As always, hope you had a great week. I got to spend the weekend at Hilton Head Island, SC. Beaches weren’t crowded so social distancing was a breeze. In true deep value fashion, we snagged our Airbnb at a 75% discount rate to its historical rental price. I told you we eat, sleep and breathe this stuff!

Anyways, enough about my travels. More stocks.

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- Investing in Chapter 11 Stocks

- An Aswath Damodaran Update

- Bill Nygren on Investing in Crisis

- Mittleman Global Value Equity Q1 Update

Let’s get it!

—

May 20th, 2020

Tweet of The Week:

There are three types of sell side analysts pic.twitter.com/J2u2t9iHUs

— Stacy Rasgon (@Srasgon) May 17, 2020

__________________________________________________________________________

Investor Spotlight: Mittleman Global Equity Value

GIFs by tenor

GIFs by tenor

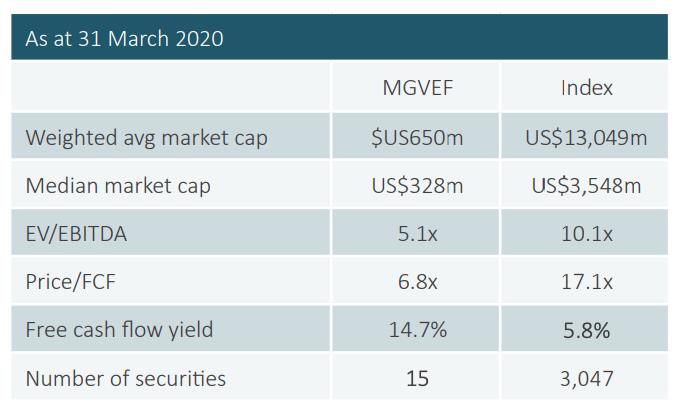

Mittleman Global Value Equity: -33.4% in Q1 2020

Mittleman Global Value equity lost over 30% in Q1. The investment company takes a global approach to investing in small/micro-cap companies.

Here’s their portfolio stats as of April 1:

The portfolio’s cheap … real cheap. 33% of their holdings are in the US, 18% in Canada and 21% in Hong Kong.

Let’s take a look at their top three holdings:

-

- Clear Media (100.HK)

- Aimia, Inc. (AIM.CA)

- Revlon (REV)

Clear Media (100.HK)

Business Description: Operates as an outdoor advertising company in the People’s Republic of China. It provides bus shelter advertising solutions. The company serves e-commerce, IT digital product, entertainment, beverage, food, realty, business/consumer service, realty, telecommunication, and education industries. As of December 31, 2018, it operated a bus shelter advertising network of approximately 54,000 panels covering 24 cities in Mainland China. – TIKR.com

What’s To Like:

-

- Durable business with NIMBYism qualities

- Strong insider ownership

- 30% Gross Profit margins

- 15% FCF Yield

What’s Not To Like:

-

- Going through low-ball takeover offer

- Chinese company

- Low-ball offer, if accepted, represents significant value destruction

Mittleman’s Take: “The overleveraged status of CCO, into the maelstrom of the COVID-19 crisis, apparently led them to accept a very low valuation, which puts minority shareholders at risk should enough take up the offer. MIM is optimistic that enough shareholders will reject the low-ball offer. MIM has taken advantage of the price appreciation however and sold a significant portion of the position to buy a couple of new positions and add to select existing holdings”

Chart Analysis

![]()

The sudden jump in stock price reflects the low-ball take-out bid. Should shareholders reject the offer we could see it trade back down on the news.

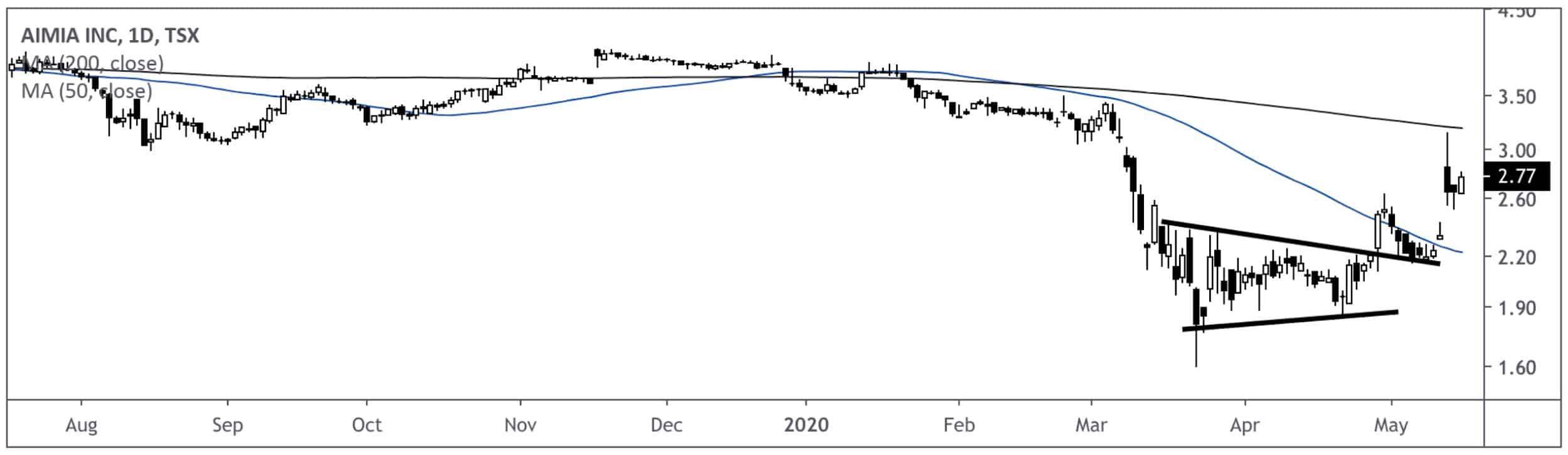

Aimia, Inc. (AIM.CA)

Business Description: Aimia Inc., together with its subsidiaries, engages in loyalty solution business in Canada, the United Kingdom, the United Arab Emirates, the United States, Australia, and others.It invests in Club Premier, a Mexican coalition loyalty program; and BIG Loyalty, AirAsia’s loyalty program. The company offers loyalty strategy, program design, implementation, campaign, analytics, and rewards fulfillment; and the Middle East loyalty solutions business, which includes the Air Miles Middle East coalition program, as well as Intelligent Shopper Solutions (ISS), Aimia’s international data analytics and insights services. – TIKR.com

What’s To Like:

-

- Crazy cheap based on NAV and net cash

- Decent business providing a needed service to airlines and customers

- Positive changes on the board

What’s Not To Like:

-

- Cash burn creates melting ice cube

- Long-standing distrust in management’s ability to unlock value

Mittleman’s Take: “Aimia also has C$700M in tax assets that MIM does not include in its NAV estimate of C$8.00 / US$5.75 per share, which is 3.8x the quarter-end price. Alas, the perverse illogic of market pricing at times, and yet what wondrous opportunities are produced by such sentimental extremes.”

AIM jumped almost 13% on April 29. The stock now sits at $2.77. This is still well beneath MIM’s estimate of fair value.

Chart Analysis

I missed this move when it broke out of its symmetrical triangle. Now I’m hoping for some sideways consolidation for another optimal reward/risk set-up.

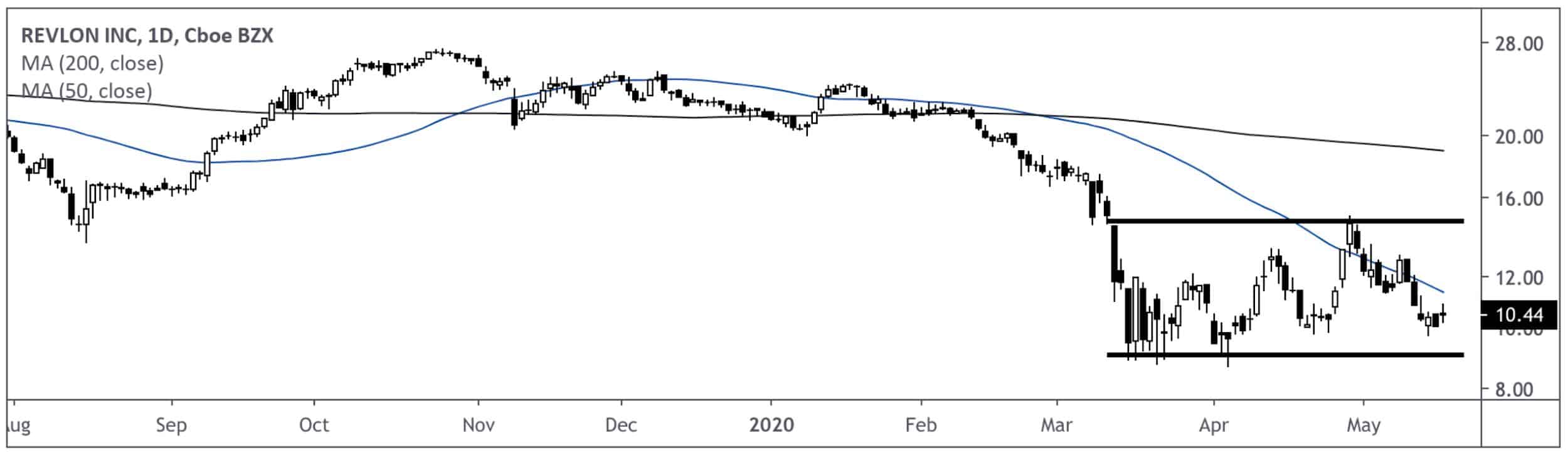

Revlon, Inc. (REV)

Business Description: Revlon, Inc., through its subsidiaries, develops, manufactures, markets, distributes, and sells beauty and personal care products worldwide. The company’s Relvon segment offers color cosmetics and beauty tools under the Revlon brand; and hair color under the Revlon ColorSilk and Revlon Professional brands. Its Elizabeth Arden segment markets, distributes and sells skin care products under the Elizabeth Arden Ceramide, Prevage, Eight Hour, SUPERSTART, Visible Difference, and Skin Illuminating brands; and fragrances under the Elizabeth Arden White Tea, Elizabeth Arden Red Door, Elizabeth Arden 5th Avenue, and Elizabeth Arden Green Tea brands. – TIKR.com

What’s To Like:

-

- 50% Gross Profit Margins

- 87% Insider Ownership

- Large Insider w/ Cash To Help Sustain Burn from COVID

- Improved terms on short-term debt

What’s Not To Like:

-

- Overleveraged at 16x Net Debt/EBITDA

- Growing Long-term net debt

- 20% Sales Hit due to COVID

Mittleman’s Take: “Revlon’s mass market positioning (except for the 20% of sales from prestige brand Elizabeth Arden) should play to the trade-down effect that tends to support mass market brands much better than prestige brands during recessions. Revlon will likely sell its hair colour business (#1 market share in mass market), its fragrance business or Elizabeth Arden for valuations high enough to facilitate substantial deleveraging of its balance sheet.”

Chart Analysis

REV’s range-bound between $16 and $9.50.

__________________________________________________________________________

Movers & Shakers: Bill Nygren & Aswath Damodaran

Bill Nygren and Aswath Damodaran are two heavy-hitters in the value investing world. This week we look at two of their latest publications. Let’s start with Bill.

Investing in Crisis with Bill Nygren

Value Investor Insight released their interview with Nygren on April 30. There’s a ton of knowledge bombs, so I encourage you to read the entire transcript.

Here’s some of my favorite snippets from the interview …

“Our early focus was to sort through all the companies whose share prices had fallen significantly to identify those that fell less on an enterprise-value basis and that were more in the eye of the storm.”

This is an interesting concept, and Nygren explains why they focus on enterprise value in the following paragraph:

“When share prices are indiscriminately cut in half, the company with net cash really has been much more heavily hit.”

Bill uses an example to illustrate this concept …

“A simple example: Say two stocks fall 50%, from $20 to $10. Let’s say one has $3 per share in net cash, so its EV has fallen from $17 per share to $7, meaning the market is valuing the business at 60% less than it did when the stock was at $20. The cash presumably was worth $3 before and still is, so the business is worth incrementally less than the fall in the stock price.”

The discussion then pivots towards their latest investment in Pinterest (PINS). I know, not the type of stock you’d expect in a traditional “value” portfolio.

But that’s why I love the guy.

Here’s his basic thesis on PINS:

“The company isn’t yet making money because it has incremental costs in preparing to be a much larger-scale enterprise than it currently is, and also because it is still in the early days of monetizing its platform. The priority to grow users – which now number more than 300 million on average each month, growing 15% a year – is higher than the priority to maximize advertising per user.”

This isn’t the first time we’ve seen PINS dropped in a value portfolio. Scott Miller’s Greenhaven Road initiated a position this past quarter.

Nygren finished the interview with a comment on lasting lessons from the COVID-19 equity collapse:

“We’re pretty good at looking past current events and what companies could be worth on a long-term basis. That doesn’t mean we’re better than anyone else at guessing how the virus evolves or when the economy returns to normal. We need to make sure our portfolios don’t depend on us being experts in areas where we are not.”

Aswath Damodaran: Re-examining The Value vs. Growth Debate

Damodaran’s latest Musings on Markets is loaded with discussions on global equities, valuations, gold, copper, etc. You name it, he’s covered it.

What we care about is his section on Value vs. Growth. I know, you can’t get enough of that debate.

Here’s my favorite bits …

-

- “Value investors believe that it is assets in place that markets get wrong, and that their best opportunities for finding “under valued” stocks is in mature companies with mispriced assets in place. Growth investors, on the other hand, assert that they are more likely to find mispricing in high growth companies, where the market is either missing or misestimating key elements of growth.”

- “It is quite clear that 2010-2019 looks very different from prior decades, as high PE and high PBV stocks outperformed low PE and low PBV stocks by substantial margins. The under performance of value has played out not only in the mutual fund business, with value funds lagging growth funds, but has also brought many legendary value investors down to earth.”

One major realization from this article was that low P/E stocks don’t always offer protection in downturns.

Check this out:

-

- “Note that it is the lowest PE stocks that have lost the most market capitalization (almost 25%) between February 14 and May 1, whereas the highest PE stocks have lost only 8.62%, and to add insult to injury, even money losing companies have done better than the lowest PE stocks.”

That’s nuts! Damodaran caps this argument perfectly, saying (emphasis mine), “If I had followed old-time value investing rules and had bought stocks with low PE ratios and high dividends in pre-COVID times, I would have lost far more than if I bought high PE stocks or stocks that trade at high multiples of book value, paying little or no dividends. The only fundamental that has worked in favor of value investors is avoiding companies with high leverage.”

__________________________________________________________________________

Whitepaper of The Week: Investing in Chapter 11 Situations

In honor of JC Penny (pour one out!) I found an interesting whitepaper on Chapter 11 investment situations. You can read the entire paper here. The authors (Yuanzhi Li and Zhaodong Zhong) review the trading, value and performance of Chapter 11 investments.

Let’s dive in.

Setting The Stage

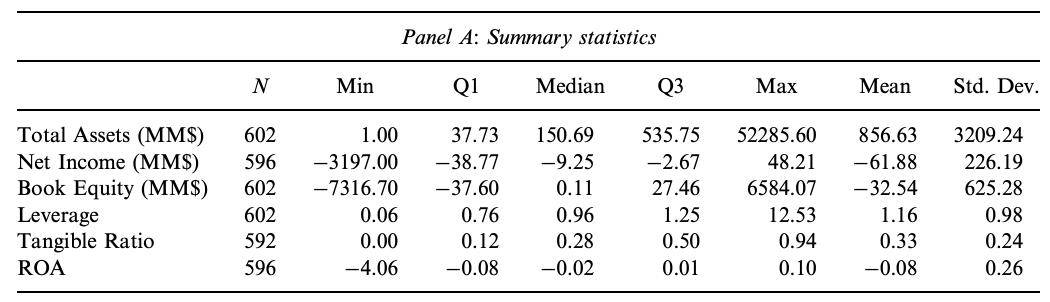

The authors looked at 602 total cases of Chapter 11 bankruptcy. Here’s the distribution of cases:

Here’s what the characteristics (metrics) of those 602 companies look like:

The average company in this study had $150M in net assets, lost around $9.5M in net income and generated -2% ROA.

What surprised me was the leverage ratio (total liabilities/total assets). It’s below 1.

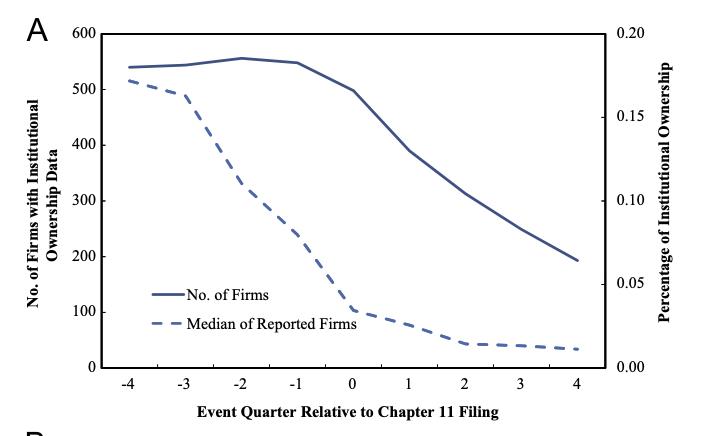

Trading Post-Chapter 11

Chapter 11 stocks resume trading activity after a brief decrease post-filing. The paper shows this in the graph below:

This begs the question — who’s doing the trading in these post-Chapter 11 situations? The answer: not institutions

Here’s the graph:

The Performance of Chapter 11 Stocks

Let’s get to what really matters … return statistics. The paper defines performance by Holding Period Return (HPR). The holding period = number of days from the first trading day after filing to the resolution date, or the first trading day after the resolution date if there is no trading on the resolution date.

MHPR = monthly holding period return.

Here’s the breakdown:

MHPR = -16%

Ouch!

Concluding Thoughts

What should you take away from this study? Investing in post-Chapter 11 stocks are hard and (on average) lead to negative returns.

But I view post-Chapter 11 through the SPAC lens. Sure things are garbage on a median basis — but that shouldn’t stop you from digging through the dumpster. You never know what you might find! __________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!