The following is straight from Operator Jose, a member of the Macro Ops Hub.

The Corn to Soybeans Ratio is very important to American farmers. In normal conditions, it’s a key factor that helps them decide how much Soybeans or Corn they’ll put into the ground. Both crops compete for the same acreage area. I like to think of it like this:

Farmers have a portfolio, but instead of money, they have acreages. There are two assets they can choose to invest in. Either Corn or Soybeans. This key decision is ASSET ALLOCATION. Whether they want more exposure to Corn prices, or prefer holding more Soybean bushels, depends on many factors, but price is a big one.

Farmers can check, even months prior to the harvest, how much money they’ll receive for every bushel they pull from the ground. This is done by evaluating the relationship between the Corn and Soybean futures that’ll be trading by harvest time.

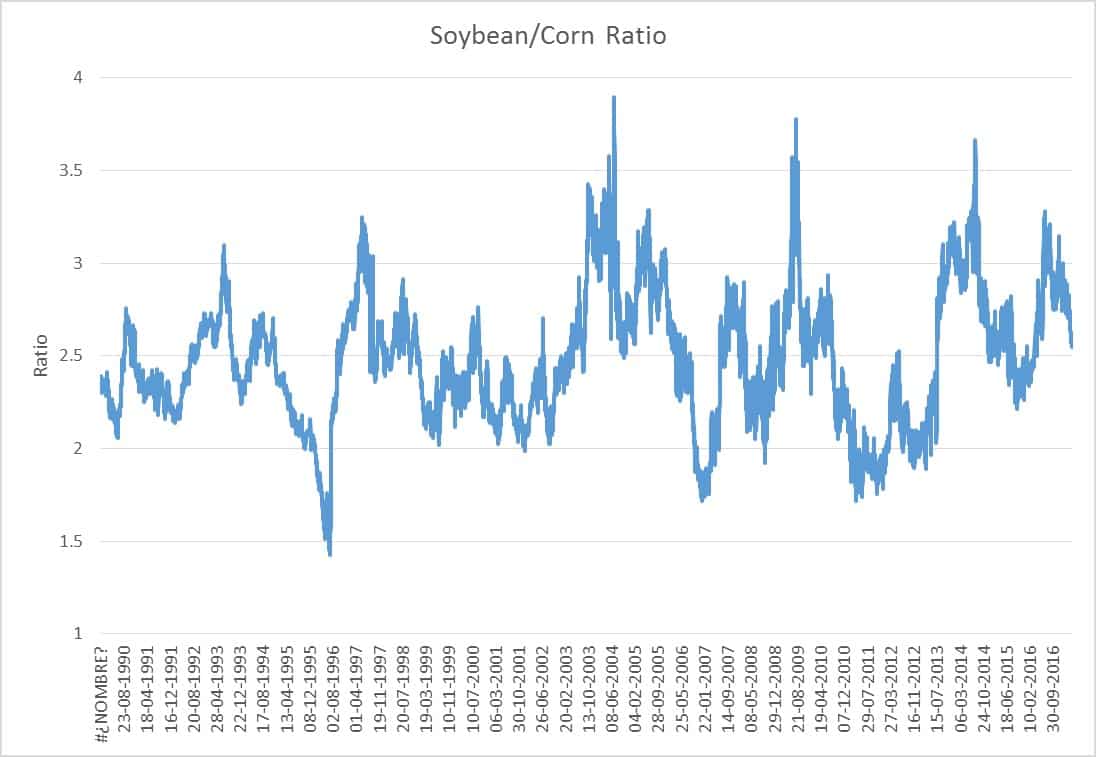

Here´s the long-term relationship for the front month futures:

The ratio is Soybeans over Corn. Whenever the ratio is over 3, farmers get 3 times more money for every Soybean bushel than Corn. Sometimes the ratio goes crazy due to weather risk and supply imbalances, but in normal conditions it shouldn’t be over 3.

Whenever the ratio is over 3, farmers plant a heck of alot more Soybeans than Corn. And by the laws of supply and demand, this will eventually cause the ratio to go down as Corn becomes scarcer relative to Soybeans.

The best way to play this relationship is through a spread trade. You can use one contract of Soybeans per two contracts of Corn. This means you’ll have 5,000 bushels of soybeans and 10,000 bushels of corn on a notional basis.

If we’re bearish on the Soybean/Corn spread, meaning we think corn prices will rise relative to soybean prices, we’ll need to short one contract of Soybeans, and go long two contracts of Corn. If bullish, meaning we think soybean prices will rise relative to corn prices, we do the opposite — buy one contract of Soybeans and short two contracts of Corn.

You’ll notice that this chart is very similar to the previous spreads chart, but the Y-axis is now quoted in points instead of in a ratio. Every point on the Y-axis is worth $50 per the spread trade.

The reason we use a spread instead of playing the commodity straight up is to hedge weather risk. Weather is THE principal risk factor in grain commodities. Weather produces a largely asymmetric effect: while bad weather alone could completely destroy a crop yield, good weather by itself won’t produce a bumper harvest. Good weather is just one factor involved in a successful growing process. By taking the spread we’re strictly betting that Corn futures will do better than Soy futures no matter the other general conditions. Weather risk is partially hedged.

I´m bearish on the Spread. Here are the fundamentals that support my theory:

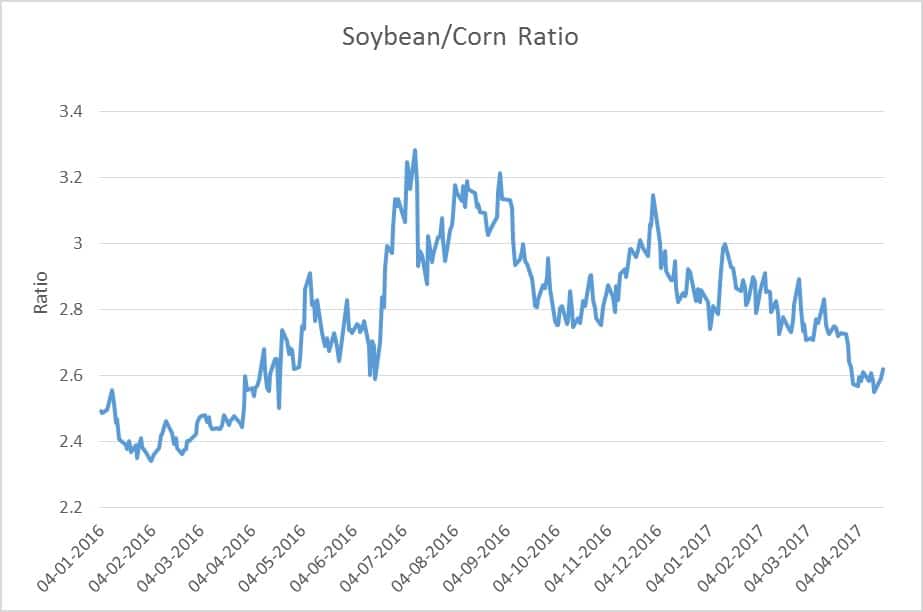

The chart below shows how the Soybean/Corn ratio went over 3 last year when farmers planted too much Corn relative to Soybeans (Soybeans became scarce and therefore fetched a higher price). Since December the ratio has been falling.

The ratio didn’t do much in February and March other than consolidate. But at the end of March the USDA released the Prospective Plantings report. This report shows how many acreages farmers intend to commit between Corn and Soybeans. The keyword in this report is “Intention”. Following our portfolio analogy, the farmers are telling you the percentage of their portfolio they’re willing to invest in Corn or Soybeans.

But keep in mind that the grains aren’t in the ground yet. These farmers can change their planting intentions. There’s currently a small portion of Corn being planted right now, but there’s still time to switch acreages in later stages. Farmers aren’t forced to stick to what they reported in the prospective planting report.

On March 31st the report was released showing a decline in Corn acreages of 4% and an increase in Soybean acreages of 7%. Less Corn supply means each kernel is worth more. And more Soybeans means each is worth less. This confirmed my bearish bias on the spread. All that was left was price action to follow.

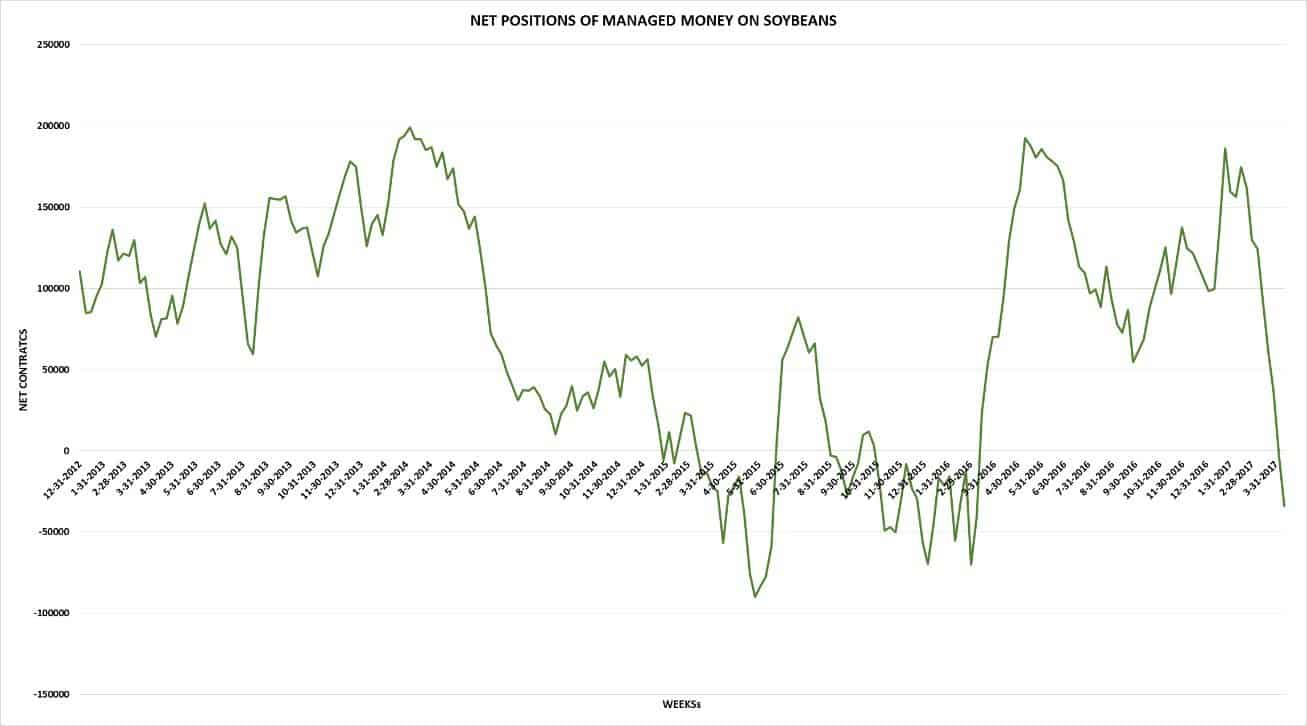

What do you think the big funds did on the day of the report? They shorted 11,000 contracts of Soybeans… and went long 20,000 contracts of Corn… a big 10,000 spread trade.

Amazing! It was almost like forecasting the future….

Here´s a chart with the Net Contracts position of Managed Money in the Soybean market. Notice the downtrend. They are finally net short!

The spread went from around 230 per bushel to 168 — a 27% move in 7 days. Report day was the biggest red candle of almost 30 points.

I believe there’s still downside potential to this trade. Price has retraced almost completely since the day of the report, and as I said, I don’t think the market has fully discounted a big soybean crop this year. And if you check the long-term historic spread, there’s still downside potential.

I am short the New Crop Spread ZSX17- 2*ZCZ17 (Short 1 November Soybean Future and Long 2 December Corn Futures.) These are the futures at harvest time when the market should be overflowing with Soybeans relative to Corn.

To learn more about how we trade at Macro Ops, click here.