On Wednesday night, I had a call with John Welborn, Chairman of Fenix Resources (FEX).

FEX is our iron ore producer, expanding production from 1.3Mt/year to 4Mt/year+. It also boasts a growing logistics business and port infrastructure assets worth more than the current market cap (excluding its net cash position).

You can read our deep dive into the company here.

The TL;DR is that the company has ~900% upside between its 4Mt/year of potential production, $20M in future logistics EBITDA, and ~$161M in hard asset value between its net cash and port assets/logistics infrastructure.

My base case with any stock is that there’s always something I’m missing – some skeleton in a closet somewhere. That’s even more true when I find a stock with 900%+ upside, like FEX.

That’s why I wanted to talk to John. I wanted anything to kill the thesis … or my upside target.

The call didn’t kill my thesis.

It reinforced my view that FEX is massively undervalued for explainable reasons. Moreover, John understands the catalysts needed to realize that value in the market … and has a plan.

But before we dive into my call notes … I want to tell you about our Macro Ops Collective.

The Collective includes all of our research, a full library of reports and videos on theory and strategy, our proprietary market dashboard, plus our internal slack where the team and I, plus fund managers and die-hards from around the world talk shop, exchange ideas, and shoot the shit.

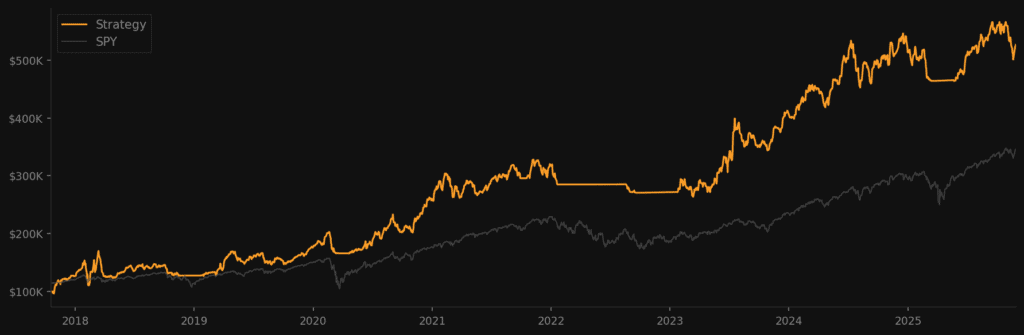

We’re having a decent start to the year, with our book up ~40% YTD.

Enrollment into our Collective is open until the end of this week, and spots will fill up fast.

If you want to join our crew, just click the link below. I’m looking forward to seeing you in the group.

Alright … back to the call notes. I hope you enjoy it.

John’s background and how he got into the mining industry …

John grew up in Midwestern Australia and spent most of his young adult life as a professional rugby player (see below).

After rugby, Welborn worked as an investment banker specializing in mining finance. According to John, “Everyone wanted to work in mining finance in Australia because it’s such a big business. It’s where I learned about the inner workings of mining companies.”

John’s first stint in mining is important because of how bad it went. In 2014, John joined Equatorial Resources (EQX.ASX) to develop an iron ore mine in the DRC (what could go wrong??).

The timing couldn’t have been worse. From January 2014 to January 2016, iron ore prices fell by 68% (see below).

The project failed. So John took his lumps and moved to gold.

Around 2015-2016, John joined gold producer Resolute Mining (RSG.AX). During his stint at RSG, Welborn improved the company’s balance sheet and helped bring four gold mines into African production.

John left Resolute Mining in 2020 and found himself COVID-locked in Midwestern Australia.

He always thought he’d return to the gold space. He spent most of his COVID lockdown looking at gold projects and thinking of ways to consolidate the Midwestern’s numerous stranded gold deposits.

Then he found FEX …

How John joined Fenix Resources (FEX) …

“I reverse-recruited myself into FEX.”

John found the company by reading a press release on the company’s latest financing round.

He learned his lessons from the 2014 Equatorial debacle, and he saw something different in FEX (paraphrased, emphasis added):

“They were trying this pop-up shop method. The company had low-cost, low-complexity iron ore they could extract at super-high margins. So the initial plan was to use as little capital as possible to get the project running. And then take the cash we generated and return it back to shareholders.”

It worked.

FEX raised AUD 15M in 2020. Since then, it’s paid AUD 65M in cumulative dividends.

The strategy worked. More importantly, John saw a future for FEX that went far beyond the company’s “pop-up shop” cash return vehicle.

He spent that year buying 15M shares in the open market, got appointed to the board, and became chairman.

I then shifted the conversation to FEX business segments, starting with the cash cow: mining.

How John thinks about FEX’s mining business …

“My number one focus is profitability. I focus on profitability because we generate such high margins. And I want to ensure that we don’t get complacent and it stays that way.”

This was the most critical part of the conversation. FEX’s mining business is its heart. It generates ~100% of the company’s cash flows and is vital to us achieving 900%+ upside over the next few years.

John has two goals with the mining business:

- Get production to 4Mt/year in the short-term (1-2 years)

- Add resources and extend mine life to grow production to >10Mt/year in the medium/long term

The fact that they haven’t done this yet is one of the reasons the stock trades so cheaply. The market wants production growth, and it wants 10YR+ mine lives.

Why does John care so much about 4Mt/year? Because it translates to $216M in pre-tax profits versus the current market cap of $175M (AUD 264M).

The good news is that FEX is executing this strategy. Shine Iron Ore officially restarted a few days ago. One down … one to go.

Then there’s resource development and mine life extension. There are two ways FEX can accomplish this:

- Buy more tons from their JV with Sinosteel Midwest Corporation

- Spend money to develop nearby stranded assets

Then there’s forecasting iron ore prices … which took a turn I wasn’t expecting.

How John thinks about forecasting/modeling iron ore prices …

I will paraphrase John’s comments on iron ore pricing and forecasting as there’s not much I can add (emphasis added).

“Near-term we are modeling $100/t, that’s because we can lock-in swaps above that price. That gives us a decent idea of what our short-term floor looks like.”

“Long-term they are not trying to out-think the analysts. So what this means is internally we think about an $80/t price environment and try to make our business work at that price.”

Okay, I lied about not adding anything. I thought the following comment on iron ore as a commodity was fascinating… especially from the Chairman of an iron ore producer!

“I’m not necessarily bullish on iron ore as a commodity. Don’t get me wrong, I think we make a ton of money if iron ore stays at or above $100/t. But I’m not one of these CEOs that gushes over their commodity. We’re ore junkies. Our job isn’t to glamor about the commodity, but to extract it and sell it at the highest margin we can.”

That’s the opposite of what you hear from 99.99% of mining CEOs. Anyway, let’s return to John’s thoughts on iron ore prices.

“Personally there is a structural bearishness to commodity forecasts. But its misguided. Africa comes online more slowly than people think. Then look at China’s property downturn. you would’ve expected a much bigger impact on steel production, but you didn’t see it.”

“There’s a broader lifestyle index that people don’t realize. What I mean by that is for the first time you have billions of people starting to enjoy the luxuries we in ‘developed’ worlds take for granted … things like air conditioning, more advanced buildings, cars, infrastructure, etc.”

My next favorite segment was John’s thoughts on costs.

How John thinks about lowering costs …

“Everything we do comes down to moving tons of ore. That’s the denominator. If you can justify an expense by telling me how we can finance it with however many tons we need to move, I’ll hear it. But it always comes down to how many tons of ore we must move to justify every expense.”

John explained his philosophy on costs through a story.

A truck driver once threw a pair of new-ish safety goggles in the trash. The goggles cost $50 and apparently could’ve been worn a few more times before being thrown out.

John saw this and said, “why did you throw those away? They were still good. That’s $50 you threw away. That means we need to move 1 ton of ore to recoup that expense.”

Before you assume that John’s a hard ass and there’s a ton of truck driver turnover … consider that FEX posted a 9% truck driver turnover ratio this year. The industry standard is 50-100%.

John tracks everything at FEX through efficiency and cost-savings scores. Drivers get bonuses for saving fuel, driving safely, and meeting various health/well-being criteria (they have saunas for these guys!).

John said there are ~3 KPIs for every position on the mining side. Everyone knows how their role impacts costs and margins down to the ton.

“Remember, it all comes down to tons of ore required per expense.”

John also emphasized that “every employee understands their role in the FEX machine. They know they are valued, and they can see the value they contribute to our company.”

The final part of our conversation revolved around capital allocation and risk scenarios.

How John views capital allocation, thesis killers …

“If iron ore goes to $60/t, I hope to God we have the balls to buy everything we can. We could just own the Midwest.”

FEX is in growth mode. That doesn’t mean they won’t pay some dividends. However, their primary goal is to invest in production growth and resource expansion.

That’s why I love the above quote.

FEX’s share price would get destroyed at $60/t iron ore. However, the company has a strong balance sheet and could use that price environment to buy tons at pennies on the dollar.

Thanks to its port infrastructure and logistics assets, FEX can sell these stranded tons profitably, unlike its local peers.

John also prefers buybacks to dividends, which surprised me, considering he owns 15 million shares.

Finally, the thesis-killers.

I prefaced my question by saying, “I see two ways this trade fails. The first is that iron ore prices collapse below your AISCs and you pause growth plans. The second is that AUD/USD breaks out and iron ore stays flat which compresses margins and reduces cash flow.”

Here’s John’s response (paraphrased, emphasis added):

“That’s something we worry about, too, which is why we hedge using swap contracts in AUD for our iron ore. The swap contract protects us against changes in commodity price and the currency.

We’ve been fortunate that AUDUSD has traded in this range for what seems like forever. But that could change, and we want to be prepared.”

John said that FEX hedges ~40-50% of its production with these AUD-backed swap contracts.

He even considered hedging 100% of their breakeven cost structure—that is, hedging enough production to cover all expenses, with the remaining ore as pure profit.

However, the company remains “opportunistic” in its hedging – for example, FEX hedged production when iron ore prices spiked to $120/t.

I’m generally against hedging. If you’re bullish on a commodity, you want an unhedged book to gain the most leverage to the upside in commodity price.

But maybe that’s not the best way to think about iron ore. I’m not bullish on iron ore the way I am on tin, copper, or even gold/silver.

At around $85- $100/t, FEX generates more cash flow than its market cap. If that’s my thesis, a cash flow story, maybe it makes sense to hedge closer to 100% of production and lock in those cash flows.

I’d love to hear feedback on this topic.

Concluding Thoughts

I left the call more bullish on FEX than before. Maybe it’s my bias, but here’s the rub: The hard assets alone (port + logistics assets + net cash) are worth more than the market cap.

So you get the mining business for free—which will grow from 1.3Mt/year to 4Mt/year and generate more free cash flow than its market cap, assuming historical iron ore prices.

And before you go … remember to join us in the Macro Ops Collective!

The Collective includes all of our research, a full library of reports and videos on theory and strategy, our proprietary market dashboard, plus our internal slack where the team and I, plus fund managers and die-hards from around the world talk shop, exchange ideas, and shoot the shit.

You’ll get access to CEO interviews, like the one you just read, that you can’t find anywhere else online. We find ideas nobody’s talking about to generate returns and provide differentiated research and insights.

We’re having a decent start to the year, with our book up ~40% YTD.

If you want to join our crew, just click the link below.

Can’t wait to see you there.