The following is an excerpt from our Macro Intelligence Report (MIR). If you’d like to learn more about the MIR, click here.

Last July, we laid out the case for why China is the most important macro factor this cycle. We talked about why it’s a debt riddled neutrino bomb waiting to go boom… But… we also noted how the Chinese Communist Party (CCP) had been injecting liquidity into its economy in order to steady the boat during its all-important National Congress last year.

Our pitch was that we were tactically bullish but strategically bearish (which so far looks to have been the right call).

Well, now that the big gathering of Marx lovers is over and Xi Jinping has been anointed the Grand Emperor for life. The CCP has the all-clear to move forward with managing the country’s deleveraging and transitioning from an export economy to a consumption based one

Why does this matter? Why is China so important to global markets?

Well, it’s mainly because they are the world’s marginal buyer of commodities… by a wide mile. So when China wheezes the rest of the world (and especially emerging markets) catches cholera.

Here’s a short summary of just how important the red dragon has become.

It’s been said that China builds a new skyscraper roughly every five days.

In the last year alone, the country has built half of the worlds new super skyscrapers (buildings with a minimum height of 656 feet). To put that into perspective, there’s only 113 buildings in New York city, total, that are over 600 feet.

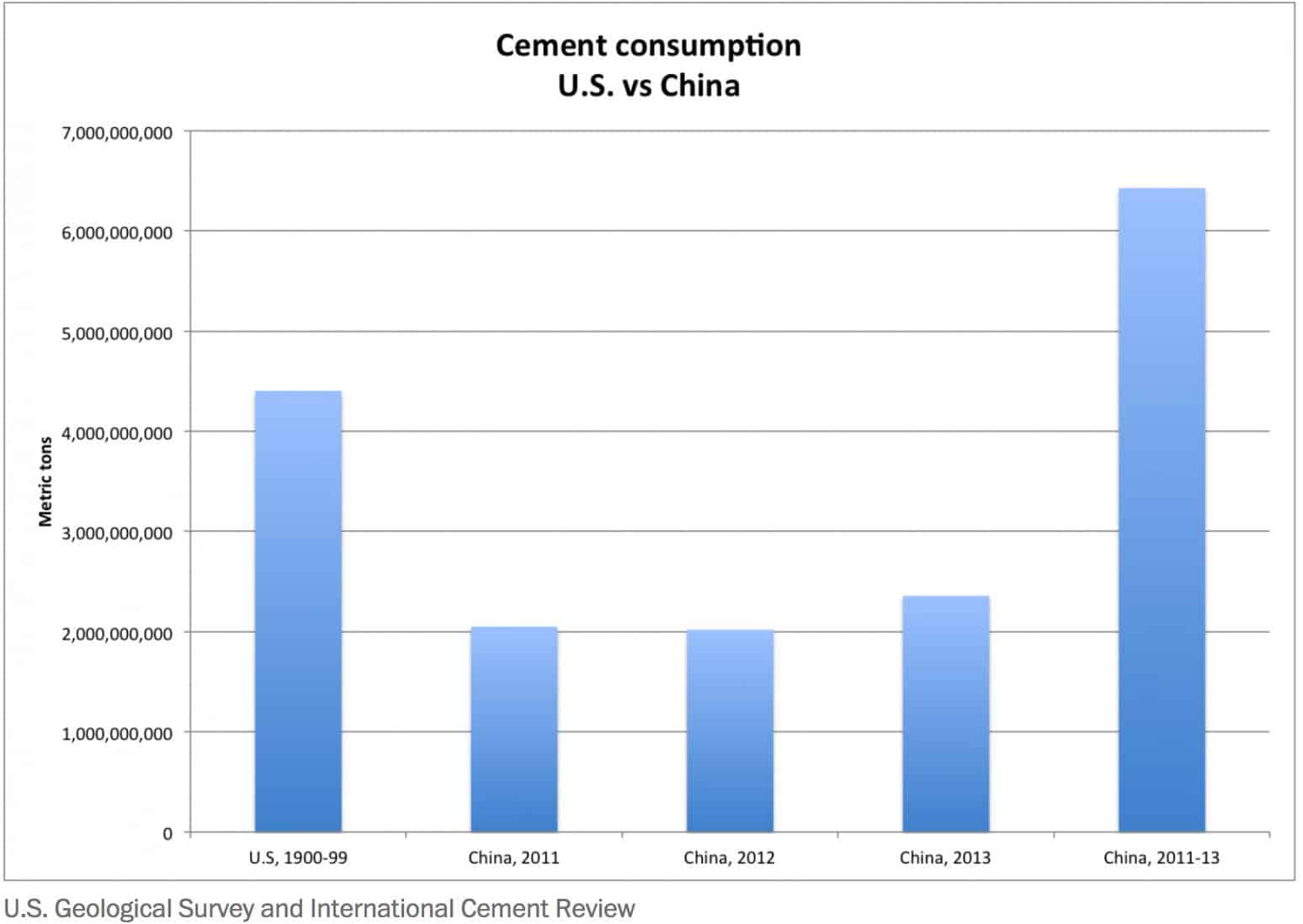

That takes a LOT of steel, copper, cement and other such resources. Another fun fact that I often like to share is this mind bender: China consumed more cement from 2011 to 2013 than the US did in the entire 20th century.

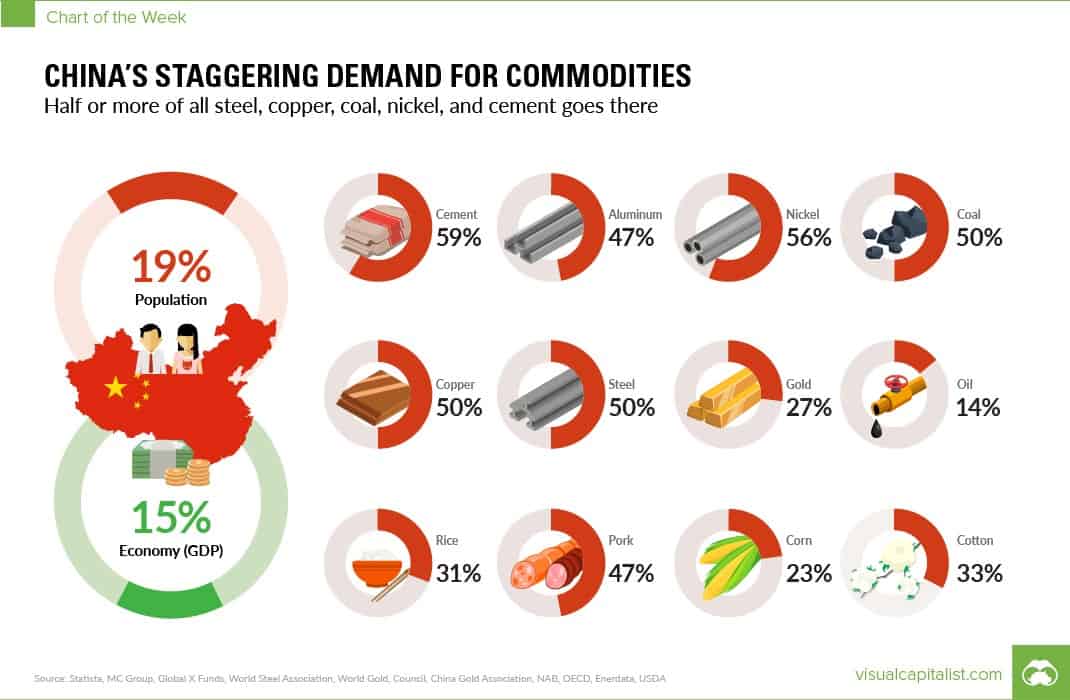

China dominates global commodity consumption. They consume more than half the world’s cement, nickel, coal, copper, and steel every year (image via Visual Capitalist).

Paul Podolsky, a PM at the macro hedge fund Bridgewater, estimates that over “70 percent of the swings in the global economy are driven by swings in the Chinese economy.”

Famed short-seller and fund manager, Jim Chanos, recounted the following regarding China a while back in an interview with the FT :

This story is internally now one of our great stories.

A real estate analyst was addressing the partners and he said: ‘Currently there’s 5.6 billion square meters of high rises in China under construction. Half residential, half office space.’ And I thought for a second and I said: ‘No, you’ve gotten the American, rest of the world metrics wrong. You must mean 5.6 billion square feet. Because 5.6 billion square meters is roughly 60 billion square feet.’

And my analyst looked at me sort of terrified. He was a young analyst at the time. He said: ‘I know. I double checked. It’s 5.6 billion square meters.’ And I thought for a second and I said: ‘Well if half of that’s office space, that’s roughly 30 billion square feet of office space. And that’s a five foot by five foot office cubicle for every man, woman and child in China!’

And that’s when we all looked at each other and our jaws dropped. We realized, wow, this is a once in a lifetime kind of thing, where this whole country is in effect building itself out in a very short period of time.

So then we looked at the capital spending of their miners, and we went back and looked at a time series of those that were around from 1990 on, and once again it was just one of these hit your head kind of moments.

And with the government’s explicit backing to do whatever it takes to keep China growing faster than the rest of the world’s major economies. Right now markets believe in two things: central banks have the market’s back and China has the global economy’s back.

Those are two very, very big pillars and they’d better hold up… because everybody believes them.

This is important —> Right now markets believe in two things: central banks have the market’s back and China has the global economy’s back… One of these beliefs is going to be tested in the coming year.

Before I explain why, let me first layout what exactly makes the CCP and its leader, Xi Jinping, tick. Since they ultimately pull the levers in the country which affect the rest of the world so much.

It can be boiled down to the following: power and control.

Xi Jinping, as the leader of the CCP, cares solely about keeping his grip on power. All leaders, especially authoritarian ones, sit under a heavy sword of damocles. Xi is no different. Maintaining power and control are necessary to his survival.

The same goes for the broader party and its members. The CCP fears social unrest more than anything else; lest the people take to the streets and begin to demand a voice in government. Both know that the best way to keep the peace is by keeping the engine of economic progress turning and never letting things regress, too much.

This is one of the many reasons why undemocratic systems are inherently fragile. They don’t have the shock absorbers that are organic to democracies — we can vote our frustration out.

Question. Do you know why communism is superior to capitalism?

Answer: Because it heroically overcomes problems that do not exist in any other system.

Anyways, so Xi and fam know that they must maintain stability, both economically and politically to ensure their survival. And since their government is filled with very bright technocrats, they know that they have to deal with their debt problem. They can’t afford to keep kicking that can down the road, anymore.

In addition, communism is all about outward appearance. Dog and pony shows are extremely important in reminding the people that the communist system is really the best. Which is why the CCP’s coming centenary anniversary in 2021 is such a big deal. They need to celebrate 100 years of economic progress.

It’s very important that the Chinese economy is strong like dragon for the centenary in just three years time. The technocrats know this. And they know that if they want a strong economy in 2021 then they need to slow it down, now. This was the theory first put forth by macro hedge fund manager Felix Zulauf, which I wrote about here.

Here’s Felix’s updated thinking on this hypothesis from a recent interview he did with Real Vision (emphasis mine).

2021 is the 100th anniversary of the Communist Party… So I assume that the current president, who is now president for a lifetime, wants to have a good economy in 2021. If he wants to have a good economy then, he’s no dummy, and his experts aren’t either because I think, actually, the Chinese government has the best experts of all the governments in the world. So they have to slow down the pace of the economy in ’18-’19, and reduce some of the risks they have built up. And I think you are seeing that already.

And I think the Chinese think that the fiscal stimulus in the US could take up some of the slack. And I think it is timed that way that when the US pushes their economy a little bit further through the fiscal stimulus, that they could retreat some and it would be balanced. Of course, it will not be balanced because China’s effect and impact on the world economy today is much bigger than the US economy.

So I think the Chinese will most likely overdeliver in their restructuring efforts over the next two years, compared to what the world expects. If that is true, then we will have a stronger dollar for longer, and will have weaker commodities for longer. But once the world then gets disappointed in ’19 or whenever they figure that out– the Chinese are beginning to kick start their economy from 2020 onwards. So I think there are many cycles within these long cycle that we are in. And the mini cycle, I think, is topping.

The theory sounds solid doesn’t it?

I mean, we know the Chinese government is worried about its excessive leverage. And we know that political anniversaries and pageantry are important in their culture. And… it would be wise — and China’s technocrats are wise, if not sometimes hamstrung — for China to move aggressively in deleveraging while the US (its counterpart engine for global growth) is firing on all cylinders, with unemployment sittings at 17-year lows and capital expenditures trending towards generational highs…

But a theory is just an opinion if we can’t back it up with numbers. And as macro operators, we need to be like the late W. Edwards Deming where, “In God we trust; but all others must bring data.”

So let’s peruse the data. And since China likes to fudge the more popular datasets, we’ll look at a dashboard of more esoteric stuff that tends to fly under the radar, unmolested.

Here’s one of my favorites.

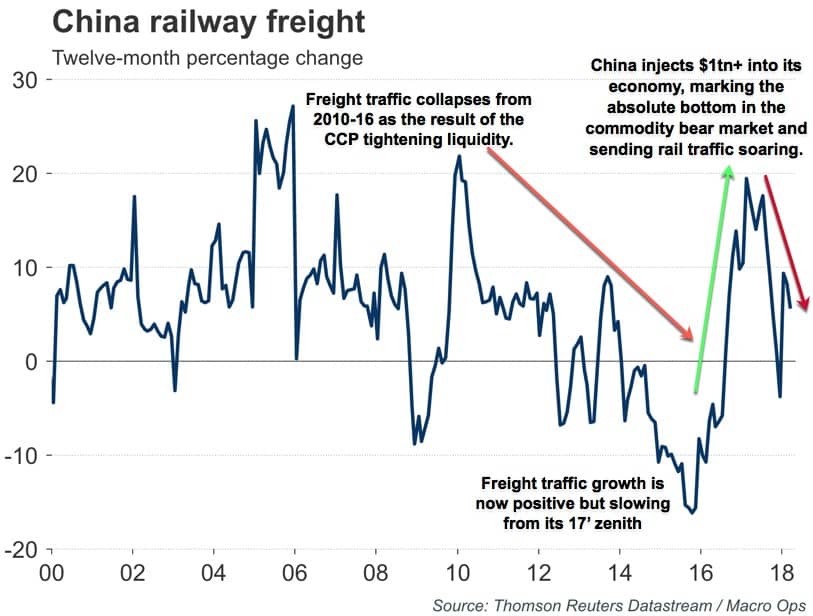

It’s the YoY change of railway freight. Remember, in our recent article, we talked about why it’s best to view data at the second derivative level. Because the rate-of-change reveals important trend changes in velocity. Well, we can see that in the chart below.

Growth in railway freight slowed, then turned negative, from 2010-14’ when China was doing its stealth tightening.

Looking at this chart alone would have tipped you off to something being amiss. You could have triangulated this with price action in commodity and emerging markets to either help you to side-step or go outright short into what became a nasty bear market.

And then in early 16’, this chart reflected the massive credit injection by the PBoC (China’s central bank) by hockey sticking upwards, which subsequently marked the nadir of the commodity/EM bear market.

Now, while growth in freight traffic is still positive. It’s slowed dramatically since its 17’ peak and looks to be decelerating further. Something we’ll have to keep a close eye on.

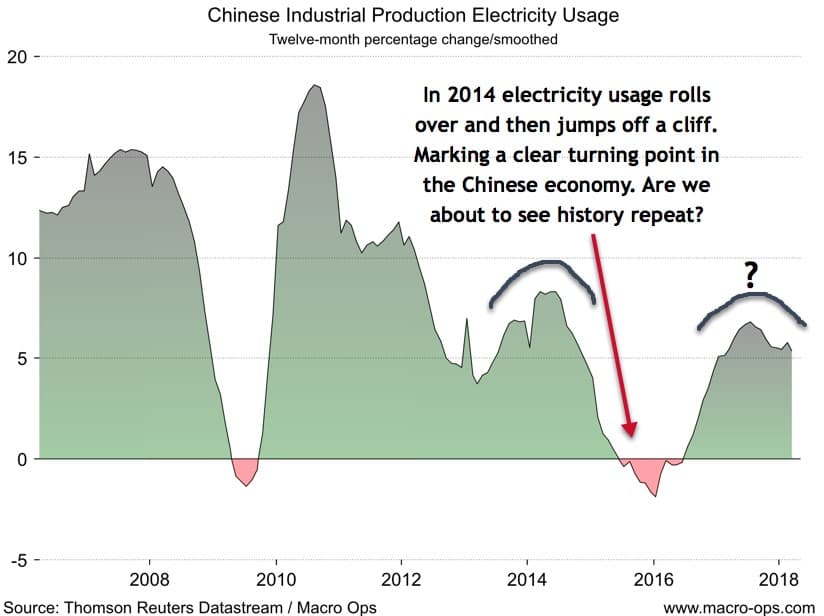

Now onto the second derivative of another favorite of mine… year over year Industrial Production Electricity Usage… Fun!

This one is sketching out the same pattern as railfreight traffic. Growth is clearly decelerating from its high-water mark hit last year.

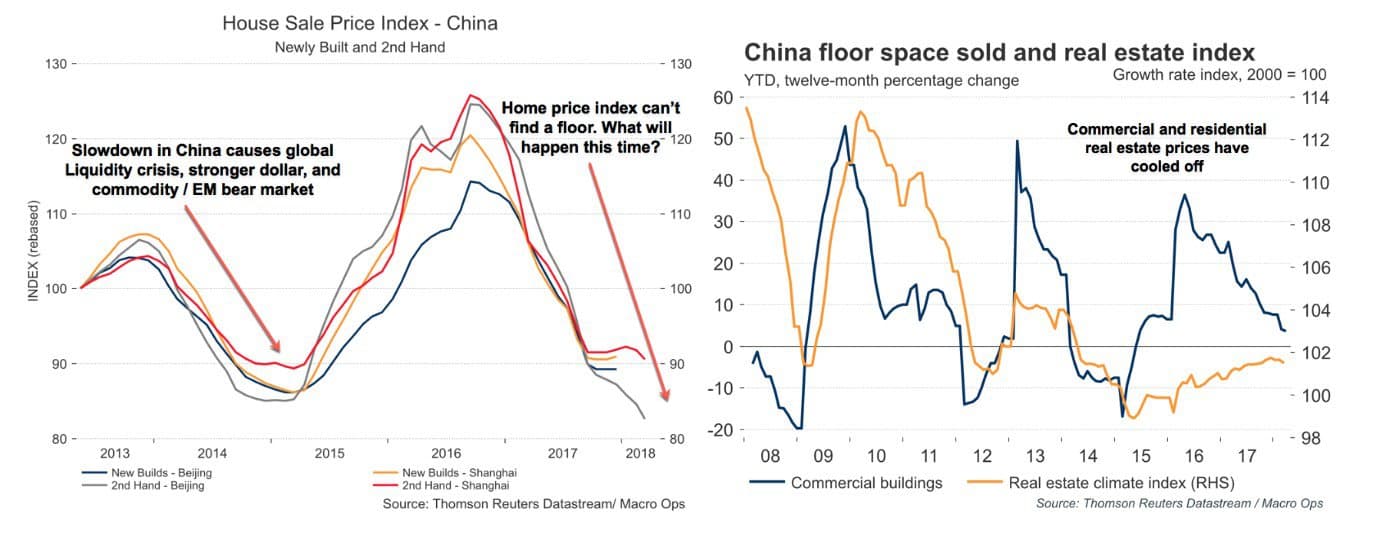

Real estate, both commercial and residential, are telling a similar story.

Home prices in China’s two hottest cities, Beijing and Shanghai, are falling. And the growth in the amount of commercial floor space sold is about to turn negative for the first time in over 3-years.

Real estate plays an important role in the Chinese consumer psyche. If this trend continues it’ll make the economy’s transition to a consumption based one, that much more difficult.

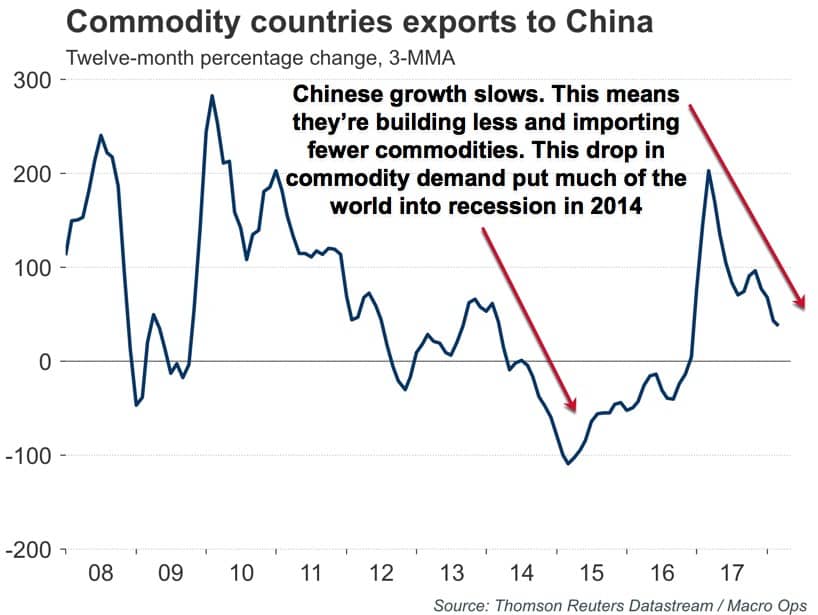

Since China is such a dominant source of global commodity demand, I’ve found that tracking their imports from commodity producing countries to be a fantastic bellwether for what’s really going on in the country.

Below is a chart showing the year-over-year changes in exports to China from the countries largest commodity trading partners.

This chart, like the others, paints a picture of decelerating growth.

Our theory now looks less and less like an “opinion” and more like the word of God, doesn’t it?

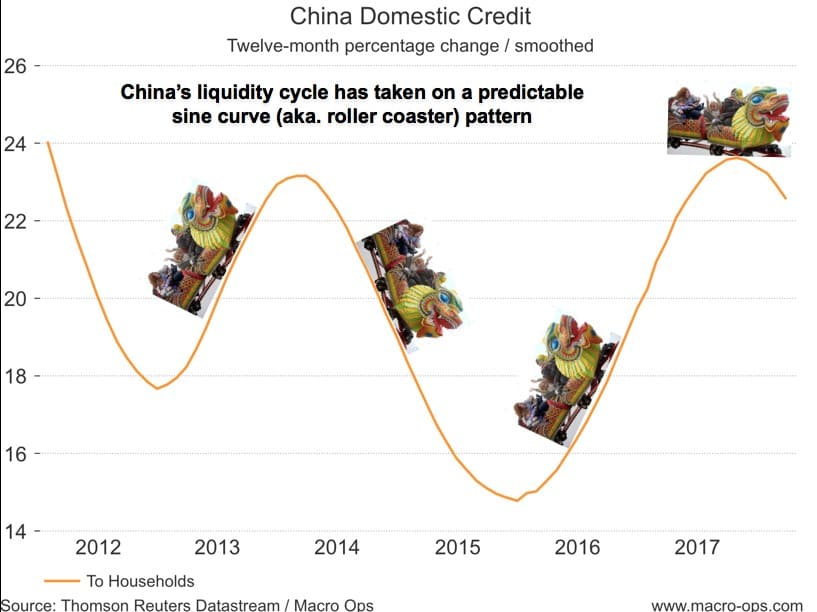

But, we can go even further. Let’s look at the source of this deceleration. The supply of money (liquidity), itself.

China’s M1 money supply (narrow money) growth turned negative following its large upswing in 16’-17’. Here it is, charted along with the year-over-year change in industrial metal spot price index. Notice any correlations? Perhaps any leading correlations?

Hopefully, the puzzle pieces are beginning to come together for you.

China is the dominant source of global commodity demand. And liquidity (ie, money supply) drives demand. So ceteris paribus, collapsing Chinese liquidity leads to falling commodity prices.

So this chart and the next one should have us somewhat concerned; because they clearly show that liquidity in China is rolling over.

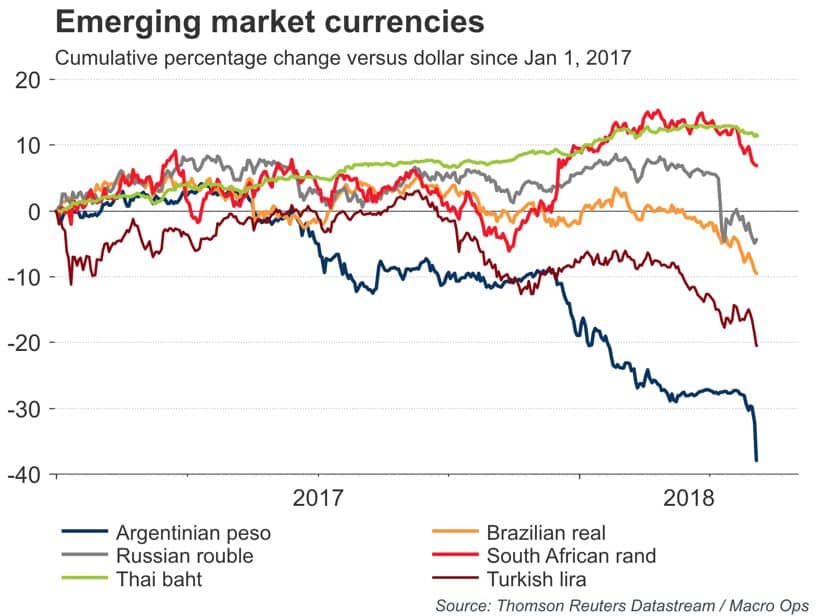

People have been wondering why emerging market debt and currencies have dived into a hole, recently. Well, the above is why. China is deleveraging and the rest of the world is just starting to feel the affects.

Does all this mean that we should sell all our positions, convert to cash, and join a friendly prepping community?

No, not exactly…

I’m no curmudgeon or China doomsdayer. I think China will manage things just fine. But growth there is clearly decelerating. And the CCP’s actions give weight to our “slowdown into 2021” theory. So, as long as the data continues to confirm our theory, that’s the one we’ll base our assumptions off of.

I’m guessing the CCP learned its lessons from the painful economic slowdown in 14’-16’ and will proceed with more caution this time around. Taking one step back for every two forward in their move to deleverage — or crossing the debt river by feeling the stones, as Deng Xiaoping would say.

Lucky for them, the US economy is booming and will help soften the blow to the global economy. Which is why we’re not predicting fire and brimstone, just yet.

The above was an excerpt from our Macro Intelligence Report (MIR). If you’d like to learn more about the MIR, click here.