The Solar Thematic reminds me of Rare Earths circa 2024. Back then, investors understood China’s stranglehold on Rare Earths but didn’t truly care until China imposed export bans in late 2024/early 2025.

Here’s what most investors miss about Solar: China has an even greater grip on the solar value chain than Rare Earths. Pair that with an Energy Security At All Costs macro environment, and you have another potential Chinese supply chain squeeze.

Solar is quietly becoming a Trifecta Lens Thematic:

- Fundamentals: Bombed-out manufacturers due to Chinese oversupply and loss-making operations, mixed with cheap hardware and picks-and-shovels plays.

- Technicals: TAN/SPY in the early stages of its bull cycle.

- Sentiment: Value and commodity investors hate solar, and nobody’s talking about it.

The most significant bear argument is that Solar is a terrible industry and business. Why compete with China, which always wins on price? Why bother looking at PV manufacturers after they flooded the market with inventory only to crush margins? Why not just use *insert Trump Voice* “beautiful, clean, coal.”

My bet with solar is that those questions don’t matter because we’re in a different geopolitical and market regime, a new Multi-Polar World.

And there are different rules in this world: It’s not about the lowest-cost solution or widget, but the safest and most domestically dependable one; bifurcated markets are the New Normal; it’s not about the highest EROI, but securing all the energy you can get your hands on.

Solar is bipartisan and helps meet the US’s growing energy demand. It’s also a bifurcated market that’s incentivized to reshore the entire supply chain and remove China from the equation, which is probably a good thing if China moves on Taiwan in the near future.

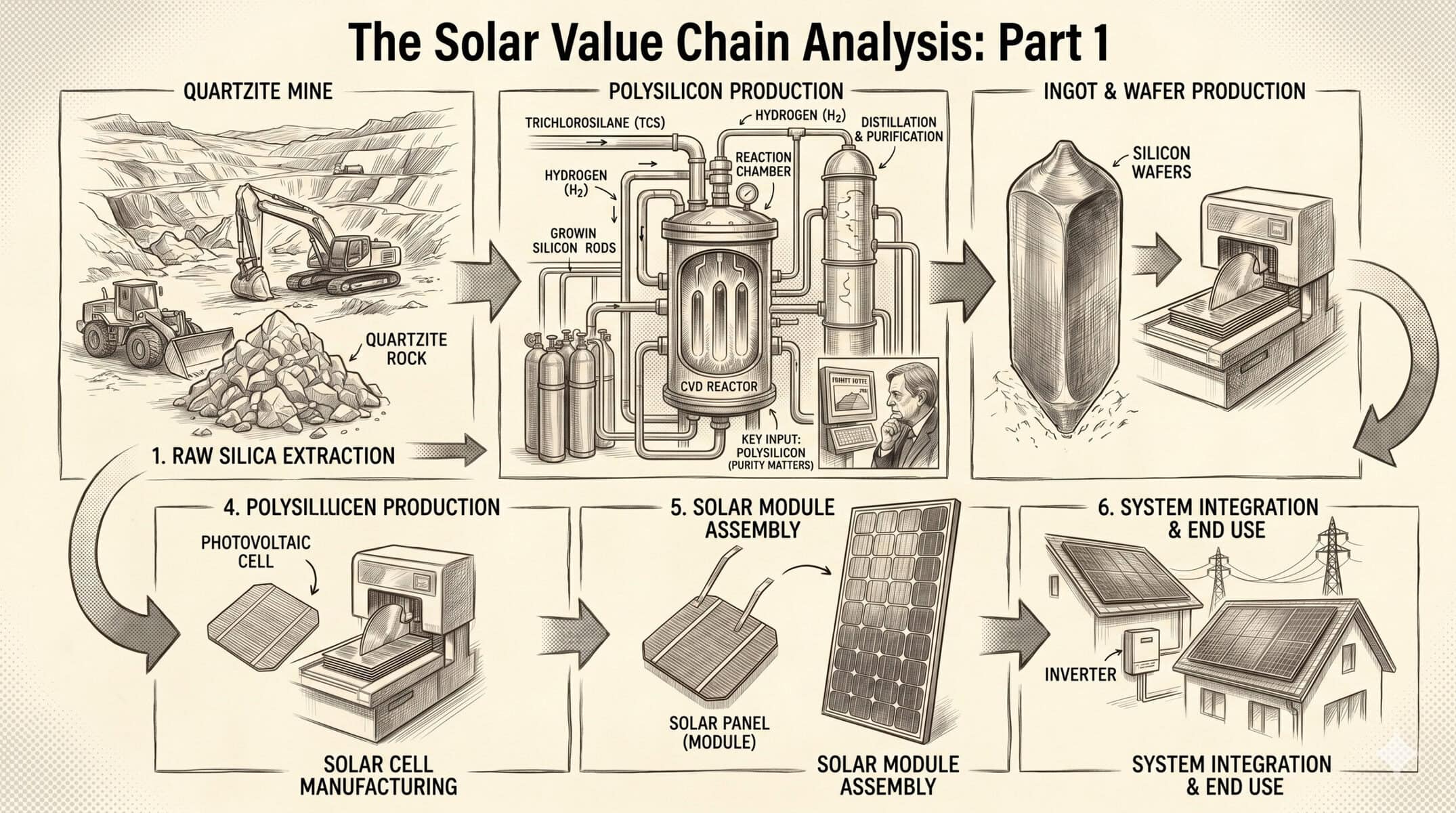

Over the next few weeks, I’ll dive deep into the Solar Value Chain and explain the four main industry systems:

- Upstream: Silver and Polysilicon

- Midstream: Solar PV Manufacturers

- Brains: Power Electronics

- Deployment: Installation and Management

My goal is to provide you with a clear understanding of the entire solar industry, identify market leaders within each system, and offer a basket of potential Solar Thematic bets.

This week, we explore the Polysilicon system. But before we do, I want to mention our new Collective enrollment period.

We’re opening enrollment to the Collective for the rest of the month. The Collective is one of the few places on the internet where serious traders/investors meet, build lasting relationships, share investment ideas, and foster a truly rich life. It’s unlike anything else out there.

The Collective includes all of our research, a full library of reports and videos on theory and strategy, our proprietary market dashboard, plus our internal Slack where the team and I, plus fund managers and die-hards from around the world talk shop, exchange ideas, and shoot the shit. We will be raising our prices by over 25% within the next few months. So if you’ve been on the fence, now’s a good time to jump so you can lock in current pricing.

We’re off to a good start this year (+45% YTD), but we know we can do better.

So if you’re interested in learning more about our Trifecta Lens trading philosophy, our Solar Thematic research (or all our other research), or what it would look like to join our community, click the link below.

I can’t wait to see you in there.

China’s Dominance & FEOC Rules

I’ve written before about how China controls 70% of rare earth mining and 85%+ of the processing, which is a lot. But it’s not as high as China’s control over the solar manufacturing chain:

- Polysilicon production: 93% (second highest: Germany at 4%)

- Wafer manufacturing: 96.6% (second highest: Vietnam at 1.4%)

- Solar cells: 92.3% (second highest: India at 2%)

- PV modules: 86.4% (second highest: Vietnam at 5%)

China is the solar supply chain. This is why investors hate the space. Why compete with the lowest-cost producer that dominates 90%+ of the market?

The IEA even said, “the world will almost completely rely on China for the supply of key building blocks for solar panel production.”

The polysilicon supply chart below is textbook China: oversupply with low-cost material until nobody else can make money. Then, wait for that material to become Nationally Strategic.

It’s like this along every node of the solar value chain.

And remember, in a normal environment this data would kill a bull thesis. But we’re in a Multi-Polar Regime, and the right playbook for analyzing solar stocks isn’t traditional micro-economics, but Energy Security and Resource Nationalism.

Enter FEOC Rules.

Congress added the Foreign Entity of Concern (FEOC) Rule to its One Big Beautiful Bill. The rule says that solar projects starting after January 1, 2026, must source at least 40% of materials from non-FEOC countries, with the percentage ramping to 60% by 2030.

Basically, it forces US companies to not buy Chinese products.

There are three ways companies can “fail” this FEOC rule:

- The project owner is a Specified Foreign Entity (buying from Jinko Solar).

- The owner is a Foreign-Influenced Entity.

- The project receives material assistance from a prohibited foreign entity that exceeds the specified percentage threshold.

Follow the FEOC rules and you get a host of tax credits and other government goodies. Don’t follow them and … well of course you wouldn’t not follow them. You’re an American company and love America, right?

There is a National Security angle to this FEOC bifurcation. Remember the Huawei 5G ban in 2019? Turns out the Chinese also planted funny stuff inside solar cells.

For instance, in May 2025, U.S. experts disassembling Chinese-manufactured solar inverters found undocumented communication devices: cellular radios not listed in product documentation that create hidden backdoors capable of bypassing utility firewalls.

Lithuania banned Chinese inverters by preventing remote Chinese access to solar, wind, and battery installations exceeding 100 kilowatts.

The UK’s ex-chief executive of the National Cyber Security Centre has gone so far as to say, “China was actively inserting itself into critical civilian infrastructure to ‘physically wreak havoc on our critical infrastructure at a time of its choosing.”

These ex-Chinese measures make sense in a Multi-Polar Regime, and are the crux of our bullish Solar Thematic.

Historically, it paid to buy whatever commodity China was buying. Today, it pays to buy whatever part of the value chain the world wants to take from China.

Two weeks ago, I wrote about the solar demand story and why it will be a vital cog in the Energy Security solution.

We’re at an interesting point where demand could inflect just as supply bifurcates, creating massive demand for left-for-dead US/US-allied solar companies.

Let’s dive into the value chain!

Upstream: Polysilicon & FEOC

There are many materials that go into PV solar modules (see above).

Honestly, I’m bullish all of those materials, especially copper, antimony, silver, and tin.

I want to focus on polysilicon because it provides the best framework for understanding the impact of the FEOC rules.

Polysilicon accounts for ~10% of a module’s total cost with no practical substitute in crystalline silicon modules.

China has 93% market share in polysilicon production. But that doesn’t mean anything if US companies want to remain FEOC-compliant.

Toyo, for example, signed a one-year deal in January for US-based polysilicon.

The small problem is that there are/were only really three US/FEOC-compliant polysilicon producers left:

- Hemlock Semiconductor (a division of Corning (GLW)

- Wacker Chemie (WCH.XTE)

- REC Silicon (stopped production in 2025)

Funny enough, the best way to play it is via Wacker Chemie (WCH), a European chemicals company whose polysilicon business hangs in the balance, awaiting its Section 232 ruling.

On the surface, it’s everything you hate about an idea: European, cyclical, currently loss-making, binary event outcome, margins slashed, and did I mention it’s European?

But the more I dug in, the more I liked. WCH owns US polysilicon assets whose value could be worth 3-4x its current market cap in a Resource Nationalist World trading at cycle lows.

Wacker Chemie (WCH.XTE): Nationally Strategic Asset

WCH is a $5B chemicals company specializing in polysilicon and silicon manufacturing. The company is globally recognized as a leading producer of hyper-pure semiconductor-grade polysilicon, claiming to supply material for one in every two microchips worldwide.

It does this from its Charleston, SC facility, something you wouldn’t assume when finding a German-listed chemicals company.

WCH operates an entire semiconductor business that’s quite profitable and could probably support the stock price on its own. But the Charleston facility is our Golden Goose and inflection driver.

It is the only U.S. site with a fully integrated “closed-loop” system that recycles byproducts into other chemicals, such as pyrogenic silica. It is also the most modern facility in the US (built in 2016).

What Happened: Section 232 Investigation

The U.S. Department of Commerce initiated a Section 232 investigation into the national security impact of polysilicon imports on July 14, 2025. From what I could find, the DOC wanted to see where WCH got its raw materials and if it complied with the Nationally Strategic Supply Chain measures.

Its solar polysilicon business tanked due to the investigation as plant utilization collapsed, margins fell from 20% to 11%, China ramped up overcapacity, and revenue declined to EUR 883M.

The Alternate Reality: China Decoupling Creates a Strategic Asset

Let’s assume China moves on Taiwan in the next 8-12 months. If that happened, it would force US industries to decouple supply chains from China, because by that point, we’d probably be at war with China.

Here’s the interesting part: WCH’s Charleston facility is currently the only major U.S. facility capable of high-volume, hyper-pure electronic-grade polysilicon.

A China decoupling would redirect every supply chain that requires hyper-pure electronic-grade polysilicon to WCH’s doorstep. Again, it’s about finding hidden Nationally Strategic assets that other investors miss.

The Charleston site is one of those assets.

It produces approximately 20,000 metric tons of high-purity polysilicon annually. For comparison, new 2025/2026 international polysilicon plant projects of similar or slightly larger scale (16,000–30,000 MT) have announced initial investment budgets ranging from $800 million to over $1 billion just for basic solar-grade capacity.

Then there’s the construction timeline. It would take a minimum of 5-7 years to build WCH’s current facility from scratch. The US would not have that kind of time in a massive decoupling event … industries wouldn’t survive if they had to wait 5-7 years for a reliable hyper-pure electronic-grade polysilicon provider.

Remember, there are only two main polysilicon providers in the US: Hemlock and WCH, and WCH is the only company that can claim to supply one in every two microchips globally.

There’s an interesting dynamic here that is worth exploring.

On the one hand, you could argue that a decoupling could hurt WCH’s export business to China, which accounted for ~60% of its solar polysilicon sales. On the other hand, a decoupling would force billions of dollars in new demand for WCH’s polysilicon that would otherwise have gone to China. It would also eliminate China’s overcapacity pressures, which drove revenues and margins lower in 2025.

But assume that China takes Taiwan, the US decouples from China, and FEOC rules/Section 232 favor WCH. Here’s what that would look like for WCH’s Charleston asset:

- Wacker would become a geopolitical monopoly provider for the Western alliance.

- With the Chinese supply cut off, Wacker and Hemlock Semiconductor would be the only major producers left standing for the West.

- Wacker could likely charge large premiums over current prices as Western solar manufacturers would have no other choice if they want to maintain production.

Suddenly, the cycle-low European chemicals company becomes a Nationally Strategic Energy Asset play. And wow, does that change the valuation potential.

What’s A Nationally Strategic Polysilicon Asset Worth?

Today, investors view WCH as a European chemicals company trading near its lows for ~51x NTM EBIT.

However, there’s a reality in which WCH becomes a US-based Energy Security company with a Strategic Asset in Charleston, SC, providing the domestic solar industry with high-purity polysilicon … and it’s one of two players in the space that can meet demand.

What’s that worth?

If you ask Gemini, you get anywhere from $5B-$7B just for the Charleston, SC facility. WCH owns other US assets, including:

- Adrian, Michigan: Manufactures silicones.

- Calvert City, Kentucky: Produces polymers and binders.

- Eddyville, Iowa: Focuses on biosolutions, such as cyclodextrins.

- San Diego, California: A biotech manufacturing site for pharmaceutical ingredients.

- North Canton, Ohio & Chino, California: Specialize in silicone mixtures under the SILMIX brand.

- Allentown, Pennsylvania: Produces silicone-coated adhesive products.

It also owns two other facilities in Germany.

Call it $6B replacement cost for Charleston, SC. That’s roughly the company’s current enterprise value. So you’re getting all the other industrial assets for free.

But that $6B price tag assumes a normal geopolitical environment.

What happens to the value in a Decoupling Event? A wartime scarcity premium could send WCH’s polysilicon asset to $12B for two main reasons:

- Replacing this capacity takes 5 to 7 years. During a conflict, the U.S. government cannot wait that long, making existing operational capacity “priceless”.

- As China compromises Taiwan’s “silicon shield,” the U.S. could treat the Charleston site as a “defense-rated” facility under the Defense Production Act (DPA).

That’s how WCH goes from being valued as a cyclical chemicals company to a US Defense Strategic Asset.

The Tape: Bouncing off Cycle Lows

WCH looks like most cyclical stocks with oddly predictable trading ranges. My Neanderthal brain is telling me just to buy this chart because “it usually goes up after it has come down to this level.”

Maybe it’s that simple … buy the market and put a stop below this pivot low around EUR 60/share.

There are a lot of risks with this thesis. They could fail the Section 232 investigation and shut down the solar polysilicon business. The US/Europe could pivot away from investing in solar energy. Or the US and China could become friendly trading partners again.

Who knows (especially in this environment).

All I know is you have the ingredients for an asymmetric risk/reward opportunity: misunderstood company, cycle lows, beaten-down industry sentiment, long-term secular demand tailwinds, and a Nationally Strategic Kicker to boot.