After a brief stint of daily content, I’m back with your weekly favorites. From here on out, expect your normal Wednesday morning Value Hive in your inbox. We’re back in the saddle.

If you haven’t had a chance to check out my latest podcast episodes, you can find them here:

-

- Episode 9: Dave Waters, Alluvial Capital

- Episode 10: Maj Souedian, GeoInvesting.com

So far Dave’s podcast has the most listens of any podcast I’ve done. Congrats Dave! I’m excited to release this week’s podcast.

Anyways, we’re deep in the heart of investor letter season. Here’s what we got this week:

-

- White Crane Capital

- Wolf Hill Capital

- Alluvial Capital

We also have a resource from expectations investing OG Michael Maubouisson.

Let’s dive in!

—

February 05, 2020

It Pays To Take The Under: First, a big congrats to the Chiefs for pulling off a Super Bowl win. I know Brent Beshore is ecstatic, and I couldn’t be happier for the state of Kansas ;). Before kick-off, bettors who took the UNDER on Demi Lovato’s National Anthem song duration of 2 minutes made some cash. The line? +180. Not bad.

___________________________________________________________________________

Investor Spotlight: Letters and More Letters

GIFs by tenor

GIFs by tenor

I’m excited to dive into these letters. Each one presents ideas on the markets and new positions. Make sure to read these in their entirety. I don’t know if its selection bias, but most of these managers are damn good writers.

Let’s start with White Crane.

White Crane Capital: +10.4% in 2019

White Crane Capital returned 1.8% in Q4 and 10.4% in 2019. For those unfamiliar with White Crane’s strategy (like I was before writing this), here it is:

“The White Crane Multi-Strategy Feeder Fund Ltd. seeks to identify securities across the capital structure that trade at a discount to our estimate of intrinsic value (valuation discrepancy), with corresponding company specific events to cause the price to converge to intrinsic value (catalyst). A multi-strategy approach is used to generate an uncorrelated return to broader equity and fixed income markets throughout the market cycle”

I like White Crane because it exposes me to an area of competence I lack: bonds. I want to learn more about investing across the capital structure. And I find White Crane’s letters a great resource.

As of December 31, the Fund was 55% long and 44% short for 11% net exposure. But what I’m interested in is their position in Yellow Pages (YLO).

White Crane bought YLO’s senior secured bonds in January 2018. Their thesis at that time included the following (from the letter, non-exhaustive):

-

- Leverage at the senior secured level was approximately 1.7x. The business had transitioned such that, by our estimate, approximately 50% of the Company’s EBITDA was derived from its digital assets. Applying conservative multiples of 3.0x EBITDA for the print business and 6.0x EBITDA for the digital business resulted in asset coverage of approximately 3.0x.

- The indenture had bondholder friendly (i.e. tight) covenants including sweeps on free cash flow generation and asset sales.

- Despite experiencing revenue declines, YLO continued to generate substantial free cash flow.

YLO redeemed its senior secured notes in full in the fourth quarter 2019. White Crane accrued a 10% yield over the life of their investment at, “what we believe [to be] very low credit risk.”

Why did they think YLO’s bonds offered low credit risk? They focused on cash flow. They ignored perceptions (emphasis mine):

“We believe our approach of focusing on YLO’s cash flow generation allowed us to understand the reality of this strong credit, rather than focusing on the perception. In the current markets, it sometimes seems that investors perceive profitability and cash flow generation as being afterthoughts, while we take a more traditional view in believing they form the bedrock of security valuation.”

Cash flow forms the bedrock of security valuation. Love that quote.

———————————-

Wolf Hill Capital: +32.3% in 2019

Gary Lehrman’s Fund returned 7.47% in Q4 2019 and 32.3% for the year. Since inception (Feb. 2019) the Fund’s returned 115.98% for partners. Not bad Gary!

One thing to note about Wolf Hill’s returns: they generated positive alpha from their short positions. To generate 4.6% from shorts in a “rip-roaring” market is worthy of a hat tip.

Let’s dive into Wolf Hill’s newest ideas:

-

- Cornerstone Building Brands (CNR) – Long

- Renewable Energy Group Inc (REGI) – Long

- Westshore Terminals (WTE.CN) – Short

All information about the ideas come straight from the letter.

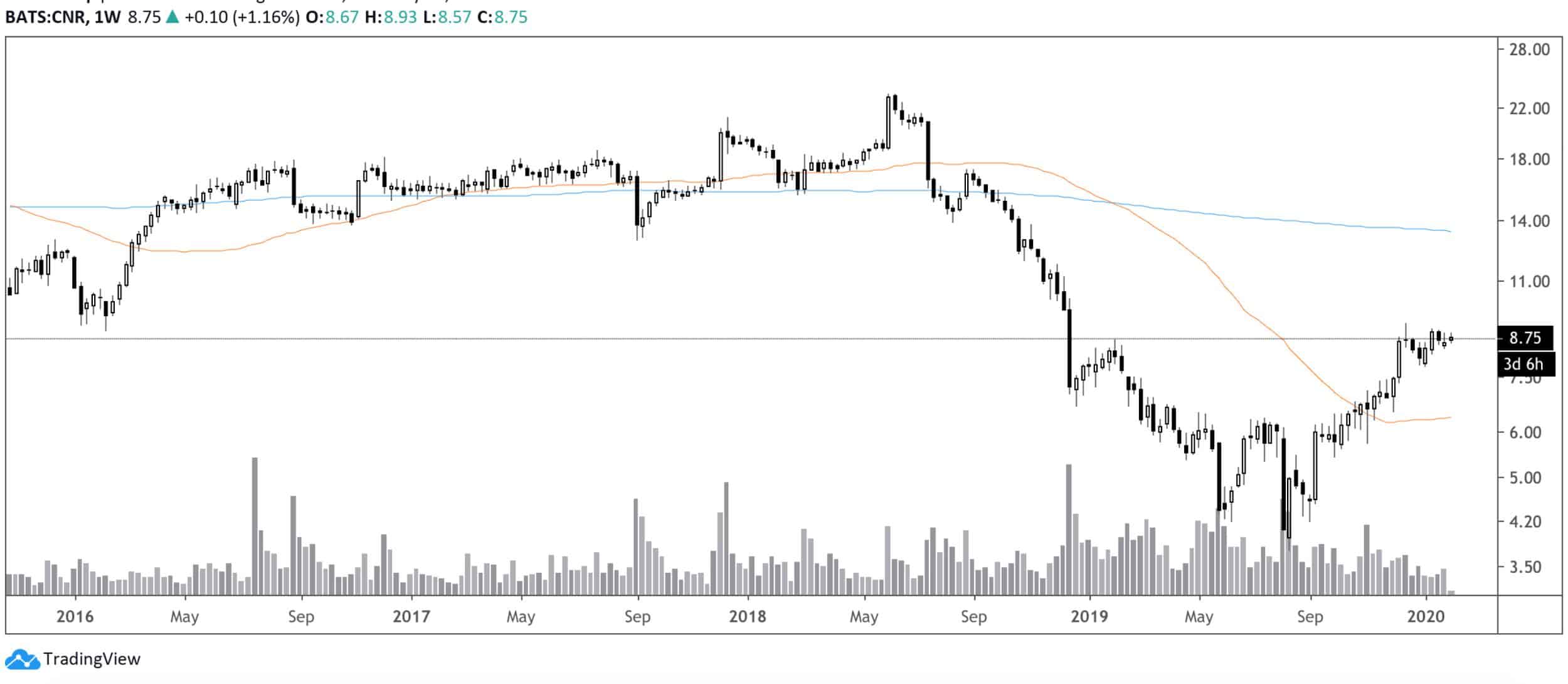

Cornerstone Building Brands (CNR) – Long

CNR is the largest North American manufacturer of outdoor building products. They serve both commercial and residential construction end-markets.

Wolf Hill claims CNR is another “classic public market LBO.” Here’s their logic:

“… The market cap represents a small portion (20%) of the company’s total enterprise value and the majority of the outstanding stock is in fact held by private equity firms CD&R and Golden Gate Capital. The combination of CNR’s robust free cash flow generation and our anticipation of improving earnings creates what we believe will be a powerful recipe for shareholder returns as deleveraging and multiple expansion take hold.”

Where will the value unlock come from? Wolf Hill has a few ideas:

-

- Cyclical tailwinds from robust residential construction trends

- Consolidating manufacturing facilities

- Investing in high ROI automation equipment

Let’s take a look at the charts …

As you can see, CNR’s about broke even since 2019. We’ll leave this idea with Wolf Hill’s closing remarks:

“We believe CNR will have the wind at its back as dovish Fed policy will keep mortgage rates persistently low, allowing new home and commercial construction projects to maintain their healthy growth trajectory. At today’s valuation, CNR offers exceptional upside potential, driven by healthy end-market demand and company specific initiatives which should drive earnings growth and balance sheet de-leveraging.”

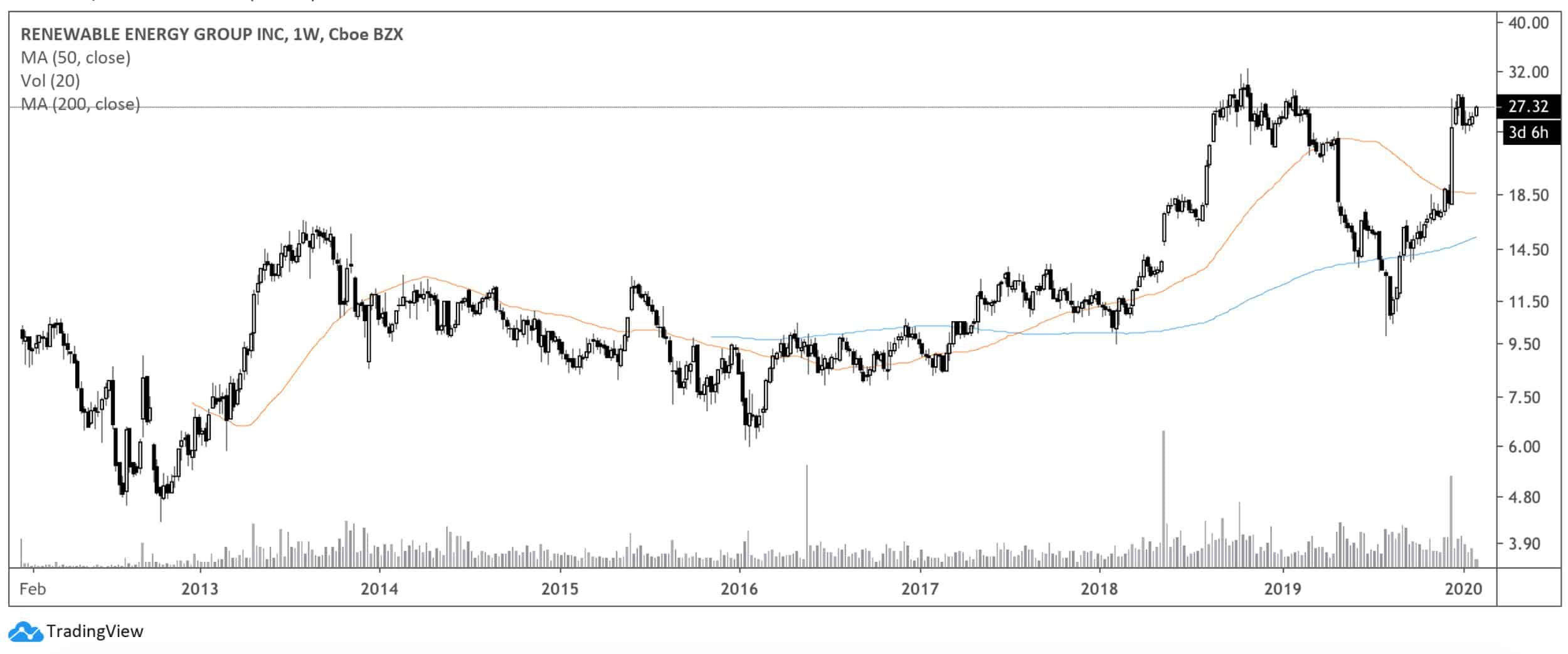

Renewable Energy Group, Inc. (REGI) – Long

REGI is the largest producer of biodiesel and second largest producer of renewable diesel in the US. Wolf Hill built a “meaningful position” in REGI during Q4 2019 around the “call-option like” event: Blenders Tax Credit.

Wolf Hill explains the BTC, saying, “The BTC was a piece of legislation first implemented in 2005 that provides a $1/gallon tax credit for biodiesel producers. Since 2005 Congress has often allowed the BTC to expire, only to reinstate it retroactively”

Congress reinstanted the BTC in December on a retroactive basis. This also provided an extension of the BTC through 2022. What does this mean for REGI? One monster tax-free windfall: $500M in cash ($13/share).

Let’s go to the charts …

The stock’s flirting with all-time highs. Wolf Hill remains bullish after the stock’s run-up. Here’s why (from the letter):

“In Summary, if we conservatively value REGI’s renewable diesel facility at $1b, the market is assigning a negative $300mm valuation to the rest of REGI’s portfolio! No, that was not a typo. We believe that REGI represents a +$3b collection of assets – in fact we cannot fathom a scenario where REGI is worth materially less than today’s valuation over any extended time frame. We anticipate the next leg higher in REGI’s valuation to occur in conjunction with the upcoming earnings announcement where management is likely to announce an aggressive share repurchase authorization and to quantify the compelling economics of deploying capital into an expansion of the company’s renewable diesel portfolio.”

This idea might be worth looking into (I don’t own a position).

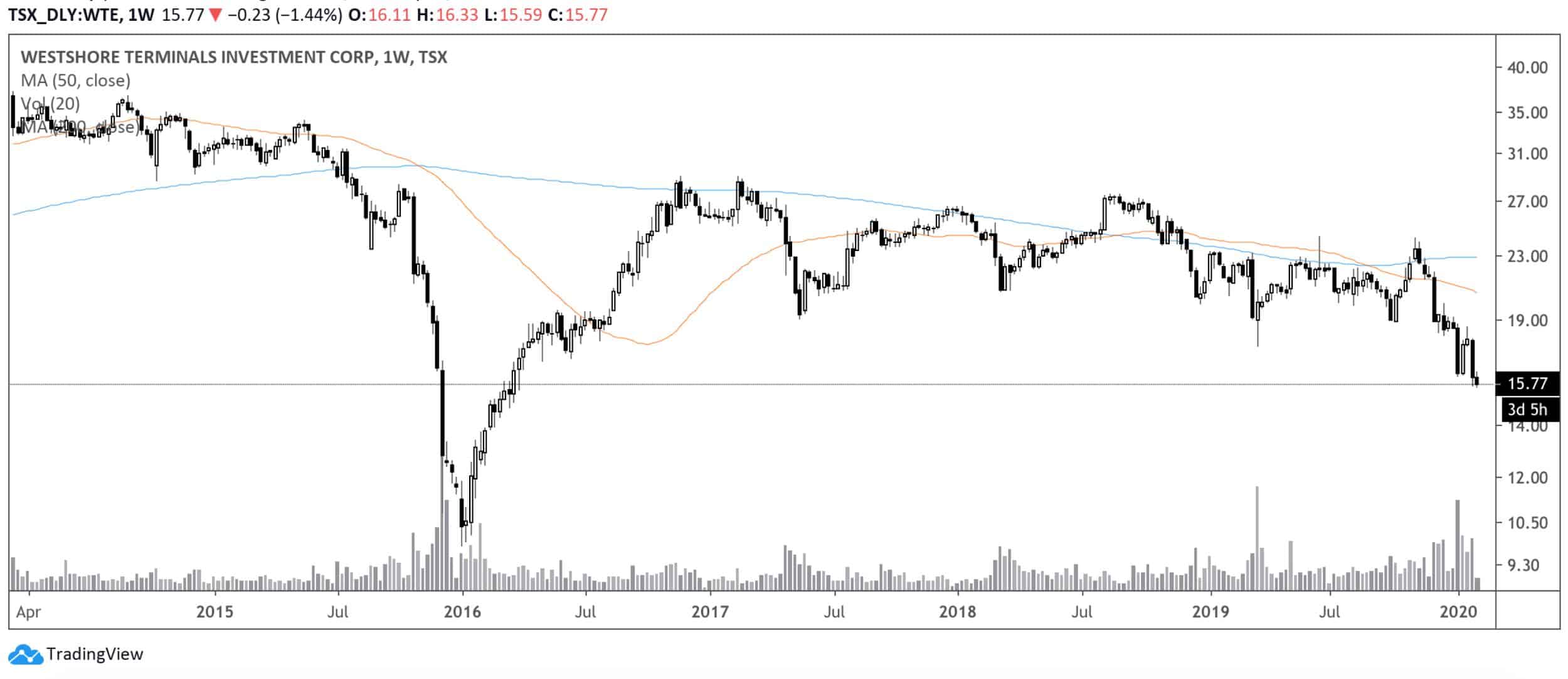

Westshore Terminals (WTE.CN) – Short

Westshore operates the largest coal export facility on the American West Coast from a port in Vancouver. Wolf Hill believes the short is now more compelling at lower prices ($18 compared to initial short at $20). Here’s why:

“In addition, Westshore’s second largest customer, Cloud Peak, was on the verge of bankruptcy and would ultimately be forced to idle mines that were shipping through Westshore as Cloud Peak export economics no longer made sense.”

Let’s go to the charts …

The stock’s down around 15% since Wolf Hill’s letter release.

At year-end 2019, Wolf Hill had 12 longs and 11 shorts.

Alluvial Capital: +18.5% in 2019

Dave Waters returned 5.8% in Q4 and 18.5% in 2019. Since starting Alluvial Capital, Dave’s returned 39.8% to LPs, or 11.8% annualized. Dave’s a great guy and awesome investor. Check out my podcast with him above if you haven’t had the chance.

Also, go follow Dave on Twitter @alluvialcapital. Anyways, back to the letter.

There’s five areas Dave believes his Fund has succeeded:

-

- Undiscovered Markets

- Corporate Events

- Obscured Value

- The Truly, Truly Illiquid

- Special Situations

Of course, my favorite of these is the Truly, Truly Illiquid. Yet Undiscovered Markets offer tremendous opportunities for the patient (or stubborn) investor willing to look. Dave explains these Undiscovered Markets (emphasis mine):

“Searching for value in little-known market segments with barriers to investment has been a profitable enterprise for Alluvial Fund. The Borsa Italiana AIM segment, for instance, goes unexplored by most funds because of the tiny size and limited trading liquidity of its constituents. We are already looking for the next treasure trove!”

Fish where the fish are and the fishermen aren’t.

Let’s take a look at Alluvial’s newest holding: Butler National Corp. (BUKS). For full disclosure, I am a shareholder in BUKS. Here’s Dave’s take on the company:

“Butler is an odd little company with operations in two industries. The first is aerospace: the firm performs aircraft upgrades, modifications, and testing. The second is casino management: Butler has a majority stake in the entity that manages the Boot Hill Casino in Dodge City, Kansas. These lines of business have nothing to do with each other and there are no possible synergies gained from operating both. Thankfully, the company is aware of this and is exploring a disposition of the smaller, less profitable casino management business by way of a sale or spin-off. “

Of course, I agree with Dave’s thesis. Also, if you want to check out my thesis on BUKS, click here.

Per Dave’s letter, “Butler trades at a price-to-earnings multiple of just 6 and has substantial excess cash on its balance sheet. Currently trading around 70 cents, I believe shares are worth well over $1 today and potentially far more in coming years.”

As a fellow shareholder, I hope we’re right Dave!

___________________________________________________________________________

Resource of The Week: Managing The Man Overboard Moment

GIFs by tenor

GIFs by tenor

Shout-out to Ensemble Capital’s twitter account for this resource. If you haven’t, go follow them. They produce great content and will add to your Timeline quality.

This week’s resource is Michael Mauboussin’s white-paper, Managing the Man Overboard Moment.

Mauboussin addresses the dreaded topic: when one of your stocks drops 10%+ in one day. At this moment, it’s important to keep your compass pointing North. Mauboussin looks at the data, 5,400 events in the past quarter century.

Through his analysis, he develops a checklist for investors. The checklist helps decide whether to buy, hold or sell the free-falling stock. Here’s the checklist:

The entire paper is worth the read, as is anything Mauboussin writes.

___________________________________________________________________________

Tweet of The Week: Tiho Brkan on Wall Street Analysts

— Ryan Holiday (@RyanHoliday) February 4, 2020

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com. Have a great Christmas holiday.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!