Let me share one of my favorite trading quotes with you, it’s from Market Wizard Bruce Kovner. He said (emphasis mine):

One of the jobs of a good trader is to imagine alternative scenarios. I try to form many different mental pictures of what the world should be like and wait for one of them to be confirmed. You keep trying them on one at a time. Inevitably, most of these pictures will turn out to be wrong — that is, only a few elements of the picture may prove correct. But then, all of a sudden, you will find that in one picture, nine out of ten elements click. That scenario then becomes your image of the world reality.

This is an important concept to always keep front of mind… even more so now.

Looking out at the macro environment I see a ton of moving, diverging, opposing variables. All of which can whip markets in a multitude of directions and speeds going forward. Dominant market narratives are coming and going faster than Trump staff members. It’s making for an interesting macro game, for sure. And the way to play this environment successfully is to imagine alternative scenarios and wait for one of them to be confirmed.

So let’s do that.

Let’s explore a few potential macro scenarios. Try them on and see how they fit. And hopefully we’ll come away with a better understanding of how to make money in the evolving landscape and also how to protect the money we have — both of which will be equally important in the month’s ahead.

Reflation Scenario — The “Overheat Phase” of our Investment Clock framework

This is the scenario we latched onto in the summer of last year. It was appealing and had a lot of things going for it.

It was contrary to the popular market narrative of “lower inflation for longer” that was predicated on continued US dollar strength, weak commodities, and low inflation expectations. All of which had become crowded trades.

In addition, we were seeing increasing macro evidence in the data that those assumptions were wrong. That in fact, sentiment was still too negative and growth should surprise to the upside. The supply and demand fundamentals for many commodities were rapidly improving. And the dollar was susceptible to a large sell off in order to rebalance one-sided positioning.

This scenario has largely played out. Economic strength has surprised to the upside. Commodities have recovered, the dollar sold off, and bonds repriced on upward revisions to growth and inflation expectations.

And a lot of macro data continues to support this scenario.

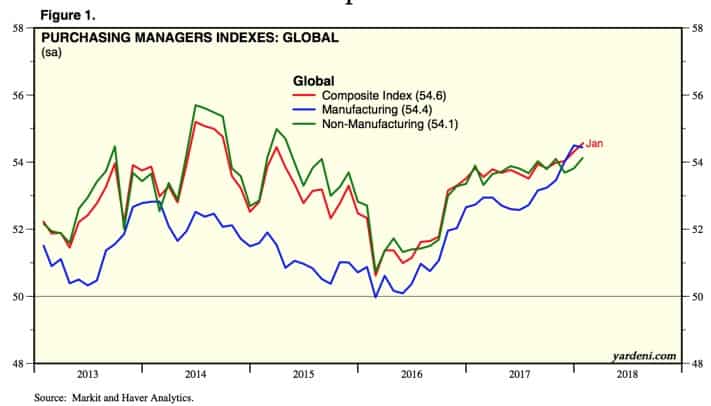

Things like the Global Composite Purchasing Managers Index, or PMI, recently hit multi-year highs (chart via Yardeni.com).

The primary trend in global equities is up and the trend is supported by very strong earnings.

Global earnings momentum is actually at its highest level in 8-years.

None of these are bearish. In fact, things look pretty dang bullish… especially over the intermediate term. A recession this year is very very unlikely.

But, this narrative has now become one of the popular market narratives. That means that expectations are now higher and positioning in this thematic is more crowded — hence, much of the narrative is adequately priced in.

Speculators are extremely long crude oil. They’re also holding record short positions in bonds. And it’s become near heresy to oppose the now popular “Dollar Bear” take.

Fundamentals by themselves are meaningless. It’s the market’s pricing of fundamentals that matter. Like the original OG Trend Trader, Ed Seykota, put it:

Fundamentals that you read about typically are useless as the market has already discounted the price, and I call them ‘funny-mentals.’ However, if you catch on early, before others believe, then you might have valuable ‘surprise-a-mentals.’

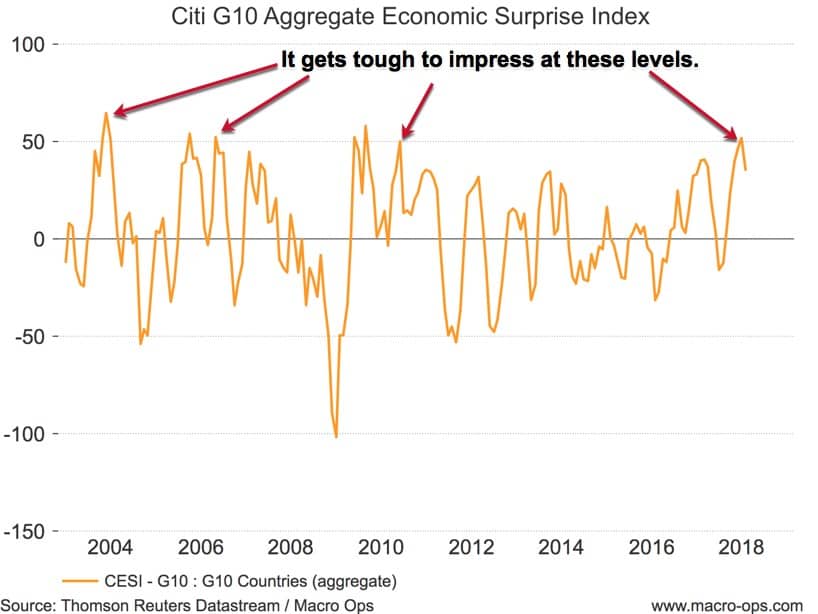

The Citi Economic Surprise Index (CESI) composite for all the G10 countries has hit a point that typically precedes reversion. This index measures economic expectations against the actual results. So when data surprises to the upside the orange line moves higher and vice-versa for when it disappoints.

It’s a naturally cycling index as expectations lag and react to data until narratives evolve, overshoot, until eventually the data begins surprising to the otherside.

Now expectations are high and though the data is strong, expectations might have gotten ahead of themselves. And we’ll likely see this index swing back below.

When CESI falls, bonds and the dollar tend to perform well as investor uncertainty grows and risk gets repriced.

This doesn’t mean the reflation scenario is dead. It just means that a near-term expectations adjustment is probable. The bar has become perhaps too high for this narrative to stay dominant over the short-term and needs to be lowered some.

We want to be like the macro hedge fund manager who went by the pseudonym “The Philosopher” in Drobny’s book Invisible Hands who said:

While most pundits and many market participants try to decide which potential outcome will be the right one, I am much more interested in finding out where the market is mispricing that inflation will go to the moon, then I will start talking about unemployment rates, wages going down, and how we are going to have disinflation. If you tell me the markets are pricing deflation forever, I will start talking about the quantity theory of money, explaining how this skews outcomes the other way. Most market participants I know do not think in these terms. The market is extremely poor at pricing macroeconomics. People always talk about being forward looking, but few actually are. People tell stories to rationalize historical price action more frequently than they use potential future hypotheses to work out where prices could be.

We always want to think about the narratives currently being priced in and weight these expectations against disparate possibilities of alternate futures. This allows us to identify repricings and that means trends…

Deflation Scenario — China and The Global Liquidity Suck

Macro hedge funder Felix Zulauf laid out the bearish deflationary scenario a few months back on the Master’s in Business podcast. Lucky for us, Kevin Muir of MacroTourist transcribed the talk. Here’s an excerpt from it that which sums up this thesis well (emphasis mine).

China I believe is in an interesting position right now. You heard President Xi’s speech last week, and in 2021 there is the 100th anniversary of the Chinese Communist party and it’s very clear that they want to have a strong economy at that time. If you want to have a strong economy in 2021, you stimulate in 2020. And they are central planners. So that’s means they have to take their foot off the pedal in 2018, 2019. I think in ‘18 and ‘19, they will address the imbalances in the financial sector and that will slow down the Chinese economy in ‘18 and ‘19, which will also slow down the rest of the world.

So we are entering a period where sometime in ‘18, I would say the peak of the market will be in the first half, the peak in the economy is probably from mid-2018 on, and then we slow down into 2020.

And 2022 is the next Chinese Congress, and President Xi is probably the first leader who tries to run for a third time. So he wants to have a very good economy in 2021 and 2022. That means he has to first slow things down, restructure some of the imbalances in the system because if he tries to carry through, it could backfire on him. It could be the worst of all worlds. Namely a completely overheated situation, with high inflation rates, etc…

That’s why I think the leader of this cycle, China, is going to slow down next year.

We recently heard news of China’s President Xi Jinping moving to end presidential term limits, making him the de facto Emperor Ruler. So Felix was on the mark with that call… though I don’t think this has surprised many China watchers.

But the idea that Chinese Communist Party (CCP) may be moving to deleverage the economy and take their foot of the pedal in order to prime it for a 2021 liftoff, is an interesting one. It certainly seems plausible and the recent tone taken by Xi and the party over combating gross financial speculation and leverage seems to fit. Recent moves such as the decision to nationalize Anbang, China’s 2nd largest “insurance company” (aka leveraged WMP ponzi scheme) help bolster this view.

Some of the incoming data out of China also gives weight to this idea.

For instance, China’s PMI just printed its worst drop in seven years and is now near the zero growth level (50 marks breakeven growth).

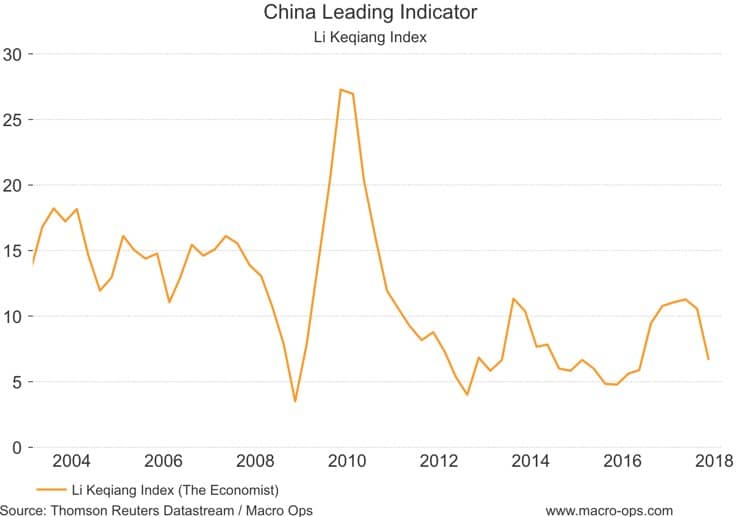

The Li Keqiang Index. An index that measures China’s economic health by compiling electricity consumption, rail cargo volume, and loan growth. Has rolled over and is officially nearing “that’s probably not good” territory.

China’s credit impulse, which was a key driver of the global recovery that began in 16’, has been trending lower. Jurrien Timmer of Fidelity, the author of this chart, noted in an accompanying tweet how China’s economy “tends to run in two-year cycles” which we can see in the chart. That means we should see its credit impulse continue trending lower. And possibly drag commodities down with it.

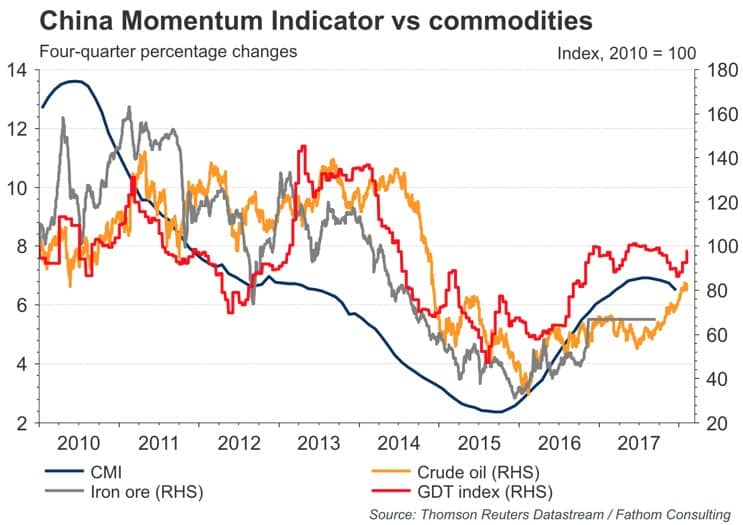

Fathom’s China economic momentum indicator, which leads GDP, is also rolling over. The trend in this indicator tends to persist for sometime once it gets going.

And this indicator is highly correlated to commodities, for obvious reasons.

If this scenario plays out it’d be bearish for commodities, bullish for bonds and safe assets, and if not straight out bearish for global equities it’d certainly raise the heat on volatility going forward.

Felix noted in the interview that (again, via MacroTourist), “You always need to figure out what is the leading theme in the market cycle. In the last cycle, it was real estate, in this cycle it is China. And that’s why China is so important.”

I agree with Felix that China is one of, if not the, main driver of the macro story currently. His idea about them moving to deleverage now in order to set them up for their big 100th is certainly plausible and the current data along with CCP talking points, gives credence to it.

With that said, the one stop gap to this scenario getting too bearish, is that the CCP prizes stability over everything else. The survival of their political regime absolutely depends on it. They know this all too well. This forces them to be short-sighted. And they’ll no doubt open the credit floodgates if things get too bad.

A slow and heavily managed growth decline is much more likely than a full-blown credit crisis. That means we’ll probably continue to see Chinese data whipsaw back and forth going forward. Never getting too bad nor too good.

Middle Road Scenario — A Little reflation, A Little Deflation, Some Higher Volatility and a Stock Pickers Market

I give this scenario the highest weighting currently. It boils down to a continuation of the bull market in stocks. But with volatility picking up and greater dispersion between various market and asset returns. Essentially, I expect that, unlike last year, we’ll see a lot more losers but still plenty of winners.

I also believe there’s the potential that the US stock market will lead the way, with relative momentum in the US picking up. At least for some time.

The recent tax changes are bringing back a tidal wave of foreign held cash. This cash is going to go to Capex, buybacks, dividends, and M&A.

The buybacks should put a persistent bid under the US market. Especially with the dearth of new issues in the still tepid IPO market there’s the increasing likelihood we start to see an asset shortage (more money chasing fewer securities) in the year(s) ahead. This could really cause a melt-up scenario in US stocks. And with the temporary boost to the real economy there’s the potential we see a growth flywheel kick into effect here in the US.

The earnings momentum in the US has hardly ever been higher. While at the same time, earnings momentum appears to be slowing somewhat in the other advanced economies.

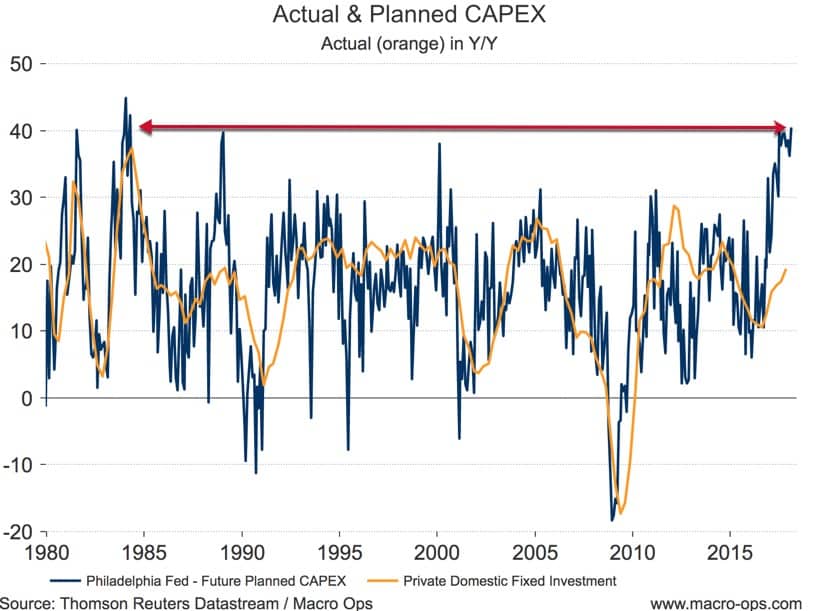

Look at the chart below showing planned and actual capex. The last time planned capex was at these levels I was in my first year of life and The Gipper was in office.

Under this scenario a number of interesting macro trends would unfold. Leading to significant reversals in some assets and the acceleration in trend in some others.

This scenario would reward stock selection over passive indexing. And various liquidity and momentum indicators point towards a few certain sectors in the US market along with some select companies that look ready to run under this setting.

This is what we’ll be covering in March’s Macro Intelligence Report (MIR). We’ll be diving into the Middle of the Road scenario and covering which sectors and which stocks are best set to thrive in the not too hot, not too cold macro regime.

If you’re interested in keeping up with this dynamic macro environment with us, subscribe to the MIR by clicking the link below and scrolling to the bottom of the page:

Click Here To Learn More About The MIR!

There’s no risk to check it out. We have a 60-day money-back guarantee. If you don’t like what you see, and aren’t able to find good trades from it, then just shoot us an email and we’ll return your money right away.

The dominant macro narrative is changing quickly. #PeskyPowell ain’t Janet Yellen. Don’t miss your chance to take advantage..

Click Here To Learn More About The MIR!