Mineros S.A. (MSA.V): Capital Returns in Mining Done Right

Last week, we introduced our mini-series on junior mining stocks … and how we’ve picked massive winners that have outperformed their benchmarks and underlying commodity prices.

As I mentioned, nobody cared about these ideas when I shared them … nobody outside our Macro Ops Collective community. No matter who I pitched them to, the ideas fell on deaf ears. Why invest in junior mining stocks at 40% free cash flow yields when NVDA gaps up daily?

I even tweeted about the ideas I saw in March … and people didn’t believe me!

Like this guy …

If investing in 40%+ FCF-yielding companies with excellent capital return policies is “boomer talk” then I need an AARP card.

So today, I’m sharing my deep dive on Mineros S.A. (MSA.V).

MSA is a mid-tier gold mining company operating in two countries, Colombia and Nicaragua. We bought our shares at $0.81 for a $243M market capitalization (Note: $ = Canadian dollars).

Since 2019, the company has returned $117M in dividends while reducing total debt from $114M to $43M. That’s ~$188M in cumulative shareholder returns.

We bought the stock for three main reasons:

MSA has torque on higher gold prices, which should lead to outsized free cash flow generation over the next few years.

The company will use those cash flows to eliminate all outstanding debts.

MSA can juice shareholder returns once debt-free via increased dividends and/or buybacks.

In short, MSA can return at least 80% of our cost basis by 2026 between dividends, debt reduction, and share buybacks at the current gold price and estimated production guidance.

Since publishing our piece on March 5, the stock has increased by ~47% (10% per month, not bad!) while reducing debt and paying dividends.

If these ideas excite you, you should consider joining our Macro Ops Collective.

It’s a private investment community with former hedge fund managers, Market Wizards, and full-time traders. All trying to become consistently profitable while having a hell of a good time in the process.

If this sounds like your type of place, join us using the link below. We can’t wait to see you.

Now, onto the idea.

You’ve already heard the elevator pitch on MSA.V above, so let’s dive into the company’s mining assets.

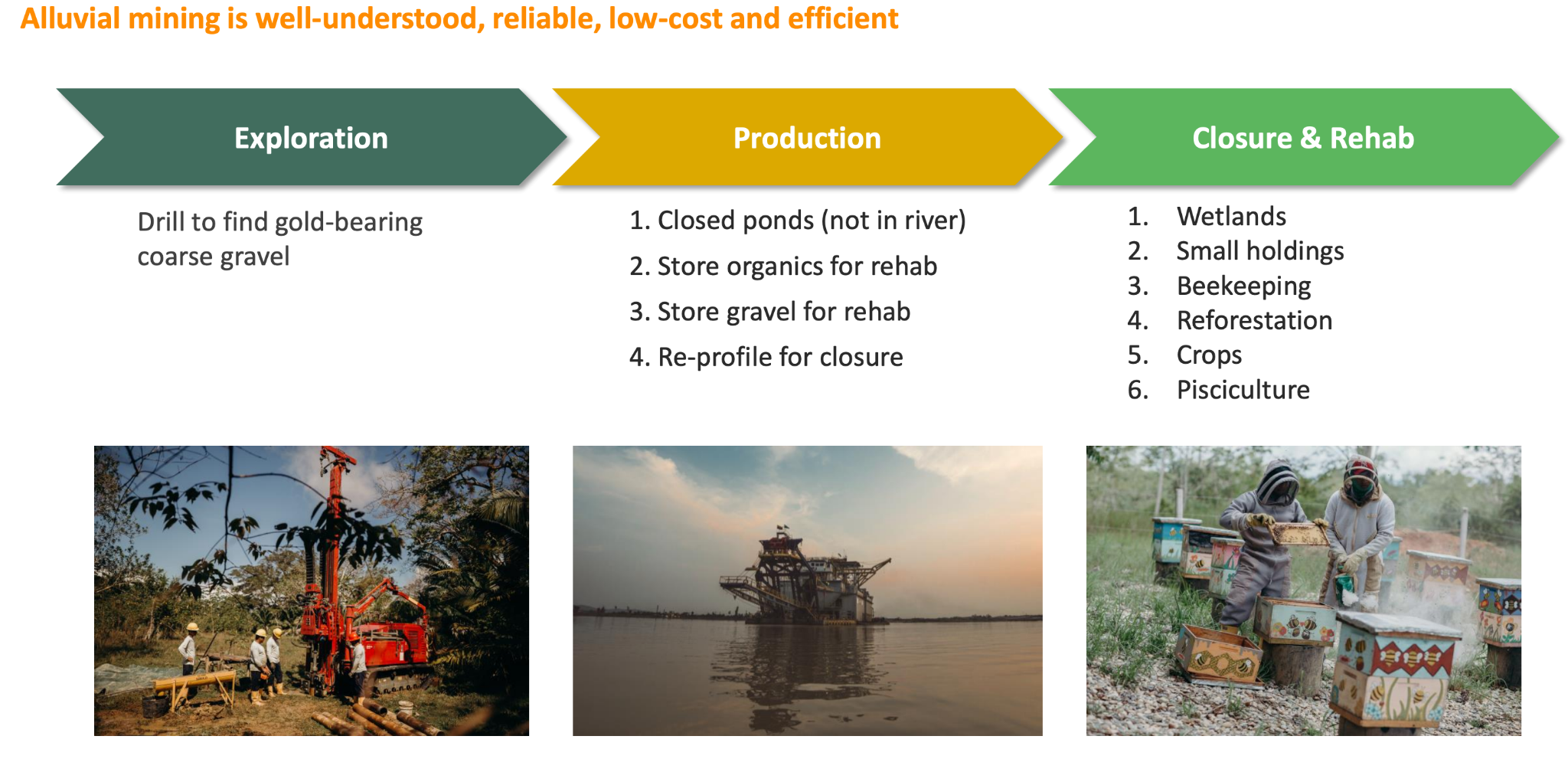

Colombia: Alluvial Deposit w/ History of Profitable Mining

MSA’s Colombia alluvial deposit represents ~42% of annual production (or 86,000-96,000 oz/year). According to the company’s latest DFS, the deposit has 10+ years of reserve life left.

Alluvial mining is slightly different than a conventional open pit operation. It’s more like a Canadian oil sands project (see below).

Here’s how the company explains the process (emphasis added):

“Alluvial Au deposits mined from closed ponds in the floodplain adjacent to the Nechí River as free Au is hosted in sand and gravels with no use of cyanide or mercury as the Au recovery process is done through only gravity.”

Alluvial mining is efficient, somewhat predictable, and low-cost. For example, MSA has produced at least 80,000oz annually from this asset since 2018 at sub-$1,400 AISCs.

Then there’s the Nicaraguan asset.

Nicaragua: Low-Cost, High Volume Underground Gold Mine w/ Growth Opp

MSA’s Nicaraguan asset produces gold from two underground mines (Panama & Pioneer). Like Andean Precious Metals (APM.V), MSA also purchases and processes gold from local artisanal miners.

About 30% of production comes from the company’s underground mines, with the remaining 70% from third-party artisanal miners.

In 2027, the company plans to expand underground production by ~44,700 oz/year from its Porvenir satellite deposit.

Since 2018, the Nicaraguan asset has produced between 107,000 oz - 130,000 oz annually at a ~$1,420/oz AISC (see below).

So far, the thesis seems straightforward. You have a company with two decent gold-producing assets with greenfield expansion options and a history of returning capital to shareholders.

This is where things get fun. Let’s model potential shareholder returns over the next few years.

Shareholder Returns: How We Get Paid

The company estimates it will produce 209,000-220,000 oz of gold in 2024 at an average AISC of $1,480/oz.

Here’s a back-of-the-napkin model of the next three years with the above assumptions. We also assume the company spends ~13% of its revenues on capex (historical averages) and an average gold price of $2,050/oz.

We estimate ~$66M in annual free cash flow for a 27% yield at our cost basis.

Then there’s capital allocation.

There are two things I expect the company to do this year (2024):

Pay a dividend of ~$25-30M (in line with prior years at lower gold prices)

Pay off half of the remaining long-term debt (~$20M)

Those two decisions alone would get us a 21% shareholder yield and the company would still have ~$70M in net cash on the balance sheet.

So by the end of 2024, we’d get $50M in shareholder returns plus a business generating $66M+ in free cash flows at a lower EV due to debt reduction and positive cash flow.

Between 2025 and 2026, MSA can add another $144M+ in shareholder returns from dividends, buybacks, and debt repayment (see below).

There are a lot of factors in the above model, and they’re all assumptions that could change, etc.

However, management has a clear path to returning 80%+ of our cost basis to us over the next three years. And they’re one of the few mid-tier mining companies with a history of capital returns, without straining their cash balances.

Let me explain.

Over the past five years, MSA has averaged ~$48M in cash and equivalents. Our model estimates the company will have $79M in cash by the end of 2026. In other words, the company would still have a 64% higher cash balance than its 5YR average even after returning $194M to shareholders.

I want to clarify that I don’t know if management will buy back stock, pay more dividends, or just hoard the cash (I doubt given their capital allocation history). Just that they’ve historically done these things with less free cash available.

The point is that there are multiple ways for us to make 20%+ on our investment at ~$2,000/oz gold.

The company could return >100% of our investment within three years if gold stays where it is or trades higher over that time frame.

I know what you’re thinking … this seems like a no-brainer. A lay-up. So why does the opportunity exist? What did we do to deserve Mr. Market’s blessing?

There are a few reasons.

First, the company is a mid-tier gold miner with assets in Colombia and Nicaragua, and it trades on the TSX Venture Exchange. I could stop there, and you’d understand.

Second, gold miners have dramatically underperformed spot gold prices (besides IDR). Despite up 58% from the lows, MSA.V is still down 21% from its IPO price.

Finally, there’s the unrelenting belief that mining companies are capital incinerators. While this is true for the majority of mining companies, it’s not the case here. MSA has paid an annual dividend for 13 consecutive years and hasn’t issued a single new share since 2021.

Conclusion: Many Shots on Goal For 20%+ Yields

MSA.V is one of those rare mining stocks that has a clear path to generate 20%+ yields and return 80% or more of your investment within a few years.

The company has done everything right. They’ve reduced debt, paid dividends, not diluted shareholders, maintained healthy cash balances, and sold off high-cost mines.

At our cost basis of $0.81/share, I feel confident that this position will generate at least a 20% return on our investment. And it wouldn’t shock me to see yields inflect even higher if gold stays above $2,100/oz.