Murata is the world’s largest producer of multi-layer ceramic chips (MLCCs) with over 40% market share. The company cranks out over 150 billion MLCC pieces per-month. The next closest peer, Samsung Electric (SEMCO) produces 100B pieces per-month.

Here’s why we’re interested in Murata now: The company’s main revenue source (MLCCs) will see a demand explosion from two sources: electric vehicles and 5G telecommunications.

The company owns the entire manufacturing process from start to finish, vertically integrating the supply of raw materials, sheet-casting, sintering, processing and finishing and inspection/packaging. They do all this in-house, allowing them to process, create and deliver customer orders faster than competition.

The company owns the entire manufacturing process from start to finish, vertically integrating the supply of raw materials, sheet-casting, sintering, processing and finishing and inspection/packaging. They do all this in-house, allowing them to process, create and deliver customer orders faster than competition.

Murata’s dominant market share position allows it to invest more money in R&D than its competitors while keeping R&D expenses a lower percentage of total revenue. As an example, Murata will spend $1B on R&D this year compared to SEMCO’s (MLCC competitor) $416M R&D investment.

It also doesn’t hurt that the company’s long-term stock chart is tantalizingly bullish (see below):

These facts below should get anyone excited about the coming MLCC demand boom (emphasis mine):

-

- The required number of automotive MLCCs increased from 3,000 units in 2012 to 8,000 units in 2018

- Battery EVs (BEV) require much more MLCCs than internal combustion cars. They are expected to require around 30,000 MLCCs.

- TESLA’s Model 3 contains over 9,000 MLCCs and their Model S & X each have over 10,000 MLCCs.

- Murata predicts the MLCC usage of smartphones in 2024 will be 1.5 times more than that in 2019.

- For instance, 5G smartphones which support sub-6GHz frequency band will need 10~15% MLCC more than those of 4G smartphones; and 5G smartphones which support mmWave will need 30~35% MLCC more than those of 4G smartphones. In estimation, each 5G smartphone will need more than 1000 units MLCC in the future.

It’s clear MLCCs will be vastly more important in five years than they are now. And we’re going to need a heck of a lot more of ‘em. In turn, MLCC producers, most notably the world’s largest, should be worth significantly more five years from now.

If that’s not convincing enough, The Global and China Multi-Layer Ceramic Capacitor (MLCC) Industry Report (2019 to 2025) expects MLCC supply to reach 6.1T/year by 2025. That’s six times higher than today’s production levels!

This essay will review the following:

-

- What is an MLCC and Why Is It Important?

- Murata’s Founding & Culture of Innovation

- Murata’s Growth Story: Betting on EV & 5G

By the end of the essay, you’ll know what an MLCC is, why it’s important, where future demand will surface, and why Murata is the best-positioned company to capture that demand.

What Is An MLCC and Why Are They Important?

Multilayer Ceramic Capacitors (MLCC) are devices that store energy in the form of an electric field between layers of ceramic and metal material. Think of MLCCs like an Italian sub. Each layer consists of alternating genoa salami and capicola. MLCCs are also used to differentiate between high/low frequencies.

They were born out of necessity in Germany during the 1920s. The Germans ran out of the material, Mica. Luckily, they had spare porcelain (ceramic derivative) and tried it. The rest as they say is history.

MLCCs main benefits include the best high-frequency performance of any capacitor, as well as better stability in high temperatures. They also have a high voltage threshold, meaning they can withstand heavy electrostatic discharge without damage. Both of these features come in handy with electric vehicles (we’ll discuss that later).

The main disadvantage is smaller capacitance (the ability of a system to store an electric charge) per volume. MLCCs present a tradeoff between higher capacity for temperatures and voltage at the expense of electrical charge storage.

Two classes of MLCCs: Class I and II

Class 1 capacitors work best when high stability and low loss is required.

Class 2 capacitors have a higher capacitance per volume with thermal stability of typically 15%, so are better suited for less sensitive applications (source: JJSManufacturing)

They come in surface-mounted and leaded versions. Surface mounted means they “mount” surface boards (like CPUs and processors). Leaded capacitors have an epoxy coating and wires to assist in conduction.

There’s an MLCC In Every Device You Use

Chances are you use devices that use MLCCs every single day. Ceramic capacitors are the most produced capacitors in the world. Manufacturers crank out 1 Trillion of these microscopic devices every year.

They’re used in everything from smartphones to EV batteries to bluetooths and camera sensors.

Point to an electronic product or device and odds are, you’ll find an MLCC in it.

Why Are MLCCs Important?

MLCCs are inexpensive, extremely reliable and can withstand high voltages, frequencies and temperatures. This makes them the go-to capacitor for consumer electronics, 5G telecommunications and EV components.

They’re also incredibly scalable, with the smallest MLCC the size of a grain of sand.

As more devices need higher computing power at the edge, OEMs will look for the smallest MLCCs available. The smaller the MLCC the smaller OEMs can make their devices (see: wearable smart watches).

But perhaps the biggest reason why MLCCs are important is their ability to perform in EV batteries/cars and 5G smartphones and base stations. These two categories will drive MLCC growth for the next 5-10 years.

There’s one company that dominates the MLCC market: Murata Manufacturing. But before we understand where Murata sits in the current market, we need to understand the history of the company and its cultural fabric.

The Birth of Murata Manufacturing: The Story of How One Man Turned $102K Into A $14B Empire

Akira Murata founded the company in 1944 as a personal venture. At the start it was merely a small, family-run operation.

The company originally specialized in basic capacitors to solve the needs of a small number of customers.

But Murata wanted more. He wanted to help more customers and find new business. In 1947, he asked one of his school professors, Mr. Tanaka about a new ceramic product called barium titanate. Before discovering barium titanate, Murata used titanium-oxide. Titanium-oxide boasted a dielectric constant of 70-100. Barium titanate on the other hand had a whopping 1,000 – 10,000 constant.

Murata reorganized the company three years later with $102K of his own money (adjusted for inflation). It was also at this time Murata built his first factory outside Kyoto. The story on how he found the land to build the factory is fantastic.

In 1950, Murata received a call from a former work colleague at the Kyoto Research Institute, Mr. Senda. Senda happened to be the director of a ceramic laboratory. Senda showed Murata a large plot of land with massive pottery-stone reserves (i.e., ceramics).

In 1950, Murata received a call from a former work colleague at the Kyoto Research Institute, Mr. Senda. Senda happened to be the director of a ceramic laboratory. Senda showed Murata a large plot of land with massive pottery-stone reserves (i.e., ceramics).

This moment sparked Murata’s vision of factories, employees and subsidiaries across Japan.

Today, Murata generates over $14B in revenue and $2B in operating income. All that from a $102K investment. That’s a cool 19,607% return on Murata’s initial capital. Not bad.

So how did Murata go from a single factory to 77,00 employees and 150B capacitor production per month? To answer that question we have to understand the company’s culture and philosophy.

Murata’s Founding Philosophy: Pursuit of Originality & Moving First

Electronic component manufacturers are commodity businesses. They win by offering the lowest priced product to their customers. In doing so, they hope to gain market share at the expense of operating profit margins. Make it up in volume, right?

Murata’s competitive advantage is simple: they offer products that their competitors don’t. They’ve done that since their founding in 1950. The company notes in its 2019 report: “Murata offers products that competitors do not offer, to people that need them. This marked the start of Murata’s ‘pursuit of originality,’ which has led to originality across all aspects of our business, including our technology development capabilities, manufacturing capabilities, networks and organizational cooperation to integrate these elements.”

These strong competitive advantages took over half a century to solidify. And they were built on the back of solving a customer’s specific problem. Akira was the master of solving specific problems. He did things that didn’t scale (custom-building parts vs. mass production) to win the trust and adoration of customers.

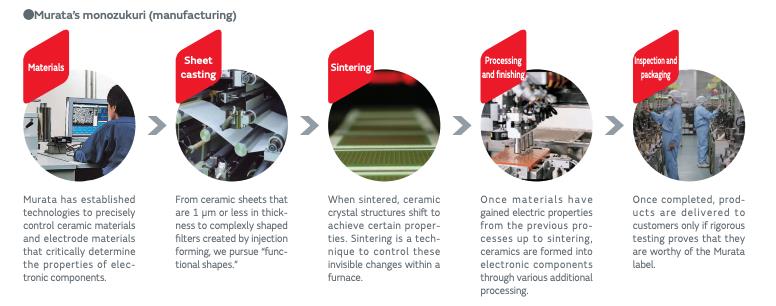

This Pursuit of Originality is best shown in the company’s R&D segment, monozukuri manufacturing process and dogged determination to do everything in-house.

By keeping everything in-house, Akira could tinker with new raw materials, diagnose different manufacturing processes and create unique orders for specific customers. All the while keeping costs down and completion times quick.

Murata’s early success allowed it to scale quickly while reinvesting most of its profits into R&D to develop new products. This paved the way for Murata’s First Mover Advantage. Something it’s kept since its founding.

A History of Moving First

Murata’s history is earmarked by first-mover advantage. From its beginnings in 1940, the company recognized technological shifts and developed products for those rising industries. Murata was first-to-market with Japan’s first mass produced temperature compensating barium titanate ceramic capacitor for radios. That was five years after the company’s founding. Yet they saw the technological shift happening in radio during WWII.

The company executed during the 50s and 60s. They developed ceramic capacitors and semiconductors for black-and-white TV in the 50s and commercialized ceramic filters during the color-TV boom in the 60s.

Next came the 70s with the CB transceiver boom in the US and expanded use of audio-visual equipment in cars. Murata launched GIGAFIL dielectric filters for microwaves, commercialized ceramic resonators, chip ferrite beads and multi-layer LC filters during the decade.

The 90s and early 2000s gave rise to the Internet, miniaturization of mobile phones and spread of PCs. This led Murata to commercialize bluetooth modules, develop 0.4×0.2mm multilayer ceramic capacitors and MEMS gyro sensors.

Today, Murata continues to innovate and develop market-leading technology.

Murata’s scale is one of the many competitive advantages it has over its peers. It’s helped the company deliver 16.5% CAGR over the last decade (362.5% return).

As we’ll see in the final section, Murata is the best-positioned company to capture the positive MLCC demand shock from Electric Vehicles and 5G telecommunications technology.

Murata Today, Murata Tomorrow

Despite operating in a cyclical industry, Murata’s financial results are impressively consistent.

Since 2004 the company’s averaged 35%+ Gross Margins, 12-18% Operating Margins and reported only one losing year, 2008. During that time they’ve grown revenue from $4B to $14B, operating income from $539M to $2.24B and FCF from ~$400M to ~$900M.

Given those stats, one would expect to pay a lofty multiple of EBIT for the entire business. Not quite. At the time of writing, Murata trades roughly 18x NTM EBIT and 3x revenues.

Murata relies on three competitive advantages to keep its top-dog spot in an otherwise commoditized industry:

1. They anticipate market changes and customer needs better than competitors

This goes back to Murata’s early days of solving the needs of its initial customers. The company still embodies this tradition by focusing on their customers’ future problems, and how they can develop technologies to meet those needs.

Murata can do this better than any company in its industry. It’s 92 subsidiaries and thousands of customers provide tremendous insight other companies can’t get. With all these data points, Murata can spot trends and potential product failures before anyone else.

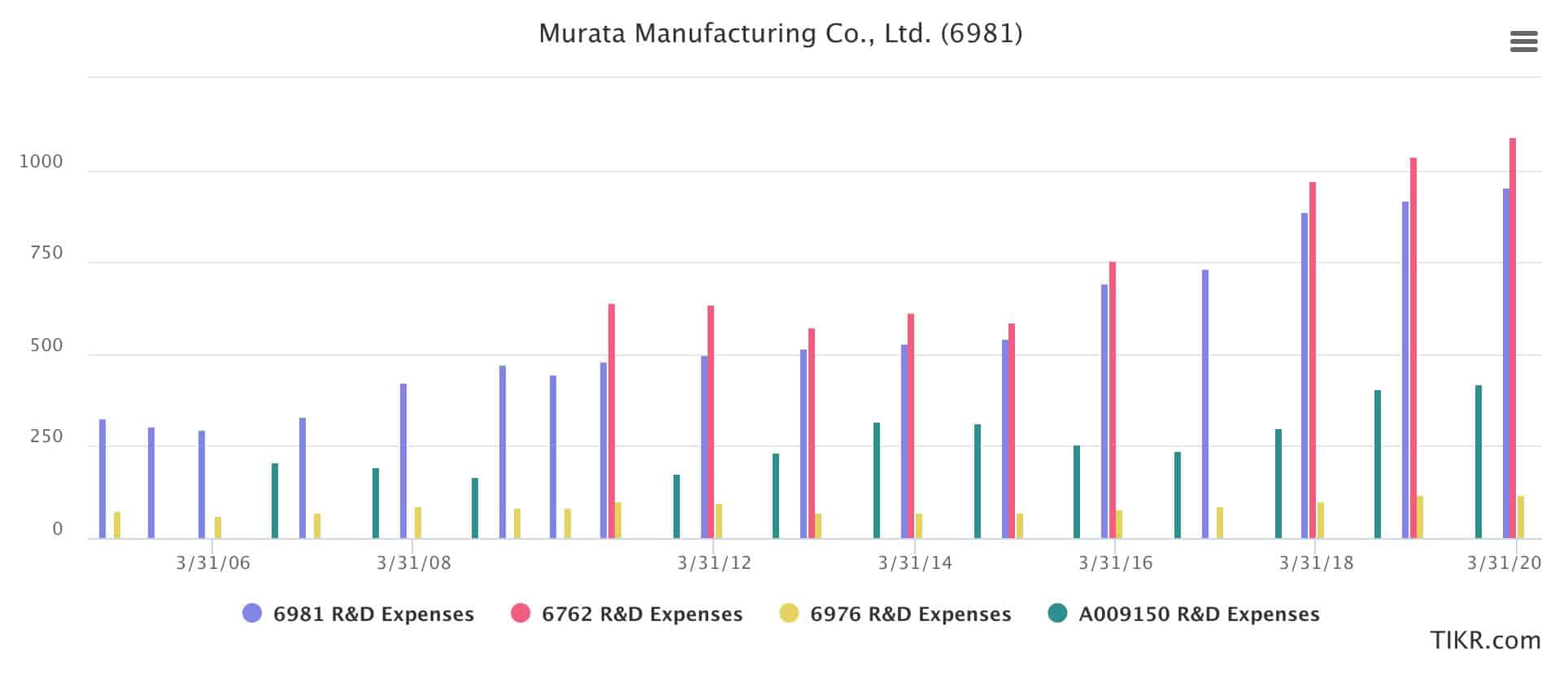

2. Continuous R&D investment enables new product development and IP accumulation

Murata has increased their R&D spend every year going back to 2004. In fact, if trends continue, they’ll invest over $1B in R&D in 2021. This is a massive competitive advantage against its competitors. The sheer dollar amount of R&D capital allows Murata to develop more products and fail more often in search of what works (see graph below).

For comparison, Samsung’s Electronics business (A009150) invested $419M in R&D last year.

Murata generates (on average) 36% of its revenue from new products. And on average the company spends ~6% of net sales on R&D. That’s important because while total R&D investment looks daunting ($1B), it still represents <10% of total revenue.

TDK is the only other company that compares to Murata’s R&D spending (TDK actually spends >$1B in R&D).

TDK is the only other company that compares to Murata’s R&D spending (TDK actually spends >$1B in R&D).

Part of this R&D strategy is to accumulate IP, specifically patents. As of 2018 the company had over 20.500 patent applications globally. That’s good for 29th highest in the world and 10th highest in Japan. It’s tough to compete with a company that has that many patents.

3. Strong Monozukuri Capabilities Enable Timely Supply

Translated literally, monozukuri means “making of things” or “production” in Japanese. But it goes deeper than that. Monozukuri encompasses, “the synthesis of technological prowess, know-how and spirit of Japan’s manufacturing process.”

Translated literally, monozukuri means “making of things” or “production” in Japanese. But it goes deeper than that. Monozukuri encompasses, “the synthesis of technological prowess, know-how and spirit of Japan’s manufacturing process.”

Murata owns the entire manufacturing process from start to finish. The company vertically integrates the supply of raw materials, sheet-casting, sintering, processing and finishing and inspection/packaging.

Here’s Murata’s Director of Components discussing the power of Monozukuri (emphasis mine):

“A major factor in acquiring this high market share is the fact that we can complete everything from development to manufacturing internally. In other words, everything from ceramic material selection to production facilities and manufacturing process technology is taken care of by our own internal framework. As a result, customer requests can be quickly led forward into development, and products can be supplied at lower cost due to various cost reduction options.”

Murata Today: The Clear Leader in Filters and Capacitors

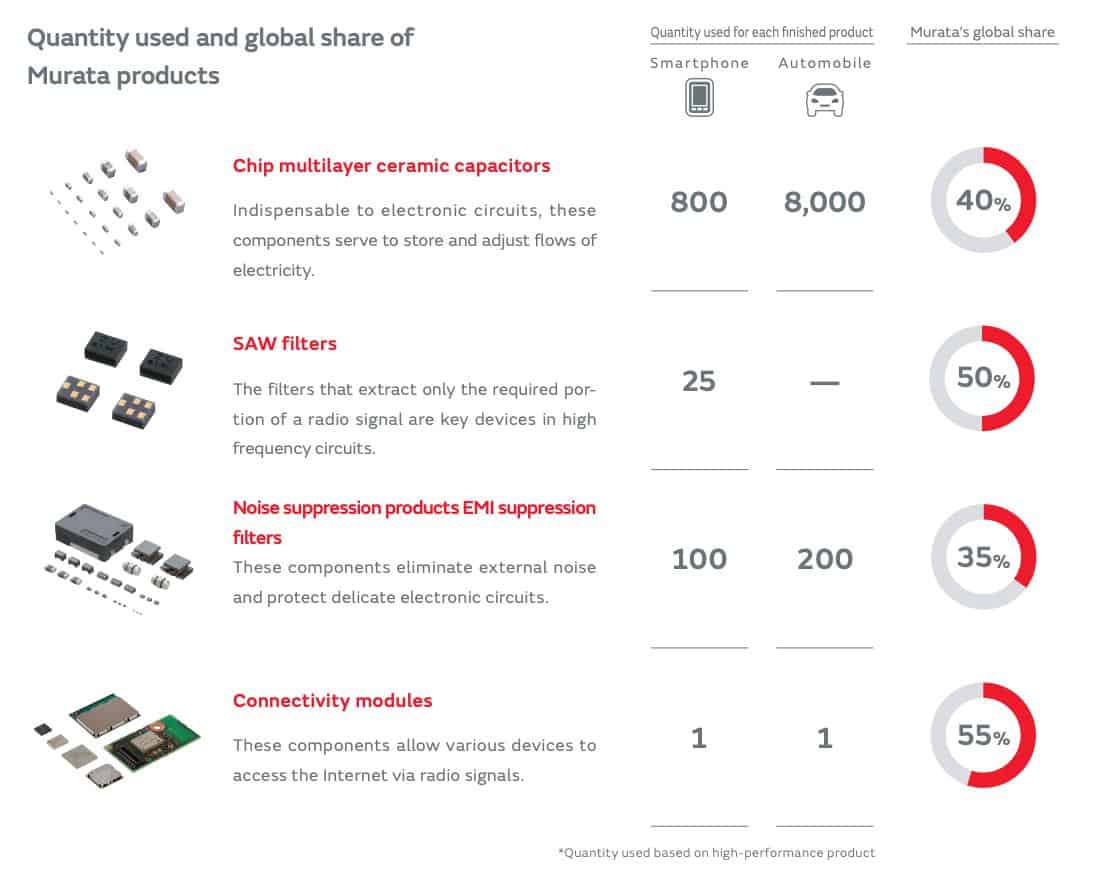

Murata competes on four major products (see global market share %):

-

Chip multilayer ceramic capacitors (40%): Discussed above

Chip multilayer ceramic capacitors (40%): Discussed above- SAW filters (50%): Extract only the required portion of a radio signal. Key devices in high frequency circuits.

- Noise suppression products EMI suppression filters (35%): Eliminate external noise and protect delicate electronic circuits

- Connectivity Modules (55%): Allow various devices to access the Internet via radio signals

The company generates 36.5% of their sales from capacitors, 27.1% from Communications Modules, 25% from “Other”, 8% from Piezoelectric Components and 2.6% from Power supplies and other modules. Broken down by industry the company generates 48% of its revenues from Communications, 16.4% from Automotive Electronics, 15.8% from Computers & Peripherals and 15% from Home & Others.

From a regional standpoint, Murata earned 50.5% of its revenues from China, 16.5% from Asia, 15% from the Americas, 9% from Japan and 8% from Europe.

Murata’s MLCC segment grew 27% YoY and is the biggest factor in the company’s continued success. Let’s see how they plan to capture the coming demand shock.

Murata Tomorrow: A Management Team Pointed In The Right Direction

It’s worth reiterating that the only thing that matters for Murata’s future success is their ability to capture the growing demand for MLCCs in the Automotive and Communications markets via EV and 5G.

Management knows this, too. Both Murata’s President and Director of Components stress the importance of EV and 5G in their 2019 Annual Report.

Here’s what President Tsuneo Murata (the founder’s son) had to say about the automotive industry (emphasis mine):

“We are also seeing changes in the automotive industry that will have a significant impact on the world of electronics. The potential of semiconductors and communication functions will increase through electrification and automated driving, and automobiles are expected to move closer to being considered electronic or communication devices just like smartphones.”

Murata’s Director of Components, Toru Inoue echoed Tsuneo’s sentiment on its two key markets (emphasis mine):

“For 5G, it is naturally important to consider which applications will become mainstream as data volumes increase significantly, but the evolution of smartphones and all kinds of wearable devices will continue to centralize on becoming smaller and thinner and featuring increased functionality, and capacitors will be required to accommodate larger capacities … In addition, EVs, V2X and automated driving require high reliability in products that will never fail even in harsh environments such as high temperatures, high humidity, high voltage and high currents.”

Before diving into valuation, let’s summarize the bull thesis for EV and 5G.

Bull Thesis: Autonomous Driving

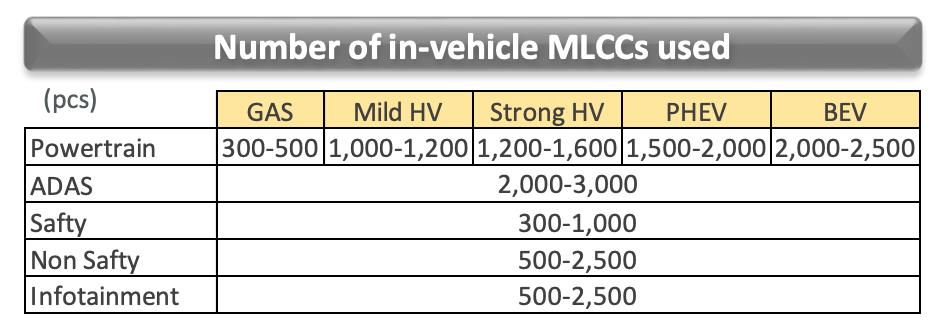

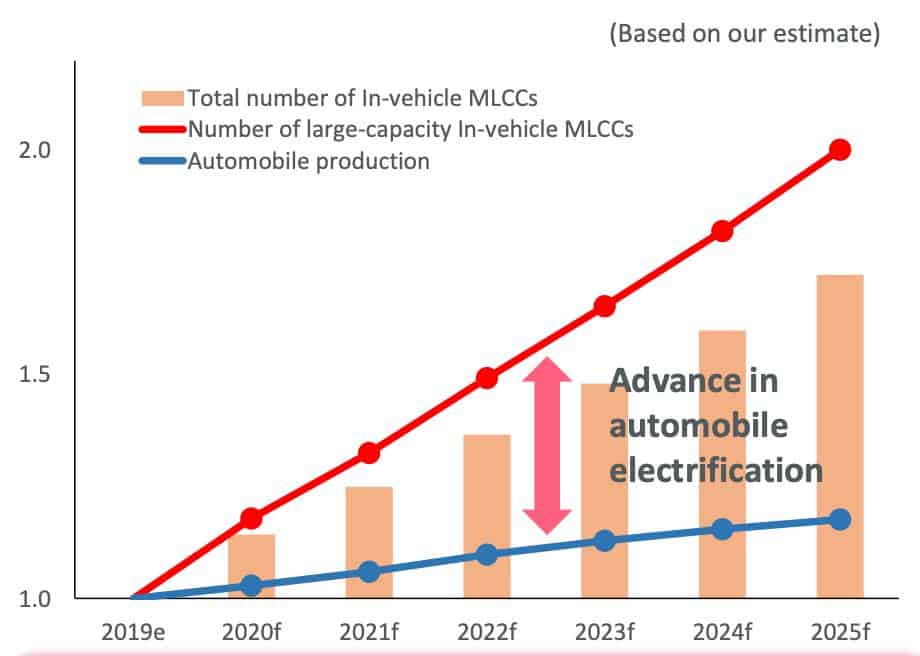

Murata’s MLCCs will meet heightened demands as powertrains move to EV and Autonomous Driving levels increase. The company expects Mild HEV (Hybrid/Electric) powertrains to reach ~15-20M units by 2024. At the same time, Autonomous Driving levels should increase from zero to a majority at Level 1 and Level 2.

This is important because higher levels of EV and Autonomous Driving mean more MLCCs in the car (see graph).

More importantly, automotive sales don’t need to be stellar for Murata to experience automotive MLCC growth (see below):

Imagine how valuable Murata’s Automotive MLCC segment will be when nearly every car on the road is fully electric with Level 3 Autonomous Driving capabilities.

Bull Thesis: 5G Communications

TSR estimates that by 2025 the world will have nearly 1B 5G smartphones in circulation. And remember, 5G smartphones need more MLCCs than LTE and “dumb” phones.

2020 MLCC Demand and Supply Analysis notes that (emphasis mine), “5G smartphones which support sub-6GHz frequency band will need 10~15% MLCC more than those of 4G smartphones; and 5G smartphones which support mmWave will need 30~35% MLCC more than those of 4G smartphones. In estimation, each 5G smartphone will need more than 1000 units MLCC in the future.”

That’s a lot of future MLCC demand.

Murata notes the reasons for increased MLCC demand in 5G phones, including:

-

- More frequency bands

- Higher frequencies

- Advanced communication technologies

- More sensors and cameras

- Larger batteries

The company has the components to meet this demand (see below):

As the largest producer of MLCC’s in the world, Murata is well-positioned to supply the needs of EV/Autonomous vehicles and 5G. But how could they fail? If we look back in five years and we’re wrong, where would the errors lie?

Risks

There’s a few major risks to Murata’s future success:

-

- Rise in Chinese-owned MLCC production

- Increased demand from alternative capacitors like aluminum polymer and tantalum due to high lead times in MLCC supply

- Inability to correctly anticipate changing customer needs/landscape resulting in poor R&D investment (i.e., burning cash)

- Increased losses in the company’s lithium-ion battery business (small part of the company’s operations)

- Economic recession (or COVID-related scare) that delays demand for 5G and EV/Autonomous vehicle investment

Valuation

Murata is a durable, consistent company that cranks out 30%+ gross margins and 12-17%+ EBIT margins like clockwork.

The company generates a 23% Operating Cushion, which isn’t bad. Yet more than 100% of that operating cushion is eaten by working capital. Last year inventory alone sucked 21% of the company’s Operating Cushion, followed by 18% from accounts receivables.

With supply gluts in the past, Murata should experience improved inventory/receivables management. This in turn will help it turn FCF positive over the next five years.

Today’s stock price assumes a few things on an EBITDA exit basis over the next five years:

-

- Average revenue growth of 5%

- 37% average gross margin

- 16% average EBIT margin

- 25% average EBITDA margin

These above assumptions get us $18B in revenues, $4.74B in EBITDA and $2.24B in after-tax operating earnings. A 15x 2025 EBITDA multiple at a 10% discount rate gets us a little over $43B in shareholder value. Which is where we stand today.

If the future demand from EV/Autonomous Driving and 5G are real and materialize, the above revenue growth rate is too low. What happens if we assume Murata grows 13%/year for the next five years?

In that world we get $25.9B in revenue, $6.77B in EBITDA and $3.2B in after-tax profits. Sticking with our 15x multiple on EBITDA gets us $62.5B in shareholder value (~42% higher than current price).

Concluding Thoughts

Today’s price assumes a low-growth environment for a company whose industry tailwinds are just getting started. The market doesn’t realize this, of course, because it’s terrible at predicting exponential growth. Who knows, maybe 13%/year top-line growth is too low? We don’t know.

What we do know is the future looks bright for Murata’s core products and markets. And Mr. Market doesn’t seem to think that.