When you develop a desire for trading, you must realize that the desire originates from the greed for profit and that it is only a feeling that has little to do with the possibility of making actual profits. Therefore, you need to identify and control the greed when it grows in you. Meticulous analysis of the possibility of making actual profit should be your priority. ~ “The God of Trading, Honma: The Creator of Japanese Candlestick Charts”

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at household’s high ownership levels in equities, before diving into what this means for future returns. We then discuss elevated risk metrics, the Buy Climax case, growths emergence over value, the bullish setup in semis, and some Ag-related news, plus more…

Let’s dive in.

***click charts to enlarge***

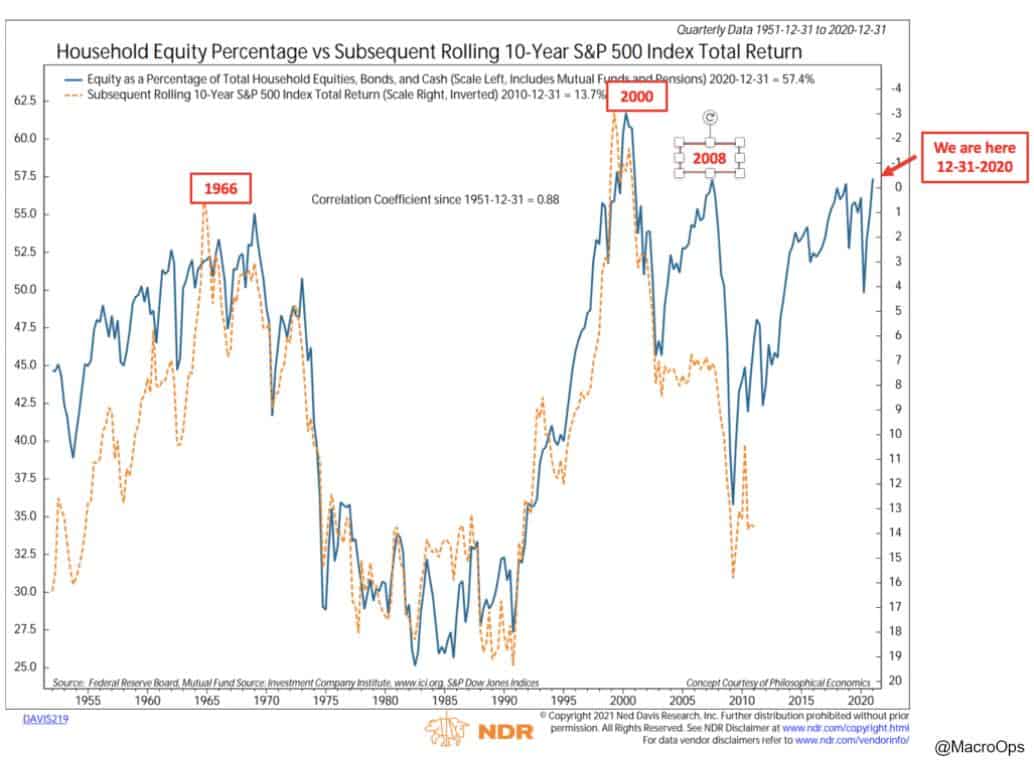

- I like to check in on household ownership of equities as a percentage of financial assets from time to time (it currently stands at 43.2%, just shy of the all-time high reached in 2000 of 44.6%).

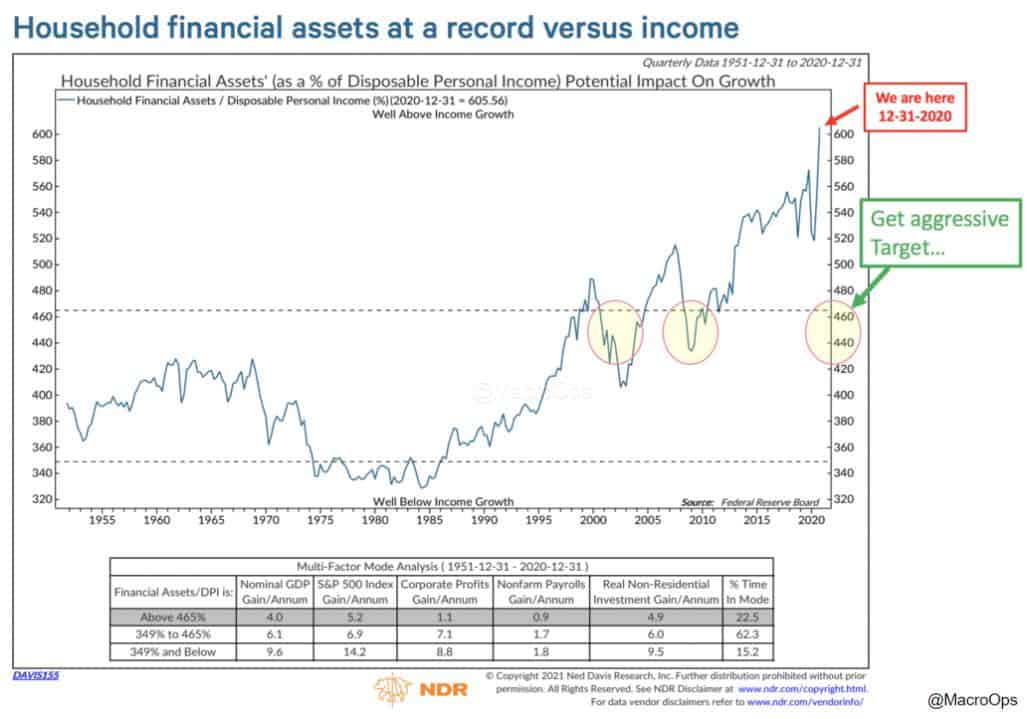

This chart from NDR via CMG Wealth gives another way of looking at things. Here is household financial assets versus income. It’s a little elevated.

- If equity ownership as a % of total financial assets continues to be a high signal guide for forward returns, then probabilities point to a -0.50% annualized market return over the next decade (NDR chart via CMG Wealth).

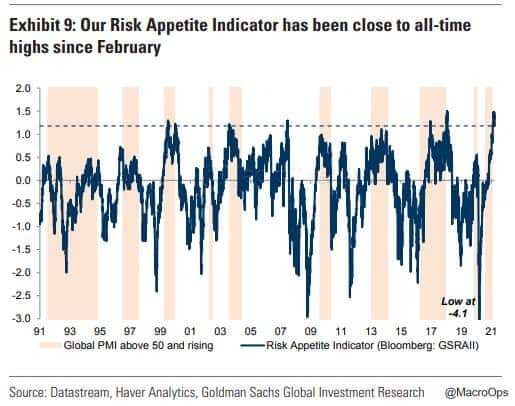

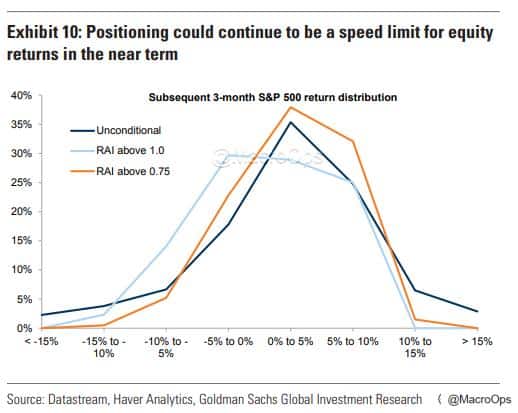

- Goldman Sachs Risk Appetite Indicator is close to an all-time high…

- From GS “high RAI levels means the likelihood of very strong S&P 500 returns (>10% over 3m) is usually lower. But the risk of very large equity drawdowns (>10%) is also usually lower, because there is likely a strong macro backdrop that has boosted risk appetite, similar to the COVID-19 recovery. Nevertheless, there is a more negative skew of returns and the probability of corrections increases.”

This fits in with our current base case. A Buy Climax over the next few weeks, maybe months even… followed by an extended period of sideways chop and volatility in US markets.

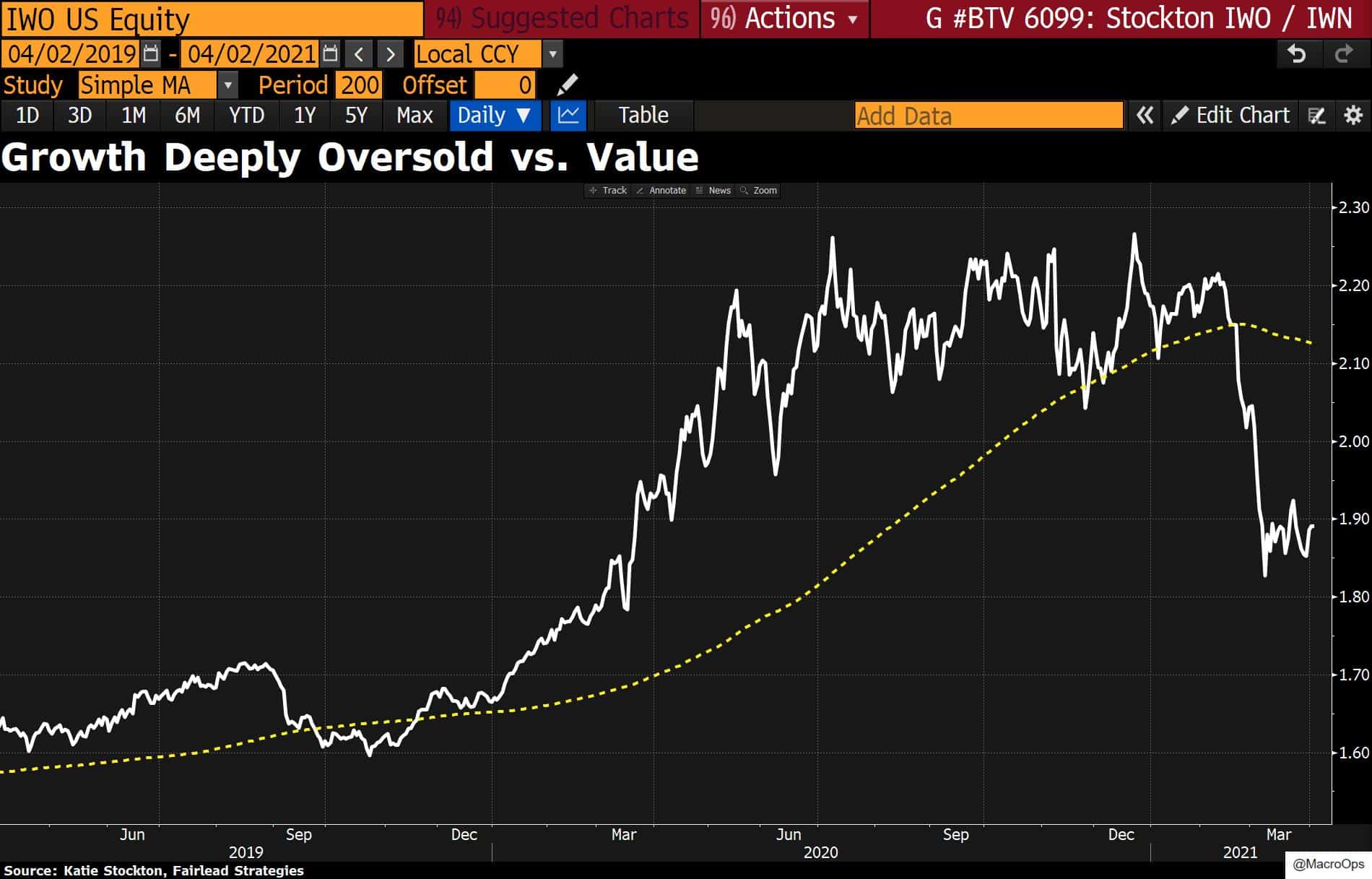

- I like the Qs here as growth is deeply oversold on a relative basis. This is likely their last hurrah before an extended period of underperformance (chart via Fairlead Strategies).

- Another bullish growth/tech chart via Fairlead Strategies, showing improving momentum in the Nasdaq.

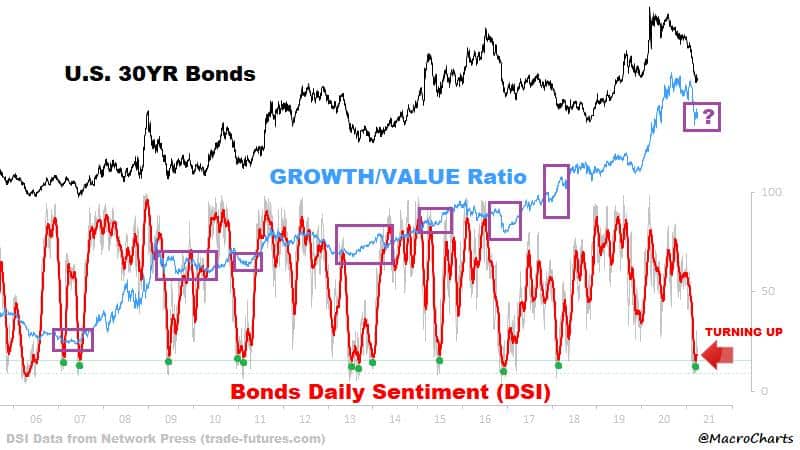

- @MacroCharts shared a number of great charts on the twitters last week. Here’s one showing the correlation between negative bond sentiment (as marked by a low DSI) and the follow-on returns in growth relative to value.

This makes sense as falling yields provide relief for more richly valued growth names.

- A couple of weeks ago I pointed out the extraordinary breadth in semis (link here). Here’s another one from @MacroCharts showing a big weekly price thrust in the SOX index. Prediction: the supercycle in computing power is going to become a mainstream narrative in the coming months.

- It’s hard to find a bearish-looking chart in the space. QRVO is one of many names breaking out from nice technicals…

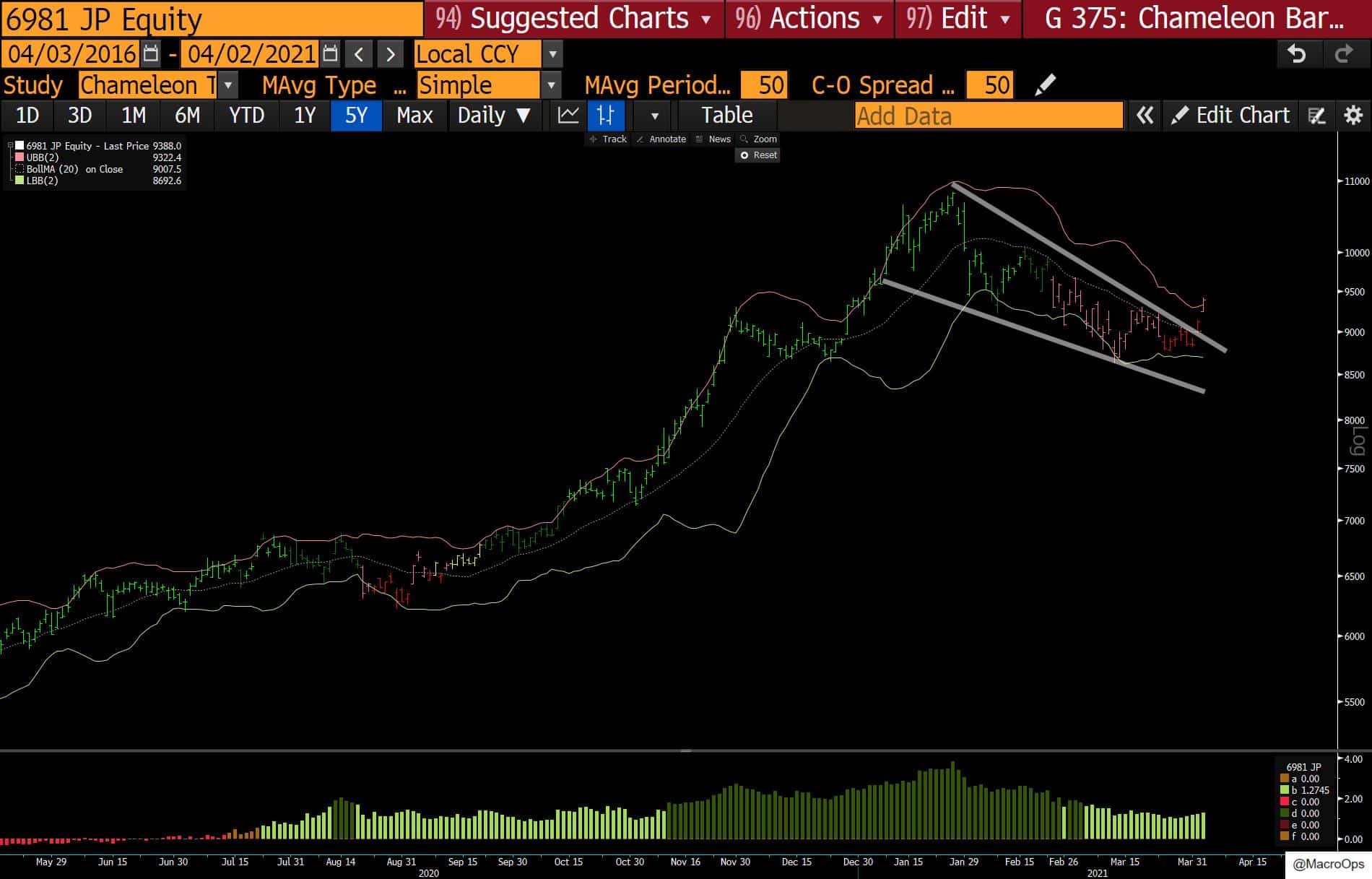

As well as the Japanese company, Murata Manufacturing. A stock we bought last year and took profits on before this recent pullback that’s giving another good entry point.

- Last month, I pointed out the impressive relative strength of Japanese financials, using Nomura (NMR) as an example. Well NMR was recently implicated in the Archego’s blow-off, apparently, the bank is on the hook for potentially $2bn in losses.

Its stock price has taken a big hit but its credit is mostly unfazed — especially when compared to the reaction seen in Credit Suisse, who also got caught up in the mess.

I’m keeping an eye on NMR and may consider putting on a starter position once its technicals firm up some.

- Wheat’s traditional premium over corn fell last week to its biggest discount since 1977 (h/t BBG). This is typically a bullish sign for both.

- We’re big Ag bulls at MO. I pitched the fertilizer company CVR Partners (UAN) in these pages back in early Jan. The stock is up nearly 200% since…

We currently hold a number of Ag-related names. A new one I’m starting to look into is Marrone Bio Innovations (MBII). It’s an AgBiotech that hails from my alma mater, UC Davis.

You have to do your DD on this company as its potential value lies all in the future… But, there may be something here… idk, we still have some work left to do.

Stay safe out there and keep your head on a swivel.