Charting is a little like surfing. You don’t have to know a lot about the physics of the tides, resonance, and fluid dynamics in order to catch a good wave. You just have to be able to sense when it’s happening and then have the drive to act at the right time. ~ Ed Seykota

Good morning!

In this week’s Monday Dozen we take a look at CROWDED trades, some of the worst earnings guidance in a decade, the US joining in on the manufacturing recession and more…

1) According to a recent study by BofAML and reported in the WSJ “The overlap in the top 50 stock holdings between mutual funds and hedge funds — two types of investors whose styles typically differ — now stands at near-record levels.”If you’re buying companies like Salesforce (CRM) at these valuations, this late in the game, you may find yourself eating like a bird and crapping like an elephant. Just saying…

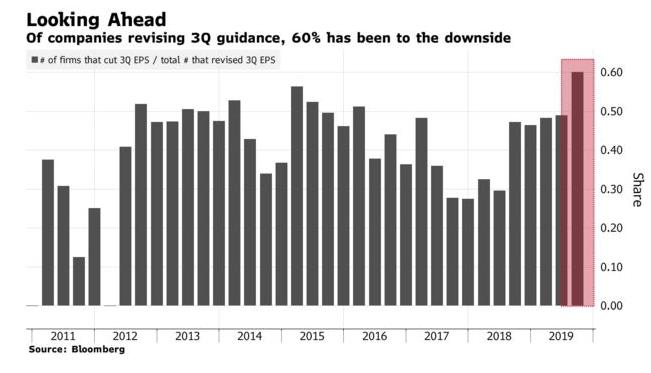

2) Third-quarter EPS guidance is the worst it’s been since 2011 with 60% of companies revising guidance, revising lower (chart via Bloomberg).

3) Upward analyst revisions as a percentage of total revisions for the S&P 500 dropped to 41.3%. You want to see negative expectations being revised higher to sustain a bull run (see 1/16 – 12/17), not this (chart via Citi).

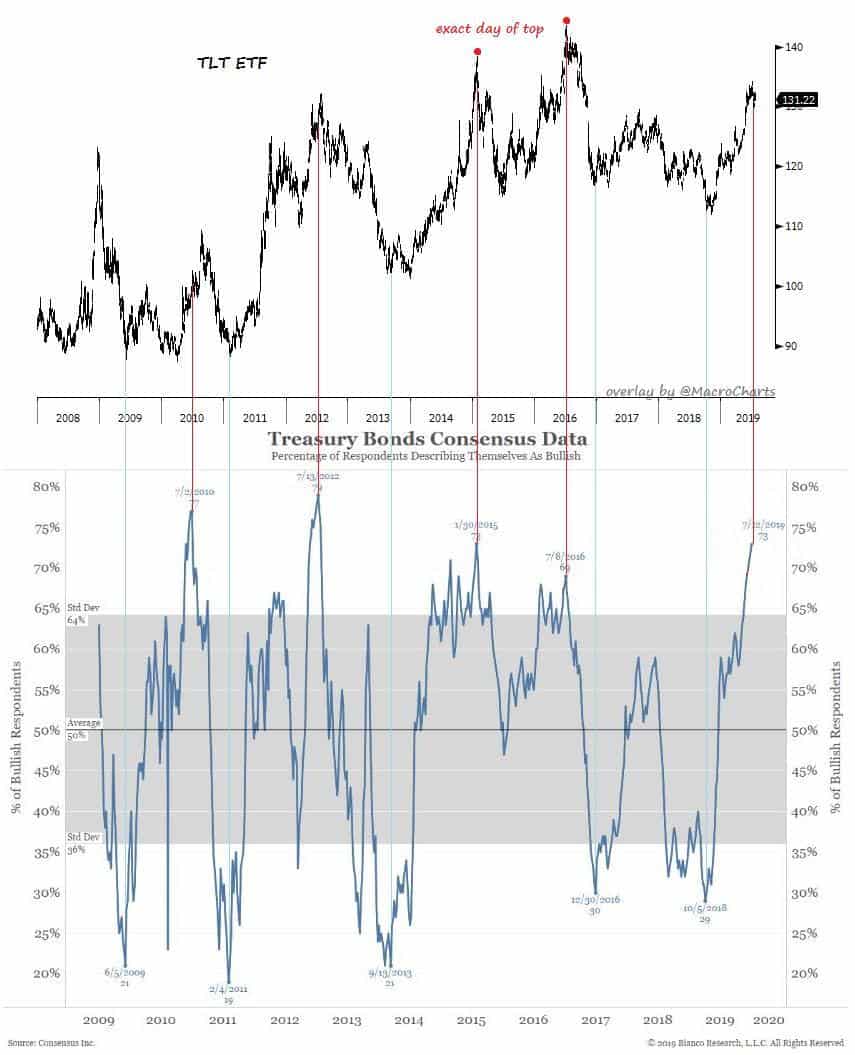

4) There are a LOT of people who are bullish on bonds, which may not be so bullish for, errr, bonds… (chart via Bianco Research and @MacroCharts)

5) Meanwhile, the market’s “implied probability of a large increase in inflation over the next five years” just hit a record low. Maybe the expectations pendulum has swung too far? (chart via @MacroCharts)

6) Shipping rates are trending up and nobody seems to care… The Baltic Dry Index (BDI) recently hit 6-year highs. Here’s a writeup I did earlier in the year laying out the reasons why I’m so bullish on shipping stocks.

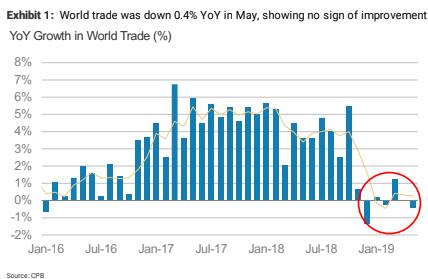

7) And we’re seeing up-trending shipping rates even though global trade is contracting. Just wait until global growth bottoms… (chart via MS)

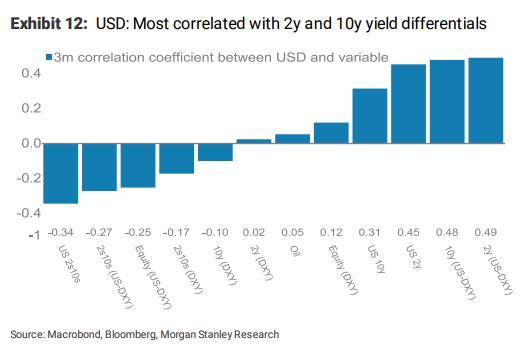

8) The US dollar (DXY) is being driven by 2y and 10y rate differentials. For the dollar to roll over, the Fed needs to get ahead of the market’s dovish pricing and do a surprise 50bps cut this week or strongly signal more willingness to aggressively cut into year end.

9) So keep an eye on this.

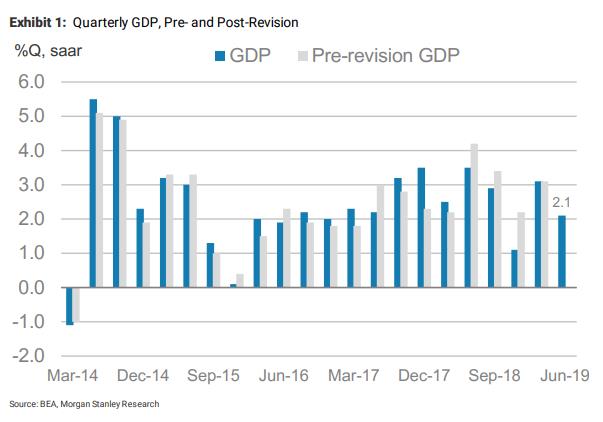

10) 2Q GDP came in at a 1.2% annualized rate and downward revisions reigned in near-term momentum. Morgan Stanley notes that “The slowdown in investment looks even more stark beginning in 1Q18. Net trade, inventories, and profits have also declined… we initiate our 3Q19 GDP tracking at 1.7%” (chart via MS).

11) Revisions versus previous (chart via MS).

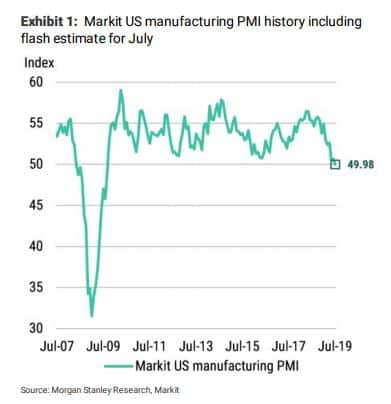

12) The world is in a manufacturing recession and the US is about to join ‘em. Markit’s US manufacturing flash PMI shows the first negative manufacturing PMI print for the US since it clawed its way out of the 09’ recession (chart via MS).