Alex here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.

Our Recent Articles —

The Global Macro Renaissance: A paradigm shift is coming that’ll bring the resurgence of global macro trading.

The Randomness Of Return Distributions: Being aware of the randomness embedded in the distribution of markets returns keeps us from falling for the ego trap where we mistake skill for luck, or information for noise.

Precious Metals Are Coiling: Precious metal stocks are coiling in a tight pattern and look set for an explosive move in one direction or another.

Articles I’m reading —

I’m a big fan of the Financial Times Alphaville blog. It’s one of the few sites I check daily. And one of my favorite writers there is Matthew C. Klein. He’s a former Bridgewater analyst and always has some interesting takes on markets and economics.

In his latest article he talks about just how bad central bankers are at their ONE job. He’s referring to price stability (i.e. inflation) and the completely ineffective models (like the Phillips curve) central bankers use because they really don’t know what they’re doing.

Even the most basic of things, such as how to measure inflation, seem to trip up our Game Masters. Here’s a snippet from the piece and the link.

There is at best a tenuous connection between what most people think they spend on and what makes up the bulk of the inflation index. About half of what’s in the Fed’s preferred price index is divorced from actual consumer spending decisions.

(Around 21 percent of America’s personal consumption expenditures deflator is health care and pharmaceuticals — even though most of that spending is done by opaque intermediaries rather than price-conscious consumers. About a sixth is “owners’ imputed rent” plus “financial services furnished without payment”. Groceries and energy prices are more affected by changes in global supply and demand for commodities than domestic wage factors. All data come from table 2.4.5 of the National Income and Product Accounts.)

This is pretty cool. Take 10 minutes and complete this survey (link here). Don’t worry about getting the questions right, just be honest in your confidence levels for each question given.

The results will tell you how confident you should be in your confidence levels. The experiment was created by Andrew and Michael Mauboussin (Michael is one of my favorite market thinkers/writers) and they were inspired by the work of Philip Tetlock, of Superforecaster fame (which by the way, is an excellent book and worth reading).

Over a 1,000 people have now taken the test and the results backup what much research has shown, that we humans tend to be way overconfident in how right we are. Here’s some of the reasons given on why that is, in a Medium post written by Andrew (link here).

Confirmation bias is the tendency to reduce our mental costs by focus on information that confirms our existing hypothesis at the expense of information that might provide evidence against that hypothesis. Our default mode for estimating the validity of a hypothesis is seeing how many facts we can think of in support our view, rather than carefully considering alternative views.

Researchers can exploit this disposition to guide their subjects into logical contradictions. For instance, in one experiment people tended to say they were happier when asked, “Are you happy with your social life?” (this question brings to mind positive examples, such as the fun party you went to last weekend) than when they were asked the complement, “Are you unhappy with your social life” (which directs your attention toward less cheerful thoughts) (Kunda et al. 1993).

In the case of True/False questions, we fall prey to confirmation bias by taking “ownership” of the first answer that comes to mind after a split and then favoring evidence that supports it (page 164 of Stanovich, West, and Toplak 2016).

Think the same things don’t affect our judgement in the market and in picking stocks or latching onto a narrative? Think again…

Lastly, here’s Greenwood Investors latest quarterly letter (link here).They’re a value focused hedge fund and on my *must read* list for HF letters. They talk about their holdings, and mention one of their favorite investments of the moment, which is Trip Advisor (TRIP) — which happens to be one of my favorite trades as well, but I’ve been waiting for stronger tape before building into a larger position.

And lastly, for reals…. here’s a fascinating WSJ article on the progress being made on quantum computing, specifically by Google whom appears to be the leader in the field. FYI it’s paywalled, but here’s the gist of the piece (link here).

That dynamism allows qubits to encode and process more information than bits do. So much more, in fact, that computer scientists say today’s most powerful laptops are closer to abacuses than quantum computers. The computing power of a data center stretching several city blocks could theoretically be achieved by a quantum chip the size of the period at the end of this sentence.

That potential is a result of exponential growth. Adding one bit negligibly increases a classical chip’s computing power, but adding one qubit doubles the power of a quantum chip. A 300-bit classical chip could power (roughly) a basic calculator, but a 300-qubit chip has the computing power of two novemvigintillion bits—a two followed by 90 zeros—a number that exceeds the atoms in the universe.

Not everyone is eager for large-scale, accurate quantum computers to arrive. Everything from credit-card transactions to text messaging is encrypted using an algorithm that relies on factorization, or reverse multiplication. An enormous number—several hundred digits long—acts as a lock on encrypted data, while the number’s two prime factors are the key. This so-called public-key cryptography is used to protect health records, online transactions and vast amounts of other sensitive data because it would take a classical computer years to find those two prime factors. Quantum computers could, in theory, do this almost instantly.

Companies and governments are scrambling to prepare for what some call Y2Q, the year a large-scale, accurate quantum computer arrives, which some experts peg at roughly 2026. When that happens, our most closely guarded digital secrets could become vulnerable.

Video I’m watching —

In spirit of the 30th anniversary of Black Monday during the crash of 87’, I went googling for the infamous Trader documentary about Paul Tudor Jones (PTJ). You can watch it here.

The video is an hour of documentary gold and I don’t say that lightly. But PTJ hated it and bought up all the VHS copies after its release. Online versions pop up from time to time but then quickly disappear. So watch while you can!

Book I’m reading —

This week I’ve been reading two books: SPQR which is a history of ancient Rome by the talented Mary Beard and I’ve been revisiting More Than You Know by Mauboussin.

I’m only a quarter of the way through SPQR so I’ll save a review for when I’m finished. But I can say that like Beard’s other work, this book is excellent so far.

I always enjoy reading More Than You Know. It feeds my “curious about everything” needs by looking at markets from a multidisciplinary perspective. The following from the book’s publisher sums up the work well:

“More Than You Know” is a unique blend of practical advice and sound theory, sampling from a wide variety of sources and disciplines. Mauboussin builds on the ideas of visionaries, including Warren Buffett and E. O. Wilson, but also finds wisdom in a broad and deep range of fields, such as casino gambling, horse racing, psychology, and evolutionary biology. He analyzes the strategies of poker experts David Sklansky and Puggy Pearson and pinpoints parallels between mate selection in guppies and stock market booms. For this edition, Mauboussin includes fresh thoughts on human cognition, management assessment, game theory, the role of intuition, and the mechanisms driving the market’s mood swings, and explains what these topics tell us about smart investing.

Here’s a cut from the book:

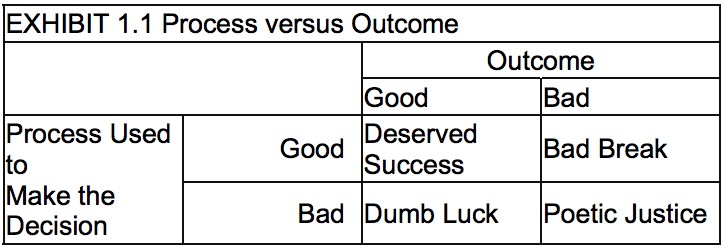

Paul DePodesta, a former baseball executive and one of the protagonists in Michael Lewis’s Moneyball, tells about playing blackjack in Las Vegas when a guy to his right, sitting on a seventeen, asks for a hit. Everyone at the table stops, and even the dealer asks if he is sure. The player nods yes, and the dealer, of course, produces a four. What did the dealer say? “Nice hit.” Yeah, great hit. That’s just the way you want people to bet-if you work for a casino.

This anecdote draws attention to one of the most fundamental concepts in investing: process versus outcome. In too many cases, investors dwell solely on outcomes without appropriate consideration of process. The focus on results is to some degree understandable. Results, the bottom line, are what ultimately matter. And results are typically easier to assess and more objective than evaluating processes.

But investors often make the critical mistake of assuming that good outcomes are the result of a good process and that bad outcomes imply a bad process. In contrast, the best long-term performers in any probabilistic field-such as investing, sports-team management, and pari-mutuel betting-all emphasize process over outcome.

Jay Russo and Paul Schoemaker illustrate the process-versus-outcome message with a simple two-by-two matrix (see exhibit 1.1). Their point is that because of probabilities, good decisions will sometimes lead to bad outcomes, and bad decisions will sometimes lead to good outcomes-as the hit-on-seventeen story illustrates. Over the long haul, however, process dominates outcome. That’s why a casino “the house” makes money over time.

And for those of you who can’t read good… (10pts if you know this half vague movie reference) here’s a video where Mauboussin talks his book at the Santa Fe Institute (link here).

And for more of my recommended books, click here.

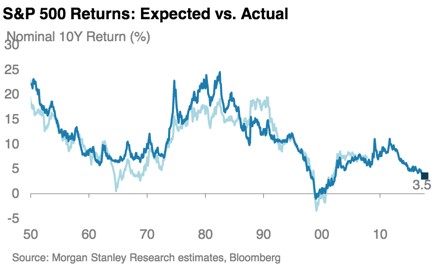

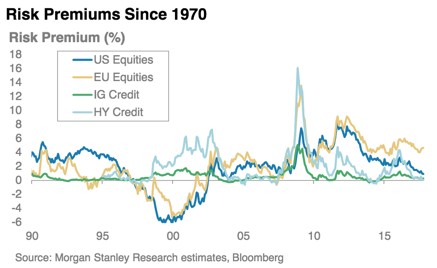

Chart(s) I’m looking at —

This chart shows the nominal expected return of the S&P over the next decade. According to this chart, we can expect an average of 3.5% in NOMINAL returns, on average, over the next 10 years. To this I say, thank God I’m not a constrained long-only US fund manager.

Also, this cool chart from Morgan Stanley. It shows risk premiums per asset classes going back 30 years. Everything is pretty tight, except equities which looks like the only +EV bet left.

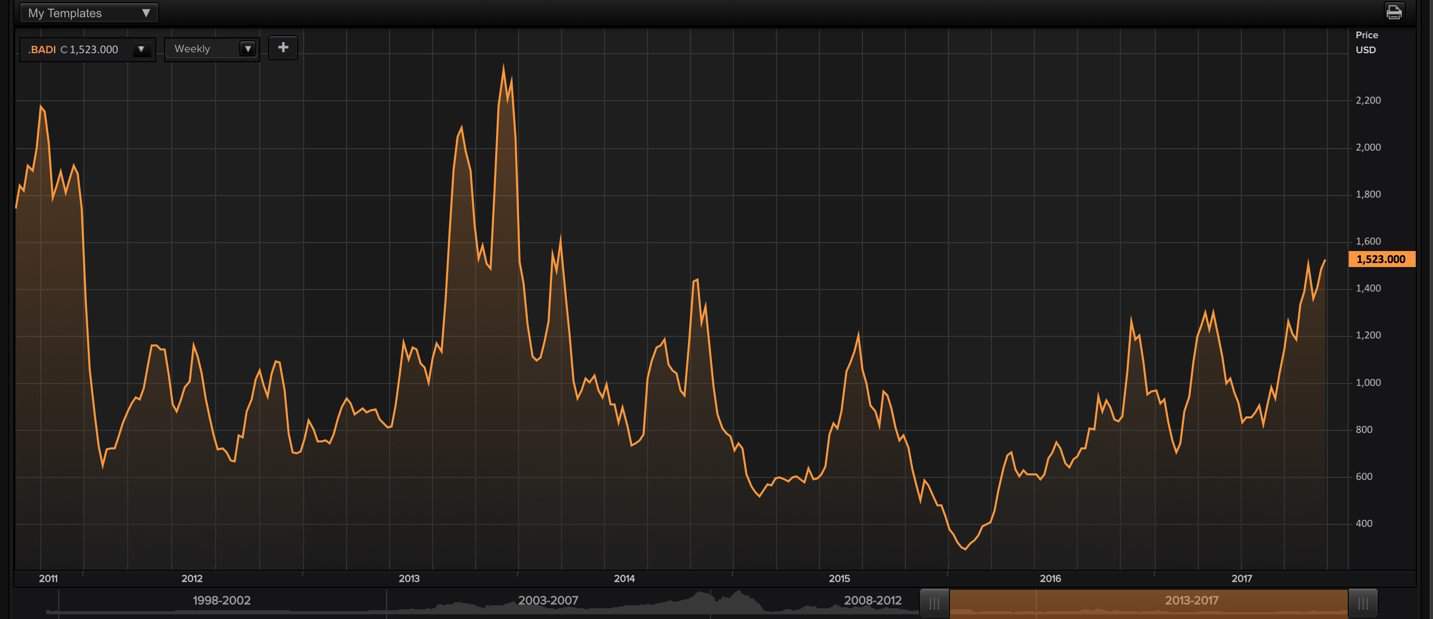

Trade I’m looking at —

I just wrote about this in the Strat Brief that goes out to our Collective Members, but I’m looking at shippers again. Below is the Baltic Dry Index. It’s making four year highs.

I’m seeing some strong tape developing in a few shipping stocks. And there’s a confluence of factors coming together that suggest there might be trade here:

Here’s the quick skinny on my take

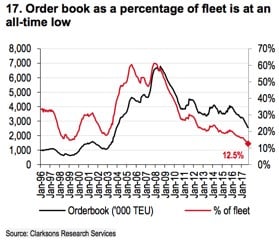

- Number of environmental regs will boost demand as well as constrain supply.

- The demand side is coming in the form of stricter Chinese regs on steel production that will require cleaner burning inputs from overseas destinations (ie, Australia and US etc.) to try and combat pollution.

- The supply side is due to new international fuel standards which aim to reduce the sulfur content in marine fuel. This is going to result in slower shipping speeds which will have the same effect as if the total fleet was cut by up to 20%.

Plus, things like fleet idle capacity are at multi-year lows, scrapings are high, and the order book as a percentage of fleet capacity is at an all-time record low.

Seems to me that we’re headed for a supply constrained environment in the coming years, especially if demand keeps growing like it has been.

Quote I’m pondering —

Everything gets destroyed a hundred times faster than it is built up. It takes one day to tear down something that might have taken ten years to build. ~ Paul Tudor Jones

I think now is a good time to keep this quote front of mind.

In a market that seems to just slowly melt up, where every little dip quickly bought, it behooves us to remember that the Turkey is the fattest the day before Thanksgiving…

This low vol period will someday end and a lot of investors have become complacent and overextended. And just like the turkey, one’s portfolio is the most vulnerable when it’s the most exposed with leveraged longs and paper gains.

This isn’t me being bearish (I’m not). Just a friendly reminder that volatility, like everything else in this game, is cyclical.

So keep your head on a swivel and stay frosty my friends.

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. I posts my mindless drivel there daily.

And if you’d like to discuss macro with the rest of the Operator community, check out our Global Macro Facebook group by clicking here.

Have a great weekend.

Your Macro Operator,

Alex