“Whoever wishes to foresee the future must consult the past; for human events ever resemble those of preceding times…this arises from the fact that they are produced by men who have been, and ever will be, animated by the same passions.” ~ Niccolò Machiavelli

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at earnings season data, high valuations, bullish expectations, and record levels in sentiment and positioning… we then talk about what this means going forward, look at some inflation drivers, and reiterate our bull case for precious metals, plus more….

Let’s dive in.

***click charts to enlarge***

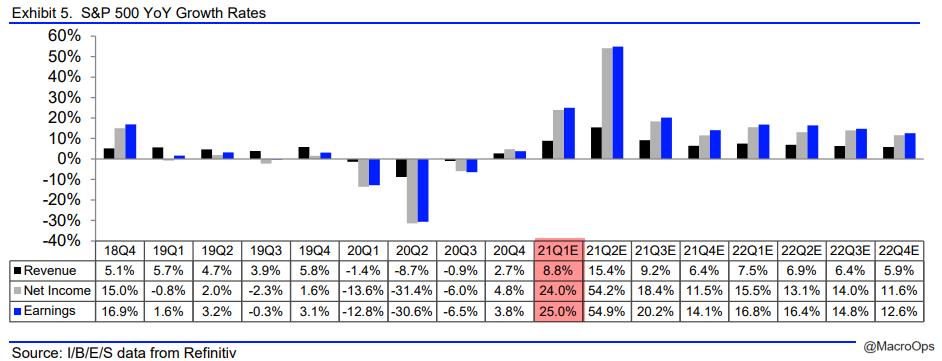

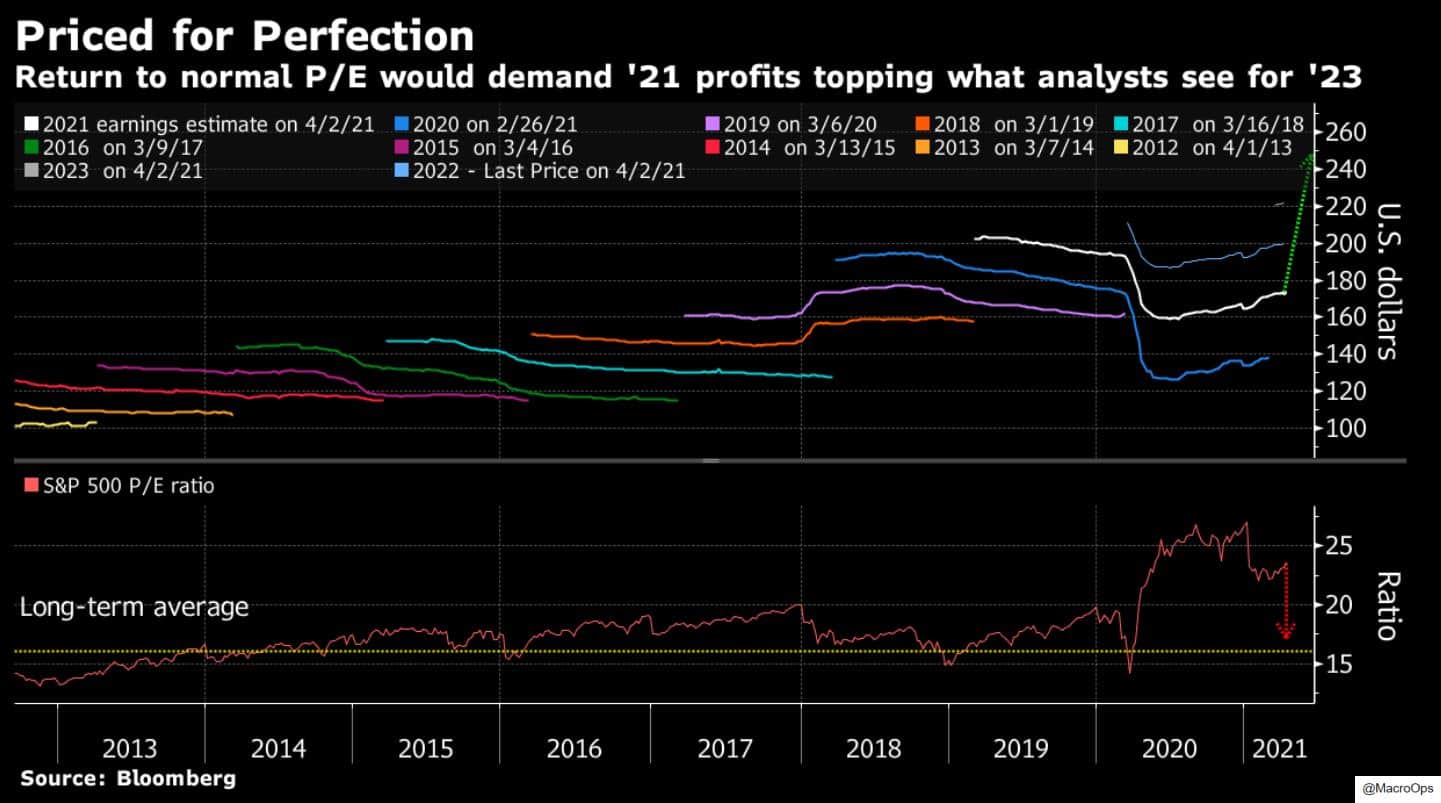

- Earnings season is upon us… Bloomberg notes the high bar that’s been set, writing “Based on existing analyst forecasts for earnings in all of 2021, the S&P 500 trades at almost 24 times estimates, among its highest valuations ever. To bring the multiple down to its long-term average of 16 times annual profits, companies in the gauge will have to make about 15% more than the equity researchers currently expect them to earn — in 2023.”

- Here are the most anticipated releases this week from Earnings Whispers.

- Ned Davis Research lays out the downside of when too much upside is priced in (h/t @modestproposal1 for the chart).

- Financials and tech have been two of the strongest sectors year-to-date, following energy which takes first spot. While energy names have benefited from a rerating of extremely bearish expectations to just mildly so, the other two sectors have been boosted by that Buyback Tailwind…

![]()

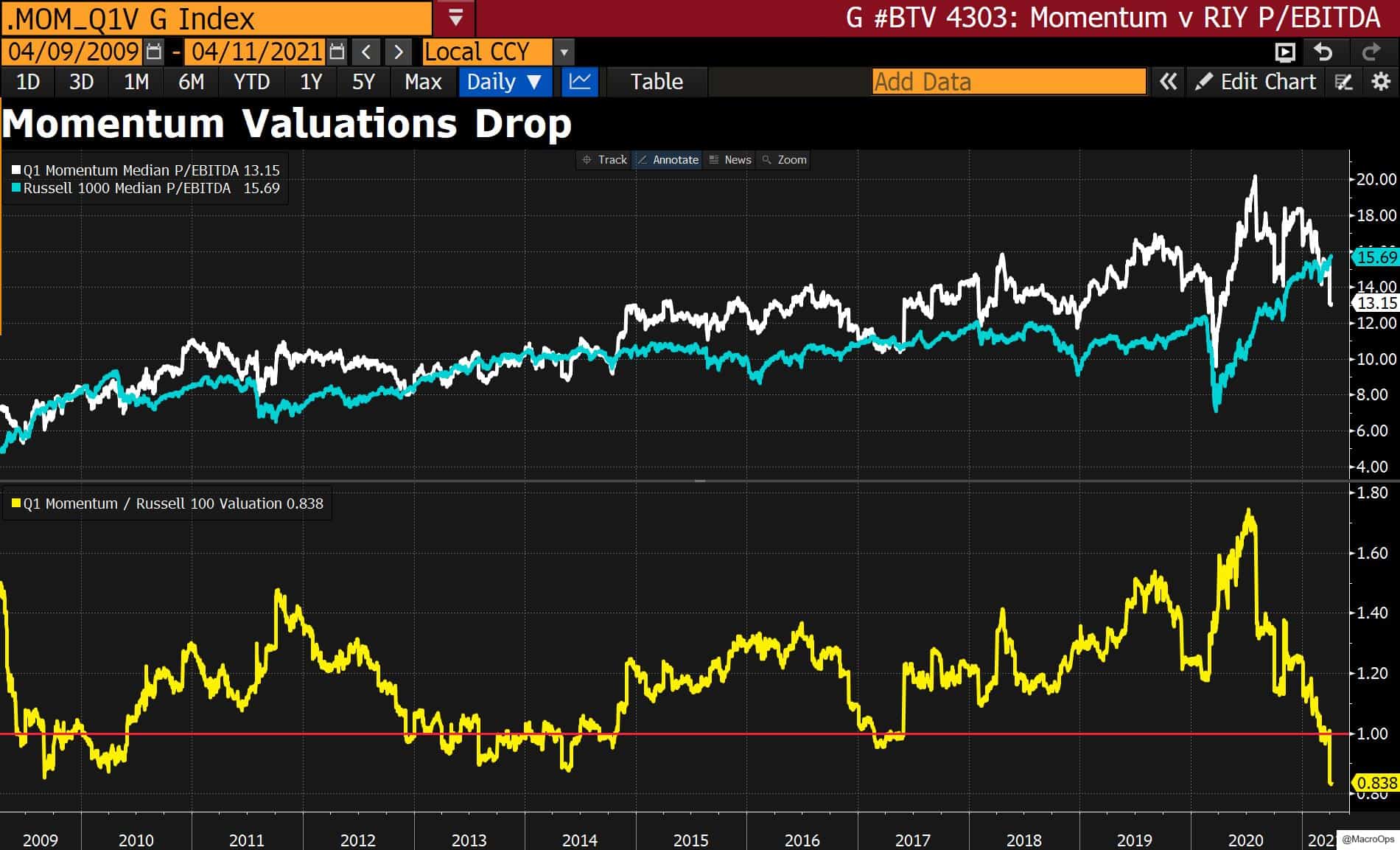

- More evidence supporting growth and momentum’s relative leadership in this Buy Climax.

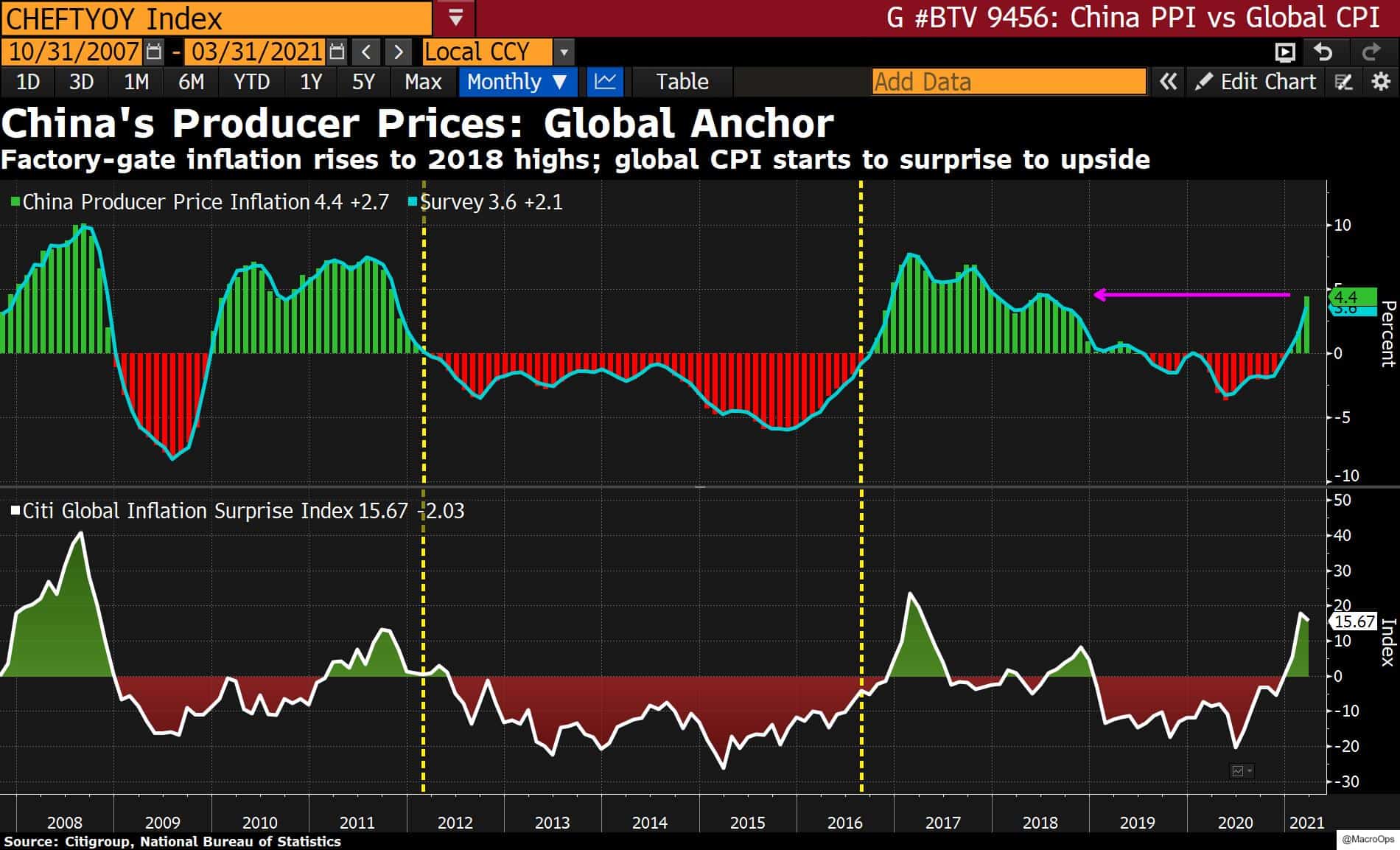

- China PPI is accelerating which tends to lead to positive inflationary surprises globally.

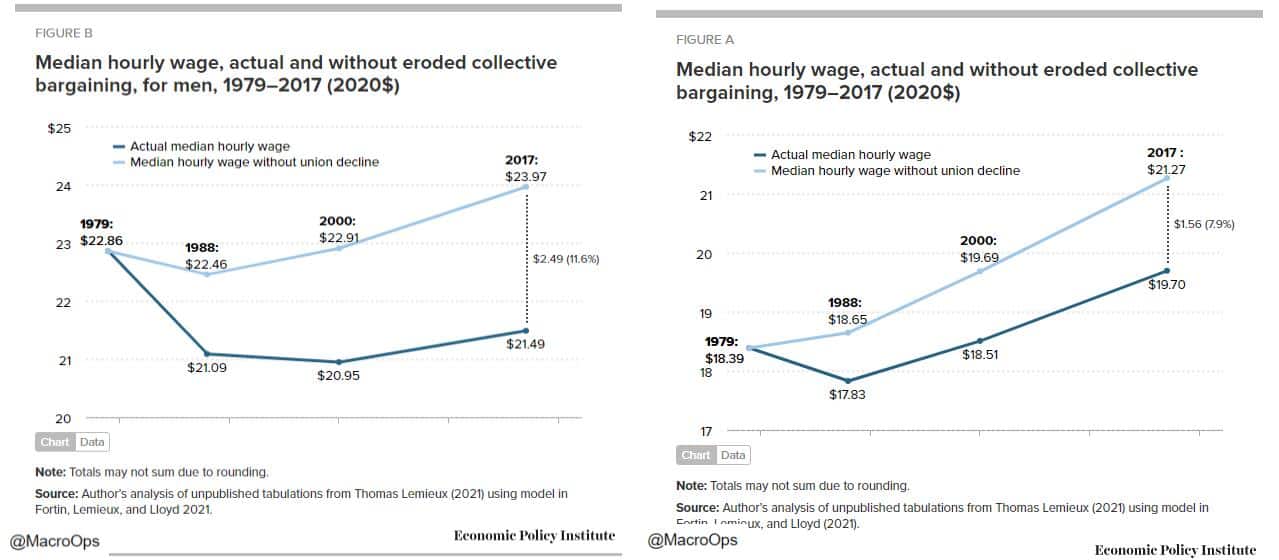

- Speaking of inflation, the Economic Policy Institute published a report last week exploring the relationship between Labor bargaining power and sticky inflation. The EPI writes:

“…the only factor more responsible for weak wage growth for the typical worker is the excessive unemployment perpetrated by central bank policymakers’ high interest rate policies and fiscal austerity. The share of workers covered by a collective bargaining agreement fell from 27.0% in 1979 to just 11.6% in 2019.This impact of eroded collective bargaining lowered the median hourly wage by $1.56 over the 1979–2017 period. Put another way, the median hourly wage was $19.70 in 2017 but would have been $21.27 had collective bargaining not declined (all in 2020 dollars).”

- The Buy Climax scenario we said was likely a few weeks ago is playing out to a T. How long it will last is anybody’s guess — buy climaxes always last longer than most expect — but sentiment is getting to a point where it can’t rise much further.

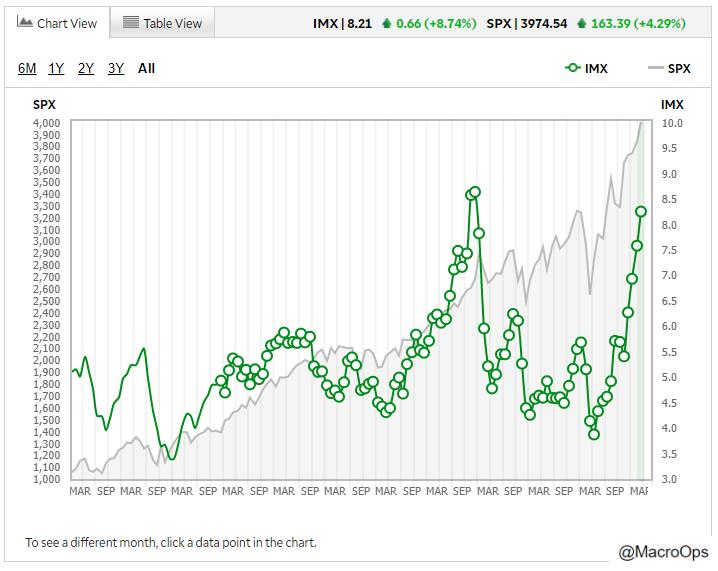

AAII Net is at its highest level since the Jan 18’ blow off top.

And TD Ameritrade’s IMX is at its highest level since then as well.

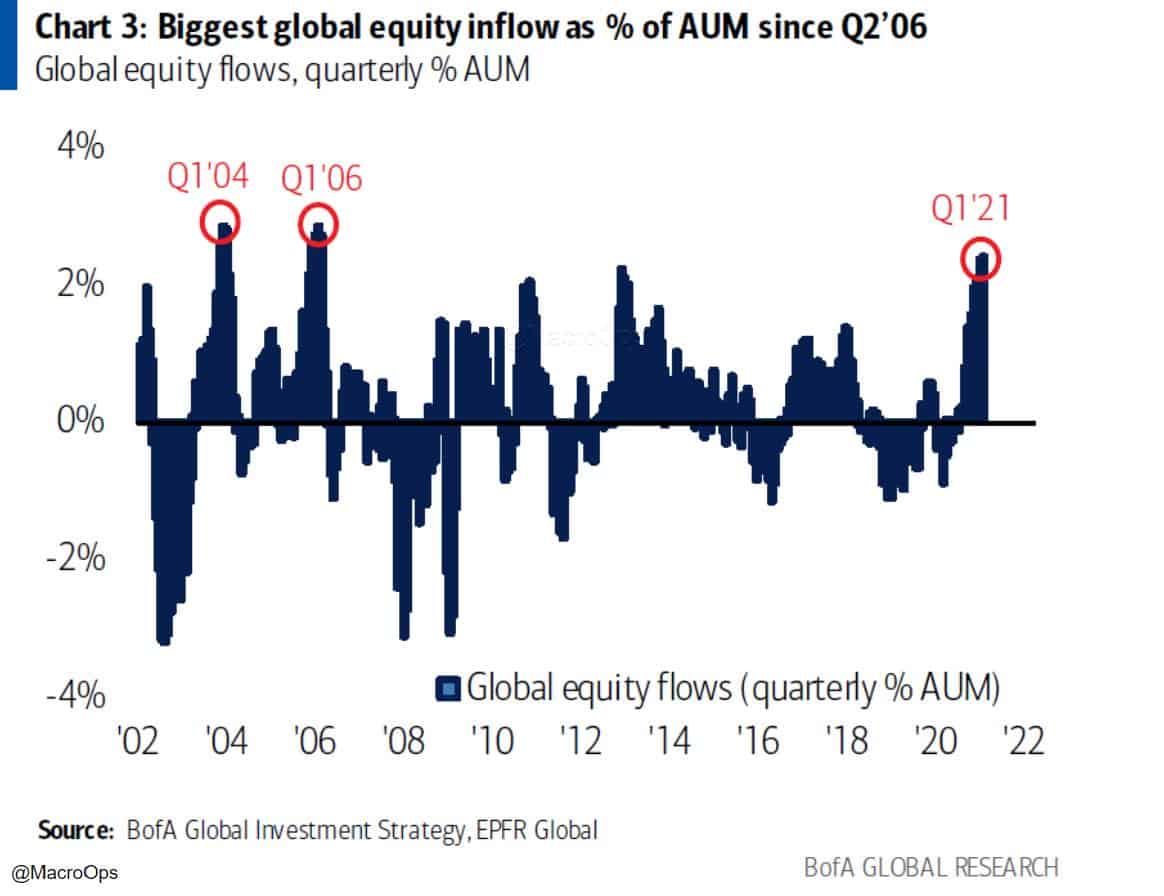

- BBG notes “Investors bought equities in record amounts in the first quarter of 2021, as a combination of generous stimulus and bets on economic recovery drove $372 billion into global stock funds… The first three months of the year saw the largest global equity inflows as a share of assets under management since 2006.”

- And wealthy BofA clients boosted their equity allocations to 63.6%, the highest level on record.

All signs suggest this Buy Climax will be followed by an extended — any likely painful — consolidation following this blow off top.

- This 40yr+ chart of lumber prices is something else…

- Precious metals are going to be the big outperformers in the second half of this year — you can go ahead and timestamp this.

I’m personally starting to slowly build positioning in miners and related plays. EXK, which I pitched back in December, continues to be one of my favorite silver miners. It’s climbed 37%ish since, but still has a long ways to go. The chart below is from back in December.

Stay safe out there and keep your head on a swivel.