Hope you had a great weekend and a good start to your week. Isn’t it funny how a ~8% drop in the S&P feels like nothing after March? Just another day in the markets.

There’s people saying we’re in a recession/depression. There’s people saying we’re in the early stages of a bull market. Whichever side you’re on — it doesn’t matter. All that matters is finding great companies that trade at crazy discounts to intrinsic valuation, ripe for a breakout.

Speaking of new ideas … our latest podcast is loaded with em’!

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- Bill Ackman Writes Blank Check

- The Math of Value & Growth

- Lemonade S-1 Analysis

- Accounting For Intangible Assets

This newsletter has a mix of in-depth analysis, company research and investor news. Let’s get after it.

—

June 17th, 2020

Chart Of The Week: I’m featuring the chart below in this week’s Premium Breakout Alerts Report. I’ll give you a few hints:

-

- Well-known company

- Robinhood favorite

- Technology-based

I really narrowed down the list, didn’t I? Anyways, it’s a beautiful cup-and-handle pattern.

__________________________________________________________________________

Investor Spotlight: Bill Ackman Cashes In (Again)

GIFs by tenor

GIFs by tenor

Bill Ackman officially signed a lease in the pages of this newsletter. We can’t get rid of him! This week he wants to issue a Special Purpose Acquisition Company (SPAC). A big one: $1B.

There’s a lot we don’t know about the Ackman SPAC. But for those unfamiliar with SPACs, check out this slide deck here.

In short, a SPAC is a holding company that has a certain amount of money to acquire an existing business to take public. The SPAC has ~2 years to find a candidate. Often, early SPAC investors have no idea what business the company will buy.

SPACs also come with warrants or rights. Think of these as call options on the future of the SPAC and the acquired company.

SPACs in Vogue

The article also mentions the popularity of SPACs in 2020. Here’s some stats:

-

- SPACs have raised $9.8 billion through U.S. IPOs so far in 2020

- SPACs have been behind some of the most high-profile public listings of the last 12 months, with the likes of space tourism company Virgin Galactic Holdings, sports betting platform DraftKings Inc and electric truck maker Nikola Corp

- Social Capital CEO Chamath Palihapitiya and Starwood Capital Group CEO Barry Sternlicht each raising hundreds of millions of dollars for them this year.

Flaming Dumpster Fires

As one Reddit user once said (and I’m paraphrasing), “SPACs are large dumpster fires full of s**t.” And they’re not entirely wrong. We don’t have a large database of SPAC return research. But what we do have isn’t good.

Anytime you find a place people call “dumpster fires”, stop. Remember the words of prophet Michael Burry: “If my initial reaction to a stock is ‘ick’, I dive deeper.”

Here’s two great resources for further SPAC Research (not sponsored):

__________________________________________________________________________

Movers & Shakers: Accounting For Intangible Assets

GIFs by tenor

GIFs by tenor

Last week we reviewed stock-based compensation and its effect on underlying profitability. This week we’re staying in the weeds with intangible assets. Let’s dive into FootNotesAnalyst’s review of intangible assets and their effect on traditional value metrics.

Value Factors: Assets-in-place vs. Cheapness

The article argues that there’s two ways to measure the value characteristic of a stock (from the article):

-

- Assets-in-place: “The value of a company can be thought of as the sum of the value derived from business activities already in place and the current value of expected future investment and growth opportunities. Furthermore, the value of existing business activities can itself be thought of as the current balance sheet value of (net) assets plus the added value derived from the way those assets are utilised i.e. their profitability.”

- Cheapness: “To further confuse matters value can also be regarded as the characteristic of cheapness based upon one or more valuation metrics. This obviously overlaps with the idea of assets-in-place but the emphasis is on selecting stocks with low multiples rather than necessarily high assets-in-place.”

Indices and algos use book-to-price as the standard value “cheapness” factor. But there’s three issues with that approach (from the article):

-

- Measurement: “Financial reporting uses a mixed measurement model with some assets reported at cost and others at current value. In addition, measurement choices available to companies mean that comparability within asset classes may be affected.”

- Goodwill: “While goodwill is regarded as an asset for financial reporting purposes, the question for investors seeking to identify ‘value’ stocks is whether it is an asset-in-place and, if so, whether balance sheet values are relevant.”

- Intangible assets: “As we explain above, the recognition of intangibles is generally limited and often inconsistent, primarily due to the very different treatment of those assets that are purchased and internally generated.”

Why You Can’t Trust Stated Book Value

Intangible assets highlight another important aspect of value investing: you can’t trust book value. There’s two instances where book value matters: asset-heavy firms and financial institutions. After that, you shouldn’t use it.

The article offers a perfect explanation why (emphasis mine):

“The problem is that, in effect, a cash rather than an accrual basis is used to account for them. Investment in intangibles produces an expense in the current period but the benefit may predominantly impact profit in future periods. Equally, past investment in unrecognised intangibles that was expensed in prior periods may now be contributing to higher profits, but there is no amortisation charge to reflect the ‘consumption’ of the asset.”

A great way to think about this is through software-based businesses and customer acquisition cost. Businesses expense the acquisition cost of a customer upfront. But recognize revenue and profits in the future. This dichotomy between expense and revenue timing creates opportunity for individuals. Devastations for quants and algos (emphasis mine):

“However, if your approach to investment and portfolio construction is based on ‘factors’, ‘styles’ and data-driven analysis then intangible asset accounting may be much more of a problem, particularly if you favour (or wish to avoid) ‘value’ stocks.”

Hidden Value Stocks

Inverting the intangibles problem we can ask ourselves, “how much are quants and indices under-reporting stated book equity for companies?” Remember, the lower the stated book value, the higher the P/B ratio. Which leads to fewer value stocks and more growth stocks.

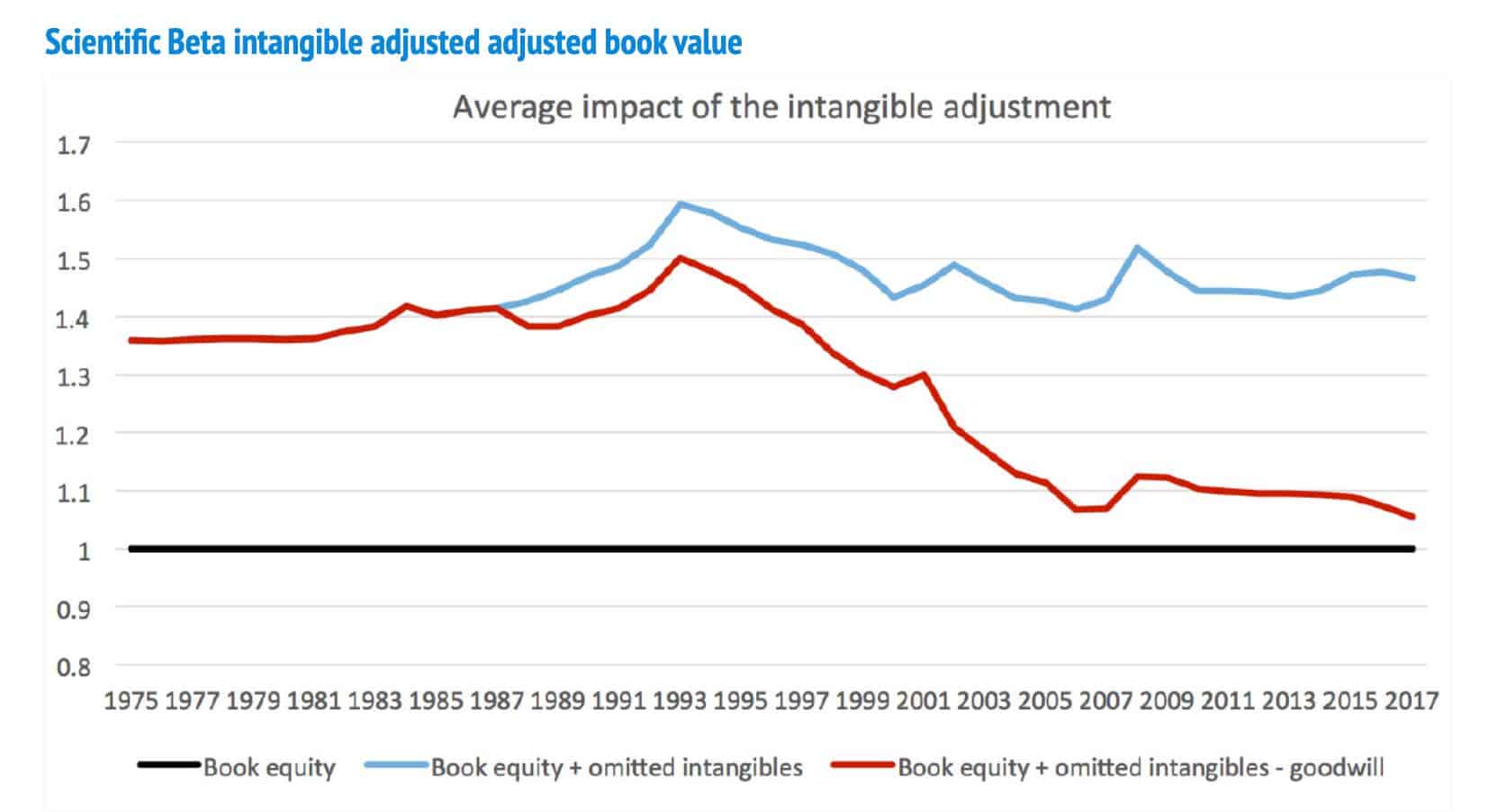

Scientific Beta tried to solve this problem by adjusting for intangible assets and removing goodwill. Here’s their results:

The study normalized standard book equity at 1. As the graph shows, adding omitted intangibles significantly increases the company’s book equity.

Note goodwill’s impact on book equity, too. Removing goodwill almost balances the gains from intangibles by 2017.

How To Use This Information

We threw a lot at you. The next logical question is, “great, how do I use this to get better?” There’s a few ways:

-

- (Unless analyzing asset-heavy/financial businesses) Don’t pay attention to book value and ROE

- Remove P/B from your stock screens

- Screen for companies with high P/B as a way to find hidden value stocks

__________________________________________________________________________

IPO Of The Week: Lemonade’s S-1 Analysis

I like combing through new and upcoming IPOs. Not because I think there’s tons of bargains in the mix. But because I learn about new businesses and new revenue models. It’s also one of the few places you can gain an information edge in markets.

One such potential IPO is Lemonade, Inc (ticker to come LMND). I found the idea from Byrne Hobart’s Substack newsletter. Byrne does a great job analyzing the bull case and risks as Lemonade hits public markets. You can also read the entire S-1 filing here.

What is Lemonade, Inc.?

LMND is a fully-digital renters and homeowners insurance company. Their mission is to quote, “Harness technology and social impact to be the world’s most loved insurance company.” How Silicon Valley of them.

The company’s goal is also simple: capture early/first-time insurance users at the beginning of their life-time spending cycle. Hold on as they earn more money and buy bigger houses. Add high-margin insurance products like pet and life as their customer matures.

Insurance is a great business. That’s why I’m interested in Lemonade. Let’s see what Byrne has to say.

A Bundle of Bets

Byrne claims Lemonade is a bundle of three bets:

-

- The theory is that small insurance claims are a market for lemons.

- The big tailwind is that reinsurers are overcapitalized.

- Lemonade thinks the industry doesn’t acquire enough customers online, and that this locks them out of low-premium policies.

Entry Market & Risk Mitigation

Byrne reaffirms Lemonade’s go-to-market strategy saying, “Lemonade’s entry point into the market is renter’s insurance.” He then describes how customers enact with the business (emphasis mine):

“[Lemonade] underwrite[s] through a chatbot, accept[s] claims through another chatbot, and offload[s] the vast majority of their risk to reinsurers through one- to three-year contracts.”

Everything’s done through an AI-powered chatbot. Straightforward enough.

How To Measure User Behavior

Byrne later explains how Lemonade wants to analyze their customers’ behaviors at three separate time periods:

-

- When they get a customer, to know how much to charge them

- When they get a claim, to know whether or not it’s legitimate.

- When Lemonade upsells or cross-sells.

That third period, “when Lemonade upsells or cross-sells” is vital to the bull case, as Byrne notes (emphasis mine):

“Their renter’s insurance product is incrementally cost-competitive only because overhead dominates their competitors’ costs, and Lemonade’s cost structure is more fixed. But in 2019 they spent $175m in operating expenses to produce $13.1m in gross profit, which is not a sustainable model. At their current operating cost run-rate, they’d break even on renter’s insurance if they had 8.6 million customers, or 20% of all households that rent.”

Why Now?

Lemonade burns through cash and reports negative net losses. Today’s market loves that kinda stuff! In seriousness, Byrne thinks the IPO is more a marketing strategy than anything else:

“My suspicion is that this is yet another marketing channel. Lemonade doesn’t need cash, but they do need attention. IPOs tend to increase name recognition, and the daytrader market is in the middle of a bubble.”

Regardless, I’m going to read the entire S-1 and learn all I can about their new-wave insurance model. Who knows, maybe they’ll crash post-IPO and present an opportunity!

__________________________________________________________________________

Whitepaper Of The Week: The Math of Value & Growth

GIFs by tenor

Michael Mauboussin’s latest work, The Math of Value and Growth made it into this week’s letter. As always, read the whole piece. It’s short (13 pages) and full of knowledge bombs. Here’s a few of my favorite snippets (emphasis mine):

-

- “But in recent decades investments have shifted in form to intangible assets, which are expensed on the income statement and are typically absent on the balance sheet (except for when one company acquires another). This is important because companies that invest heavily in intangible assets and have high returns on those investments often produce poor profits, or may even lose money. As an investor, you want that kind of company to invest as much as it can. The income statement looks bad, the balance sheet looks better, and the value creation looks great.”

-

- “The fundamental principle is that growth only adds value when the company earns a return on its investment that is above its cost of capital. The higher the return, the more sensitive the business is to growth. Growth is of no economic significance if a company’s returns are equivalent to the firm’s cost of capital. As a consequence, companies should focus not on growth per se but on value-creating growth.”

-

- “Investors often calculate the P/E multiple using the current price and next year’s earnings. As a result, they sometimes believe that the market overreacts to what appear to be modest changes in the near-term earnings. But if expectations for the trajectory of growth really do shift down, the large apparent drop in the P/E multiple is completely justified”

-

- “Here, next year’s earnings are revised down by just 2.6 percent, but the warranted P/E multiple is 25.3 percent lower. When ROIIC’s are well above the cost of capital, the value of the business is highly sensitive to changes in the growth rate of NOPAT.”

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!