Hope your week is off to a great start! We’ve got a lot to cover this week. But before we do, I want to briefly discuss the Macro Ops Collective.

The Collective is our premium service offering. It’s unlike any other investing resource on the market. We’re a group of people dedicated to the craft of investing, trading and getting smarter every day. As iron sharpens iron, so one investor sharpens another.

As a Collective member, you’ll gain access to this growing group of traders via a private Slack channel, as well as institutional-quality investment research.

You’ll receive real-time trade alerts, weekly stock ideas from the most under-followed corners of the market and invaluable briefs on market trends.

If any of this sounds interesting to you, click here to learn more.

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- Genetic Defects in Active Investors

- Sports Investing in a Post-COVID World

- The Anatomy of Stocks That Go Up

- Li Lu Speech at Columbia University

I love curating this content for you guys. Let’s dive in!

—

July 1st, 2020

Chart Of The Week: After taking 2/3rds profit on our PTON position (see last week’s Value Hive), we’re back this week with a new short trade. This chart was featured in a previous premium Breakout Alerts report.

I got short around $100.52. I’m expecting a pullback towards the 200MA before another leg down (or if I’m wrong, a reversal above the 200MA).

I’m seeing a lot more short set-ups. You can find one of them here.

__________________________________________________________________________

Investor Spotlight: Do Active Managers Have A Genetic Defect?

GIFs by tenor

GIFs by tenor

Institutional Investor published an article on a “genetic defect” found amongst active fund managers. This defect wasn’t underperformance, nor was it some sector-specific bias.

It was over-diversification.

The article begins by saying (emphasis mine), “Research has shown that active managers produce persistent excess returns on their best ideas — but they squander these returns by relying on overly diversified portfolios.”

This isn’t breaking news by any stretch of the imagination. So why is it in the news now?

Finance veteran Tim Mullaney developed a new RIA designed to eliminate this defect.

Killing “Beta Anchors”

Mullaney’s project (Melius) isn’t groundbreaking. Take only the best ideas from multiple portfolio managers and remove each manager’s diversification efforts. The logic being each manager’s combined best ideas provides enough diversification while removing the beta anchors, or stocks added to reduce risk (but also reduce return).

Melius relies on ensemble methods to capture this alpha. Ensemble methods take in multiple predictive models which (hopefully) spit out a more predictive model. We see this idea in Michael Mauboussin’s Wisdom of Crowds paper.

The Real Reason: Career Risk

Managers over-diversify to protect themselves from career risk (getting fired). This makes sense. The incentive structure of most money managers isn’t to out-perform an index. It’s to keep their job.

Inevitably this leads to closet-indexing, or managers constructing portfolios similar to the S&P 500. The article explains the phenomenon well (emphasis mine):

“Take the Janus 20 fund,” he said. “It did well for a while, but when that manager’s approach goes out of style, even if short term, what happens? The investors gets hurt, the consultant gets embarrassed, and the manager gets fired. So that’s why you don’t see highly concentrated portfolios.”

Have Your Cake & Eat It Too

Mullaney wants to have his cake and eat it too. Combining the top ideas from multiple managers has worked in the short-term (as the article notes). But what about long-term performance? This story reminds me of the Charlie Munger anecdote on the “best ideas portfolio”. Here’s Warren’s partner on the endeavor (emphasis mine):

“We’ll get the best ideas from our best people and we’ll make a portfolio just of our best ideas from our best people. Nothing could be more plausible. They’ve done it three times and it’s failed every time. Now, how would you predict that?

Well I can predict it because I know psychology. When you pound out an idea as a good idea, you’re pounding it in. So by asking people for their best ideas they were getting the stuff that people had most pounded in, so they believed. So of course it didn’t work. And they stopped doing it because it didn’t work. They didn’t know why it didn’t work because they hadn’t read the psychology books, but they knew it didn’t work so they stopped. And it’s so plausible.”

__________________________________________________________________________

Movers & Shakers: The Shake-up In The Sports World (An Investor’s Guide)

GIFs by tenor

GIFs by tenor

Andrew Walker is back with Part 6 (six!!) of his Yet Another guide to media stocks. This week he focuses on team sports investing and the changing landscape post-COVID.

If you’re looking for Andrew’s favorite two sports team stocks, look no further than:

-

- Madison Square Garden Sport (MSGS): Owns the Knicks & Rangers and trades for <$4B EV.

- Liberty Media Corporation (BATRA): Owns the Atlanta Braves + some real estate and trades for roughly $1B EV.

According to Andrew, the above valuations are massive discounts to what a private buyer should pay (emphasis mine):

“Those are mammoth discounts to the private market value of the sports teams underlying those assets; the Knicks alone would likely go for ~$5B if they were put for sale (or more than MSGS’s entire enterprise value, implying you get the Rangers thrown in for more than free!), and I would guess the Braves would be close to $2B in a sale (implying you get the very valuable real estate around the Braves’ stadium plus a few other goodies for more than free).”

COVID Clouds on The Horizon

Today’s market prices are cheap. But how cheap are they in a post-COVID world? Andrew does a great job answering this question (emphasis mine):

“The impacts of Covid on sports teams are going to be felt for decades to come, and I would not be at all surprised if Covid creates some permanent impairment in sports team values. Probably not enough impairment to justify close to today’s discount, but if you asked me if you offered me the exact same sports team at $2B pre-Covid or $1.5B post-Covid, I would almost certainly prefer to invest at the higher price in the pre-Covid world.”

What are these long-term effects Andrew’s referencing? He mentions a few:

1. Acceleration of Cord-Cutting

Andrew’s Take: “So when Corona shut down every sports league, it created a really weird cable TV offering: cable TV was effectively an overpriced sports bundle that no longer had sports. The results were pretty predictable: cord cutting accelerated.”

2. Increased RSN Blackouts

Andrew’s Take: “If I was a cable company, I would absolutely be looking to blackout the RSN. Why am I going to be given them $5/sub/month when they aren’t providing a product? Sure, the RSN could offer to take no or seriously reduced fees until baseball returns…. but, again, if I’m a cable distributor, I’m looking to tighten the screws on the RSN right now. If I blackout an RSN during a lockout, basically no one will care. But the RSN will suffer enormously.”

3. Decrease in Revenues, Salaries & Salary Caps

Andrew’s Take: “Lebron James is already making more per year in endorsements than he is in NBA salary; if the league tries to cut salaries 20% across the board, could James and a few other super stars band up and create their own league (Kyrie Irving already floated the idea, though Irving can be a little wacky….)? In normal times, I’d consider that laughable. But with the whole world on pause, a fresh league could have some advantages: there are plenty of suboptimal things about the NBA that could be improved with fresh thinking, and obviously the players could cut out the owners (who don’t really provide much) and keep the equity capital for themselves.”

The Rise of eSports

Andrew must’ve read last month’s Macro Ops Consilience Report. We dove deep into the rise of eSports and its long-term runway.

He mentions an interesting point about the second-order effects of COVID in sports: generational fans. In short, Andrew argues that kids (the next generation of potential fans) will opt for other forms of sport and entertainment (primarily esports). Why? Here’s Andrew’s answer (emphasis mine):

“A big part of being a fan as a kid is going to a stadium and experiencing a game. Kids aren’t going to get that for the next few years. Sure, they can watch the game on TV…. but they could also just go play fortnite. I would bet a significant number of kids chose fortnite over watching games on TV, and that can break the lifelong fandom bond.”

__________________________________________________________________________

Newsletter Of The Week: The Anatomy of Stocks Going Up

GIFs by tenor

GIFs by tenor

Dave Portnoy taught us stocks only go up. Fair enough. But why do they go up? It’s a trivial question at face value. But think about it. What really makes a stock price rise? Is it macro liquidity? What about margin expansion?

According to Dubra Stocks research findings, only two things mattered:

-

- Revenue growth

- Earnings growth

That’s it. While helpful, those two things aren’t useful to us as investors. We already know that.

Dubra dove deeper into these Stocks That Go Up (STGU) to determine what made them rise in addition to revenue and earnings growth.

Five Groups of Stocks That Go Up

Dubra broke these STGU into five groups:

1. The Early Innovators: “Exceptionally high revenue growth companies that generally run at lower margin. These companies are growing at all costs.”

My take: Early stage companies at the beginning of their growth curve. They have no earnings, generate massive losses. They only care about growth.

2. Maturing Innovators: “Very high margin businesses that grow somewhat slower than The Early Stage Innovators.”

My take: Companies continue to grow rapidly but are starting to lose less money, potentially making minimal earnings.

3. Mature High Moat: “Moderate revenue growth and strong margins. Far higher margins than The Early Stage Innovators but lower margin than the Maturing Innovators.”

My take: Companies now make consistently high profits and are reinvesting less of their cash-flow back into the business (R&D, etc.) and using it to pay dividends, raise cash balances or buyback stock.

4. Defensible & Predictable: “Stocks with relatively low revenue growth and margins, but have strong moats and competitive advantages (regulated oligopolies, etc).”

My take: This is your run-of-the-Dempster-mill Buffett company. Massive, strong moat and durable earnings power.

5. The Survivors: “This is a group that is otherwise unremarkable in terms of revenue growth and margins whose returns are predominantly the result of surviving major periods of uncertainty in the markets.”

My take: Lackluster group with no real place in the study. Goodwill, in other words.

Invert, Always Invert

We’re closer to a working formula for finding STGU. One last step, invert.

Dubra inverts his question and asks, “What are characteristics of stocks that go down (STGD)?”

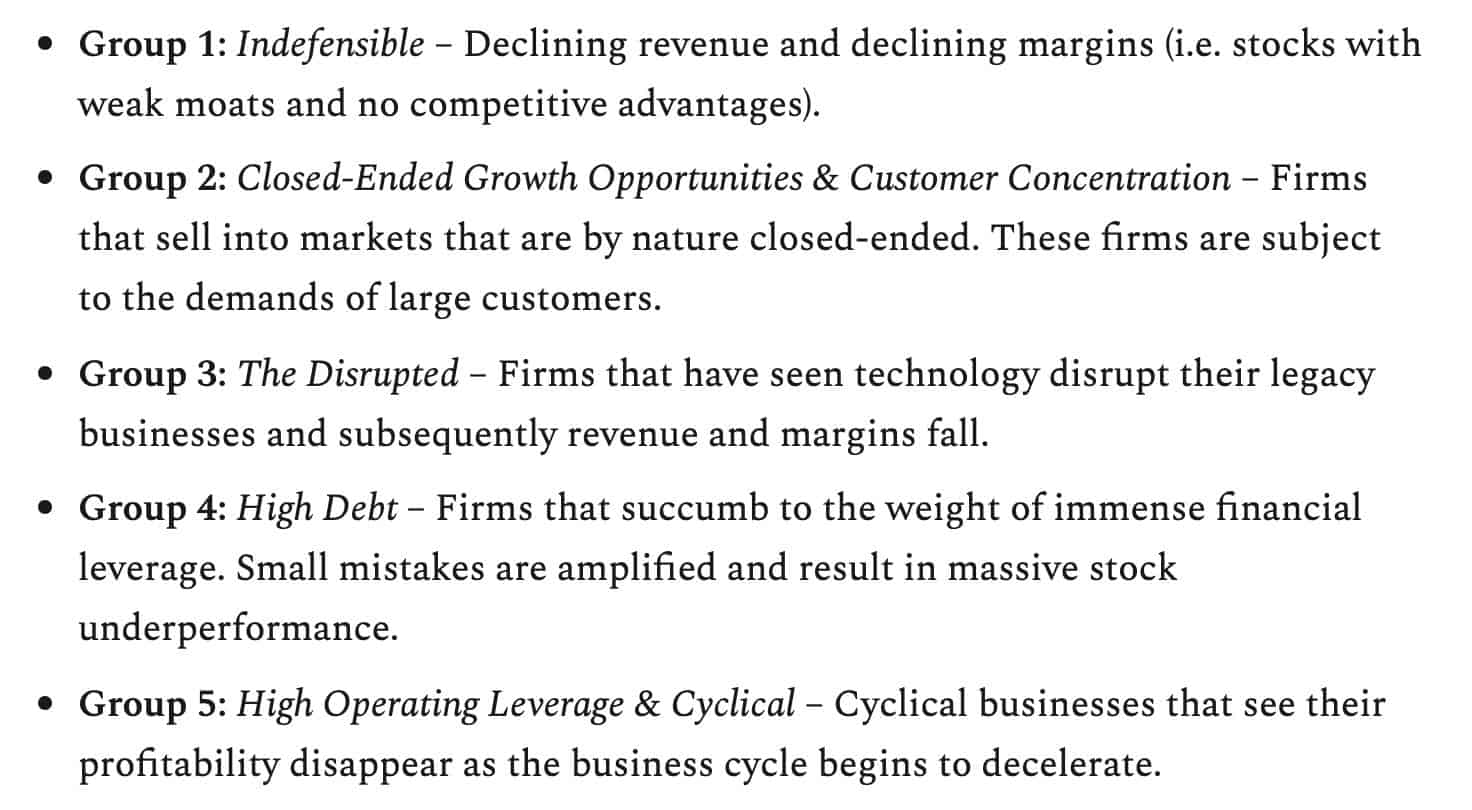

He outlined another five groups (from the newsletter):

These five groups combine to make one terrible stock (unless it’s 2020 — then that’s to the moon). Dubra notes the common traits of STGD (emphasis mine):

“What we find is that STGD generally suffer from combinations of financial leverage (too much debt), operational leverage (too much overhead) and cyclicality (not enough revenue when they need it). These characteristics amplify negative developments and create scenarios of irrecoverable loss for investors.”

Bringing It All Together

Dubra gives us a TL;DR of his research. And yes, it is as simple as you think.

Stocks That Go Up: “generally coincide with high revenue growth and the ability to grow at high rates over long periods of time. Better said, STGU tend to benefit from open-ended growth opportunity that enables both high growth and high durability of that growth.”

Stocks That Go Down: “exhibit characteristics of financial leverage, operational leverage and cyclicality. Those things are to be avoided in a thoughtful way.”

__________________________________________________________________________

Lecture Of The Week: Li Lu at Columbia University, 2006

GIFs by tenor

GIFs by tenor

Li Lu is one of my investing heroes (behind Burry). Lu’s approach to investment is logical, straightforward and produces incredible results. He’s one of the few (if only) man Charlie Munger trusts with his capital.

Check out this lecture Lu gave at Columbia University in 2006. Lu’s words of wisdom penetrate time, creating evergreen content.

It’s an hour and 46 minutes and worth every second.

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!