As traders, one of the most important traits we can adopt is humility. We have to embrace our fallibility.

Markets are complex systems. We cannot know all the relevant variables and causal relationships. Therefore, when we make a market prediction or place a trade, we can’t truly know if the subsequent outcome occurred for the reasons we believed, for reasons we’re unaware of, or if it was all just random noise.

This presents us with a dilemma: We must act on incomplete information and then iterate off results where we can’t fully know the causes.

So we never really know if we were right for the right reasons, right for the wrong reasons (i.e., lucky), or a little bit of both. Hence the need to stay humble.

Where traders get into trouble is when they’re right a lot for the wrong reasons but they think they’re right for all the right reasons. They think they’re making money because they’re skilled but really they’re just lucky.

Daily Speculations and the Risk of Overconfidence

Nassim Taleb writes about this problem, saying:

At any point in time, the richest traders are often the worst traders. This, I will call the cross-sectional problem: At a given time in the market, the most successful traders are likely to be those that are best fit to the latest cycle.

Being aware of the randomness embedded in the distribution of markets returns keeps us from falling for the ego trap where we mistake skill for luck or information for noise. And since the two are difficult to distinguish over a short time frame, it forces us to focus on managing our risk in a way that tilts the odds for success in our favor over the longer term.

In his book Fooled by Randomness, Nassim Taleb offers a useful analogy of the “dentist investor” on the difference between noise and information. Here it is:

The wise man listens to meaning; the fool only gets the noise. The modern Greek poet C.P. Cavafy wrote a piece in 1915 after Philostratus’ adage “For the gods perceive things in the future, ordinary people things in the present, but the wise perceive things about to happen.” Cavafy wrote:

“In their intense meditation the hidden sound of things approaching reaches them and they listen reverently while in the street outside the people hear nothing at all.”

I thought hard and long on how to explain with as little mathematics as possible the difference between noise and meaning, and how to show why the time scale is important in judging a historical event. The Monte Carlo simulator can provide us with such an intuition. We will start with an example borrowed from the investment world, as it can be explained rather easily, but the concept can be used in any application.

Let us manufacture a happily retired dentist, living in a pleasant, sunnytown. We know a priori that he is an excellent investor, and that he will be expected to earn a return of 15% in excess of Treasury bills, with a 10% error rate per annum (what we call volatility). It means that out of 100 sample paths, we expect close to to 68 of them to fall within a band of plus and minus 10% around the 15% excess return, i.e. between 5% and 25% (to be technical: the bell-shaped normal distribution has 68% of all observations falling between -1 and 1 standard deviations). It also means that 95 sample paths would fall between -5% and 35%.

Clearly, we are dealing with a very optimistic situation. The dentist builds for himself a nice trading desk in his attic, aiming to spend every business day there watching the market, while sipping decaffeinated cappuccino. He has an adventurous temperament, so he finds this activity more attractive than drilling the teeth of reluctant old Park Avenue ladies.

He subscribed to a web-based service that supplies him with continuous prices, now to be obtained for a fraction of what he pays for his coffee. He puts his inventory of securities in his spreadsheet and can thus instantaneously monitor the value of his speculative portfolio. We are living in the era of connectivity.

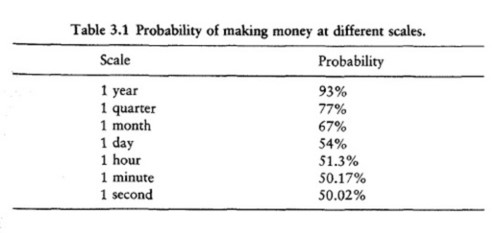

A 15% return with a 10% volatility (or uncertainty) per annum translates into a 93% probability of making money in any given year. But seen at a narrow time scale, this translates into a mere 50.02% probability of making money over any given second as shown in Table 3.1. Over the very narrow time increment, the observation will reveal close to nothing. Yet the dentist’s heart will not tell him that. Being emotional, he feels a pang with every loss, as it shows in red on his screen. He feels some pleasure when the performance is positive, but not in equivalent amount as the pain experienced when the performance is negative.

At the end of every day the dentist will be emotionally drained. A minute-by-minute examination of his performance means that each day (assuming eight hours per day) he will have 241 pleasurable minutes against 239 unpleasurable ones. These amount to 60,688 and 60,271, respectively, per year. Now realize that if the unpleasurable minute is worse in reverse pleasure than the pleasurable minute is in pleasure terms, then the dentist incurs a large deficit when examining his performance at a high frequency.

Consider the situation where the dentist examines his portfolio only upon receiving the monthly account from the brokerage house. As 67% of his months will be positive, he incurs only four pangs of pain per annum and eight uplifting experiences. This is the same dentist following the same strategy. Now consider the dentist looking at his performance only every year. Over the next 20 years that he is expected to live, he will experience 19 pleasant surprises for every unpleasant one!

This scaling property of randomness is generally misunderstood, even by professionals. I have seen Ph.D.s argue over a performance observed in a narrow time scale (meaningless by any standard). Before additional dumping on the journalist, more observations seem in order.

Viewing it from another angle, if we take the ratio of noise to what we call nonnoise (i.e., left column/right column), which we have the privilege here of examining quantitatively, then we have the following. Over one year we observe roughly 0.7 parts noise for every one part performance. Over one month, we observe roughly 2.32 parts noise for every one part performance. Over one hour, 30 parts noise for every one part performance, and over one second, 1,796 parts noise for every one part performance.

A few conclusions:

-

Over a short time increment, one observes the variability of the portfolio, not the returns. In other words, one sees the variance, little else. I always remind myself that what one observes is at best a combination of variance and returns, no just returns (but my emotions do not care about what I tell myself).

-

Our emotions are not designed to understand the point. The dentist did better when he dealt with monthly statements rather than more frequent ones. Perhaps it would be even better for him if he limited himself to yearly statements. (If you think that you can control your emotions, think that some people also believe that they can control their heartbeat or hair growth.)

-

When I see an investor monitoring his portfolio with live prices on his cellular telephone or his handheld, I smile and smile.

George Soros once wrote, “I contend that taking fallibility as the starting point makes my conceptual framework more realistic. But at a price: the idea that laws or models of universal validity can predict the future must be abandoned.”

And market wizard Mark Weinstein would say, “Don’t be arrogant. When you get arrogant, you for sake risk control. The best traders are the most humble.”

Embrace Fallibility and Stay Humble

So be humble. Take fallibility as your starting point. Be aware of the random nature of markets over various temporal cycles. Don’t mistake noise for information or skill for luck. And always focus on protecting your capital first.

Drop any questions/comments in the comment section below. And if you’d like to get my thinking, ramblings, and occasional trade ideas, then just put in your John Hancock along with your email below.