Remember, you don’t get any money just because you know why the market is going up or down. You only get money if your plan has positioned you to capitalize on the market’s movement, regardless of whether you know why the market is up or down on a particular day. ~ Jim Paul, “What I Learned Losing a Million Dollars”

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at net share issuance and buybacks, compare this era to that of when FDR was in office, dive into the Ag market, corn demand, soft commodity positioning, and what this means for inflation. We then end with a bullish setup in the cannabis space, plus more…

Let’s dive in.

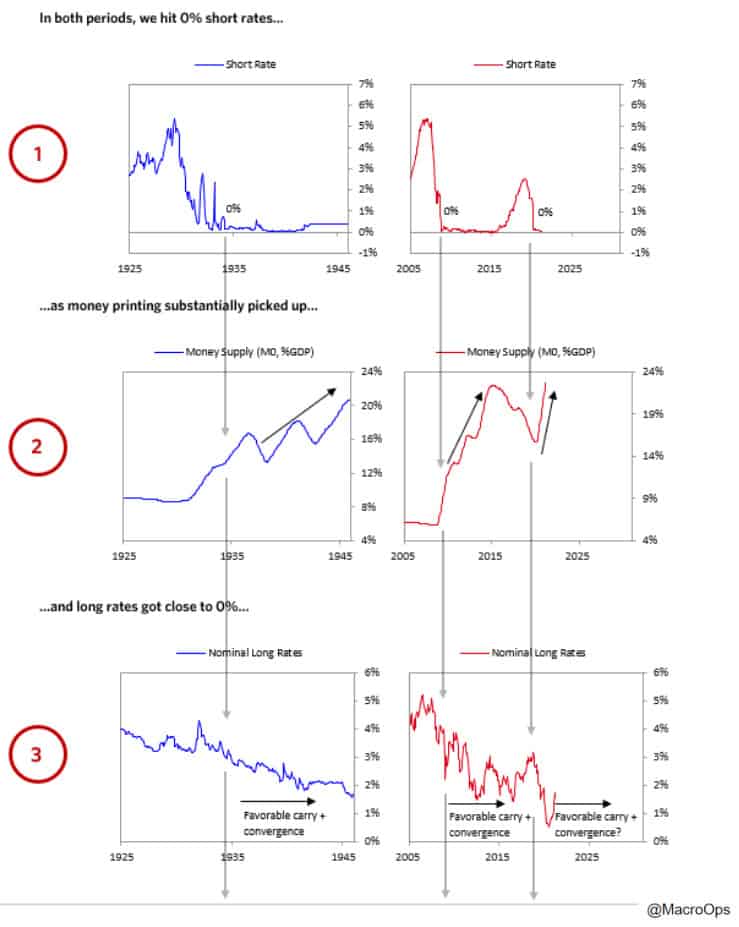

- Ray Dalio published a short piece (link here) last week where he compares the Biden administration as well as today’s economic environment to FDR and those of the 30s. There are no doubt a number of similarities, as well as differences. But one thing is clear, we’re moving back into an era of big government.

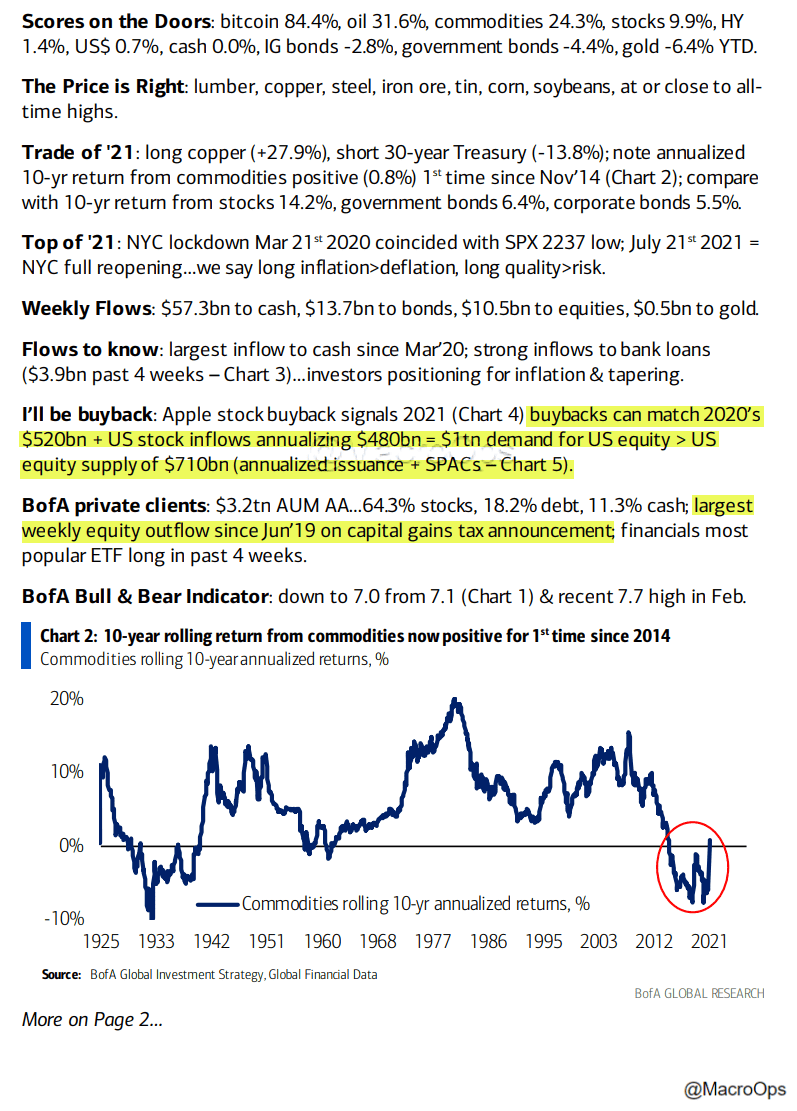

2. BofA notes in their latest Flow Show report that the acceleration in buybacks and stock inflows should be greater than the annualized new supply of shares (highlighted in yellow). Long-time MO readers know that the Equity Supply & Demand Equation is a critically important thing to watch. So on the surface, this is a positive but what they don’t account for is the fast-growing supply of crypto which is diverting flows from equities. I have a Market Note on this topic going out tomorrow.

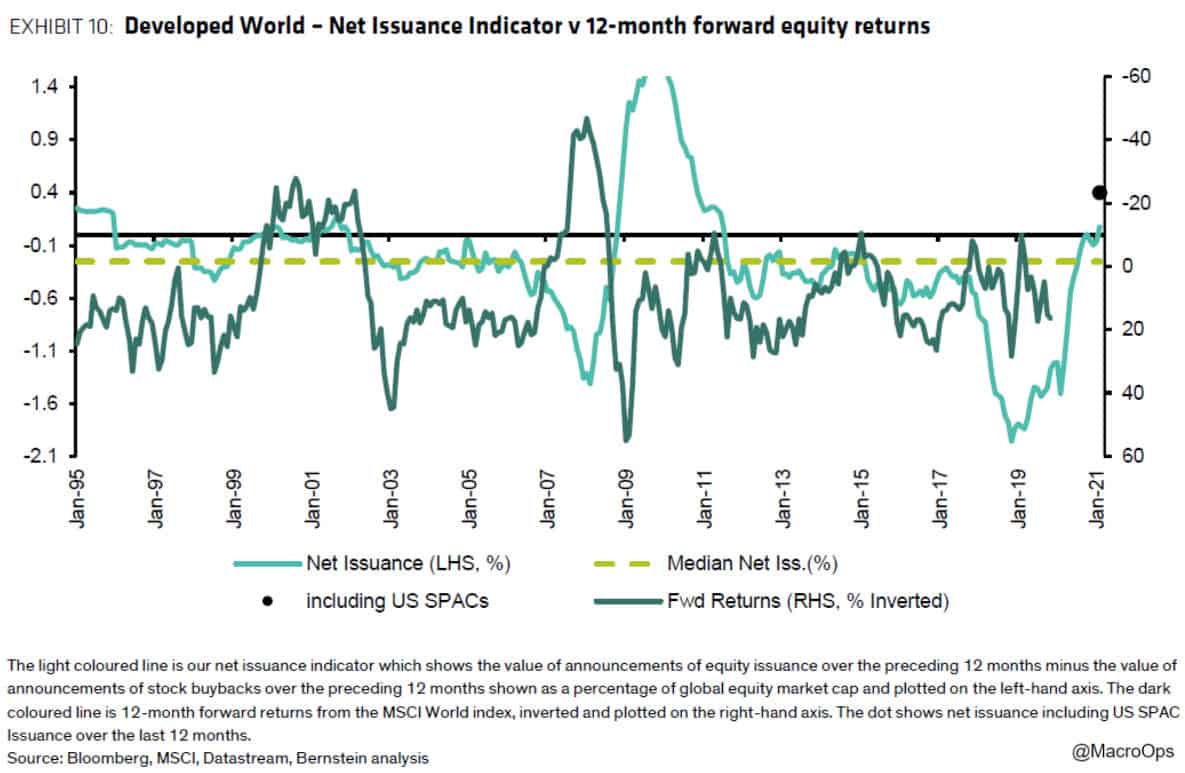

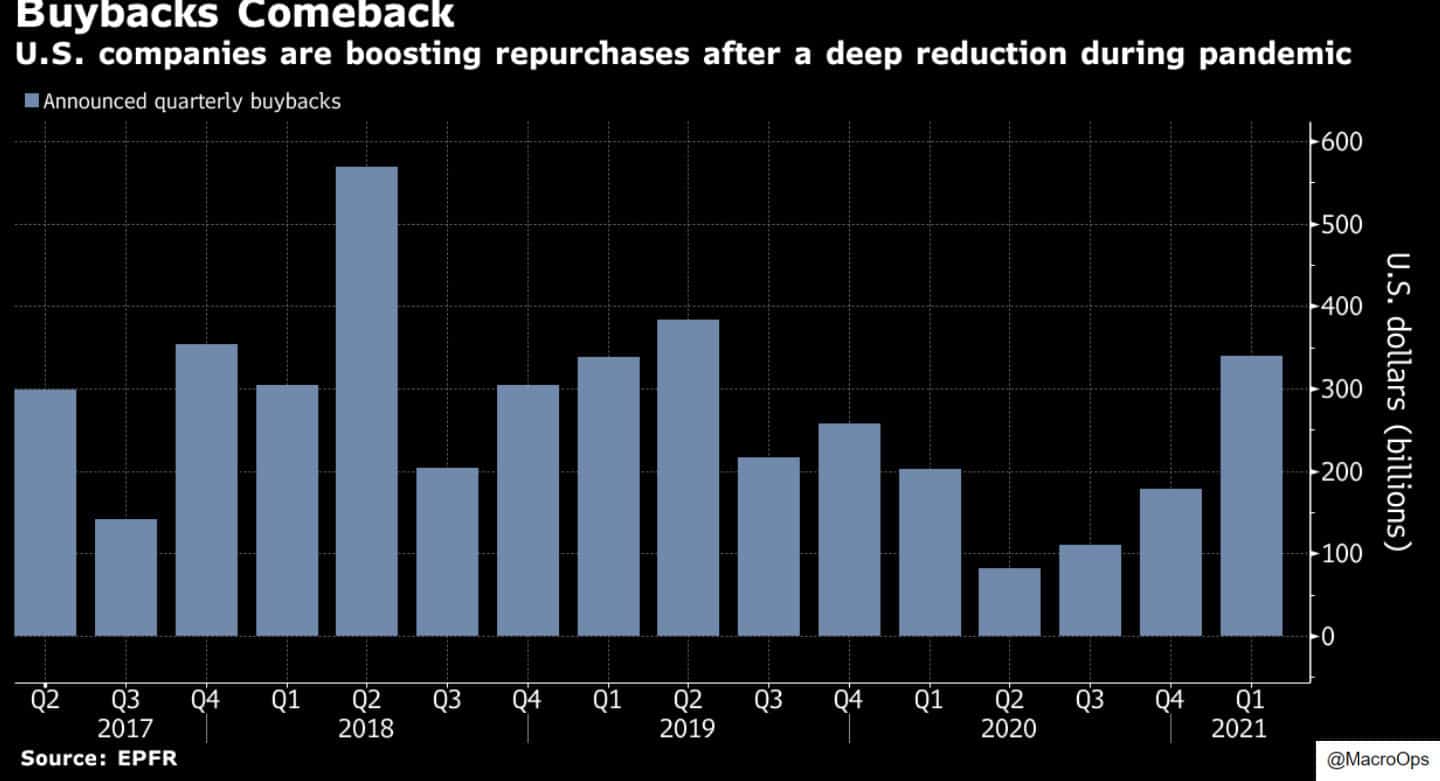

3. This chart from Bernstein shows that developed world net issuance is at levels not seen since the GFC. Though things are a bit different in the US where announcements like AAPL’s $60bn buyback authorization last week, are helping to return quarterly buybacks back to pre-pandemic levels.

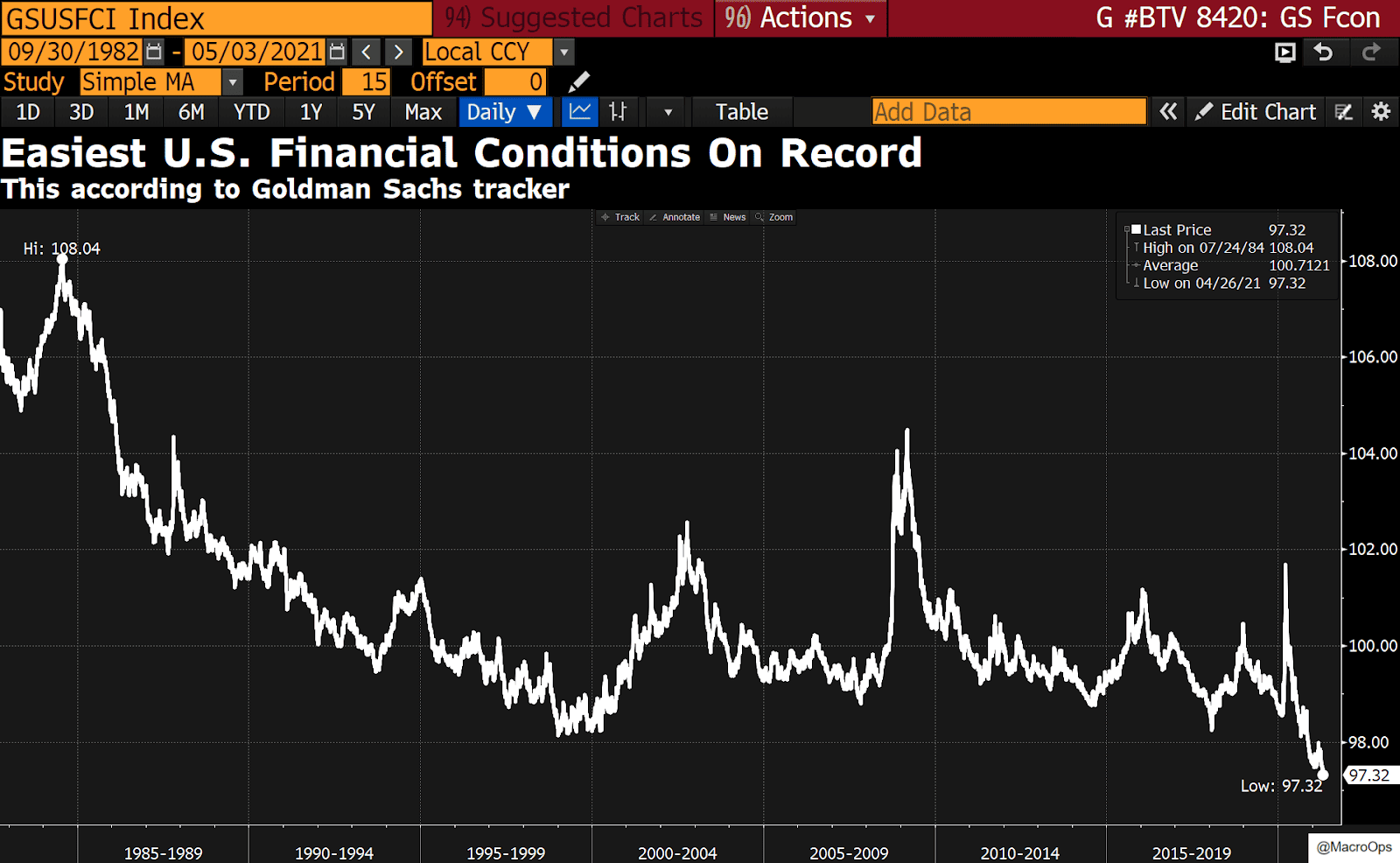

4. With financial conditions the loosest they’ve ever been, it’s plenty easy for companies to borrow to buy back these shares.

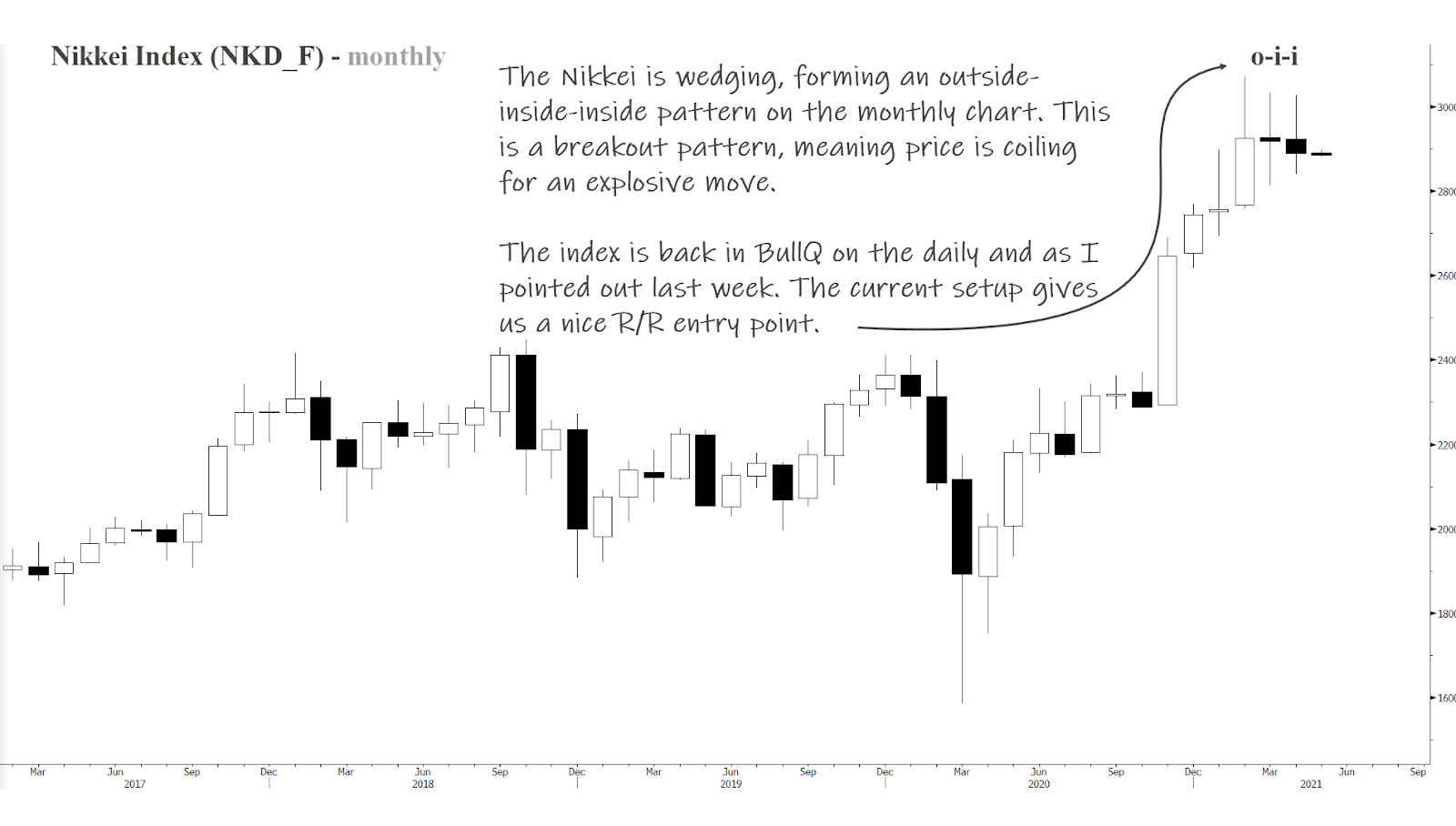

- The end of April brings us new monthly charts to look at. The big takeaway from looking at global equity markets on the longer-term timeframe is that that path of least resistance is up… With that said, things are certainly getting stretched and we’re firmly in the Climatic phase of the Buy Climax, though these can and often do go on longer than most expect. One of many great-looking monthly charts is Japan’s Nikkei Index. The chart is coiled on the monthly, having formed an outside-inside-inside pattern. This is a breakout pattern. My bet is it sees a strong break higher here.

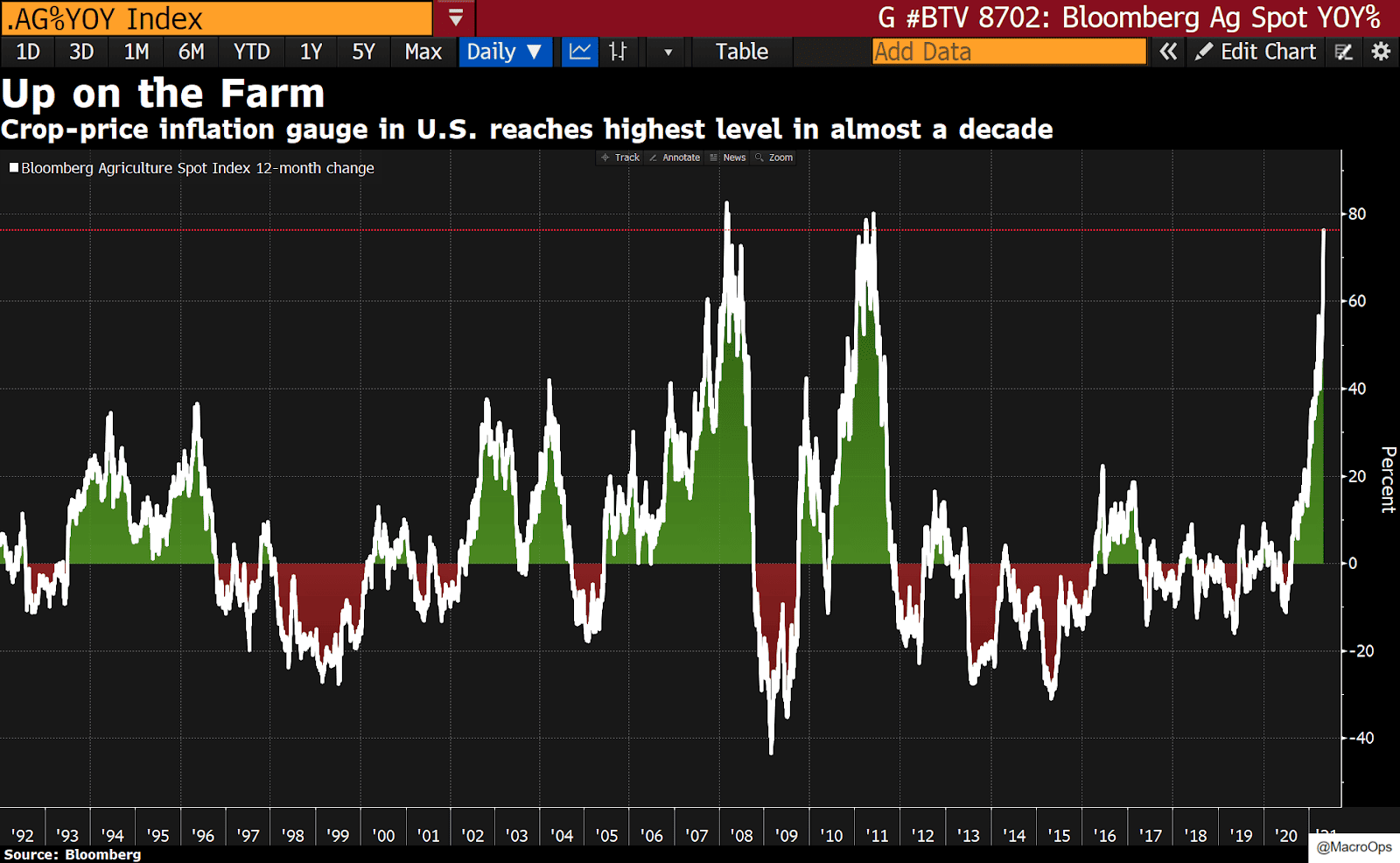

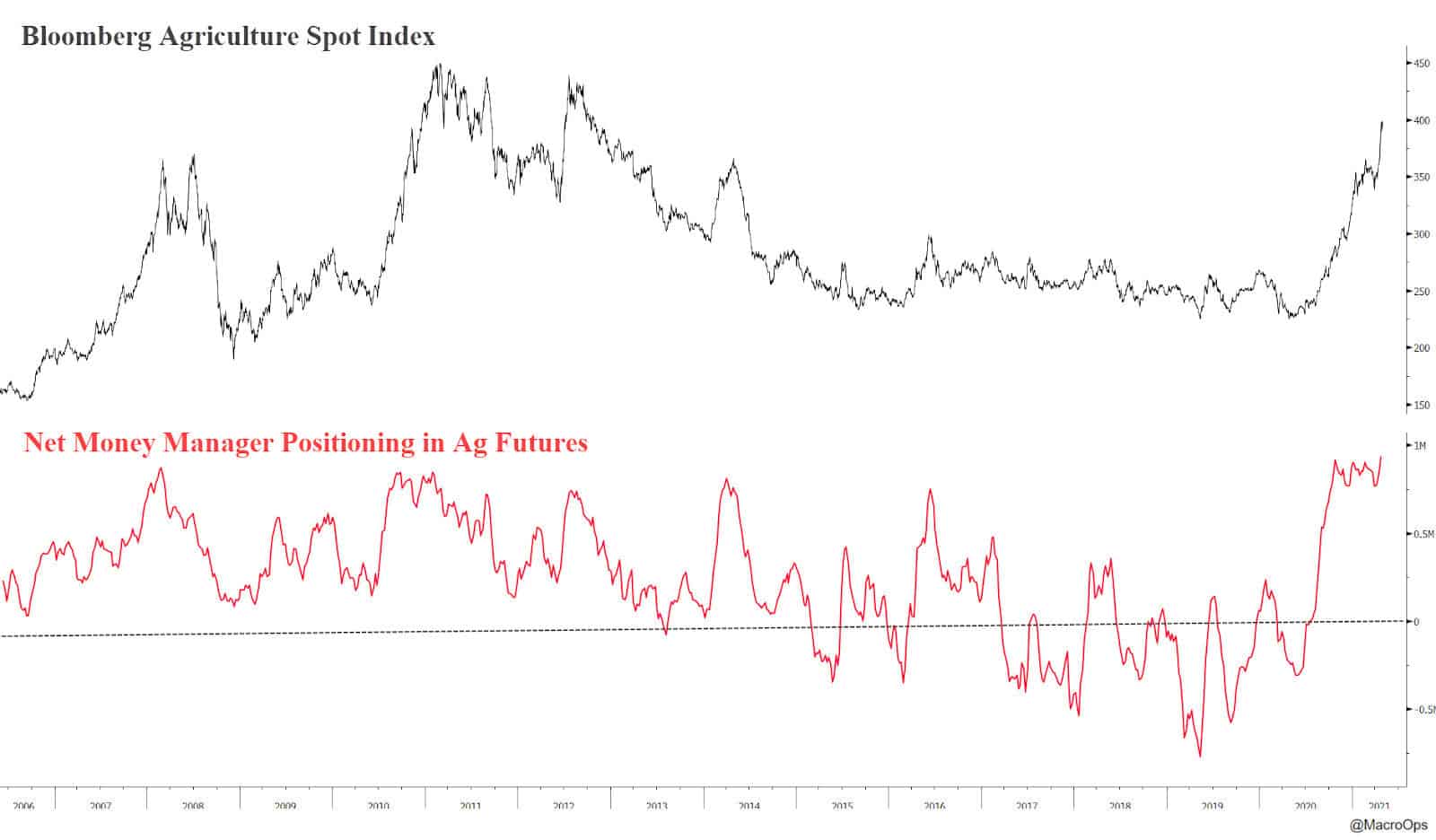

- Ag prices have been on a tear as seen on the chart below showing the 12m change of the Bloomberg Ag Spot Index. Two things to take away (1) It would be anomalous if Ag prices continued at their incredible pace higher from here and (2) there’s a lot of chatter about how this means inflation is coming but that was also the case in 10’/11’ when Ags had been on a similar run and we all know how that ended.

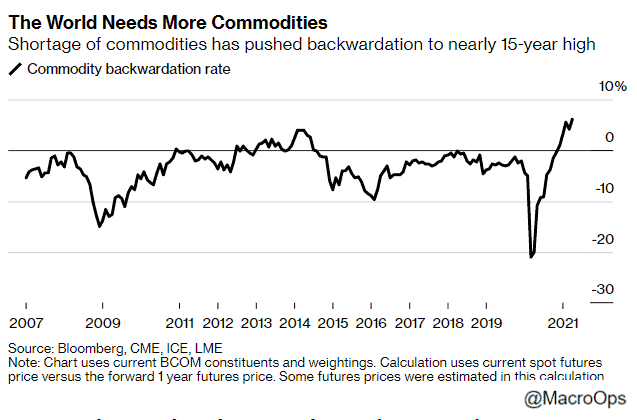

7. The quick flip in global demand for commodities has driven the aggregate commodity curve to its highest level of backwardation since at least 2007.

- The majority of this demand is coming from China where a shortage of supplies, a big inventory restocking, and a need to replenish hog herds following a bad case of African swine fever is forcing them to import a record amount of corn. According to BBG, the above has pushed China’s corn imports to 28 million metric tons. Making it the “most on record based on Bloomberg data going back six decades.” The country is expected to cut these import levels next year by 15 million tons but that will still be the 2nd largest amount on record.

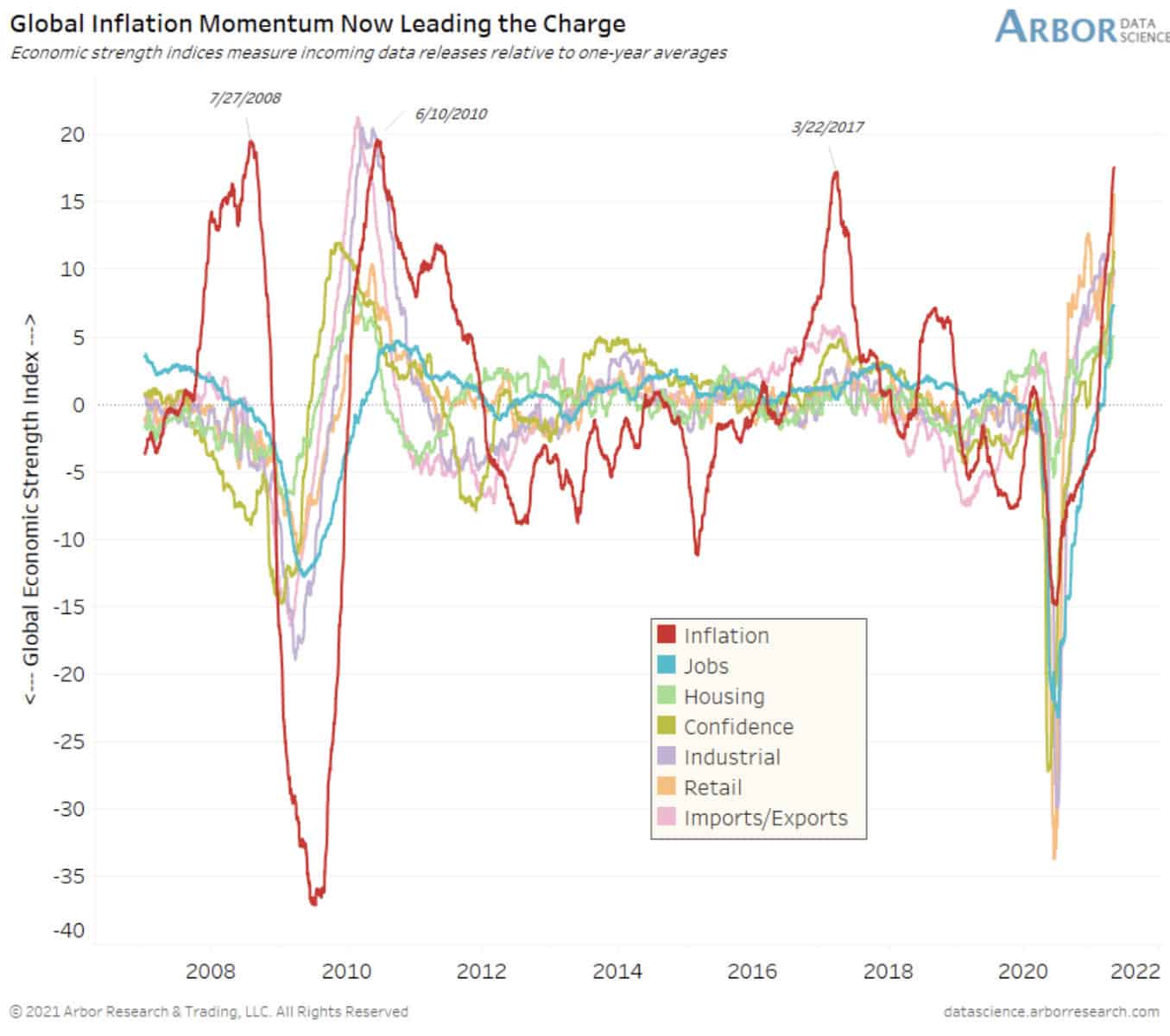

9. Global restocking, as well as COVID-induced bottlenecks, have driven inflation momentum to extremes. @benbreitholtz of Arbor Data Science points out that “Inflation expectations (i.e. TIPS Breakevens) struggled over the ensuing months after each of these instances”.

- We remain long this reflation trade because momentum and trend say to do so. But looking at extremes like the above along with those we’re seeing in positioning, I can’t help but think we’re nearing a local peak that will lead to a bit of a breather. Net aggregate money manager positioning in Ag futures is at record highs.

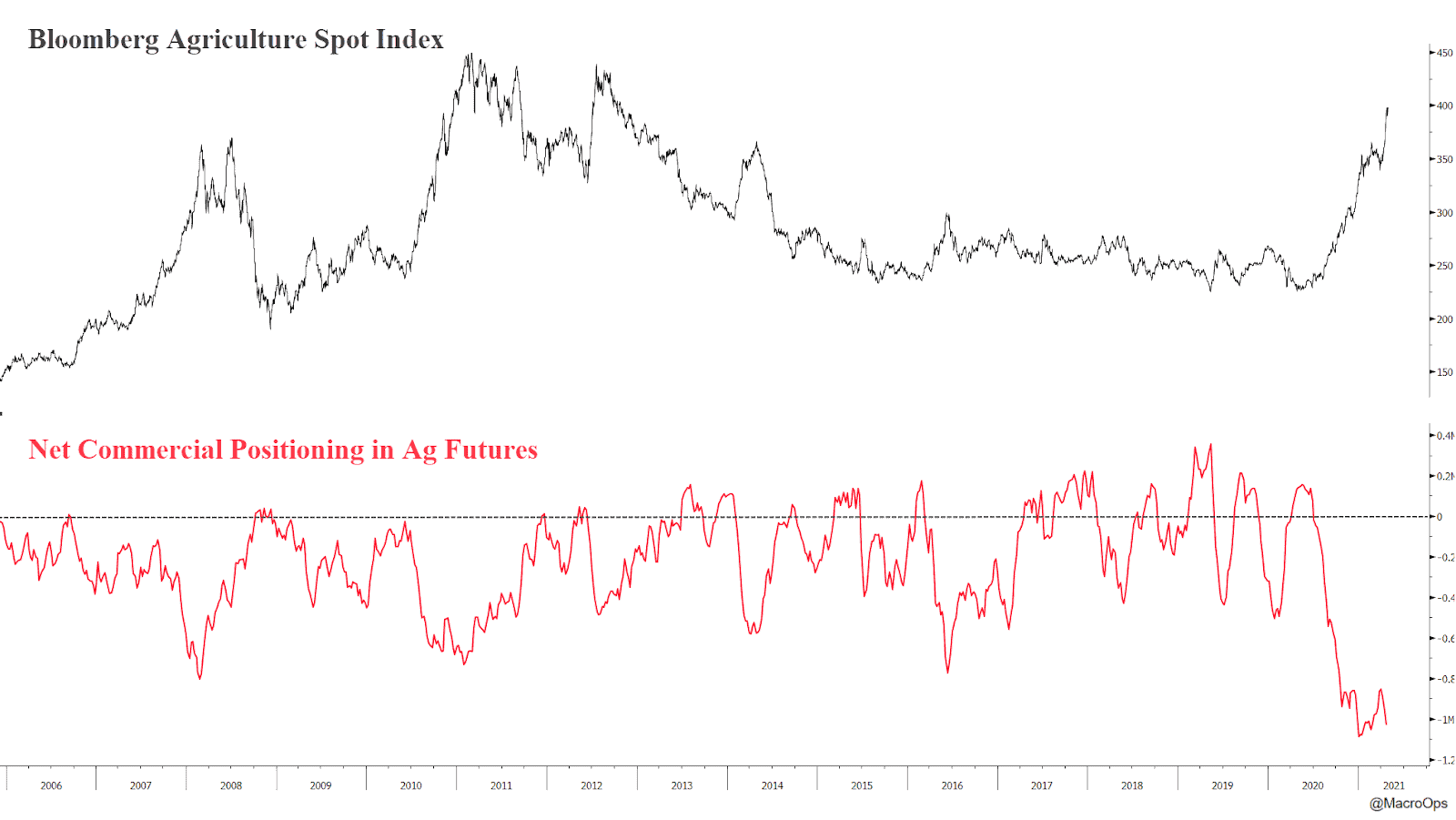

11. And commercials are holding record shorts…

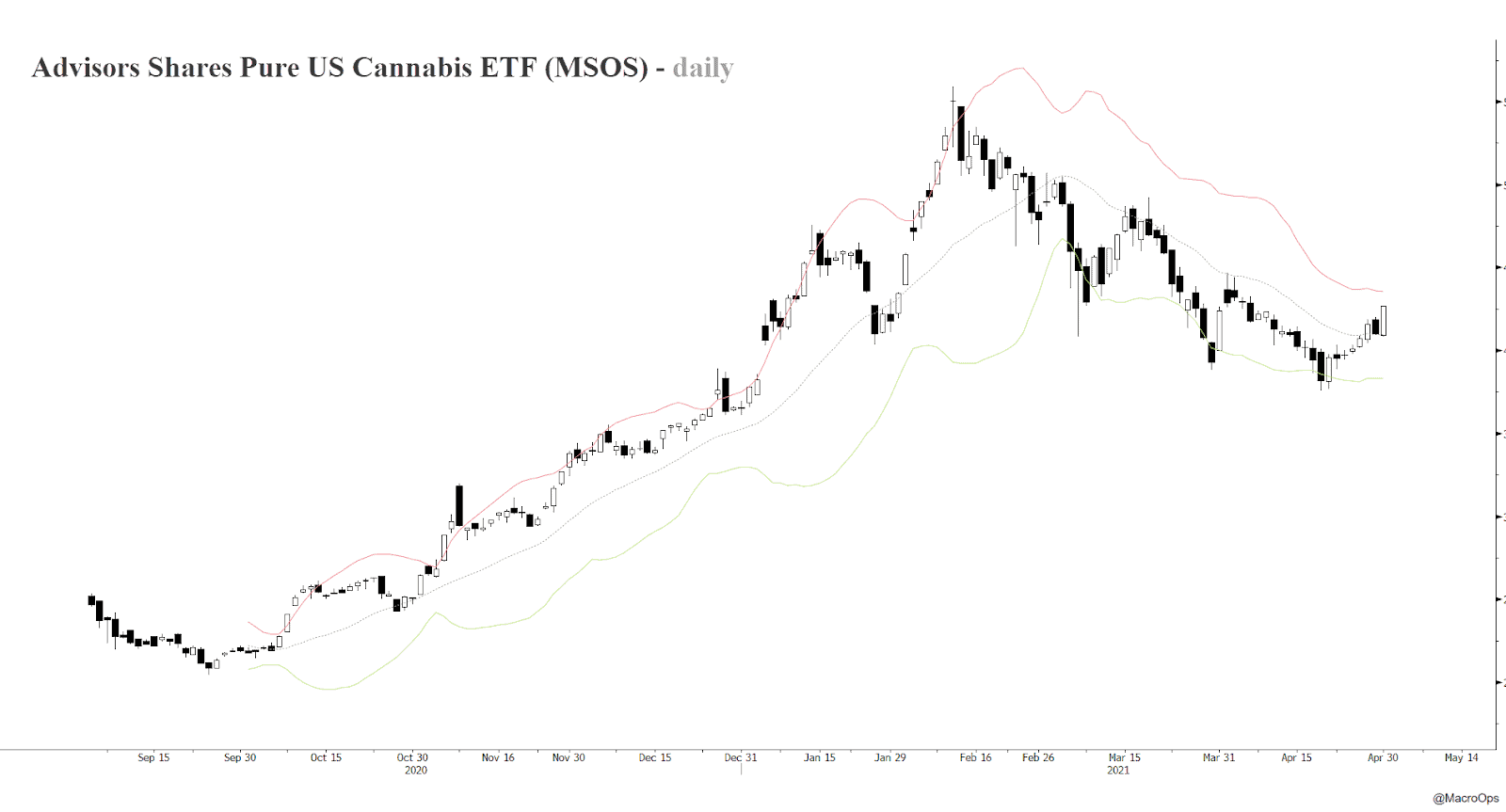

12. Cannabis plays are making a comeback. I’m interested in US multi-state operators with a lock on their regional markets. MSOS is a great play for this as its heaviest weighted names meet the above criteria. The fundamentals are increasingly bullish for this industry and the technicals are lined up. I’ll be putting out a report to the Collective later this week, outlining the bull case along with a few of my favorite names.

Stay safe out there and keep your head on a swivel.

Stay safe out there and keep your head on a swivel.

Your Macro Operator,

Alex