Hope you had a great week and weekend. Golf courses in MD finally opened up. When you haven’t hit a golf ball in 3 months, you don’t keep score. You see how many balls you lose. I only lost one ball. It was a good round.

Anyways, we’ve got three great letters for you this week from three of my favorite investment thinkers. But before we get there, I want to give a huge shout-out to Harris Kupperman of Praetorian Capital.

Kuppy came on the podcast last week and set a major record. We passed 1,000 listens in less than a day. And within three days, Kuppy’s episode has over 2K listens. I know, it’s peanuts compared to other larger podcasts. But we’re just getting started.

Thank you to every guest and listener — you make the show.

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- Tao Value Q1 Letter

- GreenWood Investors Q1 Letter

- Hayden Capital Q1 Letter

Vamanos!

—

May 13, 2020

Valuing Young Growth Companies: One of my favorite hobbies is reading Aswath Damodaran’s valuation white-papers. I know, exciting life I lead, right? My favorite Aswath paper (so far) is Valuing Young, Start-up and Growth Companies: Estimation Issues and Valuation Challenges.

I’m in the process of creating a long Twitter thread of my favorite bits of information from the paper. If you don’t have time to read all 67 pages, give me a follow on Twitter and I’ll give you the run-down!

Speaking of Twitter, I recently compiled all my favorite Mohnish Pabrai YouTube videos in one thread:

I’ve collected my favorite @MohnishPabrai lectures, talks, etc. from YouTube and put them in this thread.

Please add to this list if I’ve missed anything.

Also, Mohnish, if you’re out there. I’d love to have you on the podcast.

Start learning from the Dhando Master now …

— Brandon Beylo (@marketplunger1) May 9, 2020

__________________________________________________________________________

Investor Spotlight: Emerging Markets & Emerging Managers

GIFs by tenor

GIFs by tenor

Tao Value: -12.96% Q1 2020

Tao’s letters are great because they open me to a new world of equities: China. I’m like a kid that doesn’t want to learn to swim when looking at China. I see the other kids have fun, splashing around. But as soon as I dip my toes in, the pool turns to shark Luckin-infested waters.

Tao mentions numerous stocks, but we’re focusing on the following:

-

- China Meidong Auto (1268.HK)

- Atlassian (TEAM)

- Bilibili (BILI)

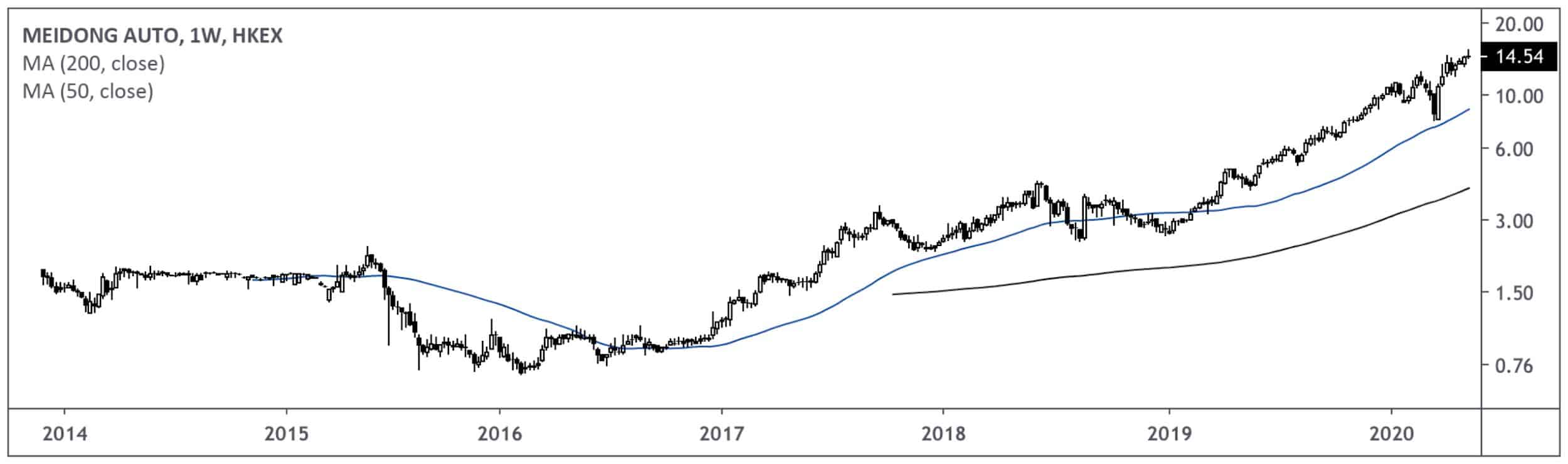

China Meidong Auto (1268.HK)

Business Description: The company is involved in the sale of new passenger cars and spare parts; and the provision of service and survey. It also provides after-sales services, such as auto registration, insurance, auto financing mortgage, auto parts, repair and replacement, sales and maintenance of automotive supplies, etc. In addition, the company engages in the trading of used vehicle and finance leasing activities. Its dealership stores cover various automobile brands comprising BMW, Lexus, Toyota, Hyundai, and Porsche. – TIKR.com

What’s To Like:

-

- 30%+ 5YR Revenue CAGR

- 76% 5YR EPS CAGR

- Strong balance sheet

- Reducing Inventory Churn/Payables Outstanding

What’s Not To Like:

-

- Chinese auto-dealership

- Specializes in luxury cars

- Increase in debt/liabilities as % of assets

- Approaching Tao’s estimate of fair value (21x normalized earnings)

What’s It Worth (Assuming 10% Discount Rate):

At the current price, Mr. Market expects 33B CNY in 2024 revenue, 1.99B CNY in EBITDA (6% margin) and a 10x EBITDA exit multiple.

Here’s what Tao has to say about valuation (emphasis mine): “On valuation though, I see the price approaching fully valued. It now trades at 25 X trailing EPS, and around 17x forward earning per share.”

That said, Meidong is growing over 30% p.a in top-line revenue while trading at 21x normalized earnings. It may not be cheap, but it doesn’t sound expensive at that growth rate.

Also, a 10x exit EBITDA multiple is quite the compression from its current 16x valuation. If multiples don’t shrink, and Meidong exits at its current multiple, shareholder equity increases to 22B CNY (21.54 HKD/share).

Stock Chart

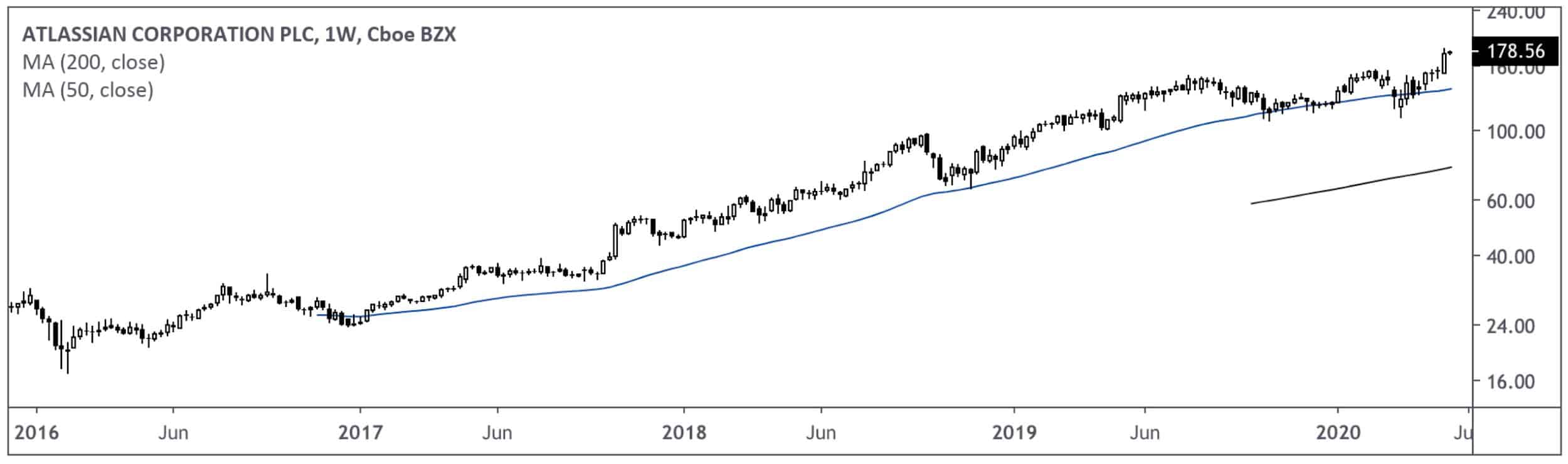

Atlassian (TEAM)

Business Description: It provides project tracking, content creation and sharing, and service management products. The company’s products include JIRA, a workflow management system that enables teams to plan, organize, track, and manage their work and projects; Confluence, a content collaboration platform that is used to create, share, organize, and discuss projects; and Trello, a collaboration and organization product, which captures and adds structure to fluid fast-forming work for teams. – TIKR.com

What’s To Like:

-

- 40%+ 5YR Revenue CAGR

- Net cash on balance sheet ($859M)

- 83% Gross Margins

- FCF Positive

- Negative Working Capital

What’s Not To Like:

-

- Optically Expensive

- Trading Near All-Time Highs

- High stock-based compensation

- Increase in Days Sales Outstanding from 10 days to 21 days

What’s It Worth:

The company’s estimated 27% EBITDA margins by the end of this year. If we assume their 30% revenue growth is correct, that gives us $434M in EBITDA by 2020, $660+ in Cash from Ops and $600M in free cash flow.

That’s great. Unfortunately Mr. Market’s priced that already. At the current price, Mr. Market’s expecting $3.3B in 2024 revenues and over $1B in EBITDA on 30% margins. Is that possible? Of course. But TEAM’s trading at 28x revenues. I would need a serious drop in price to get interested in this name. And I hope it does drop.

It’s a great business that generates loads of free cash flow.

Chart Analysis

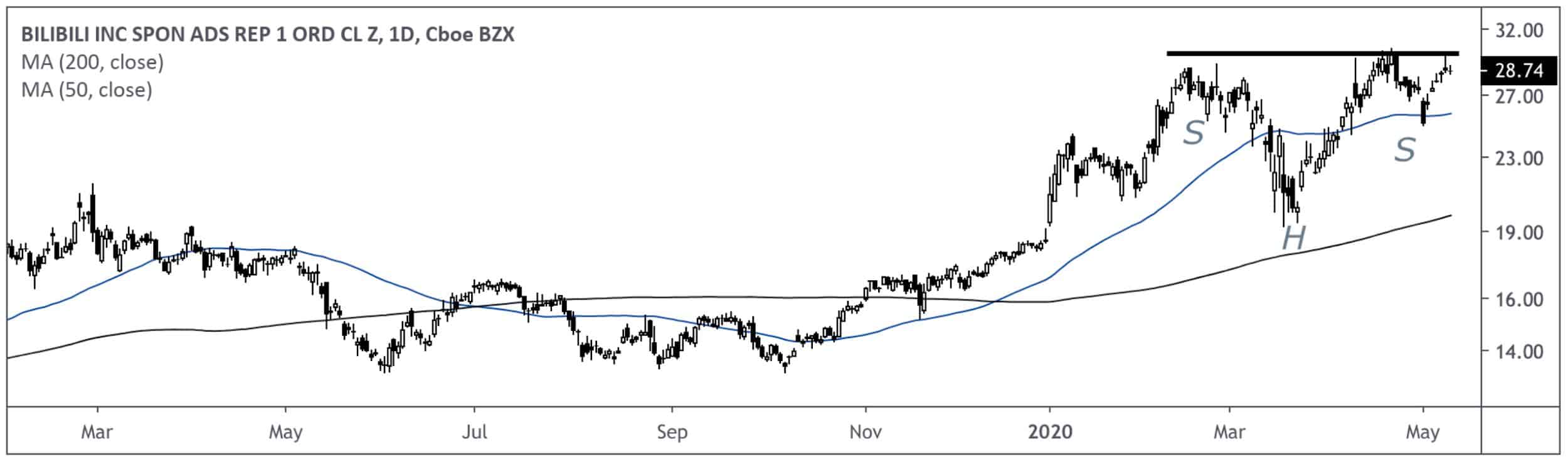

Bilibili (BILI)

Business Description: Bilibili Inc. provides online entertainment services for the young generations in the People’s Republic of China. It offers a platform that covers a range of genres and media formats, including videos, live broadcasting, and mobile games. – TIKR.com

Tao’s Take: “I believe BILI has built a moat around its mid-form PUGC platform. It now has 130 million engaging monthly active users, and wide range type of content. The network effect of attracting highquality content creators is evident, as it organically expands user base to older millennials (in their 30s) who has no ACG-related hobby.”

What’s It Worth (emphasis mine): “I estimated BILI’s game business could be worth about $3b on a 15x forward earning, which, at our cost basis, implies $2.8b for the rest operating businesses, or $22 market cap for each MAU. This is very cheap considering such a business should be able to easily monetize at $10/user (using either opportunity-cost-based survey or Chinese video/streaming/social media peers) from current 5 mere $3.7/user when they see appropriate. A reference point is that YouTube currently monetizes at $8/user globally, which is also under-done in my opinion. So, we paid 2.2X “fair” revenue for a YouTube of China, where I think a fair multiple should be between 5 to 10 times (depending how much growth you believe is still left).”

Chart Analysis: Potential Inverse Head & Shoulders

_________________

GreenWood Investors: -22% to -25% Q1 2020

Steven Wood is one of my favorite investors in the game. I love the way he thinks about ideas, situations and portfolio construction. Steven, if you’re out there — I’d love to have you on the podcast! Let’s make it happen!

Wood returned -25.60% during Q1. You can read his letter here.

Let’s review some of the stocks Steven mentioned:

-

- Correios de Portugal (CTT)

- Peloton (PTON)

Correios de Portugal (CTT)

Business Description: Correios De Portugal, S.A., together with its subsidiaries, provides postal and financial services worldwide. The company operates through Mail, Express & Parcels, Financial Services, and Banco CTT segments. It offers addressed mail, transactional mail, international inbound and outbound mail, and advertising mail distribution related services; CTT Logística, a platform for the creation of product catalogue, storage, order preparation, and distribution to the final consumer which allows customers to focus on the development and sale of their products; banking services; courier; transport solutions; payment network management services through Payshop; and documental services. – TIKR.com

Steven’s Take: “The company’s ubiquitous network that touches nearly every house and business almost every day is a fantastic delivery mechanism for the clear bull market in parcels, particularly e-commerce-driven parcels. Express networks are not properly set up for the last mile outside of highly urban areas. That’s why postal companies largely win the last mile of e-commerce. It’s a business that’s somewhat similar to a cement company, local market share matters heavily. As we all learned in geometry, when a truck’s delivery radius shrinks by half, as its market share doubles, the total area driven is reduced by ~75%.”

“Just a few years ago the company launched its own bank, which we estimate has taken almost half of all new accounts in the country since being opened. It has the highest customer satisfaction, and with a labor and physical footprint around one tenth of its competitors, it will have a permanent cost advantage versus peers.”

What’s It Worth:

Steven’s Take: “combined with the bank, and even if we take a major haircut to the bank’s GreenWood Investors LLC www.gwinvestors.com 5 value, the stock with just over a €300 million market cap today and a €32 million net cash position, means the company’s current enterprise value is deeply negative. So investors today are getting paid to take a core business which before the coronavirus, was on track to hit over €90 million in EBITDA in 2020, even after the new lease expenses and banking income are removed.”

We can cross-reference Steven’s valuation with our own, simple 5YR DCF model. Let’s make the following assumptions:

We’re also assuming a 10% discount rate and 0% perpetuity growth.

That gets us around $436M in EV ($197M from PV cash flows + $240M in terminal value). Add back our cash + investments and subtracting debt gets us another $540M in equity value for a total shareholder value of $976M ($6.50/share).

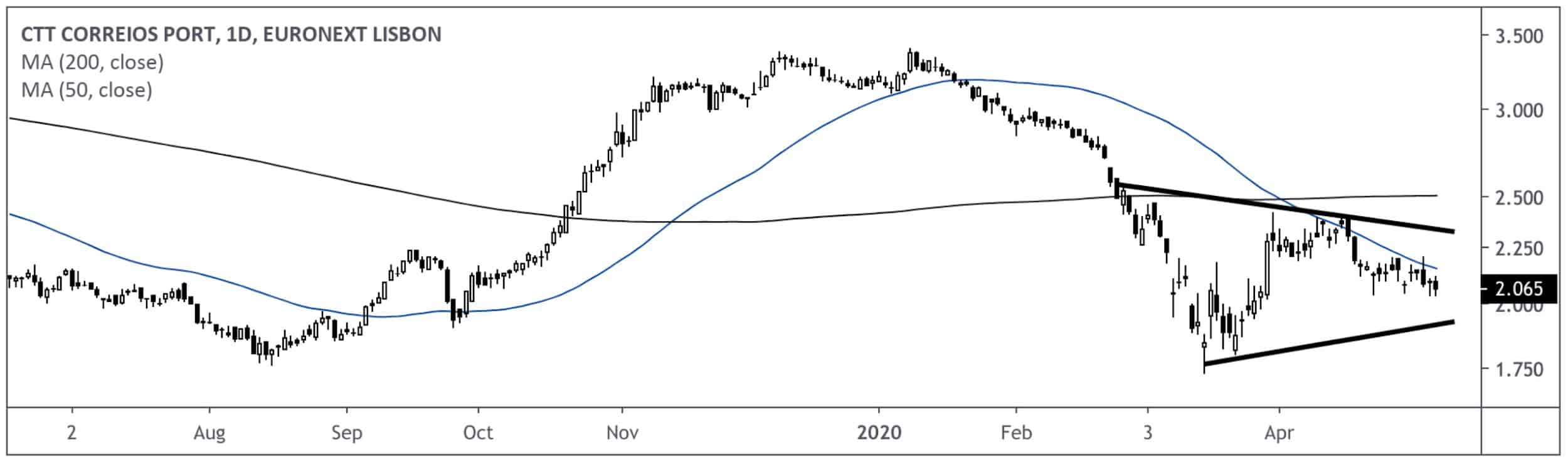

Chart Analysis

CTT remains in a clear downtrend and is forming a large symmetrical triangle. Look for a breakout above the 50MA and the upper resistance level to confirm the trend reversal.

Peloton (PTON)

Business Description: Peloton Interactive, Inc. provides interactive fitness products in North America. It offers connected fitness products, such as the Peloton Bike and the Peloton Tread, which include touchscreen that streams live and on-demand classes. The company also provides connected fitness subscriptions for multiple household users, and access to all live and on-demand classes, as well as Peloton Digital app for connected fitness subscribers to provide access to its classes. – TIKR.com

Steven’s Take: “It sells its stationary bikes and treadmills for about 10x the cheapest competitive offerings, yet it still manages to save its 2.6 million subscribers significant sums of cash every month. Because the value of Peloton lies in the millions of hours of content, as well as live exercise classes, the monthly subscription fee of $39 is dwarfed by the monthly bills of boutique fitness studio goers, which number over 30 million in the United States, and who pay over $30 per class for their endorphin rush.”

What’s It Worth:

Honestly, I don’t know what this thing could be worth in five years. We can use a revenue multiple since they don’t generate earnings. But attaching a 4x sales multiple on 2024 estimated revenue of $5.5B gets us a 30x exit EBITDA multiple.

Maybe PTON is worth 30x EBITDA in five years. But they face stiff competition from Apple’s fitness app and Soul Cycle’s new bike.

Chart Analysis: Inverse Head & Shoulders Breakout

_________________

Hayden Capital: +4.10% Q1 2020

Fred Liu, CFA runs Hayden Capital. He invests primarily in Asia/North America. As of Q1 end, he had 56% of his fund in Asian equities.

Liu mentions two stocks in his portfolio update:

-

- Interactive Brokers (IBKR) — sold

- Carvana (CVNA) — owns

Interactive Brokers (IBKR)

Why Liu Sold: “In the last year, Interactive has faced several industry-wide headwinds that hindered some of these positive developments.”

What were these developments? Two things:

1. Low net interest margins

Fred’s Take: “For example, net interest margins have declined 15% from a peak of ~1.7% a year ago, to most recently ~1.45%. This means even as accounts have grown, Interactive will make a less money per account, going forward.”

2. Zero commissions

Fred’s Take: “Industry-wide commissions have also been under pressure, as many retail-focused competitors started offering $0 trading commissions last fall. Interactive was one of the original low-price leaders, and was also one of the first to initiate the $0 commission price war via its new IBKR Lite platform, once it was clear the industry would inevitably move in this direction.”

Will the company do well over the next five-to-ten years? Yes. As a user of their product, I hope so!

But they trade around 28x normalized earnings in a low net interest margin world and zero commissions. Like Liu, I believe most of the marginal retail accounts will flow to other shops like Charles Schwab (SCHW). The UI is a bit better and the customer service is top notch.

Plus, the stock remains in a well-defined downtrend.

Chart Analysis

Carvana, Co. (CVNA)

Business Description: CVNA operates an e-commerce platform for buying and selling used cars in the United States. Its platform allows customers to research and identify a vehicle; inspect it using the company’s proprietary 360-degree vehicle imaging technology; obtain financing and warranty coverage; purchase the vehicle; and schedule delivery or pick-up from their desktop or mobile devices. – TIKR.com

Fred’s Take: “Carvana seems to be following a similar playbook. Similar to how Amazon educated the consumer and changed online shopping habits with its own 1P business and Amazon Prime, Carvana is doing the same with its marketing and hassle-free experience. Once they proved the market with their own inventory and built the trust, traffic, and infrastructure, Amazon eventually opened up the platform to 3rd Party sellers and provided them with the tools to succeed.”

What’s It Worth:

CVNA currently trades at 1.5x EV/Sales. This seems cheap given their 100%+ 5YR Revenue CAGR. The company also sees a path towards EBITDA positive by 2023. Let’s use the following assumptions:

Even at modest revenue growth, CVNA reaches over $13B in revenue by 2024. If we keep our 2x sales multiple we get $26B in EV (vs. $8.1B today). That’s over 100% upside assuming no revenue multiple expansion and roughly 30% 5YR revenue growth from here.

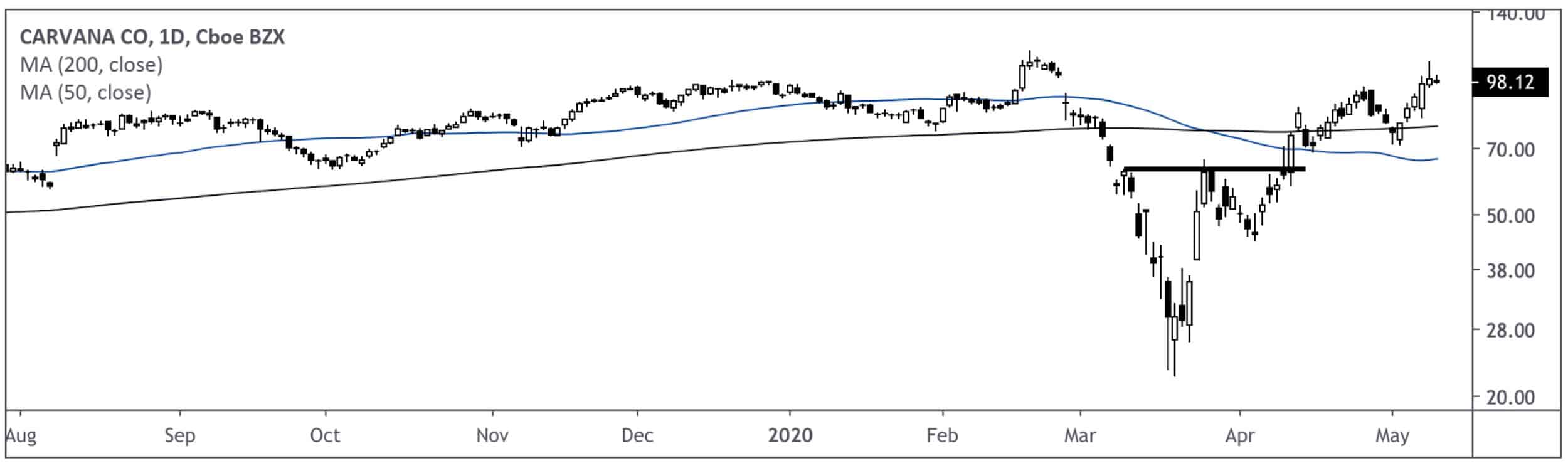

Chart Analysis

The stock remains firmly in an uptrend (above 50MA and 200MA).

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!