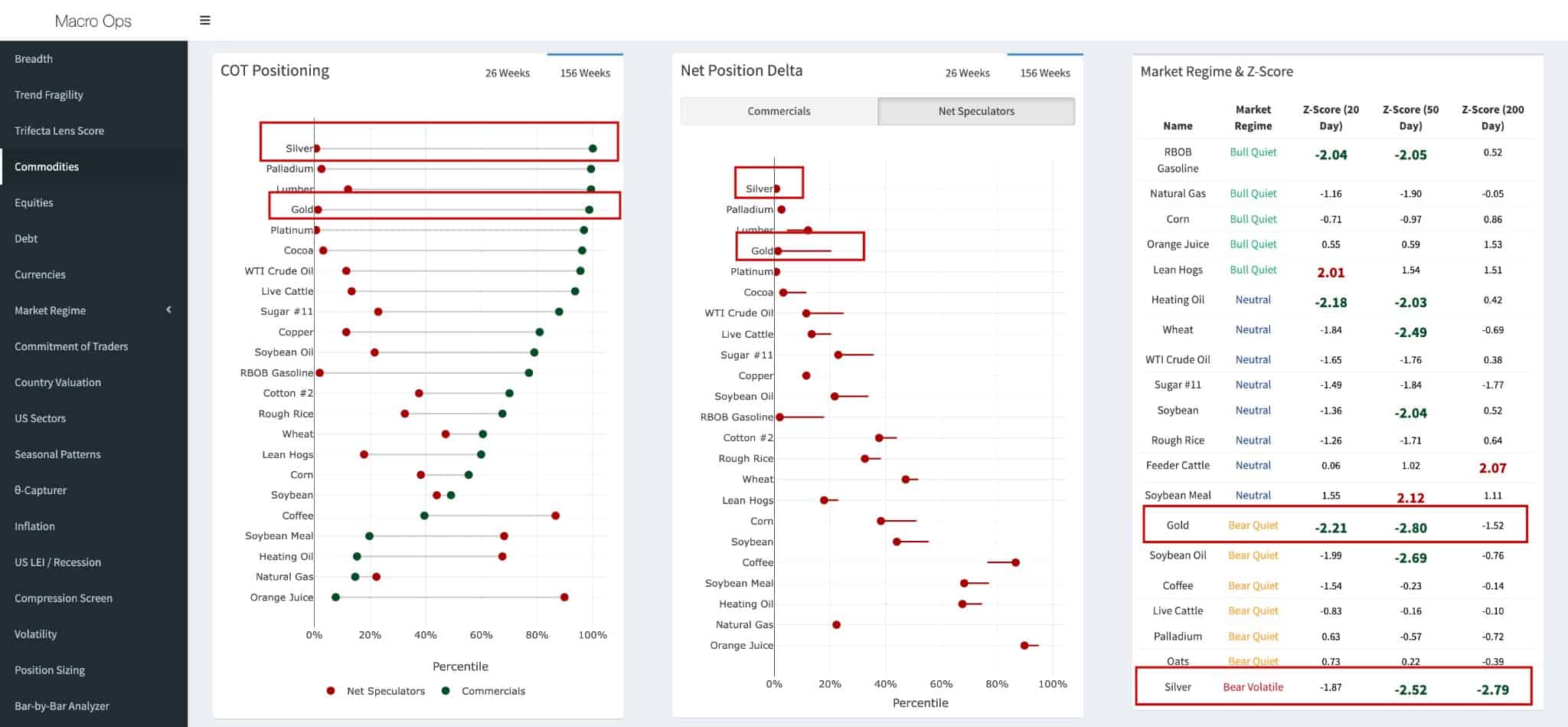

- Our Dashboard (HUD) shows positioning for both gold and silver are in the 1st percentile of their 3-year OI adjusted avg. And both are showing extreme oversold conditions; gold is over 2std below its 20d and 50d moving averages and over 1.5std below its 200dma.

- @htsfkickey shared a short thread over the weekend walking through the follow-on numbers the last time positioning was this bad in the PM space (link here).

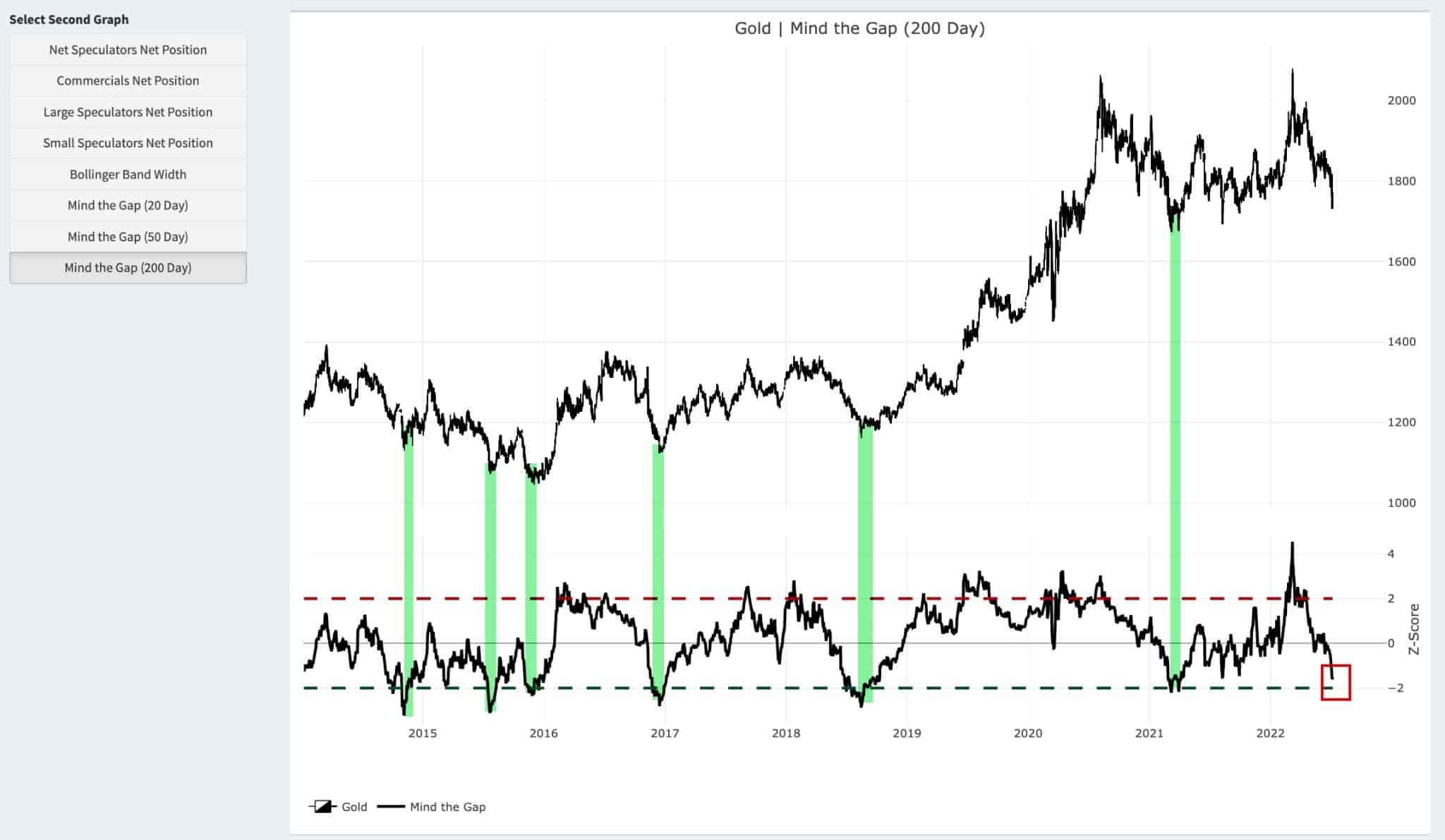

- Three forces are always at work on price (1) Trend (2) Momentum, and (3) Mean reversion. When an asset becomes extended from its moving averages, sellers begin to take profits and buyers turn more hesitant. Combined, these act as a countervailing force working to pull the asset back to its averages (20, 50, and 200dma).

Gold is nearly 2std below its 200-day moving average. A level that has preceded large mean reversion in the past.

- Similarly, fewer than 2% of miners currently trade above their 200-day moving average. Again, these are washed-out breadth levels that typically precede large rallies. Unless precious metals are entering a cyclical bear market. Which, I will show, is unlikely.

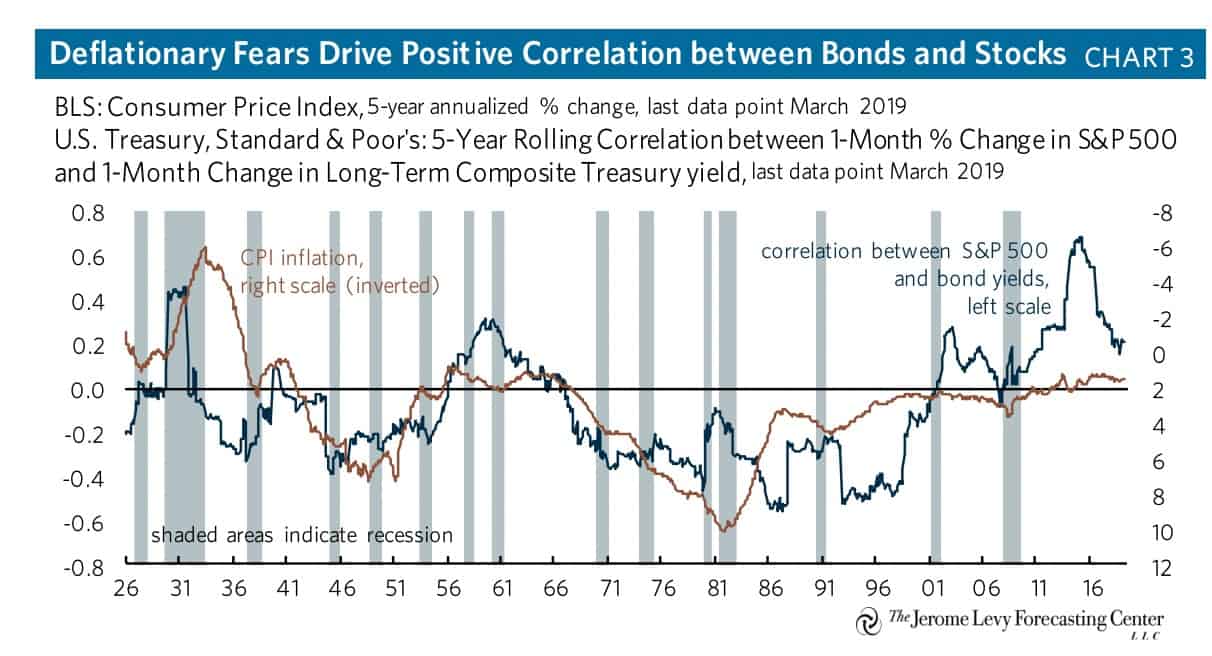

- You can read up on our framework for analyzing precious metals here. The biggest driver of PMs over the long term is the global preference for USD vs rest-of-world (ROW) assets. Subsequently, precious metals have a high inverse relationship to the US dollar (chart below is from the Jerome Levy Forecasting Center).

- The US Dollar has broken out from a 7-year rectangle. This is an obvious short-term headwind to precious metals. But this chart shows the US market cap as a % of Global cap is already at all-time highs, above the last peak in 2000.

So while we’re USD bulls — and thus PM bears — over the very short-term. It seems unlikely to us that this rally will have long legs.

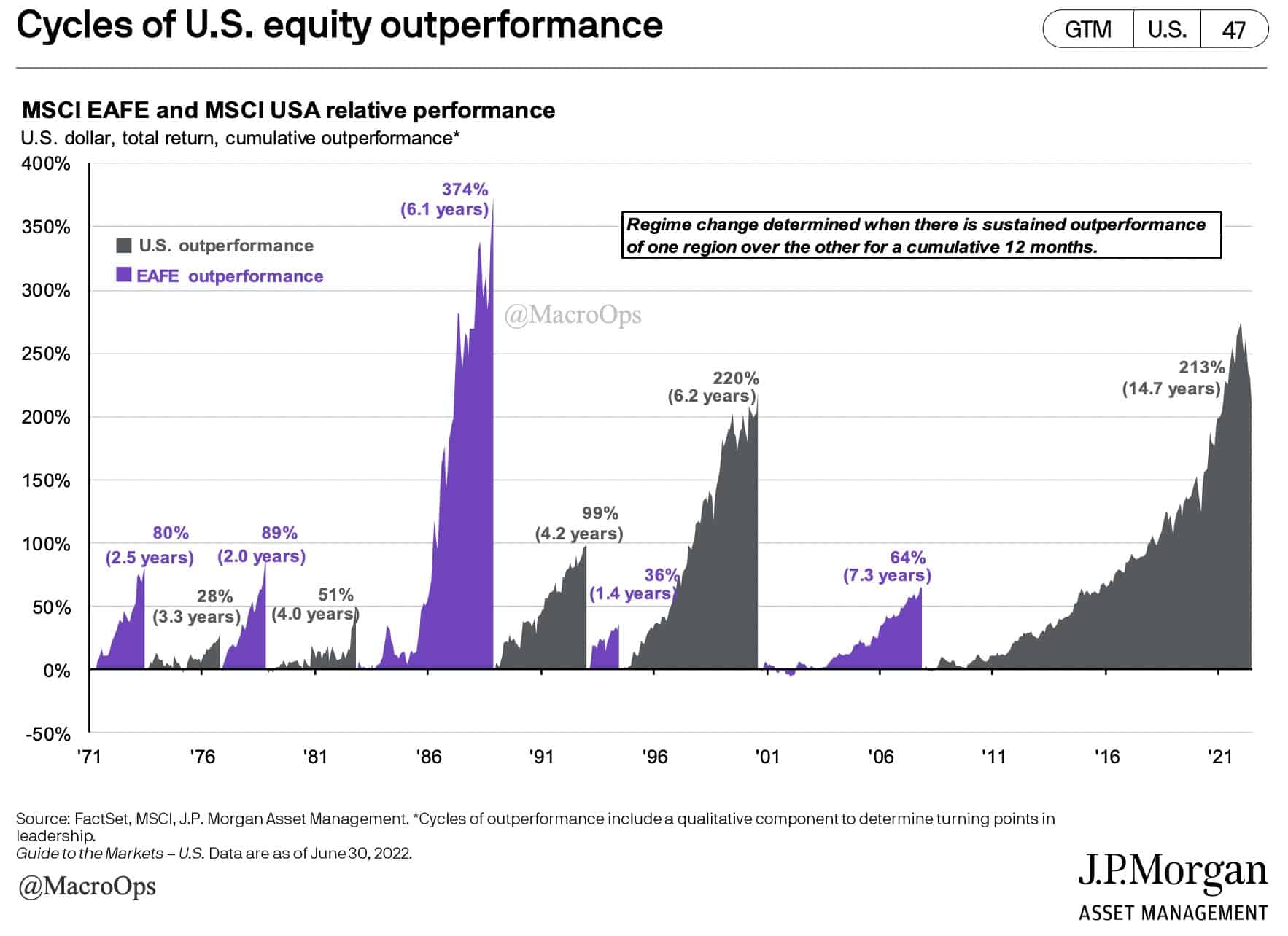

- We’re in the longest cycle of US equity outperformance. Now, this makes sense in a Big Balance Sheet Economics (BBSE) world. The world has large amounts of debt. And most of the Debt is USD based. These high debt levels have kept inflation low, as well as a hard central bank put, to prevent any spiraling financial instability. This has prolonged the trend in US outperformance.

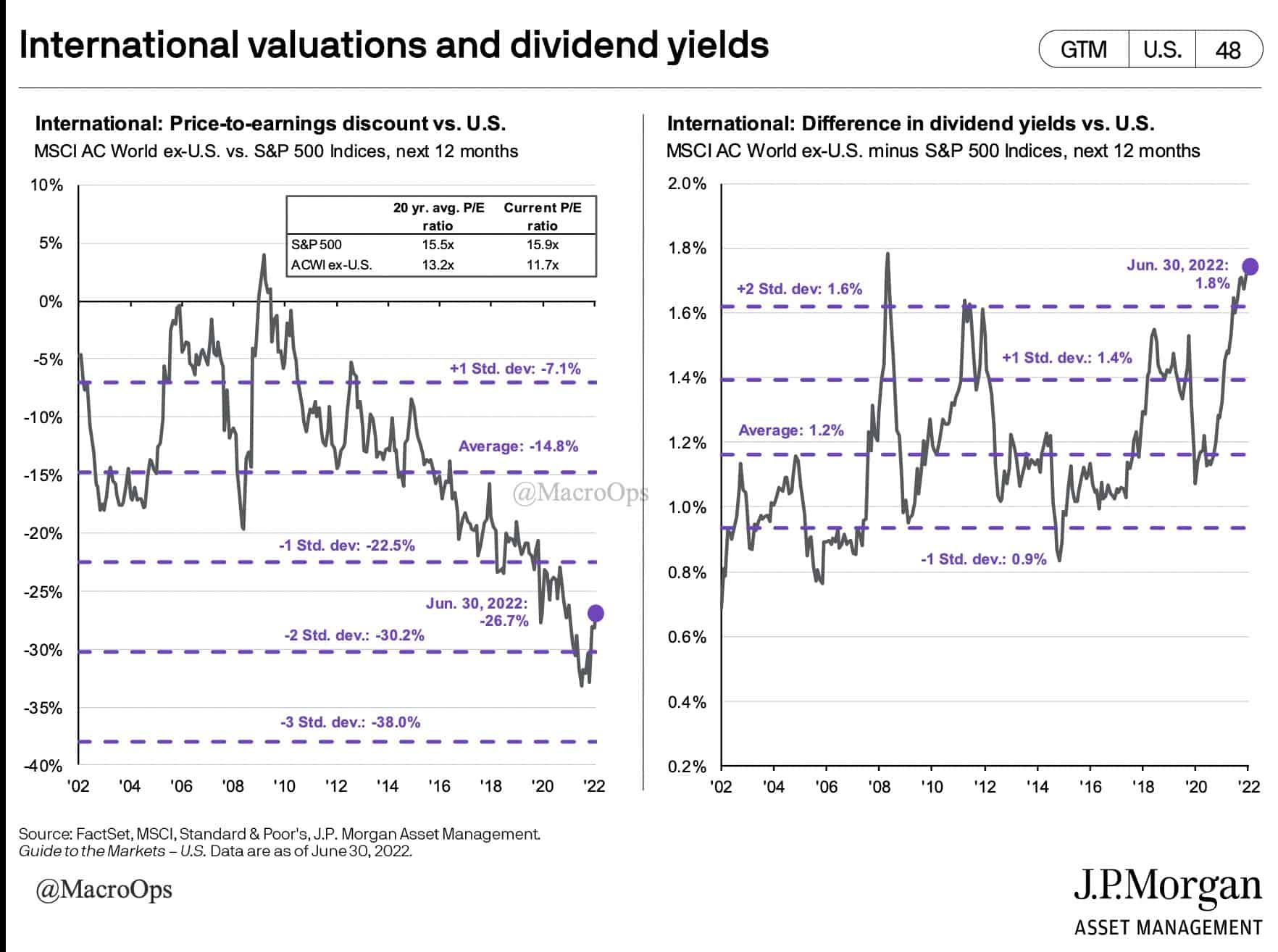

- But the RoW is now trading at a historic discount to US markets.

- The US should always trade at a premium. The USD is the world’s reserve currency. We have the largest and deepest financial markets. The best companies in the world, along with the best corporate governance. But, this premium can become too rich. At which point, capital flows reverse and find shelter elsewhere.

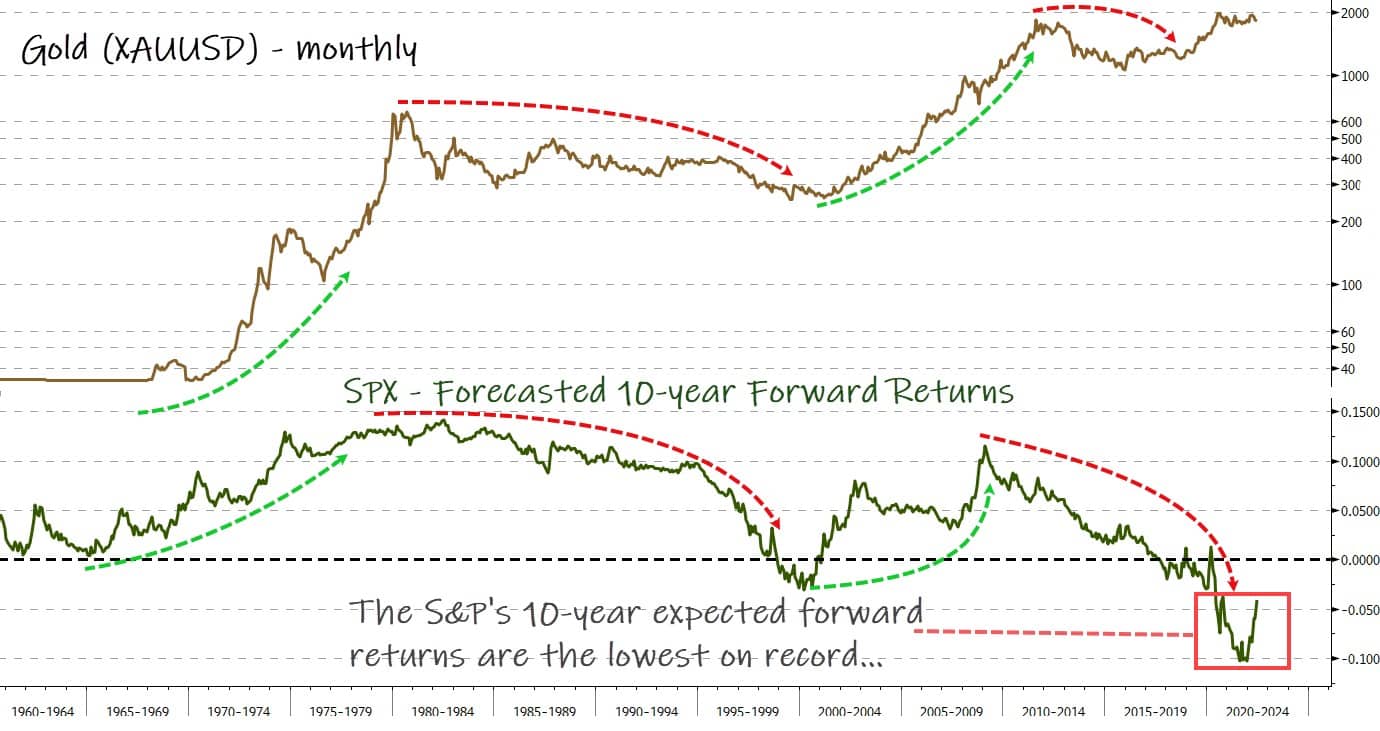

This too-rich moment tends to coincide with poor expected forward relative returns for US assets. And US markets are coming off their worst projected 10-year returns on record.

- Gold tends to do well in recessionary bear markets. Bloomberg notes that “Gold beat the S&P 500 in five of the last seven recessions over the past five decades, with an average gain of 79% in two years…

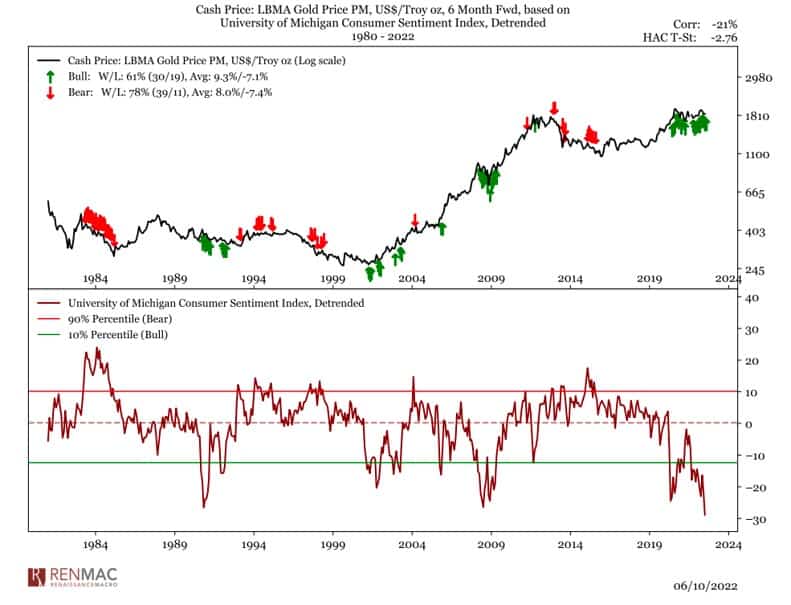

@RenMacLLC shared this great chart showing the correlation between low consumer sentiment and forward gold returns. They wrote “Consumer sentiment doesn’t work well as a macro-factor for forward $SPX returns, but it is one of the better factors for gold $GLD forward returns. Low confidence is historically associated with higher gold prices.”

- This chart from SentimenTrader shows Gold is entering its strongest 3 months of seasonality. So it has that going for it. Again, the short-term tape for PMs is not constructive. But the Trifecta (macro/fundies, sentiment/positioning, technicals) are aligning for the next major bull leg. So it behooves us to be on watch and waiting for the chart to give us entries.

**Note: Enrollment into our Collective kicks off today and will be running into the end of the week. The Collective is our full-kit soup-to-nuts service that provides research, theory, and a killer community that consists of dedicated traders, investors, and fund managers from around the world. We’ve been told that there’s nothing else like it on the web. If you’d like to tackle markets with our group (whom, I should note, has been having a great year in markets), then just click the button below and sign up. And, as always, don’t hesitate to shoot me any Qs!***

![]()

Thanks for reading.

Stay frosty and keep your head on a swivel.