Alex here with your latest Friday Macro Musings…

As always, if you come across something cool during the week, shoot an email to alex@macro-ops.com and we’ll share it with the group.

Recent Articles/Podcasts —

Boom-Bust Barometer Biffs Badly — Alex shows how the divergence between Ed Yardeni’s Boom-Bust indicator and the S&P 500 means lower stock prices ahead.

Articles I’m reading —

The Atlantic published a worthwhile read on the difficulties of prediction titled “The Peculiar Blindness of Experts: Credentialed authorities are comically bad at predicting the future. But reliable forecasting is possible”. The article focuses on the work of Phillip Tetlock and the traits that distinguish a good forecaster from a poor one (sidenote: if you haven’t read Tetlock’s book, Superforecasting, go and pick it up. I consider it required reading for anybody involved in markets).

A section of the article talks about an experiment that Tetlock began running in the 80s where he collected forecasts from hundreds of highly educated and experienced “experts” about specific events regarding American-Soviet relations. The project lasted 20-years and comprised 82,361 probability estimates about the future. Here’s a clip from the article on Tetlock’s findings.

The result: The experts were, by and large, horrific forecasters. Their areas of specialty, years of experience, and (for some) access to classified information made no difference. They were bad at short-term forecasting and bad at long-term forecasting. They were bad at forecasting in every domain. When experts declared that future events were impossible or nearly impossible, 15 percent of them occurred nonetheless. When they declared events to be a sure thing, more than one-quarter of them failed to transpire. As the Danish proverb warns, “It is difficult to make predictions, especially about the future.”

The piece goes on to point out that “Even when faced with their results, many experts never admitted systematic flaws in their judgment. When they missed wildly, it was a near miss; if just one little thing had gone differently, they would have nailed it. ‘There is often a curiously inverse relationship,’ Tetlock concluded, ‘between how well forecasters thought they were doing and how well they did.’”

Dunning-Kruger is a powerful drug… The article also mentions one study which compiled a decade’s worth of annual EURUSD prediction from 22 leading investment banks, where each year the banks predicted the end-of-year exchange rate. Wanna guess how they did? If your answer is waaaay off the mark then well done. The “banks missed every single change of direction in the exchange rate”. And “in six of the 10 years, the true exchange rate fell outside the entire range of all 22 bank forecasts.”

Takeaway: Read Tetlock, train to become a “fox”, and listen to the “experts” to develop a sense of the popular narratives but not for what’s likely to actually happen. Here’s the link.

Hayden Capital’s latest Investor Letter is out and like always, it’s worth a read. Fred Liu, who’s the manager of Hayden, typically includes a thoughtful section on investing theory in his letters which I enjoy reading. In this note, he writes about how many of the stocks he buys have a wide range of outcomes. He explains that this is why the mispricing exists in the first place as most investors tend to put them in their too-hard bucket. But it’s not necessarily a bad thing and what’s more important is understanding the “angle” of outcomes versus the width. Graphs below give you a visual of what he’s referring to.

He also reviews a number of his holdings, including one of his more recent additions, Sea Ltd. (SE). SE is a Singapore based e-commerce company disguised as a mobile gaming business that does few sales in Singapore but is big in 13 other Southeast Asian countries, with Indonesia being one of its bigger markets, that’s listed on the NYSE. It’s an interesting company that’s a compelling long even after its 185% year-to-date rise.

Here’s some notes from Fred on SE’s valuation:

However even at an $11BN valuation, if we are correct in our thesis, it’s going to look very cheap in hindsight. Sea has $1.5BN of net cash on its books, resulting in an Enterprise Value of $9.5BN. Of this, I conservatively value Garena at ~10x EBITDA (compared to gaming peers at ~12 – 17x), for ~$4.5BN today20.

The result, is the market implying a ~$5BN valuation for Shopee. This is still attractive, for a business that is #1 in the region at 28% market share and will do ~$16BN in GMV this year or a 0.3x GMV multiple (albeit a very crude / simplistic valuation measure). Especially when compared to peers such as Flipkart (>2.5x GMV), Tokopedia (~1x GMV), and the latest private rounds of others such as Tiki.vn, Bukalapak, etc at between 1.5x – 2x GMVs, this looks like a relative bargain.

… Marketplaces consistently have a 30-40% margin profiles globally. Assuming Shopee follows this “base rate”, we’re looking at ~$200M in normalized earnings power this year. At the market implied $5BN, this may optically seem fairly valued at ~25x normalized earnings. However, I expect Shopee to grow at a ~40% y/y CAGR over the next five years, ahead of Southeast Asia’s projected e-commerce growth rate of 32% y/y (Google-Temasek’s 2018 report projects e-commerce to grow 34% y/y between 2015 – 2025; LINK).

Given Southeast Asia’s accelerating e-commerce adoption (e-commerce penetration is only ~3% in Southeast Asia), the soft-datapoints indicating an inflection in profitability, “downside” protection due to the strength of Garena, and our “edge” of looking in areas of the world few US-based investors are paying attention to, we’re very comfortable making a bet on Sea Ltd. Forrest Li, the CEO, has stated he thinks Sea Ltd can become a $100BN business – we sure hope he’s right, and will be following closely along that journey.

Give the full letter a read. Here’s the link.

Oh, and one last thing. Take two minutes and give this Bloomberg profile of Salesforce CEO, Marc Benioff, a read (link here). I had to do a double take to make sure it wasn’t a piece from The Onion or something Mike Judge had dreamed up. The hubris is nauseating. I haven’t taken a hard look at CRM in a while but I’m going to throw it on my research list for short targets after reading this one. After all, perpetually buying growth is not a long-term business strategy.

Video(s) I’m watching —

I’m talking my book, but… give these videos a watch that confirms our bias on two of our current longs ;). Honestly, though, these are two well put together presentations arguing the bull case for two stocks that we believe have significant upside. The presentations are on Garrett Motion (GTX) and Graftech (EAF) and were given at the recent VALUESPAÑA conference. Here’s the link to GTX and EAF.

Charts I’m looking at—

I’ve been scratching my head over the collapsing NYSE margin numbers these last few months. The data set only goes back to the mid-’90s but there’s no comparable episode where we’ve seen investors deleverage this much outside of a bear market and recession.

Sustained bear markets are caused by euphoric overleveraging (aka. Belief Cascades, which I’ve written about here) late in the business cycle — see the margin spikes in 99’ and 06’/07’. This over-positioning creates the fragility necessary for a prolonged bear market (ie, forced selling). Not only have we not seen anything like that this cycle, but with equities near historic all-time highs, investors are derisking.

I don’t know what to make of this and if any of you have ideas, I’d love to hear them. My hunch though is that this is a sign of accumulating pent up demand that’s going to create another large up-leg in markets once this current correction plays out.

Podcast I’m listening to —

I may be a little biased but I’ve listened to Chris D’s talk with fellow MO Collective member Darrin Johnson twice and I’ll probably listen to it a few more times. It’s the best interview I’ve listened to in a while. Darrin is wickedly smart, knows his stuff, and walks the talk. Do yourself a favor and give it a listen, Darrin drops a ton of knowledge bombs. Here’s the link.

Book I’m reading —

This week I’ve been reading The True Believer: Thoughts on the nature of mass movements by Eric Hoffer. Even though the book was first published in 1951, the author’s insights into the psychology of mass movements are as timely as ever.

At only 168 pages in length, the book packs quite a punch. It’s all meat… Hoffer pulls from history to give color and examples of mass movements while dissecting the drivers and requisite environment for such movements to reach a critical mass.

I’ve riddled the book with highlights and page tags. I highly recommend picking it up as I think it’s full of knowledge that will be applicable to understanding geopolitical developments over the coming years. Here’s one of the many lines from the book that I enjoyed.

A man is likely to mind his own business when it worth minding. When it is not, he takes his mind off his own meaningless affairs by minding other people’s business.

This minding of other people’s business expresses itself in gossip, snooping and meddling, and also in feverish interest in communal, national and racial affairs. In running away from ourselves we either fall on our neighbor’s shoulder or fly at this throat.

Trade I’m considering —

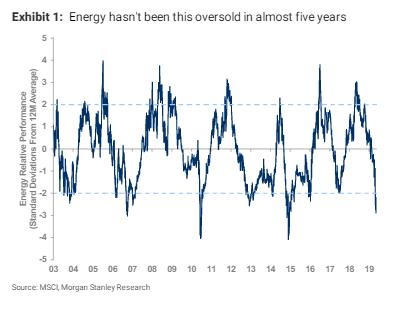

Energy stocks have been getting hammered. The selloff is being driven by the rise of the EV s-curve adoption narrative along with investor’s preference to only own stocks that trade at over 10x revenues and have “cloud” in their business description.

Gavekal Research and I have both written about why we think the market is way off-target on this one (link here). Oil recently started a positioning driven selloff (speculators became crowded on the long side) which should continue to play out over the next couple of weeks. But, ultimately, I think oil and energy stocks are setting up for a buying opportunity.

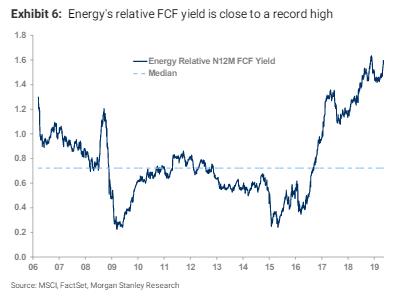

Energy hasn’t been this oversold in nearly five years.

The incessant selling has created some incredible value opportunities. Energy’s relative FCF yield is now close to a record high.

There’s a number of stocks I like in this space. One that I’m currently digging into is Sandridge Energy (SD). I first came across SD while reading one of my favorite market blogs, Adventure’s in Capitalism, that’s written by the pseudonymous Kuppy.

In a post titled 40% Less Than Carl Paid… Kuppy lays out his bullish thesis for SD. Here’s an excerpt (emphasis by me).

Since he [Carl Icahn] took control this summer and replaced old management; operating costs have been cut dramatically, non-core assets were sold, contiguous and overlapping assets were acquired in a highly accretive manner and North Park Colorado results have surprised to the upside. This is Carl’s classic playbook; add value, don’t do anything stupid and get someone to overpay for the assets. We’re in the early innings of this play, but you can now buy shares at a hair over $10 or 40% less than what Carl paid a year ago. Meanwhile, SandRidge has been dramatically de-risked and transformed since he bought his shares.

So what do you get at SandRidge today? Strip out severance for old management and the costs of the proxy fight, normalize cash flows for the current cost structure, and I think you’re paying somewhere between one and two times cash flow for a company with no debt, and a pretty unlimited pipeline of drilling locations. Now, I get that shale wells rapidly decline and that you need to re-invest in order to keep production constant. However, they’re hitting it out of the park in Colorado with IRRs of over 100% and they still have substantial cash flow from their Miss Lime assets that everyone seems to despise.

The company trades at just 1.6x EV/EBITDA… That is ridiculously cheap. Here’s Kuppy’s writeup on the stock, give it a read.

Quote I’m pondering —

Madness is the exception in individuals but the rule in groups. ~ Friedrich Nietzsche

That’s it for this week’s macro musings.

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.