Alex here with your latest Friday Macro Musings…

Latest Articles —

A Monday Dozen [CHART PACK] – I take a look at CROWDED trades, some of the worst earnings guidance in a decade, the US joining in on the manufacturing recession and more…

There Are No Limits — I share a story about Bruce Lee and his belief that a “man must constantly exceed his level”.

John Burbank Explains How to Trade Eurodollars — AK gives a breakdown of the eurodollar and lays out Burbank’s big eurodollar macro bet.

Articles I’m reading —

If you own any of the big tech stocks (AMZN, MSFT, CRM etc…) then give Horizon Kinetic’s latest Investors Letter a read (link here). If you don’t own any of these names, then, well, still give it a read because it’s that good and serves as a healthy counterbalance to what’s being passed around as accepted wisdom in mainstream investing circles today.

The letter starts with a rehash of the nuttiness that was the 90’s TMT bubble and discusses the underlying extrapolations — the collectively accepted lies — we all told ourselves to make the insane valuation cases more stomachable. It then goes into a major extrapolation that’s underpinning nearly all big tech valuations today; the continued strong growth of internet adoption. They write (emphasis by me):

If you recall the earlier table that showed global internet usage in 1999, the figure was 4.1%, up from near zero in 1995. But a critical line was crossed just two years ago. In December 2016, 49.5% of the world’s population used the internet, and sometime in the ensuing months, it exceeded 50%. Well over half the world is now on the internet: as of this March, the figure reached 56.8%.

Can a growth limit be calculated? Yes, quite easily; no Excel spreadsheet necessary. If growth were to continue at a 12% rate for five years, the global internet usage rate would equal 100%. It should be self-evident that it cannot reach 100% within five years. At some point during the next 60 months, investors will realize that growth will cease or at least slow markedly from the historical rate.

This is basic arithmetic with big implications… The letter also covers a number of their portfolio holdings, which is dominated by oil & gas, gold, and shipping stocks (looks like we have a lot in common with them). Check it out.

Tech and Media writer Matthew Ball has been writing a great series on private equity and the scourge it’s wrought on our capitalistic system. The first piece in the series is bluntly titled “Why Private Equity Should Not Exist”. Here’s a clip from the article.

While the movement is couched in the language of business, using terms like strategy, business models returns of equity, innovation, and so forth, and proponents refer to it as an industry, private equity is not business. On a deeper level, private equity is the ultimate example of the collapse of the enlightenment concept of what ownership means. Ownership used to mean dominion over a resource, and responsibility for caretaking that resource. PE is a political movement whose goal is to extend deep managerial controls to a small group of financiers over the producers in the economy. Private equity transforms corporations from institutions that house people and capital for the purpose of production into extractive institutions designed solely to shift cash to owners and leave the rest behind as trash.

That’s actually one of the more subtle paragraphs. He also gives a really good overview of the origins of PE and how it became so powerful and intertwined in our political system. Here’s the link.

And finally, Massif Capital’s latest Investors Letter provides a good working overview of the Capital Cycle along with some of their personal additions to the framework + a great overview of the mining sector. Here’s the link and a clip.

The key question for investors is thus not one of demand (which drives short term price action), but rather of competition and supply (which create structural price floors for commodities). As such, we ask: is capital flowing into the industry and flowing into projects that are going to bring on significant supply, depressing industry returns.5 On a timeline of several weeks to years, this flow of capital is positive for equity investors as it is positive sentiment about the industry made real. Balance sheets expand, and asset values get bid up. In the long run, excess supply creates structural changes within an industry that will drive down the industries base rate of return and results in liquidity flows out of an industry.

Charts I’m looking at—

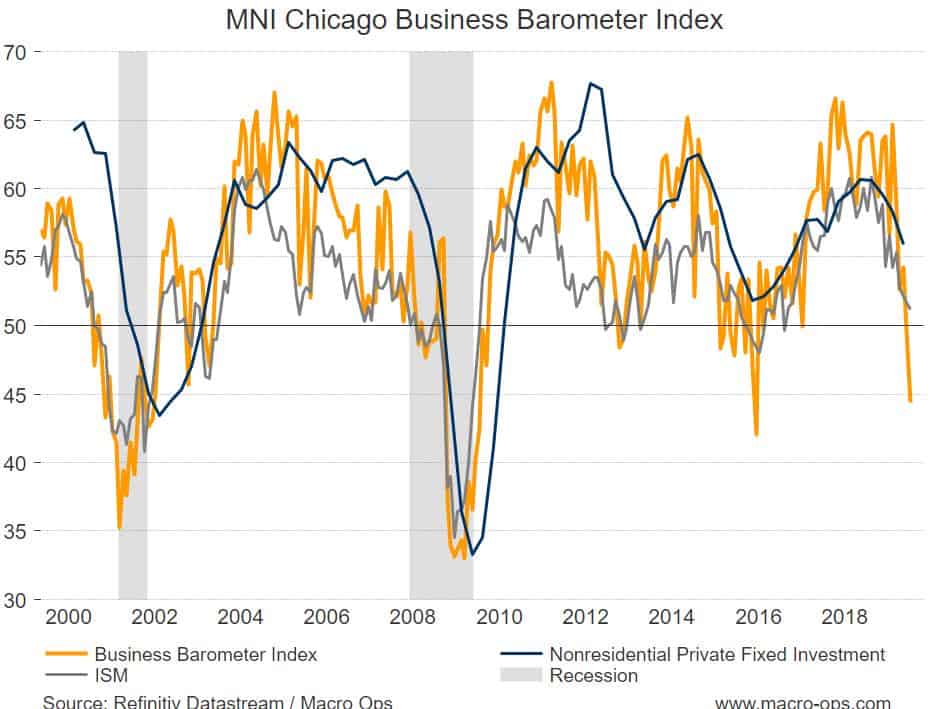

So Trump just jacked up tariffs on China (announced through Twitter, of course) before his negotiators were even done with trying to negotiate, apparently. We have a theory that Trump is escalating the trade war because he wants more rate cuts from the Fed. If he keeps it up, he’ll certainly get those cuts but they’ll come with the cost of recession. The MNI Chicago Business Barometer Index (which leads capex and ISM) is cliff diving. Watch your six out there.

Podcast I’m listening to —

Last week I shared Peter Thiel’s interview on Eric Weinstein’s podcast, The Portal. This week I gave episode 3 a listen, where he interviews filmmaker Werner Herzog (link here).

It’s a super interesting interview and makes me want to go back and watch Werner’s earlier works, like Fitzcarraldo. The dude is a total nut. He’s been shot (with a gun) while filming and refused to go to the hospital because he wanted to finish the scene. He’s trecked through the amazon for months on end, eating worms and navigating dangerous rapids just to make his vision come to life. The guy is obsessed and tells some fantastical stories. Give it a listen.

Trade I’m Considering —

SHORT SALESFORCE (CRM).

Why?

Because it’s a $100B+ market cap company that trades at over 8x sales. It buys nearly all of its growth, as one of the most active and aggressive serial acquirers of tech companies. Often doing zero due diligence, just going off the CEO — who has a major God complex — Marc Benioff’s “gut feel”. It’s also one of the most crowded hedge fund hotels in the market; CRM’s average weighting amongst funds is more than twice its weighting in the S&P. Plus they built the tallest tower in San Francisco and the stock just broke down out of a rising wedge. Also, a million other reasons.

Video I’m Watching —

This “Five Transitions in Energy Happening Now” RealVision video with Rob West is a must-watch (this clip is the 6 minute summary of the longer interview on the site). There are soooo many moving pieces in the energy space right now. Change is happening and this change is only going to dramatically accelerate over the coming decades. Large dislocations like these usually mean large mispricings, which mean large profits opportunities. It pays to stay abreast (literally). Here’s the link.

Book I’m reading —

This week I found myself rereading sections from Drobny’s book Inside the House of Money for a piece I’m writing. If you haven’t read it, House of Money and Drobny’s other book Invisible Hands, are basically Schwager’s Market Wizards books but focused on primarily macro traders.

Both are great reads. I’d highly recommend picking them up. Here’s a quote from the interview with “The Currency Specialist”.

Markets are just a compilation of information we know and information extrapolated from information we think we know. As such, the collective knowledge of a group of people is always higher than the individual parts, even recognizing for experts. Price action tends to confirm that, and price action never lies.

Quote I’m pondering —

In trading, like golf, it’s how you play the bad shots that really matters. How you play the really crap shots is the difference between the good guys and bad guys. When the shit’s hitting the fan, you don’t pull out a 1-iron. You just don’t — you play defense. ~ The “Currency Specialist”, via Inside The House of Money.

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.