Has the bleeding stopped? No. Not even close.

Yesterday, the Dow Jones Industrial Average (DJI) dropped over 10%. Over the last four weeks the DJI lost 30% of its value. Think about that. In one month the DJI dropped 30%. That’s one of the fastest declines in the history of the stock market.

There will be textbooks written about these last four weeks. How crazy is that.

And it’s only Tuesday! Hold on tight — we’re in for a wild ride.

Our Latest Podcast Episodes:

Also, if you have the time, please subscribe and leave a rating/review of the podcast on Apple Podcasts. It goes a long way in spreading the word about the show.

Here’s what we cover this week:

-

- Valuation OG Aswath Damodaran’s Pricing vs. Value

- LT3000’s Thoughts on COVID-19

- Carl Icahn’s Big Short

- The Dangers of Venture Capital Money

We’ve got a diverse group of topics, let’s dive in!

_______

March 18, 2020

COVID-19 Updates: I’m a bit pissed off. My best friend had to cancel his wedding in gorgeous Savannah, GA. I had a quaint, beach-front condo I snagged on Airbnb. Thank you, CDC, I had to get a refund.

I know, I’m salty.

Speaking of COVID-19, here’s the latest information from the CDC. Keep your gatherings under 10 people and you’re good. Which makes me wonder, how will the Duggars accomplish such a feat?

__________________________________________________________________________

Investor Spotlight: Icahn’s Big Short … Commercial Housing

GIFs by tenor

GIFs by tenor

Fresh off his banger-of-a-pick in Occidental Petroleum (OXY), billionaire Carl Icahn takes aim at another bet. This time, he’s shorting commercial housing.

Taking a page from (personal hero) Michael Burry, Icahn’s using credit default swaps against malls and office spaces.

Here’s a snippet from his interview with The Real Deal:

“You have a bunch of mortgages … so the banks went out and loaned money against a lot of shopping malls, office buildings, hotels and retail … it’s all credible institutions doing this.”

Us mere mortals would have a hard time swinging a credit default swap deal. In fact, we’d get handed the door if we tried to walk into Goldman Sachs. So how can we follow Icahn into something like this?

There’s a couple ways to play:

-

- Short commercial real estate REITs

- Short commercial real estate ETFs

- Short commercial real estate companies

Another way to play it is to go long inverse real estate ETFs. In other words, if the real estate market collapses, the value of these ETFs rise (inverse correlation).

Some popular inverse real estate ETFs include:

-

- Proshares Short Real Estate Fund (REK)

- ProShares UltraShort Real Estate (SRS)

- Direxion Daily Real Estate Bear 3x (DRV)

Disclaimer, nothing is investment advice. Just educational options if you’re looking to follow Icahn’s trade.

__________________________________________________________________________

Movers & Shakers: LT3000 & Aswath Damodaran

GIFs by tenor

GIFs by tenor

This week I had two of my favorite blogs post new content. Perfect for my two-week self-quarantine. Aswath Damodaran and Lyall Taylor published new pieces titled:

I’ll provide the cliff-notes, but I encourage you to read each post in its entirety. Both are great writers and deliver excellent content.

We’ll start with Damodaran’s piece.

Difference Between Price and Value

Damodaran starts the post by defining the main drivers of price and value. They’re different, and that’s important.

- Drivers of Value: cash flows, growth and risk

- Drivers of Price: Supply and demand

Knowing that, we can better understand Ben Graham’s claim of the market as a voting machine (in the short term), and a weighing machine (in the long run).

Along with the differences in main drivers, Damodaran elaborates on three other differences (explanations taken from blog post):

1. Price has no upper or lower bound. Value does.

Damodaran’s Take: “Since price is determined by demand and supply, and there is nothing that constrains those buying and selling in markets, at least in the near term, it follows that there is no upper or lower bound to prices … Value on the other hand has both upper and lower bounds, with both bounds being set by expected cash flows, growth and risk.”

2. Price is reactive, Value is proactive!

Damodaran’s Take: “Since pricing is determined entirely b[y] demand and supply, and there is no value center to it, it is, by its very nature, reactive … value is driven by expectations of cash flows, growth and risk, and incremental information has to be used to reassess those expectations, a more difficult task, but one that forces you to separate the wheat from the chaff.”

3. Equity prices may never converge on value (at least in your lifetime or mine)

Damodaran’s Take: “Put simply, assuming that you will be rewarded for being right on value can be a pipe dream, and Keynes was correct when he said that the “market can stay irrational longer than you and I can stay solvent.”

Finding Your Edge (as a Trader or Investor)

Damodaran notes that, “to succeed as an active market player, you have to bring something to the table, and recognizing the edge that you bring is the key to success, and that is true whether you are an investor or a trader.”

So what, exactly, does an edge look like? And are edges different between traders and investors? Luckily Aswath read our minds. He defines trading edges versus investing edges:

-

- Trading Edge: “you can be good at riding momentum or detecting shifts in it and making money from reversals …”

- Investor Edge: “your skills may lie in assessing the entire market, sectors or individual stocks, and this crisis has brought those all into sharper focus.”

In other words, who you are (trader or investor) defines what edge you take into market speculation.

And that’s the beauty. There is no “right” or “wrong” edge. There’s only the edge that matches your personality and temperament.

Let’s move on to Lyall’s post.

____________

Coronapocalypse: How To Virus Impacts Stocks

COVID-19 is a black swan to financial markets. But according to Lyall, it wasn’t the only arrow in the bear market’s quiver:

“If that wasn’t bad enough, markets have also been hit with a “one two punch” (hat tip Buffett) of a breakdown in OPEC+ supply discipline, with the cartel announcing that in an environment of rapidly falling oil demand, that they would not only not cut production further, but actually significantly increase supply, by perhaps 2-3m bbl/d.”

If one shock wasn’t enough, two would certainly pull major global markets into recession. Lyall extrapolates these shocks and their effects on wealth funds, saying:

“Many will be forced to draw down on sovereign wealth funds to support government spending/social programs, exacerbating selling pressure in financial markets as they liquidate assets.”

He hit the nail on the head. That’s why some suggest the selling has just begun. I had ValueStockGeek on the podcast last week. He echoed similar thoughts. You can check out my conversation with him here.

So far Lyall’s painted a scary (but brutally realistic) scenario of the world we live in. Which begs the question, what should investors do? Lyall offers two ideas:

-

- Stay calm

- Behave rationally

Easy enough, right? No. In fact, it’s extremely tough to keep your wits when everyone’s losing theirs. Lyall explains:

“It is an easy environment for investors to become emotional/irrational, as not only is uncertainty rife and markets in free fall – something that makes investors emotional at the best of times – but in this case the impact is amplified by the real and visceral fear investors feel for their own health & safety.”

One such fear is debt. In particular, the high levels of US government debt. Lyall debunks this fear with facts. For example, he notes that, “What has really happened is that government debt has significantly increased in the post-GFC era, but government bond yields have collapsed to zero, and while high government debt could be a problem long term, it is most certainly not a problem at present.”

Government debt is large, yes. But the debt servicing burden (i.e., interest payments) are near all-time lows.

We’re also deleveraging in the private sector. Lyall suggests that, “private sector debt intermediated by the banking system has been falling for 13 years in both the US and Europe relative to GDP. Household debt in the US, for e.g., has fallen from more than 100% to only about 75% at present.”

Good Investing Is Like Sailing

I love Lyall’s analogy of sailing and investing. As someone who lives near a sailing capital (Annapolis, MD), I found this insightful (emphasis mine):

“Good investing is a lot like sailing. When you set out to sea, you should not assume perpetually calm conditions even if all you can see is blue sky and calm in every direction. You should anticipate the occasional storm, and when you find yourself in a storm, while it is tough and uncomfortable, you should reassure yourself that the storm will eventually pass.”

This too shall pass, we just don’t know when.

__________________________________________________________________________

Resource of The Week: The Dangers of Venture Capital Money

Venture capital money (if left in the wrong hands) can be dangerous to those with it, and those around it. Maya Kosoff published a great article on the dangers of venture capital. Her worry centered with direct-to-consumer (DTC) companies like Outdoor Voices, Harry’s and Casper (CSPR).

For our purposes, we won’t dive into the backstory behind Outdoor Voices. But we will highlight the specific dangers behind accepting venture capital money early. What it means for those companies, and why growth (for the sake of growth) isn’t good.

From Inception to Millions

Ty Haney founded Outdoor Voices in 2012. Within four years raised $64M from venture capital. Her model was simple: Be the Warby Parker of athleisure-wear.

The allure of DTC models to venture capital reminds me of the greek tale of the Sirens. Their voices sound so sweet. Yet listen long enough and you end up shipwrecked. Dead.

The case for DTC investment makes sense, though. Maya lists a few reasons in the article:

-

- Remove middle-man

- Keep tight control over marketing & customer service

- Generate positive feedback loop with customer data

But there was one problem. The company was burning through cash. Maya cites Business of Finance, saying, “According to BoF, Outdoor Vices was hemorrhaging up to $2M per month last year on annual sales of around $40M.”

Think about that. The company lost $24M on $40M in sales. Ouch!

Acquiring Customers Is Hard — Really Hard

Outdoor Vices faced a problem: it costs them more money to get customers than the revenue the customer gave the company. Not only that, but most of these DTC companies focus on one product.

You could argue that specializing in a niche (like one product) is a good thing. And in a way it is. It allows you to focus on the one thing you do well. But at the same time, if you don’t build a fanatic customer base, your one thing will be the death of you.

Maya elaborates on this customer acquisition struggle:

“Customer acquisition is so challenging in the first place, they need to spend money to get potential customers in the door — and then even more money to keep them there.”

Casper, The Poster-Boy For DTC Failure

This brings us to Casper (CSPR). As a private company, CSPR was valued around $1B … with a B. What does $1B get you? A company with terrible unit economics and consistent losses. Don’t take my word for itk here’s their last three years net income:

-

- 2017: -$73.1M

- 2018: -$93.2M

- 2019 (9M): -$67.4M

A company privately valued in the billions now trades around $350M on public markets. Take a look at this chart …

It’s easy to start a DTC business. Which means it’s easy to raise funds from yield-hungry venture investors. Yet this low barrier to entry signals an equally challenging task. Actually surviving (and profiting).

__________________________________________________________________________

Watchlist of The Week: Spin-offs I’m Following

Those that have followed me for a while know that I love spin-offs. They’re a great place to find asymmetric reward/risk opportunities due to forced selling and institutional mandates.

Over the last few weeks, spin-offs (along with everything else) were taken out to the woodshed and shot.

Here’s a list of spin-offs I’m actively watching (and their charts):

-

- Fox Corporation (FOX)

-

- Envista Holdings (NVST)

-

- Cerence (CRNC)

-

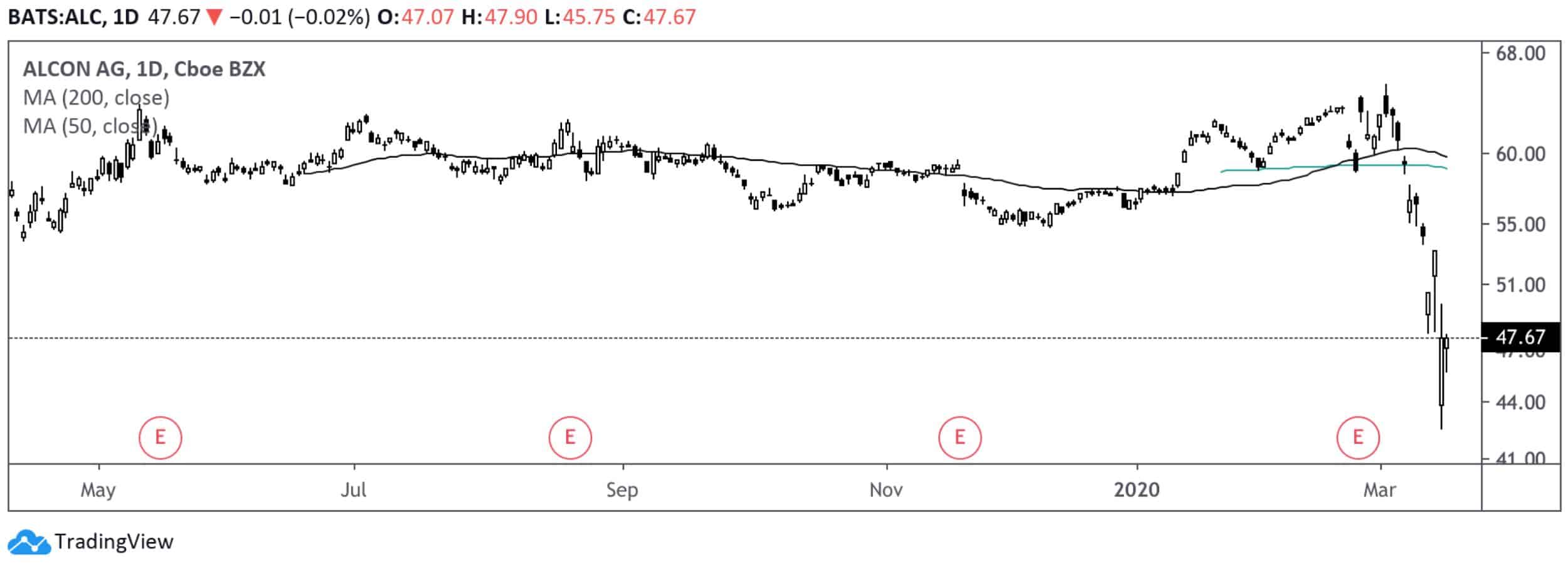

- Alcon (ALC)

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com. Have a great Christmas holiday.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!