Do you know what time it is? It’s Q1 Investor Letter time! That’s right. My four favorite market times of the year. The time where I read letters from investors much smarter than myself. Each time I come away with new ideas, new models of thought and insight into a different part of the market.

Before we get to the letters, check out our latest podcast episodes. I want to give a big shout out to all those that listen. We’re setting new weekly and average listener records each week. And we CANNOT do that without you!

If you want to help us out even more, consider leaving a review and rating on Apple Podcasts. We’re trying to hack their algo and get our name higher in the Investing category.

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- O’Shaughnessy Management Q1 Letter

- Bluehawk Investors Q1 Letter

- Vlata Fund Q1 Letter

Get out your watchlists — it’s time to add some ideas!

—

April 15, 2020

Looking For Ideas? Check Here: You’re stuck at home, quarantined, and just finished Tiger King. What should you do with your new-found free time? Watch micro-cap investor presentations.

I’ve found LDMicro’s 2020 Virtual Event a treasure trove of new ideas. The event features dozens of companies pitching their thesis. If you’re interested, check out the link here.

__________________________________________________________________________

Investor Spotlight: Q1 Letters Round One

GIFs by tenor

GIFs by tenor

We’re off to the races in our Q1 Investor Letter series. We’re starting with O’Shaughnessy Asset Management. The letter dives into Blizzards, Winters and Ice Ages. Each environment has its own characteristics, opportunities and challenges.

Let’s break ‘em down.

Blizzards, Winters and Ice Ages

-

- Blizzard: Defined by extreme volatility and uncertainty—and we’ve had historic amounts of both since February 20th. To survive a blizzard you must focus on placing each foot in front of the other.

Step-by-Step Navigation of Blizzards (according to OSAM):

-

- Executing your plan and/or process

- Reigning in leverage (if applicable)

- Avoiding blunders in confusion

-

- Winter: Sustained period of equity market drawdown and negative economic growth and rising unemployment—an economic recession.

What Happens During Winter: Cost structures change and weak hands (even considering bailouts or loans) fold.

But according to OSAM, winters are the best times to invest in equities.

The Idea of Integrated Equity Valuation

Patrick notes that traditional methods of valuing stocks might not work in the post-COVID world. Why? Company fundamentals could be that bad. His solution? Integrated Equity Valuation.

Here’s OSAM’s definition of Integrated Equity: all capital retained and reinvested by companies, properly adjusted for inflation.

Obviously, the cheaper stocks are to their integrated equity valuation the better. But here’s the crazy part — OSAM hasn’t seen a divergence between price and integrated equity value this large ever. Here’s their take (emphasis mine):

“This is the highest prediction we’ve seen for value since the highest ever in March of 2009 (a prediction which proved close to accurate), when the model predicted a return of nearly 17%/year.”

This is what they’re talking about:

Ice Age Hedges

Patrick ends the letter discussing “ice age hedges”. A sobering concept, but relevant given the circumstances. Patrick notes a few hedges for a potential ice age:

- Cash

- Productive hard assets

- Gold

- Bitcoin

_________________

Bluehawk Investors: -10.01% in Q1

Jake DuBois’ fund returned -10% in Q1. Jake dives into some new ideas and how to think about companies during times of economic stress.

Jake starts the letter discussing four reasons he’s optimistic about the future of business and companies (from the letter):

-

- Extended periods of work from home and social distancing will create some lasting change in behavior. This will accelerate trends like online dating, digital gaming ecommerce, etc

- Quality & strong balance sheet bias creates opportunities to be liquidity providers in dislocated markets

- Finding wonderful bargains in new (and current) holdings

- Larger pool of short selling opportunities

New Portfolio Additions

Jake added four new companies to his portfolio in Q1:

-

- Lululemon (LULU)

- ServiceNow (NOW)

- New York Times (NYT)

- Splunk (SPLK)

He outlines his thesis on three: LULU, NYT and SPLK. Let’s dive in.

Lululemon (LULU)

Jake’s Take: “Lululemon has cracked the code, with a hyper-loyal following, a strong DTC offering, and a strategic physical presence. Their DTC business is why we own the stock, with operating margins above 40& and growing revenue over 25% annually.”

I love LULU as a company. In fact, back in the old days, I used to work for them as a sales associate! It was the only way I could afford their clothing (sad, but true). The culture at LULU is incredible and the brand power amongst its consumers is palpable.

That being said, it doesn’t scream bargain to me. There’s also a few lofty assumptions to get to $1.5B in operating income by 2023. For example, at current EBIT margins, LULU would need over 50% revenue growth in the next three years to get to $1.5B by 2023.

Even if they get there, the current price doesn’t offer much of a discount. Slap a 16x multiple on 2023 operating income and you get $24B in equity value. That’s nearly $1B less than the current market cap.

Here’s the chart …

New York Times Company (NYT)

Jake’s Take: “With the deepest pockets (and a great reputation) come great journalists and editors, who create great content, which drives virality of stories and subscriber growth in general, which garners NYT more money and a better reputation. While this flywheel is moving, it creates adjacent opportunities too, and NYT is in the early stages of building its media portfolio to further acquire customers.”

NYT is a high-margin business with a brand-name competitive advantage. If they execute the transition to a digital-first, subscription-based model, we should see margins (and earnings) expand further. The company also sports a strong balance sheet with over $360M in net cash.

You can buy NYT for 23x current EBITDA, or 3x sales.

Here’s the chart …

That’s some beautiful consolidation right there. Might appear on my breakout alerts weekly report this week.

Splunk (SPLK)

Jake’s Take: “Splunk’s software is used for monitoring, searching, analyzing, and visualizing unstructured machine data in real time and at massive scale. The company has generated impressive growth over many years and has built up deep relationships with a largely enterprise customer base. While making tangential acquisitions that enhance its offering.”

Bluehawk started buying in mid-March — which happened to be almost the exact bottom (in short-term).

The company’s grown revenues 30%+ annually since 2016 as they pull closer towards net profit. Gross margins are an insane 80%. And they have $1B in net cash on the balance sheet. All said, quite the attractive business. But what’s the price?

Right now you can buy SPLK for 8x sales. That sounds expensive. But if the company maintains its 30% per-year growth over the next five, a 6x sales multiple on 2025 revenue would give us $38B in equity value.

Here’s the chart …

Investing in Quality Growth Stocks

Bluehawk thinks now is the time to invest in “quality growth stocks”. They say this in contrast to traditional “value-based” sectors: financials, cyclicals, energy and materials.

Jake believes Quality Growth stocks offer the best risk/reward in the market. In his words, Quality Growth stocks, “have the cleanest balance sheets, fewest demand questions, and attractive risk/reward propositions at current valuations.”

_________________

Vlata Fund: Performance Not Disclosed

Daniel Gladis, manager of Vlata Fund, split his letter between broad macroeconomic situations and microeconomic (portfolio) thoughts and ideas. I won’t spend time on the macroeconomic stuff — that’s more up Alex’s alley.

The Shopping Mall Analogy

I loved Daniel’s shopping mall metaphor for the current market environment. It goes like this (emphasis mine):

“If I were to visit the Olympia shopping centre here in Brno, I probably would find all the shops closed. Were I to bet which ones will do best in future, I would not be concerned with range of products, service level or prices. In the first place, I would be interested which of these shops will open again after this crisis.”

That’s exactly the way to think about companies during COVID-19. You’re focused on which companies will survive — not thrive. But looking further, we want to invest in companies that can thrive post COVID-19. Daniel emphasizes this, saying, “We are interested in those which not only will survive and will not be crippled in the long term but which may even emerge from the crisis stronger due to the fact that some of their competitors will fall away in the meantime.”

Vlata segregates their portfolio into four silos:

-

- Large sums of net cash

- Financial Companies

- Low Debt

- Manageable Debt Burdens

Let’s take a look at the companies within each silo.

Large Sums of Net Cash

-

- Berkshire Hathaway (BRK.B): $125B net cash

- Samsung (005930): $70B net cash

- BMW (BMW): 17B euros net cash

These companies make up 31% of Vlata Fund’s portfolio.

Financial Companies

-

- Sberbank (SBER)

Daniel’s Take: “Sberbank has owners’ equity of USD 70 billion, and last year’s net earnings were USD 14 billion. Its Tier 1 capital ratio is on the level of the best American banks JP Morgan and Bank of America even as its leverage of 6.6 is far lower.”

-

- Markel (MKL)

Daniel’s Take: “Specifically, Markel has debt of USD 3.9 billion with maturity as long as 30 years and liquid assets of USD 22 billion.”

-

- Credit Acceptance Corp (CACC)

Daniel’s Take: “At present, the company has more capital than it is able to use effectively in its business, as evidenced by the fact that in December and February it repaid early bonds that were due in 2021 and 2023.”

Low Debt

-

- Alimentation Couche-Tard (ATD.A): Net Debt/Equity of 1.5x

- Babcock International (BAB): Net Debt/Equity of 1.4x

- Crest Nicholson (CRST): Net Debt/Equity of -0.3x

- Magna International (MGA): Net Debt/Equity of 0.7x

- WH Smith (SMWH): Net Debt/Equity of 0.9x

Larger (But Manageable) Debt Levels

-

- LabCorp (LH): Net Debt/EBITDA of 2.6x

- Teekay LNG Partners: Net Debt/EBITDA of 7.4x

A Great Investment Philosophy

Daniel ended his letter with one of the best descriptions of what types of businesses we should look for during the COVID-19 crisis:

“To sum this all up, the companies we hold are very profitable in the long term, financially strong and self-sufficient. They do not need to rely on the market for external financing, and their businesses are not in those sectors most crippled by the recession and virus.”

__________________________________________________________________________

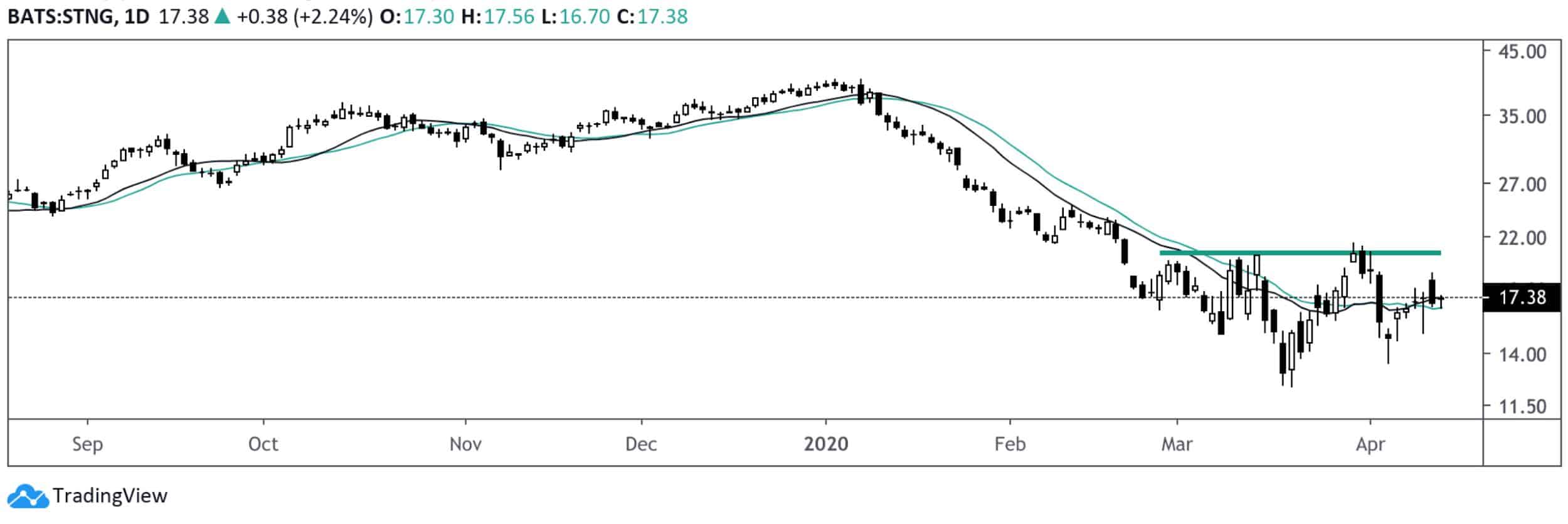

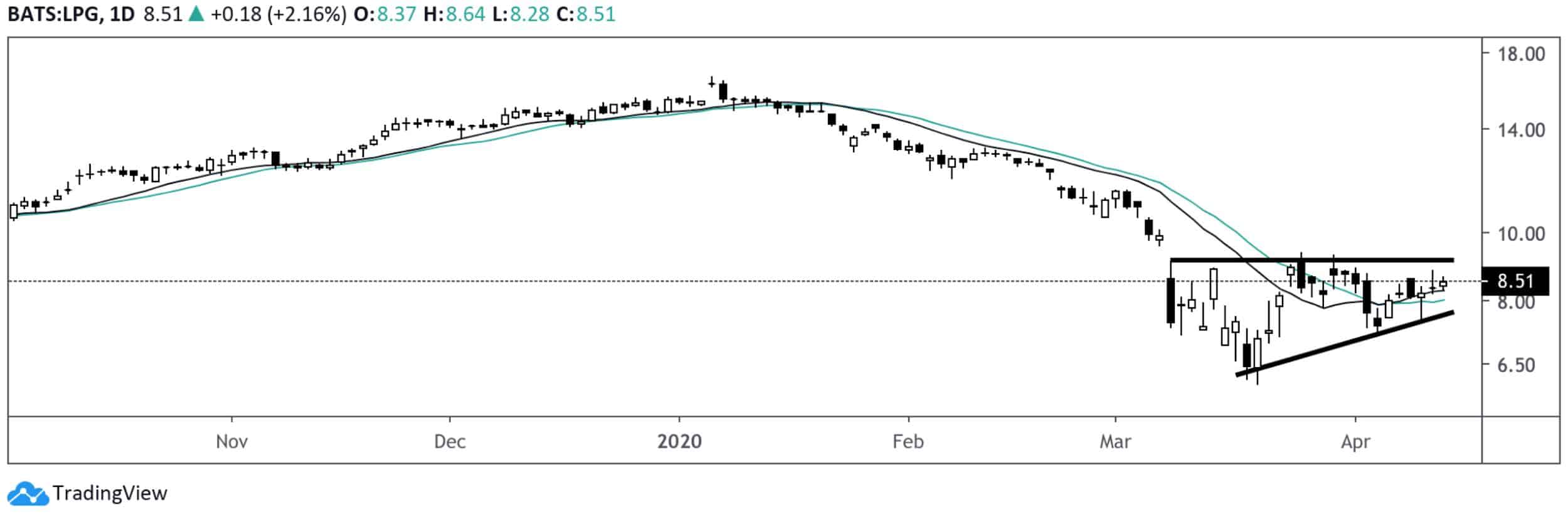

Shipping Chart Update: Base Building Development

GIFs by tenor

GIFs by tenor

In tune with last week, we’ll keep you updated on the shipping thesis playing out. These are updated charts as of Tuesday (April 14th).

-

- Scorpio Tankers (STNG)

-

- Diamond S Shipping (DSSI)

-

- Dorian LPG Limited (LPG)

-

- Teekay Tankers (TNK)

-

- Euronav (EURN)

No chart pattern forming.

-

- Overseas Shipholding Group (OSG)

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!