Alex here with your latest Friday Macro Musings…

As always, if you come across something cool during the week, shoot an email to alex@macro-ops.com and we’ll share it with the group.

Latest Articles/Podcasts/Videos —

The Fed Put Is Real and China Stimulates — Alex updates us all on China’s surprise stimulus and the Fed’s epic flip from hawk to dove.

Macro Ops Podcast: Alex, Tyler, Chris, and Mr. B — Chris hosts a monster 2.5+ hour Macro Ops roundtable with Alex Barrow, Tyler Kling and Mr. B.

Articles I’m reading —

I don’t recall how I came across this piece (Twitter maybe?) but it’s a terrific interview in Logic Magazine with an “Anonymous Algorithmic Trader” about the trends, dangers, and future of quantitative finance. Anybody who is anybody is now using “machine learning, AI, and BIG data” to run their hedge fund. Why you ask? Well, because it’s the future… Or, at the very least, it helps one raise large amounts of AUM which is really what this game is all about, at least for most.

One of my favorite sections from the interview was when the Algo Trader covered a number of the dangerous fallacies embedded into practically all machine learning/AI/quant trading models — this is a subject near and dear to our heart and one that we covered in our latest wide-ranging (and wine-fuelled) group podcast discussion (link here). But, anyway, here’s a clip from the interview after Mr. Anonymous was asked about what new vulnerabilities are being introduced to the financial system from the rising popularity of quant investing (emphasis by me).

The way that mortgage-backed securities precipitated the financial crisis is very much applicable here. One of the fallacies behind that phenomenon was the assumption that the world would behave in the future the way it had in the past. For instance, housing prices would go ever upwards.

That fallacy is intensified in the case of quantitative investing, because all quantitative models use historical data to train themselves. As these techniques become more widespread, the assumption that the world will behave in the future the way it has in the past is being hard-wired into the entire financial system.

Another fallacy in the lead-up to the financial crisis was the assumption that financial markets were so efficient that participants didn’t need to do the underlying work to figure out what the securities were actually worth. Because you could rely on the market to efficiently incorporate all available information about the bond. All you need to think about is the price that someone else is willing to buy it from you at or sell it to you at.

Of course, if all participants believe that, then the price starts to become arbitrary. It starts to become detached from any analysis of what that bond represents. If new forms of quantitative trading rely on assumptions of market efficiency—if they assume that the price of an instrument already reflects all of the information and analysis that you could possibly do—then they are vulnerable to that assumption being false.

Give it a read. Here’s the link.

I don’t think we’ve shared this one in our Friday Macro Musings (if we have, then sorry for being repetitive) but Mauboussin put out a killer research paper the other week titled “Who Is On The Other Side?” which delves into the following problem-set:

If you buy or sell a security and expect an excess return, you should have a good answer to the question “Who is on the other side?” In effect, you are specifying the source of your advantage, or edge. We categorize inefficiencies in four areas: behavioral, analytical, informational, and technical (BAIT).

Anything Mauboussin puts out is worth a read but this one, in particular, is a must… Here’s just one of the many great tidbits from the paper as well as the link to the full thing (link here).

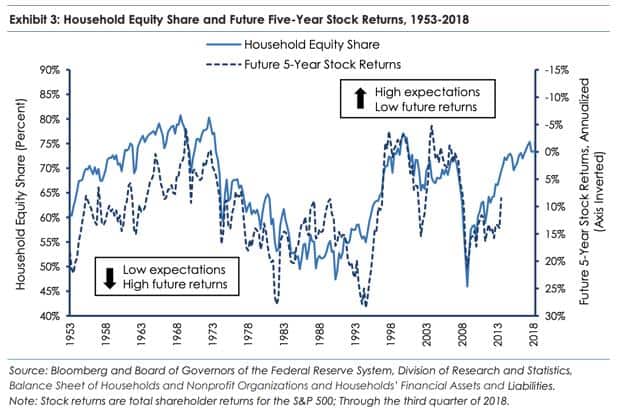

Overextrapolation. Overextrapolation, the excessive projection of recent experience, is one of the key ideas behind the psychology of belief formation. For example, financial economists have shown that investor expectations for future stock returns in the next year are highly correlated with returns in the past year. Exhibit 3 shows the percentage of household equity and fixed income investments that are allocated to equities and subsequent five-year stock market returns. Investors expect high returns after realizing high returns and expect low returns after realizing low returns.

Because stock prices are more volatile than corporate earnings, valuations tend to be higher following a period of strong price advances and lower subsequent to price declines. In contrast with expectations as the result of overextrapolation, high valuations are associated with low expected returns, and low valuations with high expected returns. This relationship holds for asset classes beyond stocks, including bonds, real estate, and sovereign debt.

Avoiding this type of overextrapolation demands the ability to “disregard mob fears or enthusiasms and to focus on a few simple fundamentals.” Seth Klarman, founder, chief executive officer, and portfolio manager of The Baupost Group, captured the concept beautifully when he said, “Value investing is at its core the marriage of a contrarian streak and a calculator.” The “contrarian” part demands an examination of the other side of the popular view. The “calculator” part ensures that valuation is sufficiently extreme to generate excess returns.

A contrarian streak and a calculator. I love that…

Also, here’s some links to a number of great quarterly writeups that have recently hit the webs:

- Coho Capital Q4 Shareholder Letter: Jake Rosser, Managing Partner at Coho, always puts out an insightful letter and this quarters is no different. Jake pitches the value case for Netflix (NFLX) and gives a masters class on the unique business advantages of combining subscription economics with massive scale.

- KKR “Global Macro Trends”: Tons of great macro charts in here with a focus on slowing global growth, changing Chinese trade dynamics, and a structurally/politically weak Europe.

- Crescat Capital Q4 Shareholder Letter: Crescat is bearish. I mean reeeaal bearish. I don’t necessarily agree with their views but I appreciate their point of view and I always enjoy hearing what those on the other side of the trade are thinking.

- Broyhill Asset Management Q4 Shareholder Letter: A measured take on the market along with an update on some of their core holdings (DLTR, OAK, MCK, WBA, AGN). They also use one of the more interesting analogies I’ve heard to describe the deflating of an asset bubble, which is:

“They say that gradually letting the air out of a bubble is like trying to gradually let a fart out at a cocktail party. It’s a risky move with a blemished track record—for party-goers and for the Fed. As a result, like those uncomfortable moments at the cocktail bar, bubbles have a tendency to linger longer than anyone expected and surprise everyone by how magnificently they burst.”

Charts I’m Looking At—

China’s A-shares market is up 26% ytd. Not a bad start to the year, though the market still needs to rally another 27% just to get back to its most recent high reached in 18’. Either way, Nomura research says the Chinese market is getting frothy and investors there are now “euphoric”, at least according to Nomura’s sentiment indicators.

Euphoric investors don’t typically bode well for the short/intermediate returns of the market in which investors are so worked up in a frenzy over. But, if you pull back some, Chinese stocks and tech stocks, in particular, have taken quite a drubbing over the last year (see below chart from KKR). Does this mean we should sell Chinese tech stocks now and buy later? or hold now and buy more later? or do neither and fuggedaboutit?

I don’t know. I’m torn to be honest. On the one hand, some Chinese tech companies are amazing innovators and are dominant businesses. On the other hand, companies like BABA and Tencent are really just corporate arms of the CCP and are vulnerable to the whim and wishes of the Party. And I’m not sure how I feel about that.

Podcast I’m listening to —

After a brief hiatus, I’ve found myself getting back into podcasts again. And over the last two weeks, I’ve listened to a number of different ones but two that really stood out for me were both Tim Ferriss productions. One was his interview with Shopify (SHOP) CEO Tobi Lutke (link here) and the other was with Business strategist and all-around Polymath, Jim Collins (link here).

From the Lutke interview, two things really stood out at me, or rather three things (1) was the best definition of hell I’ve ever heard which is “The last day you have on earth, the person you became will meet the person you could have become” (2) Lutke’s discussion on his uncomfortableness with being comfortable because being comfortable means stasis (ie, not growing) and (3) I really wish this interview could have come out in early 2015 so I could’ve learned how impressive Shopify’s CEO is and then bought in its IPO for around $26.

And then the Collins interview is just all-around fantastic. He has this habit of tracking where his time is spent throughout his day and then assigning a number evaluation to each day (-2 for a crappy day and +2 for a great one). This has helped him to quantitatively optimize his time usage and ergo his happiness. The result is he spends a lot more time doing distraction free creative work and less time caught up in shallow busy tasks. I’m thinking of implementing the same.

Trade I’m Considering—

Tyler wrote about Nintendo I think in last week’s Musings. We’ve been digging into this one and really like what we see. @HardcoreValue shared a good pitch deck outlining the long thesis on the company this week (link here).

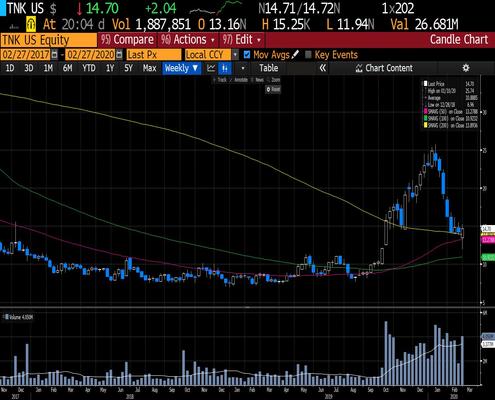

On an unrelated note, another area of the market that I’m looking at is Shippers. Below is a chart of the Invesco Shippers ETF (SEA) which has been in a bear market since its inception nearly 9-years ago.

Kuppy, who’s behind the excellent investing blog Adventures in Capitalism, has been pitching the long case for shippers for a few months now (here’s a link to his latest).

The bull thesis essentially boils down to this:

- Shipping stocks are insanely cheap with many selling for less than half and even a third of NAV using values from the secondary sale and purchase market. And many of these stocks have stable balance sheets and positive free cash flows.

- Tighter financing and an aging global fleet mean less tonnage coming online and an increasing scrap rate in the years ahead.

- Regulation, particularly IMO 2020, which states that as of 2020 all ships must either use 0.5% sulfur or lower fuel or install a scrubber to remove exhaust. There are a number of ways for shipping companies to adhere to this rule and pretty much all of them are bullish for charter rates and ipso facto shipping stocks.

So we have below asset liquidation valuations, positive future trend in supply/demand dynamics, and a coming near-term catalyst to further drive profitability. Throw in a decade long bear market and a completely forgotten/disregarded sector and you’ve got yourself a pretty decent trade setup. You know, the whole Klarman contrarian streak and calculator thing works out pretty well here.

I’m going to continue digging into this space and will be putting out a report in the coming week to those of you in our group.

Quote I’m pondering —

I am by nature warlike. To attack is among my instincts. To be able to be an enemy, to be an enemy—that presupposes a strong nature, it is in any event a condition of every strong nature. It needs resistances, consequently it seeks resistances…. The strength of one who attacks has in the opposition he needs a kind of gauge; every growth reveals itself in the seeking out of a powerful opponent—or problem: for a philosopher who is warlike also challenges problems to a duel. The undertaking is to master, not any resistances that happen to present themselves, but those against which one has to bring all one’s strength, suppleness and mastery of weapons—to master equal opponents. ~ Friedrich Nietzsche, 1844–1900

A GREAT life requires GREAT opponents, GREAT challenges, and GREAT obstacles. It’s these powerful external pressures that force us to grow, adapt, and evolve. Stress and struggle is our greatest teacher and the most valuable gift we can receive. Seek out the hard and sharp edges of life and turn from the siren calls of the crowded comfortable complacency of normalcy…

That’s it for this week’s macro musings.

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.