Our Value Investing Letter Recaps keep things simple.

Each email focuses on three value investing hedge fund letters, three ideas, all digestible in roughly three minutes.

Within each idea we answer four main questions:

- What does the business do?

- Why is it a good bet?

- Why does the opportunity exist?

- What is the prize if you’re right?

Quick housekeeping note that nothing you read is investment advice and please do your own due diligence before investing. Also, I do not own any of the below-mentioned securities as of this writing.

Finally, we get each investment letter from r/SecurityAnalysis, which you can find here.

This week we analyzed Asbury Automotive (ABG), RCI Hospitality (RICK), and Verra Mobility (VRRA).

**Note: Enrollment to the Macro Ops Collective will be open until the end of this week.

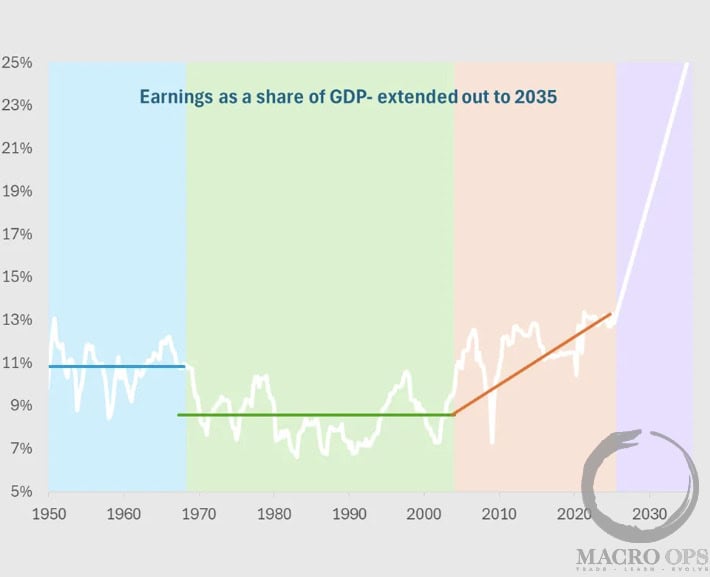

Yesterday we shared a premium report that explained our new baseline inflation rate and how its impact will create drastically different markets from the past 30+ years. Here it is again if you missed it: What Really Drives Cyclical Inflation [Part 1]. Keep an eye on your inbox for part 2 tomorrow.

This report was previously only available to our Collective members. If you’d like to join us to ensure your portfolio is protected in the coming year, enroll in the Macro Ops Collective. We’ll be shutting down access Sunday, January 1st at midnight.

Alright, back to the investor letters!

Top 3 Value Investing Letters You Need To Know About

1. Bonhoeffer Capital: Asbury Automotive (ABG)

Keith Smith runs Bonhoeffer Capital and is a frequent feature in our Value Letter Recap Series. The Bonhoeffer Fund returned -13.7% in Q3. We’ve covered one of Keith’s ideas, Ashtead (AHT), in a prior recap. And you can read the Q3 letter here.

This week, we’re examining another one of Bonhoeffer’s holdings, Asbury Automotive (ASB).

Let’s get after it.

What does ASB do?

Via TIKR.com: “ASB is an automotive dealership. It offers a range of automotive products and services, including new and used vehicles; and vehicle repair and maintenance services, replacement parts, and collision repair services.

The company also provides finance and insurance products, including arranging vehicle financing through third parties; and aftermarket products, such as extended service contracts, guaranteed asset protection debt cancellation, prepaid maintenance, and credit life and disability insurance.”

Why is it a good bet?

“Over the past 10 years, Asbury’s net income margins are up 120% with a 5x increase in revenues. These factors should lead to about a 20% EPS growth going forward.

Asbury has the highest margins (due to local clustering) and inventory turns when compared to US companies, leading to high returns on equity of 33% to 41% over the past five years.”

Why does the opportunity exist?

“What complicates the outlook going forward is Asbury’s growth plan and the cyclicality of the auto dealership business.”

What is the prize if you’re right?

“Given a conservative projected EPS growth of 5% per year, Asbury should trade at 19x earnings using Graham’s formula of 8.5 + 2 * growth rate. Applying this multiple results in about a 4x return today and an 8x return in five years.”

Further Research Material

2. Bireme Capital: RCI Hospitality (RICK)

This is Bireme Capital’s first appearance on the Value Letter Recap series. Bireme runs a Fundamental Value fund that’s absolutely crushed the market. Since inception (in 2016), Bireme has returned 22.7% net annually, versus the SPY’s 12% annual return.

You can read its Q3 letter here.

This week we highlight one of their long ideas – and a FinTwit favorite/battleground stock – RICK.

What does RICK do?

Via TIKR.com: “The company owns and/or operates upscale adult nightclubs serving primarily businessmen and professionals. It also operates restaurants and sports bars under the Bombshells Restaurant & Bar brand, as well as a dance club under the Studio 80 brand.”

Why is it a good bet?

“Even after this strong performance, RICK trades at only 14x earnings — a reasonable valuation for a company which we expect will continue to grow rapidly in the years ahead.”

Why does the opportunity exist?

“The nightclub business is performing extremely well, with T12 revenues at June quarter end up 72% YoY, benefitting from a sizable acquisition completed in late 2021. T12 operating income in the segment was $67m, up 81% vs last year and 35% above the peak level pre-COVID.

The restaurant segment, which consists of the military-themed “Bombshells” restaurants, did $60m of sales and $12m of operating income over the past year. The concept has significant growth potential, with only eleven locations open and four more already under development.”

What’s the prize if you’re right?

Me: Analysts expect RICK to generate ~$50M in FCF by 2026. Assuming a 15x FCF multiple you’re looking at a $750M shareholder value, which is lower than the current market cap. For the bulls to win from here, RICK needs to either generate substantially more FCF over the next few years or they’ll need a higher re-rating from the market.

Further Research Material

3. Tourlite Capital: Verra Mobility (VRRA)

Jeffrey Cherkin runs Tourlite Capital Management, a long/short value-based hedge fund. This is Tourlite’s first appearance on the Value Letter Recap Series. You can read its latest quarterly letter here.

This week we’ll break down one of Tourlite’s long ideas, Verra Mobility (VRRA).

What does VRRA do?

“Verra Mobility is a leader in transportation technology. The business has three segments: commercial, government and parking. The commercial and government segments represent 85%+ of revenues.”

Why is it a good bet?

“Verra is an attractive business with mid-to-high single digit revenue growth and sustainable competitive advantages …

Verra is integrated with tolling authorities and has a revenue split with rental car operators. The business should benefit from two key tailwinds including the continued shift from cash to cashless tolls and conversion of highways to toll roads …

The Government segment offers solutions to cities and school districts including red-light, speed and bus lane camera enforcement. Most of these relationships are revenue shares and Verra maintains ownership of the hardware/cameras.”

Why does the opportunity exist?

“Currently ~65% of toll booths are cashless and that is expected to grow to over 80% over the next few years … Most of these [government] relationships are revenue shares and Verra maintains ownership of the hardware/cameras.”

What is the prize if you’re right?

“Based on our projections for 2023, Verra trades at over a 7.5% free cash flow yield.”

Further Research Material

Wrapping Up This Week’s Value Investing Letters: What To Read Next

**Note: Make sure to sign up for the Macro Ops Collective today. The Collective is our premium service that offers institutional-level research, proprietary quant tools, actionable investment strategies, and a killer community of dedicated investors and fund managers from around the world. Enrollment will remain open until Sunday, January 1st at midnight.

Thanks for reading, and I hope you learned something. If you enjoy this series, let me know by shooting an email or retweeting on Twitter.

Also, please let me know if there’s an investor letter I should read that I didn’t cover here.