Alex here with your latest Friday Macro Musings…

Latest Articles/Podcasts/Videos —

A Monday Dozen — You guys have spoken and it looks like this is going to be a regular thing. Every Monday I’m going to publish the 12 most interesting charts I come across on my weekend scan. There’s all sorts of data in this post, price action, sentiment data, cycle indicators. Check it out for a quick rundown of the market.

Arlington Value Investors Letters: Five Invaluable Lessons On Value Investing — Mr. Bean poured through 9 years of investment letters from Allan Mecham of Arlington Value and pulled out the 5 most important lessons. This is a little known investor who has compounded money at 37.9% annually since the GFC — a truly mind-boggling sum, so make sure to read this guy’s investing wisdom.

Articles I’m reading —

Bill Miller, the value focused fund manager who set a record for beating the market 15-years in a row before going belly up in the GFC, was interviewed this past week in the WSJ. A lot of people dismiss Miller’s ability because of his blow up but I’ve got respect for the guy and have always found his views on markets and investing insightful and often thought-provoking. Here’s the link to the article (porous paywall, incognito) along with a few excerpts (emphasis mine)

The financial crisis [of 2008] was so overwhelming that I thought it would affect people’s willingness to take risk. So there was a wide gap between perceived risk and real risk. The proper strategy was to look where perceived risk is high and figure out the real risk. You want to buy things where the volatility and perceived risk are above the market. That’s somewhat oversimplified, but the strategy likely gets you in areas of the market where there are excess returns.

And

As Warren Buffett said at the Berkshire Hathaway annual meeting [in early May], stocks are ridiculously cheap compared to bonds and cash. One of the mistakes people tend to make is saying that stocks are expensive because their price/earnings multiple is now 17, compared to a post-World War II average of 15. But that average is distorted by high-inflation periods, including roughly 1973 through 1982, when the P/E ratio was at 7. When inflation, interest rates and volatility are at their current low levels, I would expect the average to be 20. So the P/E ratio is below what you would expect.

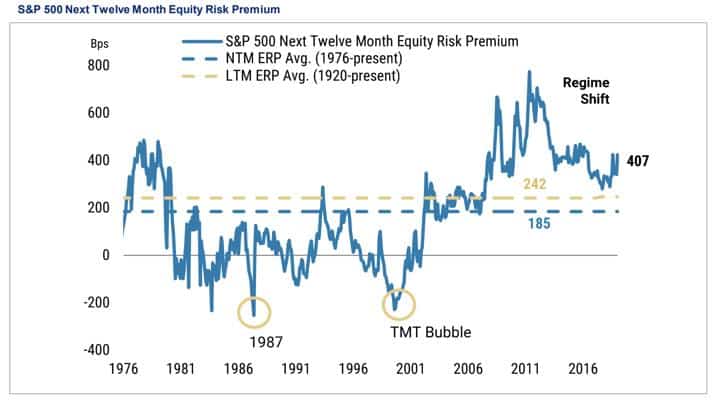

Equities aren’t valued in a vacuum. Valuation is intrinsically a game of relative comparisons. Stocks compete with bonds for capital. Lower bond yields make equities more attractive on a risk-premia basis and lowers the discount rate at which their cash flows are valued. The current equity risk premia is still well above its historical average (see chart below).

That’s not to say there aren’t pockets of the market that are ridiculously overvalued. There are. But it’s important to remember that there’s a lot more to understanding aggregate valuations than looking at simple price-to-earnings multiples sans context. Doing so can be an expensive mistake that even the best in the game sometimes make — read this Forbes piece titled “Don’t Be a Yield Pig” by Seth Klarman where he lambasts the ridiculously low interest rates and crazy high stock valuations — the article was written in February of 1992. Here’s the link and an excerpt.

Some investors, desperate for better yield, have been reaching not for a new Wall Street product but for a very old one–common stocks. Finding the yield on cash unacceptably low, people who have invested conservatively for years are beginning to throw money into stocks, despite the obvious high valuation of the market, its historically low dividend yield and the serious economic downturn currently under way.

How many times have we heard in recent months that stocks have always outperformed bonds in the long run? Funny, but we never hear that argument at market bottoms. In my view, it is only a matter of time before today’s yield pigs are led to the slaughterhouse. The shares of good companies and bad companies alike are vulnerable to sharp declines.

(Note to Collective members: I wrote more about this topic in our Feb 17’ MIR titled Margin of Spread which is hung up in our archives if you’d like to read more.)

Patrick O’Shaughnessy (@patrick_oshag) recently asked people on the twitter to share the best blog post they’ve ever read. You can find the responses in the following thread (link here). I’ve spent much of my downtime over the last week reading my way through the list. If used correctly, Twitter can be the most effective AI for information aggregation and filtering, harnessing the wisdom of the collective. It’s a pretty awesome tool… Here’s a few of my favorite posts that I’ve read so far.

Alex Danco’s post titled “Secrets about People: A Short and Dangerous Introduction to René Girard” (link here).

I’ve come across Girard’s work a number of times lately as I’ve been studying up a bunch on the human impulse to imitate others and Girard constructed an entire philosophy around what he called mimetic desire. This post talks about that and many of Girard’s other contributions to understanding human nature. Peter Thiel credits much of his “trademark contrarian style” to Girard’s philosophy which makes more sense after reading the post.

You can follow up that post with this one from Slate Star Codex titled a Book Review: The Secret of our Success which is really not a book review but a wide-ranging discussion on the role that culture plays in pushing humanity’s collective intelligence forward. It’s complementary to the post on Girard. Here’s the link.

Lastly, read this awesome lecture given by William Deresiewicz at West Point titled Solitary Leadership. The talk is about leadership but also so much more. Here’s a cut and the link (there’s also an option to listen to the speech, which is about 30 minutes long).

I find for myself that my first thought is never my best thought. My first thought is always someone else’s; it’s always what I’ve already heard about the subject, always the conventional wisdom. It’s only by concentrating, sticking to the question, being patient, letting all the parts of my mind come into play, that I arrive at an original idea. By giving my brain a chance to make associations, draw connections, take me by surprise. And often even that idea doesn’t turn out to be very good. I need time to think about it, too, to make mistakes and recognize them, to make false starts and correct them, to outlast my impulses, to defeat my desire to declare the job done and move on to the next thing.

Oh, and Michael Mauboussin shared this slightly older research paper of his where he discusses various analytical methods for estimating a company’s total addressable market (TAM). Here’s the link.

Charts I’m looking at—

US stocks have trounced their European counterparts over the last decade. We should ask ourselves, is this trend likely to continue indefinitely? If not, and we see some mean-reversion, what will that look like? Currencies are driven by speculative flows which chase relative market performance, so what would an unwind of just some of this trend do to EURUSD spot?

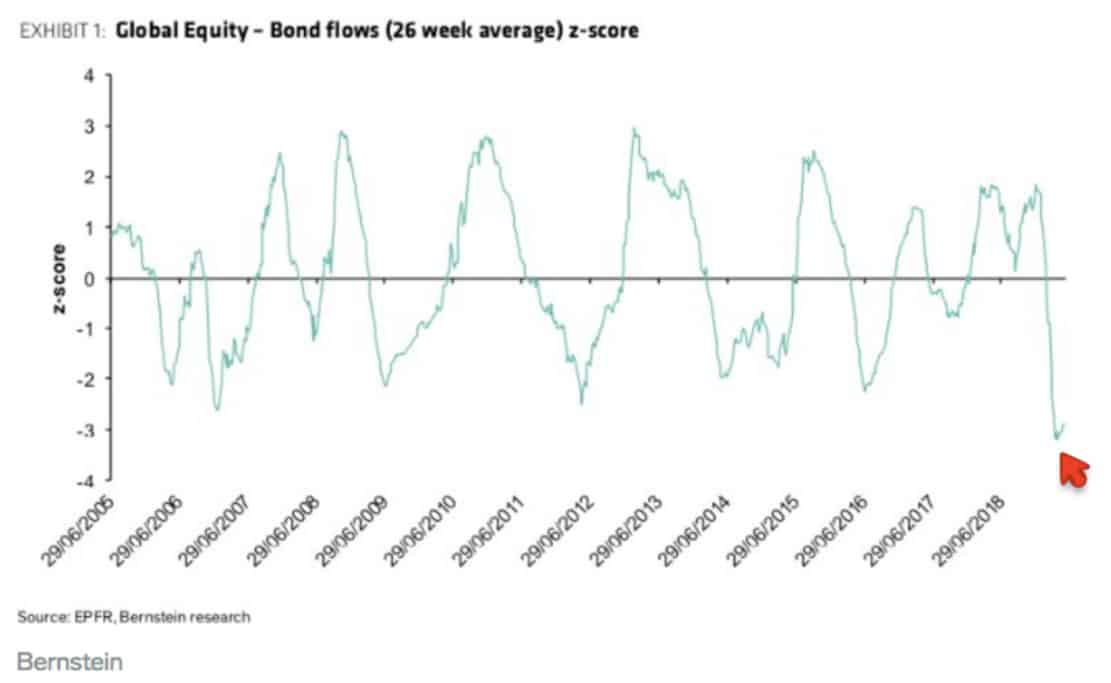

Bernstein put out the following chart (h/t @ukarlewitz) showing the z-score for global equity – bond flows. Relative flows just hit 3 standard deviations, making for the most extreme flow disparity on record, even exceeding that of 08’. Bernstein notes that similar instances have “portended large stock-market gains ahead.”

Bernstein put out the following chart (h/t @ukarlewitz) showing the z-score for global equity – bond flows. Relative flows just hit 3 standard deviations, making for the most extreme flow disparity on record, even exceeding that of 08’. Bernstein notes that similar instances have “portended large stock-market gains ahead.”

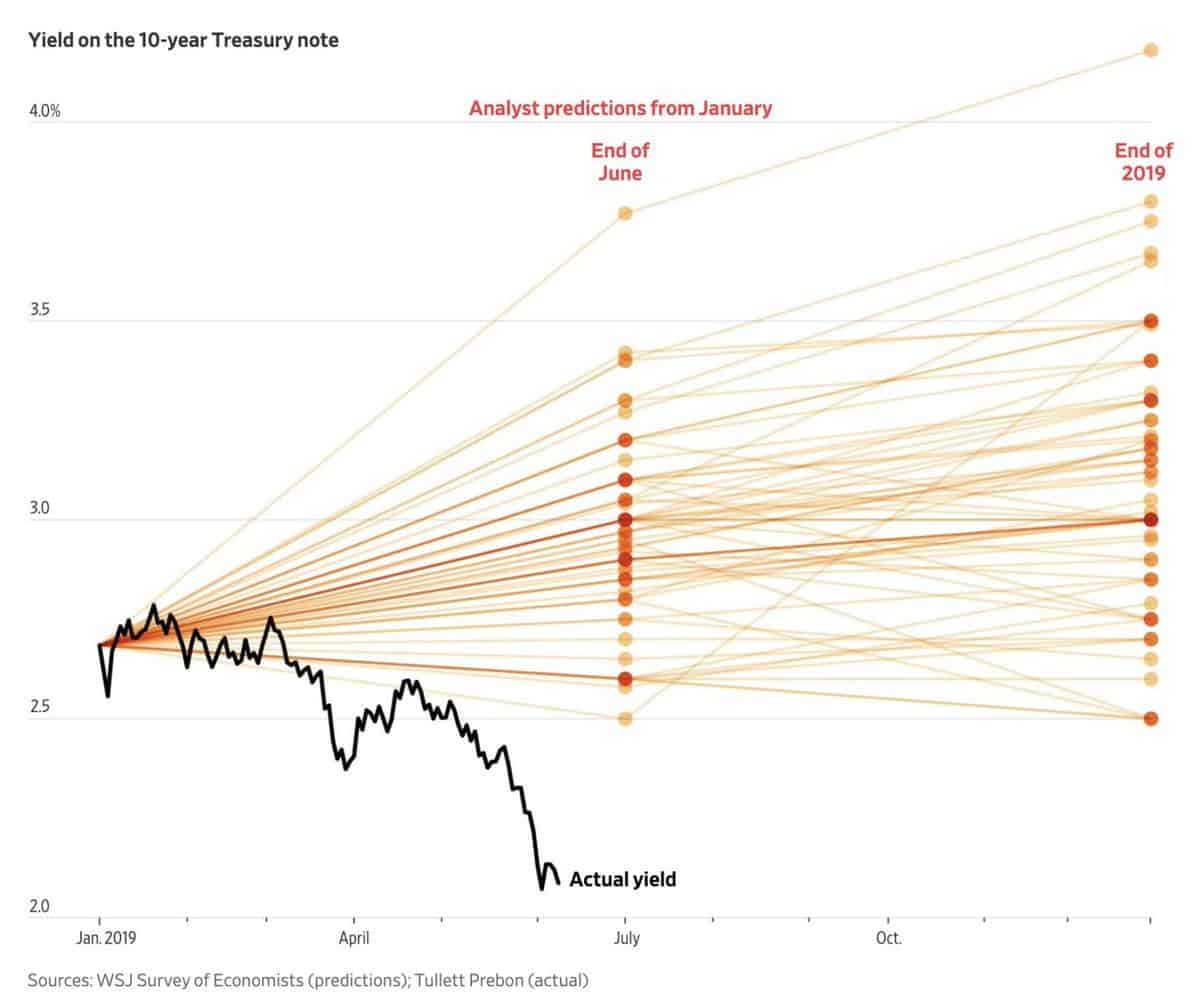

And finally this… A chart showing economist’s predictions on where the UST 10-year yield was going to trade 6 and 12 months out. This is just a friendly reminder that nobody in this game KNOWS anything; especially the “experts”.

Video I’m watching —

This is a killer video. It’s a panel discussion with some of my favorite small-cap value investors (i.e., Scott Miller, Matt Sweeney, Dan Roller etc…) It kicks off with a talk from Miller on foundational value investing concepts and then leads into a round table discussion and Q&A with all the other managers where they talk process, the business aspects of running a fund, managing risk, and a host of other things that go into being a successful value fund manager. Here’s the link.

Book I’m reading —

I just started reading Range by David Epstein this week after listening to his interview on the Invest Like the Best podcast. I’m only about 20-pages in so can’t say much on it yet. I’ll share my thoughts in next week’s musings. But another book that I’m reading which I can recommend is The Bhagavad Gita translated by Eknath Easwaran.

I’d read The Bhagavad Gita years before (though it was a different translation) and enjoyed it but found sections of it tough to get through and comprehend. Easwaran’s translation makes for a much easier read and after reading this version (I’m nearly done) I’ve got to say that this book is likely going onto my short-list of regular rereads; Easwaran’s translation of The Upanishads, one of my all-time favorite books, is also on there).

The book is short but jam-packed full of wisdom on how to live a good life. I highly recommend giving it a read.

Trade I’m considering —

Back in September of 2016 I pitched a Colombian oil & gas stock in our monthly report writing:

EC recently completed an expensive modernization project on its largest refinery (Reficar). The project was plagued by cost overruns and typical Lat-Am corruption and scandal; which led to a 100% cost increase to the tune of $8B. But now all of that’s behind it and the company possesses the largest and most efficient refinery in Latin America — making it competitive with the major refineries in the US (where it exports a lot of its product). With the major one-time capital expenditures out of the way, the company should see improving margins moving forward, bolstered by the better throughput efficiency of the modern refinery.

Investors entering into any of these stocks will be getting in near a secular bottom for Colombia. There’s big potential for long-term appreciation in these plays.

Ecopetrol SA (EC) ran up over the following two years from a price of around $8.50 to a high of $28 for a gain of roughly 230%. I participated in absolutely none of this rally, personally, but that’s besides the point… The point is… that — and you should know this if you read me regularly — I’m becoming very bullish on oil & gas stocks.

There’s incredible value in this space and the catalyst that we need to send these stocks ripping higher is a weaker dollar, which I think is coming. EC trades at just over 4x EV/EBITDA, has highly valuable strategically located assets, and a nice chart pattern forming. Another dirt cheap integrated oil & gas company that’s worth keeping on your radar. Oh, and then there’s also stuff brewing between the US and Iran that reeks of a setup by Bolton and crew to create cause for toppling the Iranian regime. But I’ll leave that topic for another writeup on another day…

Quote I’m pondering —

Certainly, if we reflect on the thousands of years that are past, of the millions of men who lived in them, and we ask,

“What were they? What has become of them?

But, on the other hand, we need only recall our own past life and renew its scenes vividly in our imagination, and then ask again,

“What was all this? What has become of it?”

As it is with that past life, so is it with the life of those millions. Our own past, the most recent part of it, and even yesterday, is now no more than an empty dream of the fancy, and such is the past of all those millions.

Whoever has not yet recognised this, or will not recognise it, must add to the question asked above as to the fate of past generations of men this question also: Why he, the questioner, is so fortunate as to be conscious of this costly, fleeting, and only real present, while those hundreds of generations of men, even the heroes and philosophers of those ages, have sunk into the night of the past, and have thus become nothing; but he, his insignificant ego, actually exists? or more shortly, though somewhat strangely:

“Why this now, his now, is just now and was not long ago?”

~ Arthur Schopenhauer, The World as Will and Idea (h/t @Jesse_Livermore)

I love that.

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.