What a wild week in markets. This morning (Monday), the S&P 500 went limit-down and triggered the circuit-breakers. That’s never happened. There will be textbooks written about this week and these trading days. Oh, and did I mention oil futures dropped over 35% at one point?

Unreal.

For younger traders/investors, things look crazy. And they are. But if there’s any silver lining it’s that you’re now earning your stripes. Markets were (for the most part) relatively easy the last few years.

I’m not saying you were sure of profits. But close your eyes and throw a dart at an S&P heat-map and you’d do well.

Now’s a good time to remind you of Warren Buffett’s two rules:

-

- Don’t Lose Money

- Don’t Forget Rule #1

Our Latest Podcast Episodes:

- Episode 15: Nick Haschka, The Wright Gardner & Cub Investments (NEW)

- Episode 14: Ryan Reeves, InvestingCity.org

Also, if you have the time, please subscribe and leave a rating/review of the podcast on Apple Podcasts. It goes a long way in spreading the word about the show.

Here’s what we cover this week:

-

- The Elephant In The Room (Oil & Gas Stocks)

- Howard Marks’ Latest Memo

- Magic Formula Top Five

There’s blood in the streets — time to get to work!

—

March 11, 2020

Never Before In History: Here’s a friendly reminder on circuit-breaker rules in case we get them at the tail-end of the week:

Circuit-breakers today:

* If the S&P 500 declines 7%, (208 points), trading will pause for 15 min

* If declines 13%, (386 pts) trading will again pause for 15 mins

* If falls 20%, (594 pts) the markets would close for the day.

(via @peterschack) @CNBC

— Carl Quintanilla (@carlquintanilla) March 9, 2020

__________________________________________________________________________

Investor Spotlight: Howard Marks’ … Nobody Knows

GIFs by tenor

GIFs by tenor

Howard Marks released his latest letter titled, Nobody Knows II. Marks covers a few main topics:

-

- Being OK with not knowing

- The potential impact of COVID-19

- Did prices change on fundamentals, or something else?

Marks admits he doesn’t know anything about the coronavirus. Nor its potential impact on financial markets. It’s a breath of fresh air after scrolling through my Twitter feed. Apparently everyone is a licensed epidemiologist over there.

Take this section for example (emphasis mine):

“And that leads me back to the coronavirus. No one knows much about it, since this is the first appearance. As Harvard epidemiologist Mark Lipsitch said …, there are (a) facts, (b) informed extrapolations from analogies to other viruses and (c) opinion or speculation.”

Marks believes we don’t have enough facts to make proper scientific extrapolations. And given that premise, anything else on the topic is mere speculation.

How COVID-19 Could Affect The Economy

Marks lists a few obvious negative effects:

-

- Contraction in economy due to factory closures

- Decline in retail spending

- Less travel

But the most important thing (pun intended) according to Marks is supply chain issues (emphasis mine):

“The unavailability of a small Chinese component can cripple the production of a large piece of equipment. And it only takes one, unless there are alternative sources. Relocating sourcing will be a challenge: it’ll take time, and there’s no assurance that the new locations won’t become engulfed in the disease.”

How To Think About Price & Fundamentals

My favorite part of the memo involves investor reactions to such news. Marks hits it home here (emphasis from letter):

“There’s no doubt about the fact that the coronavirus represents a major problem, or that the reaction so far has been severe. What really matters is whether the price change is proportional to the worsening of fundamentals.”

That’s what matters. If it does, the sell-off makes sense (and it might not be over). If coronavirus doesn’t change fundamentals, this is an overreaction.

__________________________________________________________________________

Movers & Shakers: RIP Oil & Gas Industry & Blue Chip Misery

GIFs by tenor

GIFs by tenor

With oil down over 30% at one point Sunday night, we’re (almost) guaranteed to see heads roll in the space.

Who will win out? Who will go bust? Who knows.

That said, I want to highlight some O&G stocks that might right this ship. If these companies can manage such massive drawdowns in oil prices, they’ll skyrocket at any recovery.

Here’s my list:

-

- Flotek (FTK)

- ExxonMobil (XOM)

- British Petroleum (BP)

- Dawson Geophysical (DWSN)

Let’s break each down.

Flotek (FTK)

As of writing this (Monday afternoon), FTK trades around $1/share. The stock’s down over 20% today. Here’s the chart (warning NSFW):

Things (clearly) aren’t great for FTK. On a TTM basis the company lost $75M in operating income and generated -$66B in EBITDA.

So what’s to like? The balance sheet. In fact, FTK is a net-net.

The company has $152M in current assets ($100M is cash) against $58.6M in total liabilities. That’s $93.4M in NCAV. Compare that with the company’s $59M market cap and you get a 58% discount to NCAV.

Not bad.

At this point it’s hard to tell if the company’s purely a melting ice-cube. Here’s my take:

-

- A clear bounce on this support level could provide a great reward/risk entry opportunity to own a net-net with a strong balance sheet and loads of cash.

Exxon Mobil (XOM)

There’s not much I can add to the XOM thesis that hasn’t already been said. The stock’s trading at 11x EBITDA and <15x earnings. That’s not even the wild part.

XOM has the chance to trade below book value. Think about that. A giant like XOM could trade below book value. I bet Buffett’s got his eyes on that one.

Here’s the chart …

It’s all bad. We’re in the throes of falling knife territory on the monthly chart. I’d wait for consolidation on the weekly chart. I want XOM to put in a base before looking to go long.

British Petroleum PLC (BP)

If you look at the charts, BP’s headed for lower prices — much lower prices. Looking at the monthly time-frame we find a HUGE descending triangle …

Here’s some financials:

-

- EV/EBITDA: 5.5x

- Dividend Yield: 8%

- Debt/Equity: 0.76x

- (EBITDA-Capex) / Interest Expense: 7.8x

BP has a solid financial standing. I would love for this stock to trade even further down. The next price support on the monthly chart is around $10/share. If only we would get that lucky.

Dawson Geophysical (DWSN)

Dawson Geophysical Company provides onshore seismic data acquisition services in the United States and Canada. The company acquires and processes 2-D, 3-D, and multi-component seismic data for its clients, including oil and gas companies, and independent oil and gas operators, as well as providers of multi-client data libraries (via TIKR.com).

DWSN is a micro-cap company with a market cap around $34M. Their balance sheet is one of the strongest I’ve seen in their sector. They sports $17M in net cash for an EV of $17.4M.

They’ve grown EBITDA each of the last three years, doing $5.6M in 2019. Yet on a GAAP basis, the company lost $0.66/share in earnings last year.

Let’s head to the charts …

The last time DWSN traded this low was 2003-04. Incredible. Since that time the company’s double NCAV (but loses money).

Another Net-Net

Yesterday’s decline pushed DWSN into net-net territory. The company has around $1.77/share in NCAV against $1.49/share market cap.

They have a strong balance sheet, but remain exposed to melting ice-cube syndrome.

__________________________________________________________________________

Magic Formula Galore — Ideas Abound

GIFs by tenor

GIFs by tenor

I don’t normally follow large/mega-cap stocks. But times like these are a good reminder that severe price dislocations can happen at the highest orders of market cap.

Don’t worry, I ran a Magic Formula screen on Tuesday so you don’t have to.

Here’s the top five names sorted by market cap (US-only):

-

- AbbVie, Inc. (ABBV)

- Altria Group (MO)

- Biogen, Inc. (BIIB)

- Progressive Corp (PGR)

- Allstate Corp (ALL)

These are great businesses trading at cheap prices. Let’s take a look at how cheap along with their price charts.

AbbVie, Inc. (ABBV)

AbbVie Inc. discovers, develops, manufactures, and sells pharmaceutical products in the United States, Japan, Germany, Canada, Italy, Spain, the Netherlands, the United Kingdom, Brazil, and internationally. – TIKR.com

Here’s some financial ratios:

-

- P/E: 16.8x

- EV/EBITDA: 10x

- Dividend: 5.53%

- Pre-Tax Margin: 25%

- ROIC: 19%

Here’s the chart …

Current prices imply a 10% EBITDA yield, along with a 5% dividend. That’s not bad.

Altria Group (MO)

Altria Group, Inc., through its subsidiaries, manufactures and sells cigarettes, smokeless products, and wine in the United States. It offers cigarettes primarily under the Marlboro brand; cigars principally under the Black & Mild brand; and moist smokeless tobacco products under the Copenhagen, Skoal, Red Seal, and Husky brands. – TIKR.com

I know, everyone hates MO — that’s why it’s interesting. Check out their stats:

-

- EV/EBITDA: 8x

- Dividend: 8.32%

- Operating Margin: 53%

Their main products (cigarettes, etc.) falls victim to ESG-hungry virtue signalers. Yet their capital allocation policy remains extremely shareholder friendly.

The goal is to return whatever cash MO generates to its shareholders through buybacks and high dividends.

Here’s the chart …

The stock’s in a clear downtrend with momentum to the short side. But it looks like MO put in a potential double-bottom on the weekly chart. If you’re looking to dip your toes into the market, a tight stop long around these levels would be interesting.

Biogen, Inc. (BIIB)

Biogen Inc. discovers, develops, manufactures, and delivers therapies for treating neurological and neurodegenerative diseases worldwide. – TIKR.com

Warren Buffett bought BIIB as reported in his last portfolio filing. It’s a small position, 0.08% of Berkshire. What does Warren like about BIIB? It could be the following:

-

- P/E: 10x

- EV/EBITDA: 9x

- Pre-Tax Margins: 56%

- ROIC: 31%

- Free Cash Flow: >$6B

No wonder Buffett bought. Let’s take a look at the charts …

Lots of sideways consolidation. Right now no clear move to the upside or downside. But again, we have a massive blue-chip stock trading at an 11% yield to EBITDA. That’s not bad!

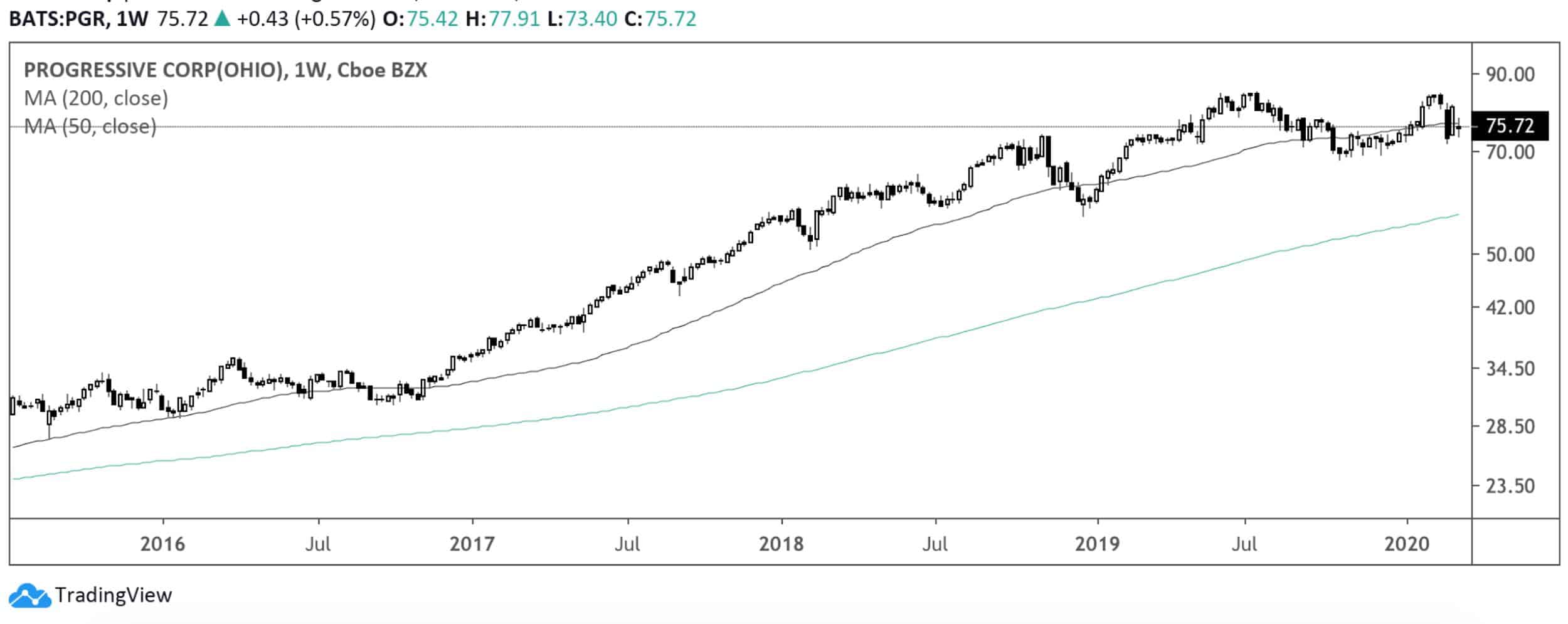

Progressive Corp (PGR)

The Progressive Corporation, through its subsidiaries, provides personal and commercial auto insurance, residential property insurance, and other specialty property-casualty insurance and related services primarily in the United States. – TIKR.com

PGR is a fantastic company at a cheap price. Don’t believe me? Check out these numbers:

-

- P/E: 12x

- P/S: 1.21x

- Debt/Equity: 0.33x

- ROIC: 24%

Insurance is a great business with a long runway and never-ending tailwinds. Let’s take a look at the charts …

Allstate Corp (ALL)

Another insurance company made the top-five on Joel’s Magic Formula screener.

The Allstate Corporation, through its subsidiaries, provides property and casualty, and other insurance products in the United States and Canada. – TIKR.com

Here’s the financial run-down:

-

- P/E: 7.6x

- Debt/Equity: 0.27x

- Dividend: 2.25%

- Pre-Tax Margin: 14%

- ROIC: 16%

ALL offers a 13% earnings yield at current prices while paying 2.25% in dividends. Let’s take a look at the charts …

Look for the 200MA to act as support should prices fall to those levels.

__________________________________________________________________________

Resource of The Week: Market Dialogue with Peter Brandt

GIFs by tenor

GIFs by tenor

Peter Brandt is one of the greatest traders to ever live. How did he do it? Classical charting principles, of course. As you know, I’m biased towards Peter’s style of trading.

While not a pure classical chartist, I always learn something new from each Peter Brandt interview.

I recently stumbled across a three-part interview series between Brandt and Jack Schwager (author of Market Wizards series). It’s a gold-mine of information:

You’re welcome for your next long car ride.

__________________________________________________________________________

Tweet of The Week: Alex Barrow With The Humor

$BA stock imitating the flight path of one of its planes

— Alex Barrow (@MacroOps) March 10, 2020

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!