Every six months, we pour over our trade logs, journals, and public writings from the previous two quarters.

We review what we thought markets would do, how we placed and managed bets on these opinions, and then compare them to how reality unfolded.

It’s a ruthless study of our mistakes in thinking and execution.

Like Dalio says, “embedded in each mistake is a puzzle, and a gem.”

Pain + Reflection = Progress.

This is, without a doubt, the most valuable exercise we do. We’re entirely transparent … sharing the good, the bad, and the ugly. Because it’s in the ugly, the mistakes, that you improve.

You don’t see this in a lot of trading/investing newsletters. Everyone claims high win rates and eye-popping annualized returns with negligible drawdowns.

Those traders pedal lies to generate clicks and sales or reaffirm a deep insecurity left from some high school breakup.

Trading will humble you. The market will humble you. It will reveal your greatest weaknesses … only after it takes most of your capital.

These portfolio reviews help expose our weaknesses, find those gems, and improve our processes for the coming year.

Macro Ops Collective.

It’s a private investment community with former hedge fund managers, Market Wizards, and full-time traders. All trying to become consistently profitable while having a hell of a good time in the process.

If this sounds like your type of place, join us using the link below. We can’t wait to see you.

Now, onto the portfolio review.

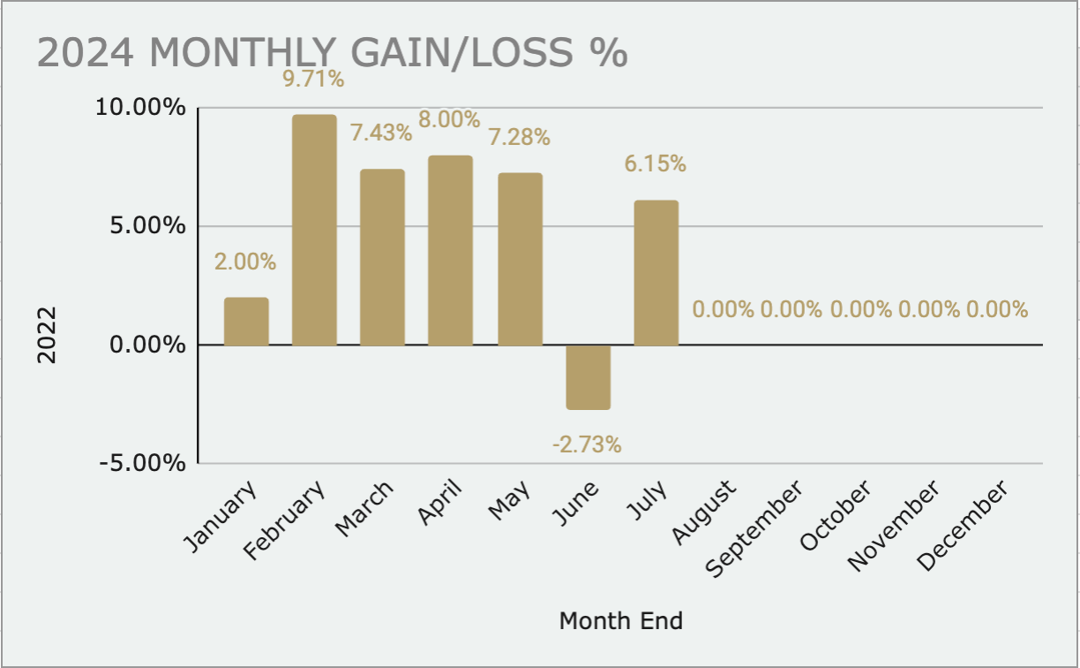

1H 2024 Return Metrics

Let’s start with general return metrics:

- 1H 2024 Return: +31.69%

- Strongest Month: February (+9.71%)

- Worst Month: June (-2.73%)

You can see a breakdown of our monthly returns below.

Soros once said, “it’s not about whether you’re right or wrong … but how much you make when you’re right, and how much you lose when you’re wrong.”

So far, we’re making a lot when we’re right (see February through May), and not losing much when we’re wrong (June).

We’re also a global macro investment vehicle. We’ll buy cotton futures, sell short currencies, and buy Square $SQ all in a week if we want.

We’ll go anywhere we think we have a repeatable and profitable edge. That’s part of the reason why we’ve generated decent returns YTD. If a market isn’t working, we simply move to one that is … and one where we have a profitable, backtested strategy.

Let’s explore where we generated our returns.

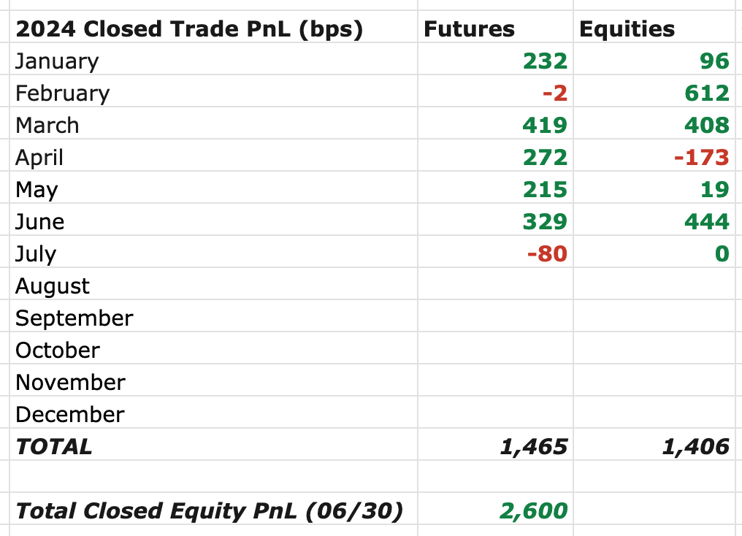

First, we’ll analyze our performance on a Closed-trade basis. We use Closed Trade PnL analysis because it doesn’t benefit us from open profits … which aren’t ours until we close the trade.

We ended June with ~2,600bps (or 26%) in Closed Trade profit split equally between futures and equities (see below).

I’ll cover the Equity section of our portfolio review while Alex covers futures and forex in his half of the update.

As you can see, three months (February, March, and June) generated 90% of our equity returns.

Let’s analyze the trades that made in those months.

Sprott Uranium (U.UN): +668bps Profit in February

We’ve traded U.UN over the past few years with modest success. But it wasn’t until we bought the breakout in August 2023 that we bagged serious profit.

We developed a fundamental conviction that uranium prices would rise (read our industry primer here) and bought on a technical confirmation (one of our differentiating factors).

We risked 75bps on the trade at an average price of CAD 18/share (see below).

You can read why we sold in February here.

We booked 668bps in profit – or nearly 7% notional – from this trade.

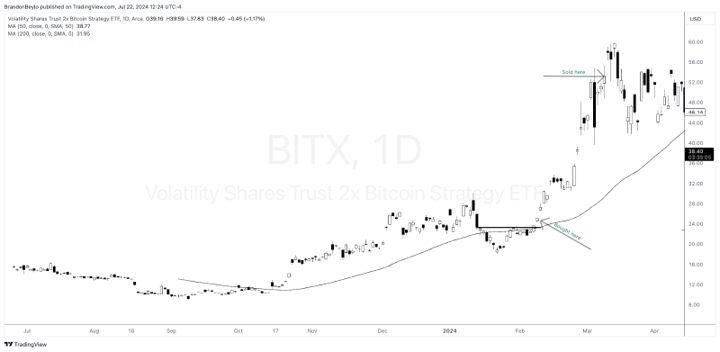

Bitcoin 2x Leveraged ETF (BITX): +440bps in March

BITX is an excellent example of our global macro trading approach. We go where we see value/inflecting technicals and fundamentals. Why stay in dead-money markets when there’s always a bull market somewhere??

Bitcoin entered its next bull market leg in February after breaking out of a two-month sideways consolidation (see below).

However, instead of trading BTC or GBTC, we chose the double-leveraged BITX. This trade sounds insane to most investors, but that’s because they lack the tools to manage risk and position sizing.

We bought BITX on 02/08 at $24.61 with an initial stop-loss at $21.69 and risked 50bps. In other words, if the ETF traded down to $21.69, we’d be out with ½% notional loss.

This sizing allowed us to get sizeable notional exposure with little actual account risk (barring a gap down).

You can see the trade below.

The ETF never flirted with our initial stop-loss, and we bagged 440bps (or 4.5% notional) in profits in ~30 days (you can do the IRR calculation, it is pretty good).

Tidewater (TDW) & Vista Energy (VIST): +354bps in June and counting

TDW and VIST have been two of our biggest winners in the portfolio. Let’s start with VIST.

VIST is our Argentinian oil and gas producer. We bought our initial position around $5/share in 2022. Since then, we’ve traded in/out of the name before exiting our entire position around $14/share in December of 2022.

We bought back our position in early January 2023 at a cost of $14/share. Since then, the stock has increased by 200%+, and we’re up ~12x our original risk capital.

We took partial profits in June as the stock closed below the 50MA for the first time since November 2023.

The best part about VIST was that it stayed cheap despite its share price rising 200%. How did they do it? The company executed on its 2025 plan, increasing reserves, expanding margins, and effectively allocating capital.

That convinced us to reinvest in January 2023 despite the stock running from $5 to $15. Plus, the stock has outperformed its peer benchmark and oil prices since 2022.

As of this writing, we hold a ~3.30% notional position.

Then there’s Tidewater (TDW), our offshore service vessel company. Like VIST, TDW has been a long-term winner for our portfolio. We’re up 205% on our initial position and up ~60% and 112% in our second and third-leg adds, respectively.

On average, our TDW positions are up ~7x their initial risk capital.

As of this writing, we hold a ~3% notional position in TDW.

Open Profits: What’s Driving Our Equity Returns Today?

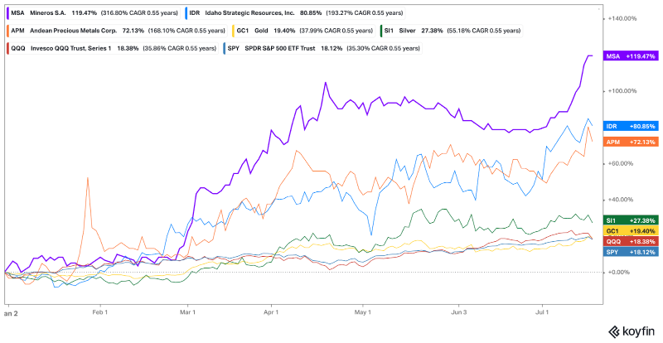

The rest of our equity book return comes from open profits in our largest positions, which include:

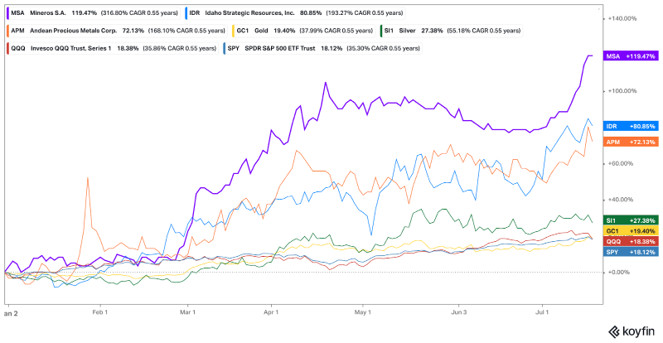

- Andean Precious Metals (APM.V)

- Idaho Strategic (IDR)

- Mineros S.A. (MSA.V)

We’ve written extensively about these names in our Macro Ops Collective, and recently shared our analysis on APM.V with the public (read here).

Here’s a quick review of the above names at the time of purchase.

- MSA.V had a 30% shareholder yield, generated 42% of its EV in annual FCF, and had net cash on the balance sheet.

- APM.V traded for less than its NCAV despite owning a silver mine that generated $30M in annual profits and a newly acquired gold mine that will do ~$25-30M in free cash flow.

- IDR had net cash on the balance sheet, low AISCs, and a path toward 20,000oz of annual production for $24M in cash flow (the market cap was $60M when we bought).

These three names have outperformed the Nasdaq 100, the S&P 500, and their respective underlying commodities YTD … and by a wide margin.

Yes, there’s been some recent chop in precious metals prices. But the long-term trends of our mining companies remain intact. So we hold.

We can tactically short gold and/or silver on technical breakdowns to hedge our PM mining exposure. That would allow us to hold our winners while hedging our largest risk factor (gold and silver prices).

Looking Ahead: Don’t Do Anything Stupid

I like how our good friend Kuppy put things in his latest research note (emphasis added):

“We get it, Trump and JD are looking for low rates to make us great again – dollar smash, gold up, reshoring, energy, BTC, with a sidecar of tech-crack down. Seems like everyone is finally realizing all paths lead to inflation…shocker..”

Our book is perfectly positioned for a reshoring, dollar-smash, precious metals-up, kind of world.

That’s the “easy” part.

The hard part now is not to do something stupid. The trend remains our friend. Our job is to sit on our hands and do nothing until the trend or fundamentals change.

Until then, we suggest you do what we’re doing this summer … trading lightly, reading heavily, and turning over as many rocks as we can to improve the portfolio … knowing very well that the hurdle rate has never been higher for entry into the book.

Your Value Operator,

Brandon