Hope you’ve had a great week. We’ve seen the first few cases of COVID-19 in the US. Batten down the hatches and put on your masks. Things could get ugly. While you’re bunkered in your home, check out our latest podcast episodes:

Also, if you have the time, please subscribe and leave a rating/review of the podcast on Apple Podcasts. It goes a long way in spreading the word about the show.

Here’s what we cover this week:

-

- Tao Value Q4 Letter

- Bain Capital Private Equity Report

- Buffett’s Interview with CNBC

Let’s get it!

—

March 04, 2020

We Have A Winner: Reader Javier emailed the correct answer to the President’s Day trivia question. Instead of sending Javier $5, he asked me to critique a valuation and write-up he’s doing on a potential investment.

I love the idea. If anyone’s looking for a set of eyes on their investment pitches/theses/write-ups, I would be happy to take a look.

Great idea, Javier! And thanks for reading!

__________________________________________________________________________

Investor Spotlight: Tao Value’s Q4 Letter

We’ve come to the last letter in our Q4 Investor Letter series: Tao Value. Only a few months before we do it all over again. If you’re like me, you can’t wait! Let’s break down this week’s letter.

Tao Value: +17.88% in 2019

Tao returned 4.25% in Q4 and 17.88% in 2019. His letter covers a lot of stocks. For our purposes we’ll cover:

-

- China Meidong Auto (1268.HK)

- Sea Ltd. (SE)

- Alphabet (GOOG)

- ALliance Data Systems (ADS)

- Huya (HUYA)

- Pinduoduo (PDD)

At the end of the year, Tao’s three largest positions were cash, CACC and GOOG. They represented 35% of the portfolio.

China Meidong Auto (1268.HK)

One of the reasons I follow Tao Value is because I’m always finding new ideas. Tao dives into markets I don’t, and uncovers stocks I wouldn’t otherwise find. China Meidong is a perfect example. Here’s Tao’s take (emphasis mine):

“The luxury car segment remains the only bright spot of overall China auto market, still growing at 8%. We also saw Meidong executed well for the first half year, racking up 32% increase in number of stores, 57% increase of revenue & 50% increase of profit year over year. The management also indicated its future plan for growth mainly through acquisitions, for which we will keep and close eye on.”

Let’s take a look at their financials:

-

- 37% 5YR Revenue CAGR

- 10% Gross Margins

- 27% 5YR Operating Income CAGR

- Profitable for the last nine years

- 29% ROE

- EBIT/Interest: 7.8x

The company’s not exactly cheap at this point. You can buy it for 13x EBITDA. Yet a year ago you could’ve bought for <6x EBIT. Nice job, Tao!

Here’s the long-term chart …

December 2018 price to revenues? 0.30x.

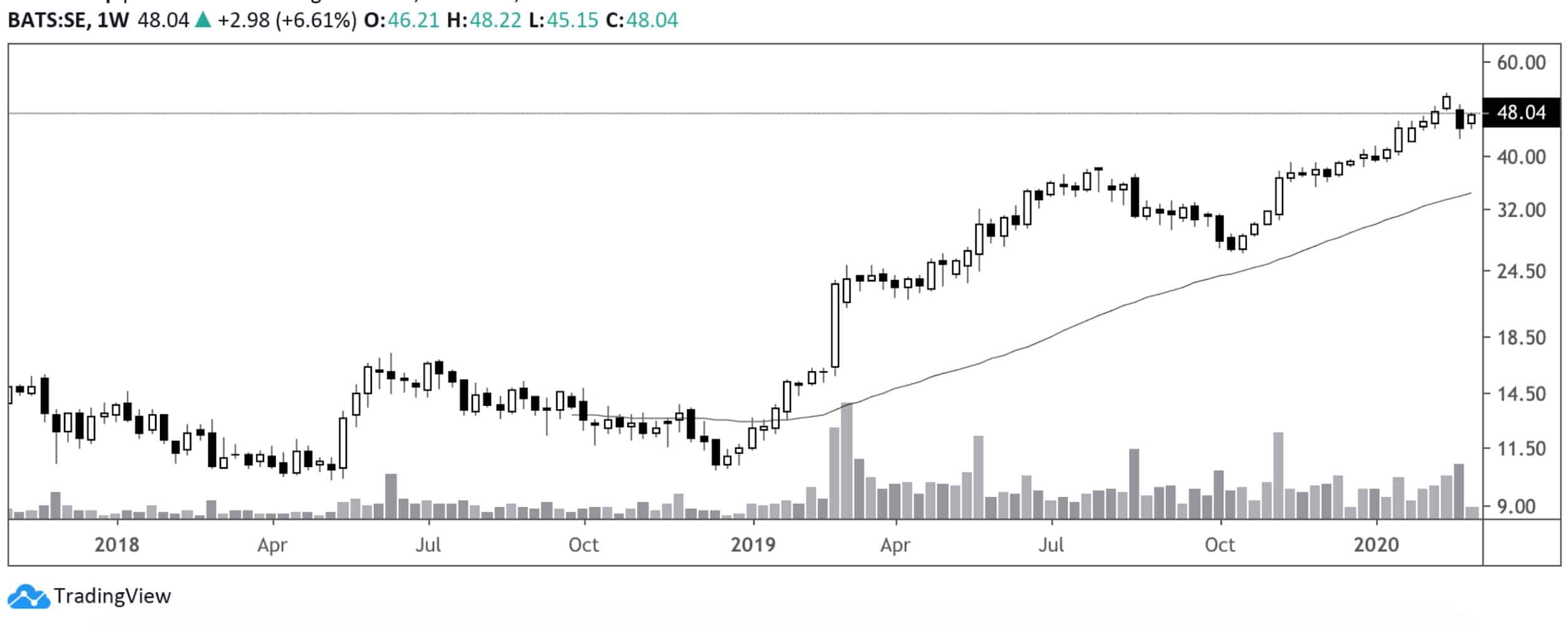

Sea Ltd. (SE)

Okay I’ll say it. SE’s becoming a hedge fund hotel. While comforting, we all know the detriment such actions can have on a company’s share price (I’m looking at you, Valeant).

Regardless, here’s what Tao has to say (emphasis mine):

“[Sea’s] continued a strong momentum in its gaming business, raising its guidance again in its Q3 earning release. For e-commerce business, it started to ramp up the monetization by scaling back on certain shipping & handling subsidization. While it helps reduce the loss, it will be important to track the growth trajectory after such incentives change. Sea is also showing up in many fund managers’ recent quarter 13F filings, indicating strong demand from US institutional managers.”

Has this opportunity left the train station? Let’s take a look at their financials:

-

- 86% 5YR Revenue CAGR

- Losing close to $1B/year in net income

- Trades at 5x Revenues

You can find SE write-ups all over Seeking Alpha and SumZero. In fact, one of our fund managers we cover (Fred Liu) is long SE.

Here’s the chart …

The company’s been a cool 3-bagger since the December 2018 lows.

Alphabet (GOOG)

GOOG’s another stock I’m seeing pop-up on many value investors’ Twitter accounts. Check out this tweet from Yaron Naymark of 1 Main Capital:

Name a stock where you think baby has been thrown out w the bathwater – earnings not significantly impacted by virus and valuation starting to get silly.

I flag $GOOG – off 14% in the last week, now 18x fwd earnings (16x ex cash) where you get Waymo and GCP for free.

— 1 Main Capital (@1MainCapital) February 28, 2020

Here’s Tao’s take (emphasis mine):

“During its most recent Q4 earning announcement, Alphabet, for the first time, disclosed separate numbers for Youtube, which has an annual run rate of $15 billion, growing 36% year-o-year. The $15 billion may appear a huge number, however it only translates into less than $8 for each of its 2 billion users. As a user, I believe the $8/year is way under value for Youtube’s services that I use, thus Youtube still has multi-folds growth path ahead of it.”

I agree with Tao. I use way more than $8/year in utility from YouTube.

Let’s look at the charts …

You can buy GOOG for 12x EBITDA and 17.5x FCF.

Alliance Data Systems (ADS)

Business Description: ADS provides data-driven marketing and loyalty solutions worldwide. It operates through three segments: LoyaltyOne, Epsilon, and Card Services. – TIKR.com

Here’s some quick financials:

-

- EV/EBITDA: 16x

- Price/Cash Flow: 3.25x

- 29% ROE

- 20% EBITDA Margin

Tao’s Take: “I believe it is moving toward the right direction of de-risking its retail portfolio, yet maybe in a slower than anticipated pace. One major update however is that ADS announced in November to name a new CEO Ralph Andretta, a long time Citi card business executive, just 5 months after they promoted the last CEO Melissa Miller from its own card business. The management shuffle seems excessive and created some uncertainty to our original thesis.”

Here’s the chart …

ADS hasn’t traded this low since July 2011. Crazy thought: if you bought and held in 2011, you’d be flat on your position while the market’s ripped higher.

Huya (HUYA)

Business Description: HUYA operates game live streaming platforms in the People’s Republic of China. Its platforms enable broadcasters and viewers to interact during live streaming. Its live streaming content covers a library of games, including mobile, PC, and console games; and other entertainment genres, such as talent shows, anime, and outdoor activities. – TIKR.com

Tao’s Take (emphasis mine): Its core e-sports streaming is facing intensifying competition from a few strong newcomers. For example, Bilibili (ticker: BILI) obtained exclusive broadcasting rights for League of Legend World Championship. Given this observation, I estimate the path to profitability for the e-sports streaming industry would be prolonged, yet Huya is and can remain the industry leader.

HUYA IPO’d in 2018 and offer limited historical operating results. We have 2016 – 2018:

-

- 160% 3YR Revenue CAGR

- $730M Gross Profit (15% Margin)

- $26.6M Operating Income

- P/E (TTM): 76x

- P/E (NTM): 30x

I hadn’t heard of HUYA until reading this letter. The company looks interesting and made a spot on my watchlist for further due diligence.

Here’s the chart …

The logic behind shorter-term share price appreciation is simple. More people staying inside in China leads to more video game consumption. This in turn leads to more streaming / people watching others play video games, etc. A COVID-19 resistant business.

Pinduoduo (PDD)

Business Description: PDD operates an e-commerce platform in the People’s Republic of China. It operates Pinduoduo, a mobile platform that offers a range of products, including apparel, shoes, bags, mother and childcare products, food and beverage, fresh produce, electronic appliances, furniture and household goods, cosmetics and other personal care items, sports and fitness items, and auto accessories. – TIKR.com

Tao’s Take (emphasis mine): We added on our Pinduoduo (PDD) position on its seemingly abysmal earning release day when the price dropped 22%. We believe the misinterpretation by Mr. Market of its branding investing activity as full expense created a great opportunity to add our position. During Q3 19, PDD ramped up aggressively in its marketing expenses, and the management disclosed a very important detail on how they measure their branding investing effectiveness, which is by measuring the behavior change after users use coupons.

Here’s some financials:

-

- 834% 3YR Revenue CAGR

- 78% Gross Margins

- -$10B Operating Loss

- Current Ratio: 1.65x

And here’s the chart …

__________________________________________________________________________

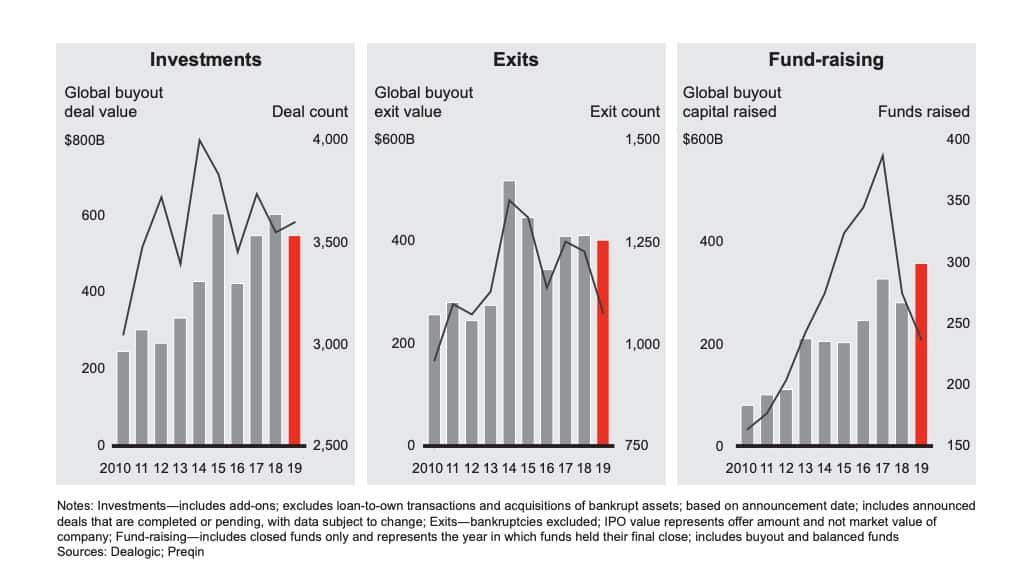

Movers & Shakers: Private Equity Deal-Making Stays Hot

Bain Capital released their 2020 Private Equity report last week. It’s a dense read at 96 pages, but well worth it. I’m covering a sliver of the information in the report here. I encourage you to click the link above and read its entirety.

Let’s dive into my favorite charts from the report …

Buyout Deals Remain Strong

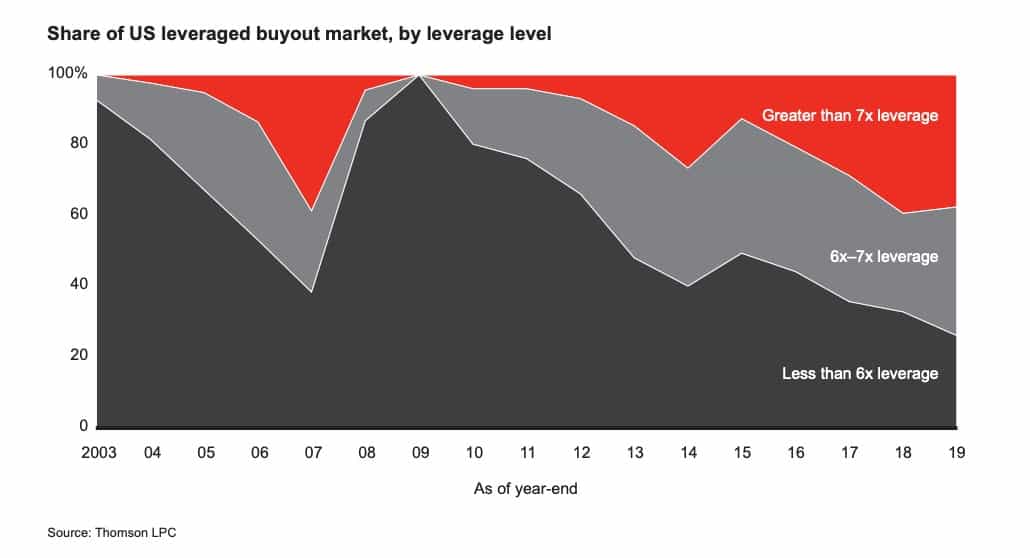

Higher Leverage on Buyout Deals

Here’s a crazy statistic (from the report): “Deals with debt multiples higher than six times earnings before interest, taxes, depreciation and amortization (EBITDA) rose to more than 75% of the total. That comes in stark contrast to the years following the global financial crisis, when their share did not exceed 25% (see Figure 1.5).”

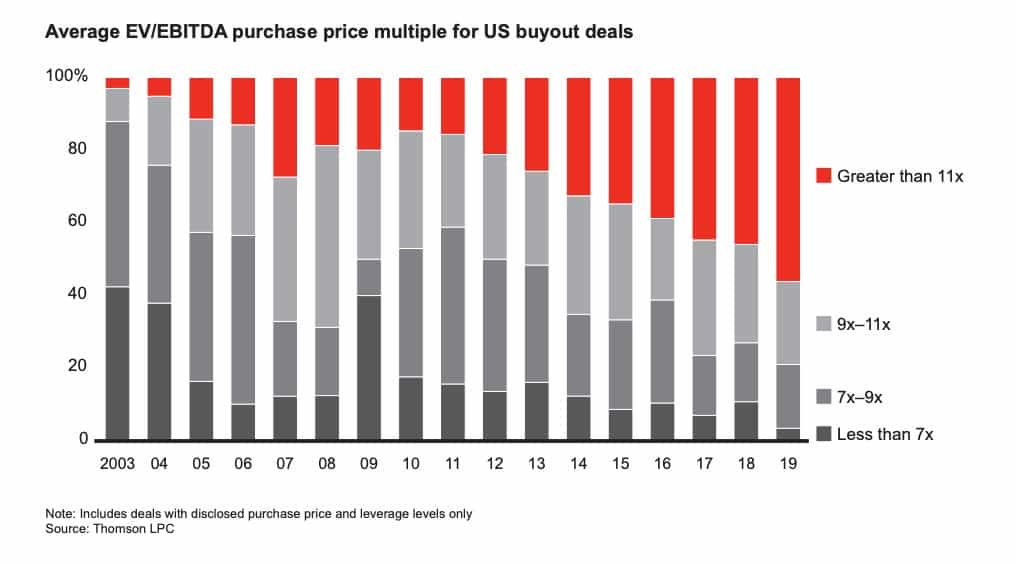

Deals At Record Valuations

Stat: “More than 55% of US buyout deals had a multiple above 11x.” Wow.

Capital on Sidelines Ready To Deploy

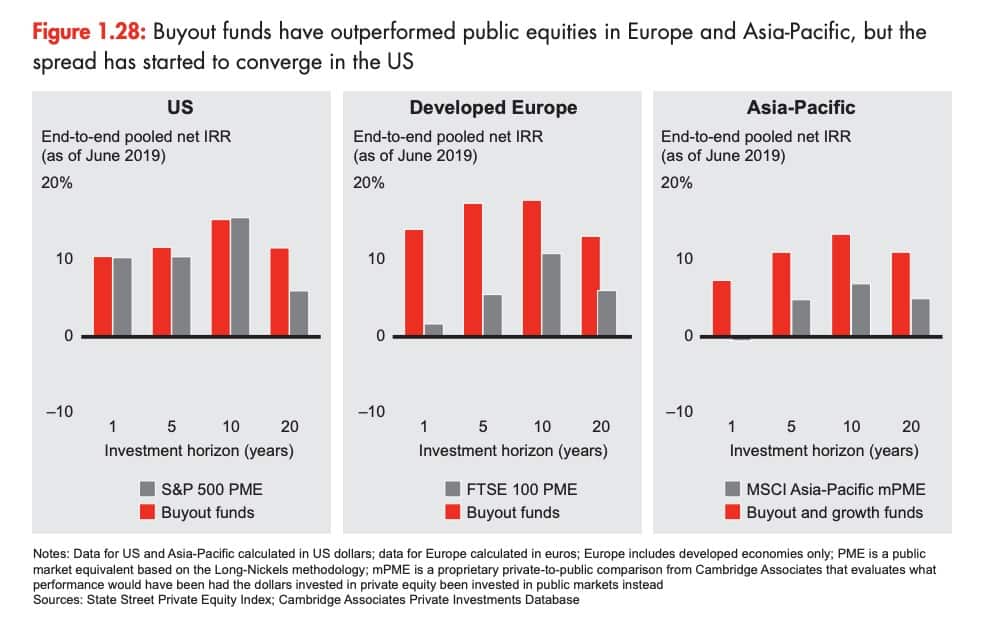

Buyout Fund Excess Returns Narrow

PE outperformance remains high in developed Europe and Asia-Pacific. But in the US those spreads have converged along shorter time horizons.

Another fun fact: margin improvement almost never works. Check out this statistic:

“For the deals where margin improvement was a critical factor in the value-creation plan, more than three-quarters did not meet the margin target.”

The rest of the report covers finer details of private equity such as:

-

- ESG Investing

- Spreads between public & private returns

- Where PE funds put their money

Give it a read.

__________________________________________________________________________

Resource of The Week: Buffett’s Chat With CNBC

Warren Buffett joined CNBC for a well-timed interview on long-term investing. Specifically, Buffett warned investors of trading news headlines. Here’s one of my favorite lines from the interview:

“When you buy a stock you shouldn’t say, ‘I bought a stock today’. You should say ‘I bought a company today.’”

Check out the full length interview here. And for those that prefer reading, here’s the transcript.

__________________________________________________________________________

Tweet of The Week: Greenhaven Road Capital 13F

First Greenhaven Road 13F (https://t.co/bZ342IZqtd) pic.twitter.com/DKgjrGHlVj

— Mine Safety (@MineSafety) March 3, 2020

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com. Have a great Christmas holiday.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!