“Around here there are three kinds of investors. Growthies, guys who love growth stocks, don’t care about valuations, and only buy stocks with strong price momentum; geeks, who are quants and invest off computer models; and shitheads, who are value investors. In other words, they buy the stocks of dirty, shitty companies because they are cheap.” ~ Barton Biggs, “A Hedge Fund Tale of Reach and Grasp”

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at corporate profits, a market “squeeze”, Hedger positioning, grossly extended semis, repaired balance sheets, bearish USD drivers, overbought emerging markets, gold’s bull run, a lagging Russian steel stock with 3x potential and more…

Let’s dive in.

***click charts to enlarge***

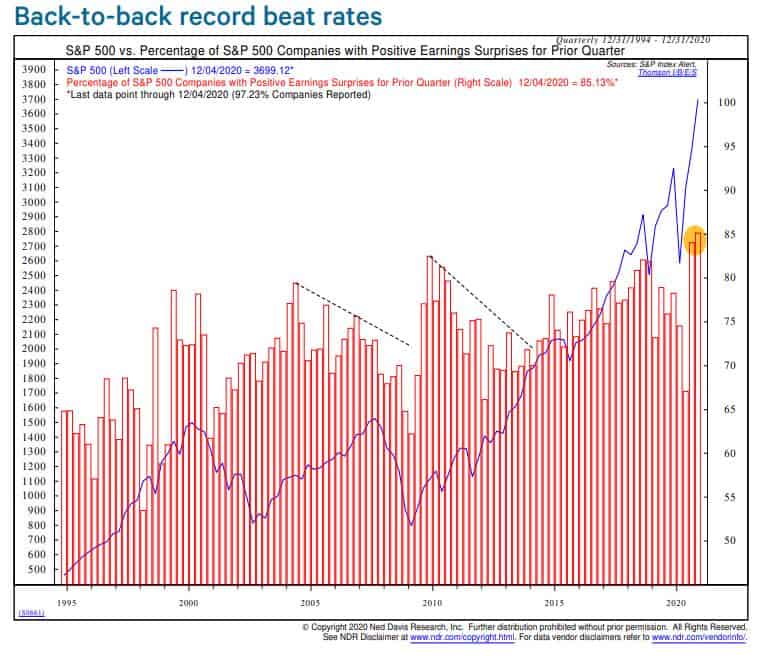

- We’ve been noting in these pages how the consensus continues to set the earnings hurdle low, giving the market an easy bar to clear. @edclissold of NDR, shared this chart this week, writing “ Of all the questions I gotten about the market recovery, surprisingly few (to me) have been about corporate profits. $SPX on track for a second consecutive record beat rate. Counterargument: estimates were cut so much that they were easy to beat. True, but…”

The consensus is still too low on next Qs numbers. Corporate profits are seeing a strong rebound, expect another easy beat…

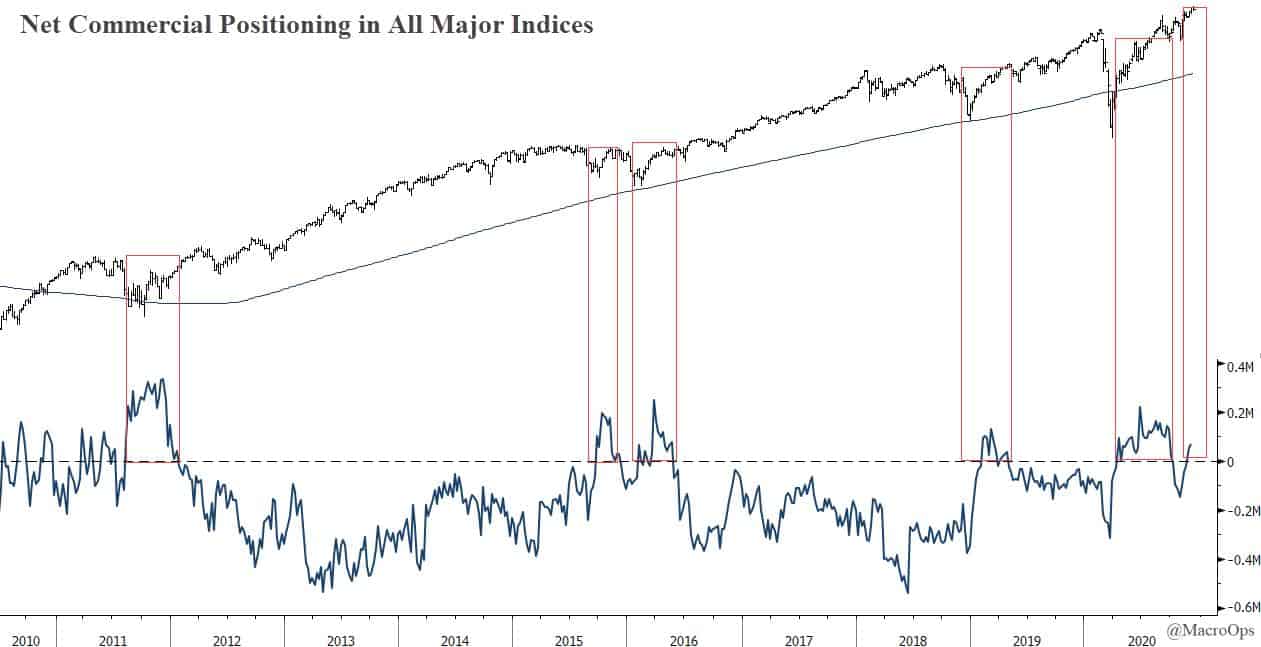

- I keep coming back to this positioning chart because it paints such a different picture than all the others. It shows net commercial positioning in all major indices is positive. Meaning, conversely, that specs are still short. This is typically more common at bottoms than tops.

- This is from JPM via The Market Ear.

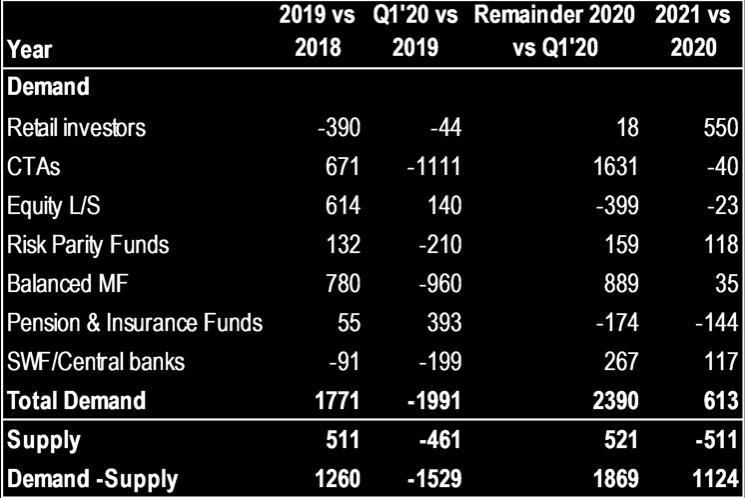

“Squeeze: a >$1 trillion better demand outlook for equities in 2021

And is not even Powell. JPM sees a much better supply/demand outlook for equities in 2021. Take it away Nikos:

“1. For 2021 we see an overall improvement in equity demand of around $600bn relative to this year. This projected improvement is driven by retail investors as well as SWFs and Risk Parity funds.

“2. At the same time we expect that global net equity supply will return next year to the very low levels of 2016-2018, i.e. a decline of $500bn relative to this year, as share buyback/LBO activities normalize and the need for equity raising subsides.

“3. Adding up all the projected equity demand changes between 2020 and 2021 and subtracting the supply change, we come up with an equity demand/supply improvement of $1.1tr in 2021 relative to 2020.”

I’ve been writing over the last few months about how we’re entering “silly season” in the market. Here’s more evidence of what’s coming…This is incredibly bullish depending on your timeframe and risk tolerances.

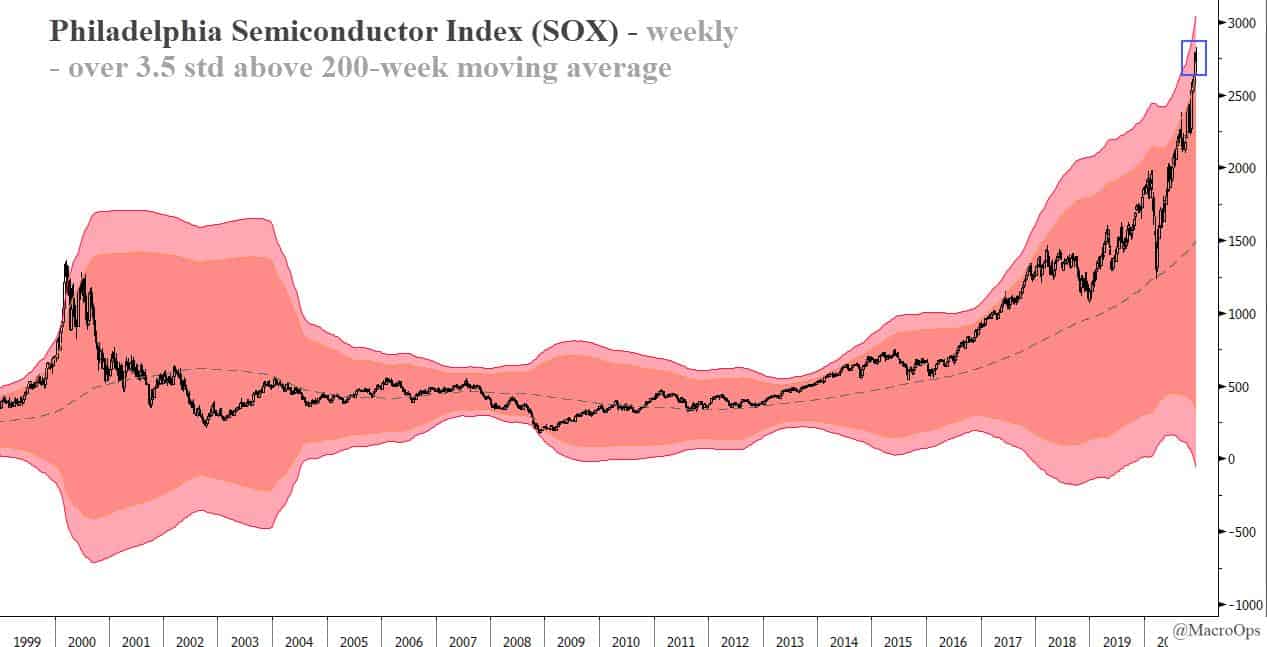

- Semis are one of my favorite leading indicators of broader market risk sentiment. The SOX index is currently 3.5x std above its 200-week moving average. That’s a bit overextended *understatement*. But, as we saw in 99’, overextension can lead to more overextension.

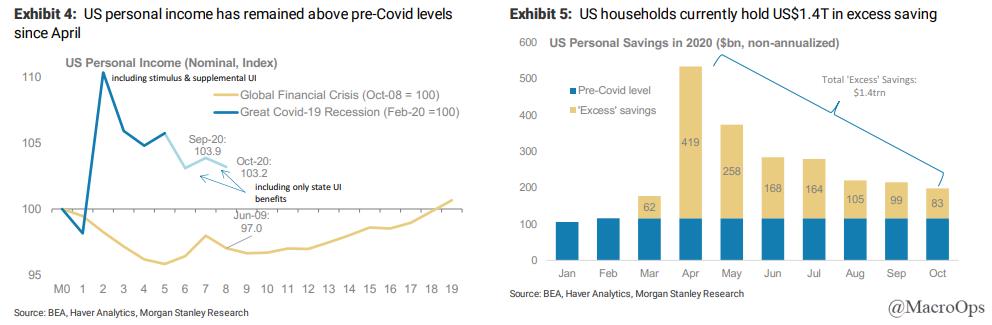

- Morgan Stanley is more bullish than the consensus on the global economic recovery. I side with them on this one. One of the major reasons why, is the incredible boost we’ve seen to consumer balance sheets this year. MS writes “US households are currently holding on to an excess saving of US $1.4 trillion, which equals about 9.3% of 2019 annual consumption expenditures.” There’s quite lot of pent up demand coming.

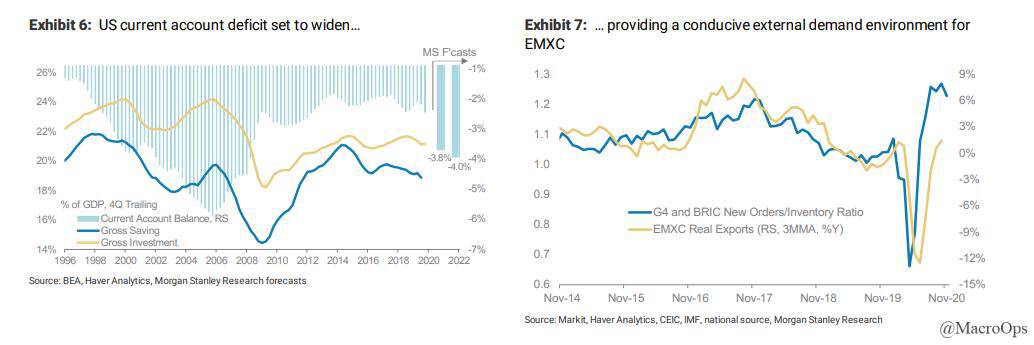

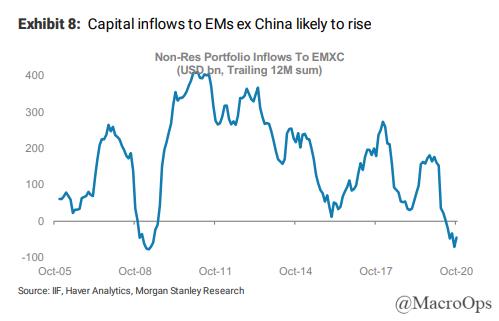

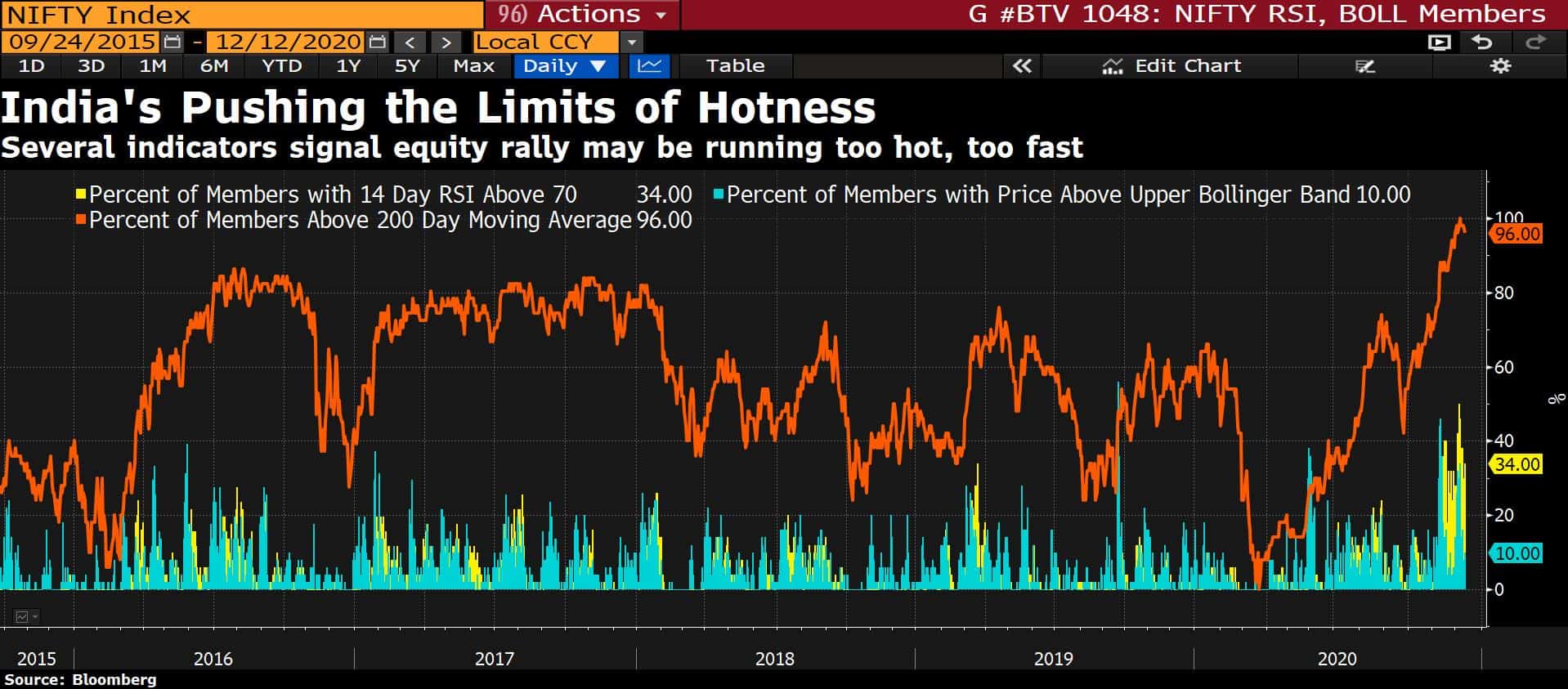

- We at MO have been bullish on EM and international equities for a while now. And while they’ve had a tremendous year, we believe this is just the start of a new leadership regime.

A big support to this trade is a weakening dollar. MS notes that “After aggressive fiscal expansion, the Fed’s decision to keep real rates low for longer will mean that the US current account deficit will widen significantly. This should boost EM exports and push the US dollar lower.”

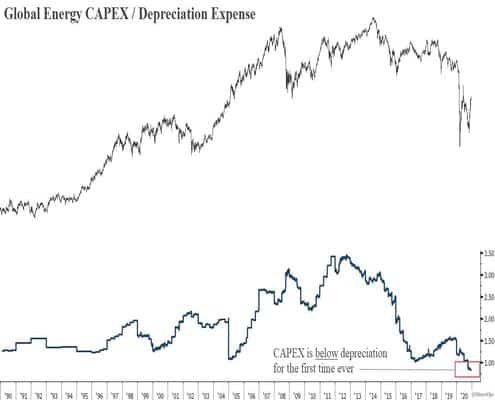

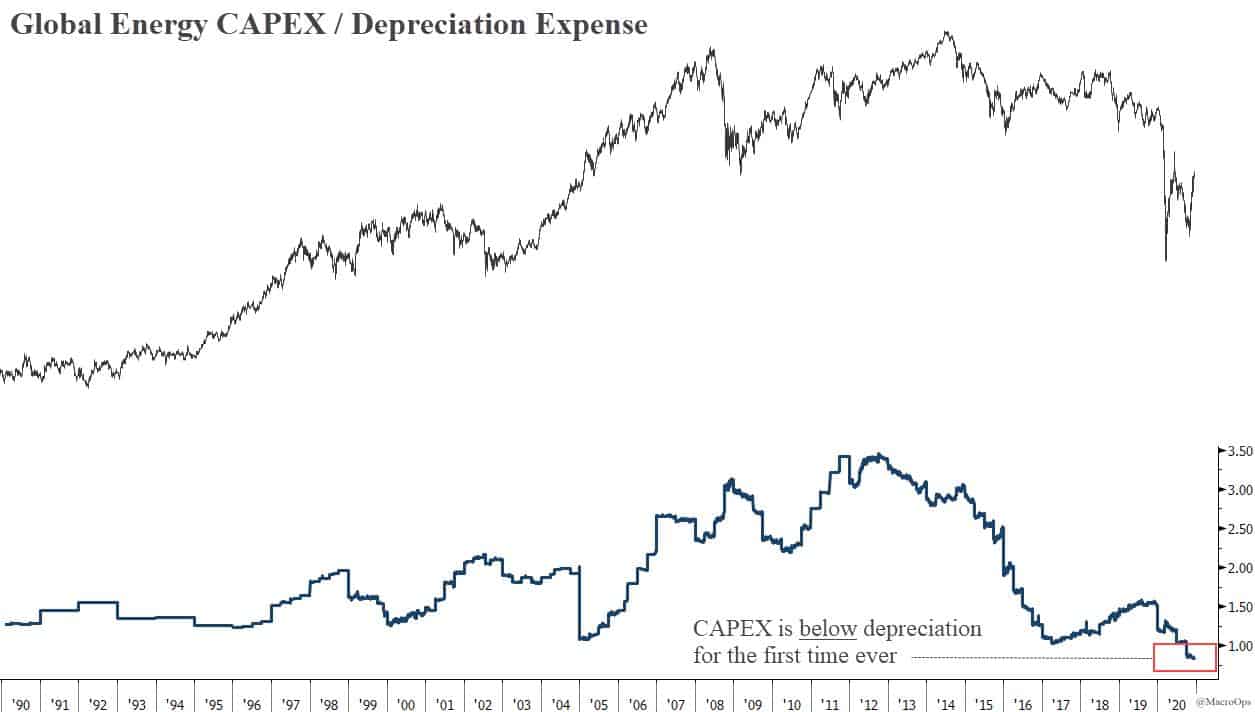

- EM is a synthetic short USD trade. Another short USD trade we like are commodities, and the energy space in particular. Wealth S-curve dynamics will drive commodity demand exponentially higher over the coming decade while our ability to meet that rising demand is becoming questionable. Global Oil & Gas CAPEX vs Depreciation is at an all-time low.

- There’s a lot of room to reverse these flows (chart via MS).

- But the trade is becoming extended in the interim so be mindful of your entries and stop placement (chart via BBG).

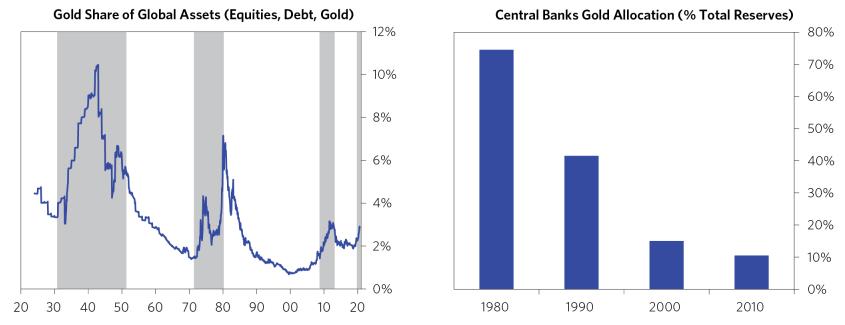

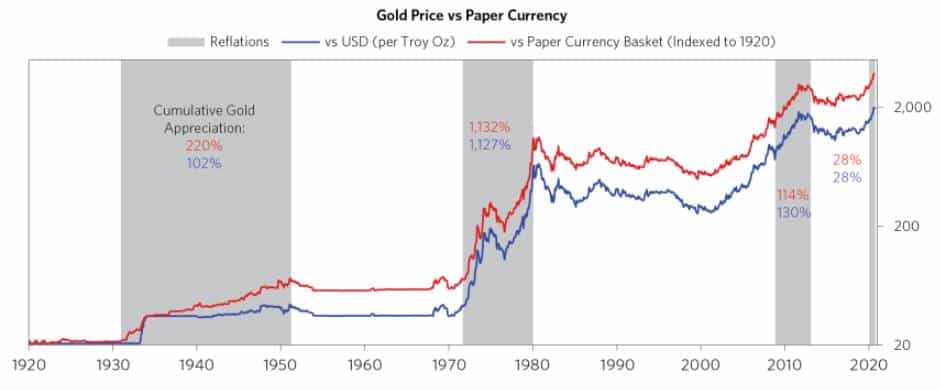

- I get asked a lot about my current views on gold. I’m long-term bullish and short-term agnostic. I don’t currently hold a position. The 1,850 level is key and I’ll consider getting in again on a sustained break above that level.

The charts below from Bridgewater show there’s a long runway for more appreciation in the barbarous relic.

- The Long-term debt cycle in chart form. The source of our current global societal woes.

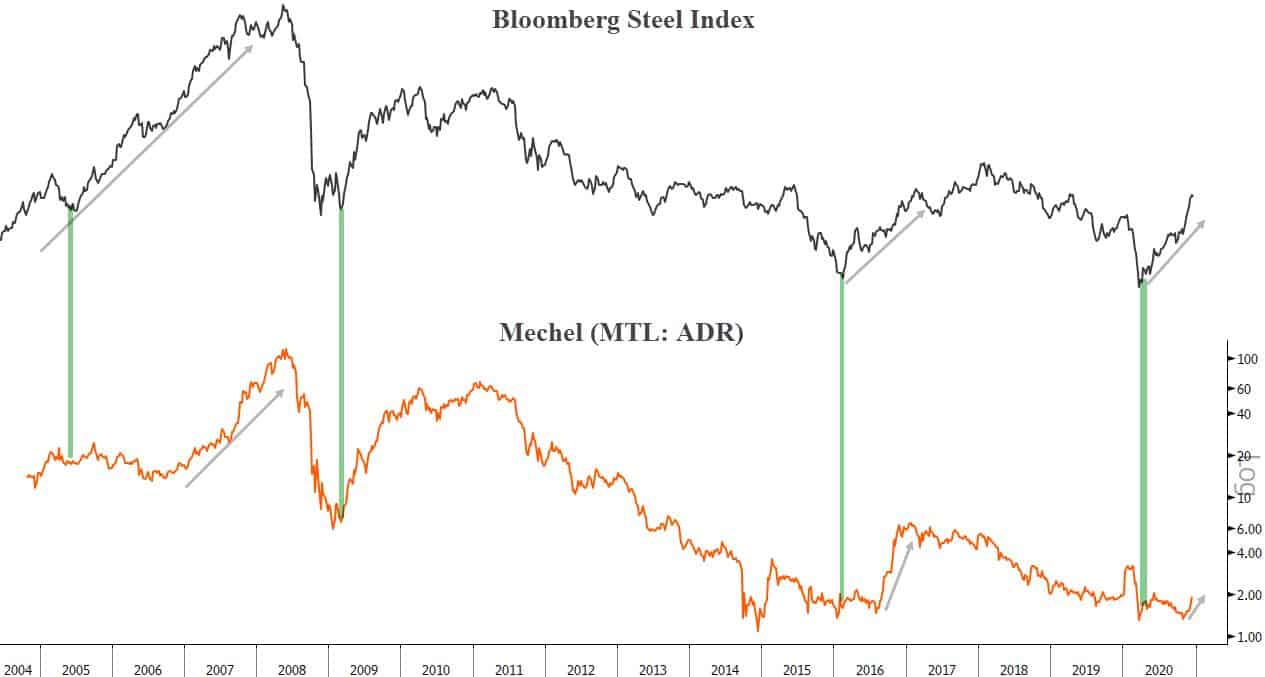

- Here’s a speculative play I’m in. MTL is a Russian steel ADR. It’s a garbage company but a fun stock to trade. It has a tendency to go on vertical runs. One of the reasons I like MTL, besides the big swings, is that it’s historically shown a fairly predictable lag in action to steel stocks globally. This makes the setups fairly easy to time.

I wrote this one up in the MO slack when I bought a position on November 30th. Two days later it spiked up 70% and I was able to cash out on some of the trade. I started adding back again early last week and the tape has since shown some nice strength.

I’m keeping a tight leash on the trade and will be quick to dump if price breaks some key levels. But, looking at the run in MTL’s peers, I wouldn’t at all be surprised to see this thing go on a quick double or triple from here.

Stay safe out there and keep your head on a swivel.