“The reason I love studying retail businesses is because it’s so graspable. If you understand very basic business concepts, you can wrap your mind around how these companies can build very strong, very profitable businesses over time. And it all starts with simple unit economics.”

Alex Morris is one of my favorite writers and Twitterers (you may know him as @TSOH_Investing). Morris is a former buy-side analyst, CFA charter holder, and the author of the investing newsletter, TSOH Investment Research Service.

Alex researches (and invests in) businesses that meet his four core criteria (from his site):

- Operates in an industry that is expected to support structural (organic) growth for the company over the next 5-10 years above GDP growth;

- With attractive unit economics and high returns on incremental invested capital (ROIIC) as a result of sustainable competitive advantages;

- Run by individuals with skill, integrity, and a long-term time horizon; and

- Offered to minority shareholders at a reasonable valuation (at a price that is expected to provide better than average equity returns over the long run)

Alex is in the spotlight for this week’s 3 Big Things.

3 Big Things distills all my podcast episodes into bite-sized summaries. Each piece features:

- One Conversation (Stocks, Psychology, Markets)

- One Framework (Mental Model, Analytical, Behavioral)

- One Idea (Long or Short)

Alright, let’s dig into my podcast with Alex Morris!

One Conversation: The Anatomy of Position Sizing

I asked Alex about his biggest struggles as an investor over the last year, and his answer surprised me. It wasn’t about analyzing a business or choosing investments. It was position sizing (emphasis mine):

“Just thinking about how to navigate stock price volatility (like 50% moves). In theory you go, ‘its all just IRRs’ … For me that’s too theoretical … I spend so much time thinking about individual businesses, but its building all that together in portfolio construction that’s more sensible than how I do it today.”

Alex uses his Spotify (SPOT) investment as an example of a more “sensible” approach to position sizing (emphasis mine):

“From out of the gate, SPOT was always a 5, 10, 20 year story for SPOT to reach sustainable profitability and scale. Position sizing in light of that fact, should’ve been more conservative from the beginning. It’s not like investing in Berkshire or Microsoft. Thinking like that informs my position sizing more…

“What you learn in practice is when you own something for those first 1-3 years, and the business results really suck and shake the foundation of what you used to believe and what you should believe. There needs to be some markers in the ground to test the thesis. It can’t be ‘place the bet, and we’ll reassess in Year 20.’”

Position sizing is one of the most important aspects of successful investing. It’s also one of the more challenging.

There is no one size fits all answer. It depends on a number of factors such as personal and LP risk tolerance, portfolio vol and return objectives, investment style, etc…

The point being is that it’s something that needs to be deliberately thought through and not just arbitrarily applied, which is how most investors do it.

You can read more of our thoughts on position sizing here.

One Framework: K.I.S.S Retail Analysis

Alex loves studying and investing in retail companies because they’re “so graspable.” What does he mean by that?

The framework for analyzing retail businesses is straightforward and requires answering only a few fundamental questions:

- How much revenue can each store generate at maturity?

- What is the average per-store EBITDA margin at maturity?

- How many stores can this business operate at maturity?

Yes, there are more questions you should ask before investing in any retailer. But get these three questions right, and you’re 99% of the way to understanding any retail investment idea.

The valuation question is equally as simple. You don’t need spreadsheets or complex formulas. It’s a math problem:

Number of Stores At Maturity * Annual Per-Store Revenue At Maturity * Average Per-Store EBITDA Margin At Maturity = Mature EBITDA

Multiply mature EBITDA by an appropriate multiple, and you have your valuation framework.

I discussed this idea with Alta Fox’s Connor Haley, which you can listen to here. You can also read more about unit economics here.

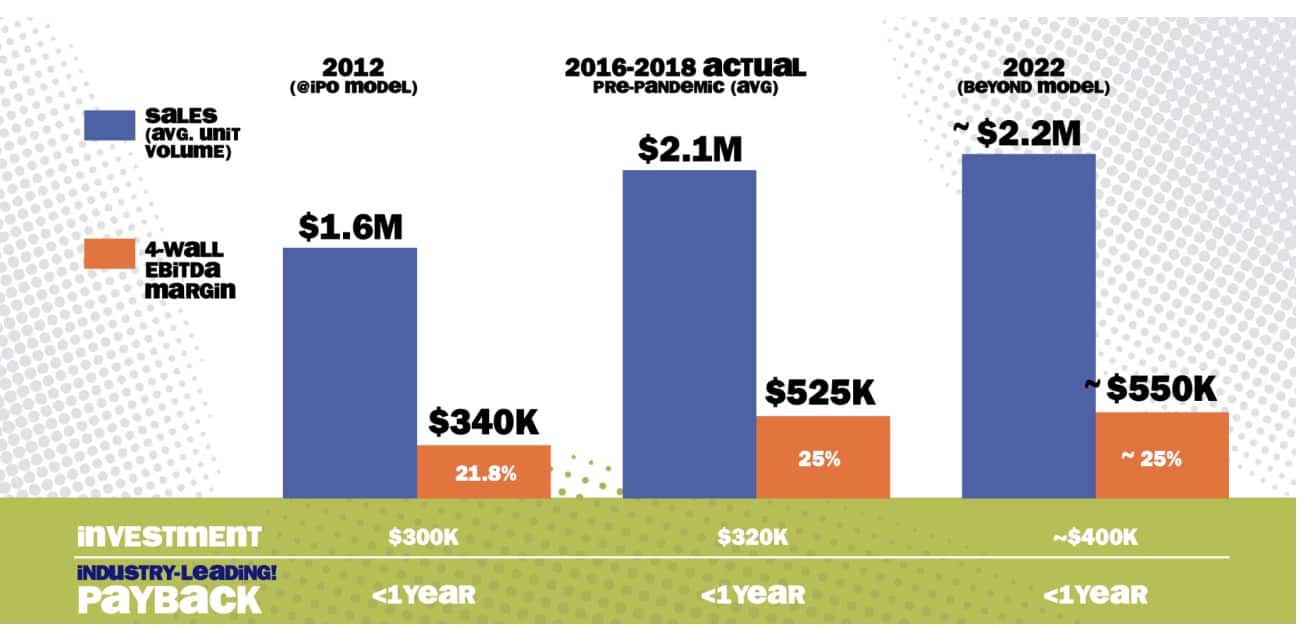

One Idea: Five Below (FIVE)

FIVE is a discount retailer that sells trendy/fad items for $5 or less (they released a new $5 Beyond section this year). They’re the only retailer obsessed with the teens-and-tweens demographic.

Stores cater to that demographic with spunky store designs, open concepts, and eight distinct product categories.

FIVE boasts industry-leading unit economics. Each store costs ~$350K to build. New stores generate ~$550K in EBITDA at 25% margins within their first year.

That means FIVE generates 150%+ new store ROICs and a payback period of <1 year. Because each new store generates so much profit quickly, FIVE can open more stores more frequently than its competition without tapping financial markets for assistance.

FIVE purposely builds stores next to high-traffic shopping areas like Target, TJ Maxx, and grocery stores. Such locations make it easy for parents to treat their kids to a unique shopping experience.

The last – but arguably most important – differentiator is FIVE’s commitment to low prices. Low prices are beneficial for a few reasons. Most of FIVE’s items are discretionary purchases of trendy things for kids. These aren’t the most durable items. But if you pay $5-10 for it, who cares if it breaks?

Two, low prices allow tweens to buy what they want, and parents can treat their kids without breaking the bank. Parental reviews show that though parents enter the store expecting 1-2 purchases, they leave with 5-7 items.

Finally, FIVE’s low prices insulate it from online competitors like AMZN. Most of FIVE’s products are (to steal Cliff Sosin’s phrase) “Un-Amazonable,” as the cost of FIVE’s average product makes shipping the item uneconomical for online retailers.

FIVE currently operates ~1,200 stores with plans to add ~1,000 stores by 2025 and reach 3,500 stores by 2030. The company should generate nearly $1B in EBIT by 2026 if they’re remotely right on store count growth and revenue growth.

Since its IPO, FIVE has traded at an average of 27.5x EV/EBIT. Assume a 25x multiple of 2026 EBIT, and you get ~$22B in shareholder value or nearly $400/share.

Disclosure: I own FIVE stock in my SEP IRA at this time.

Wrapping Up: Where To Learn More

Thanks for reading, and I hope you learned something. Check out these resources if you want to learn more about Alex, his Investment newsletter, other podcasts, etc.:

- Alex Morris on Twitter

- Alex Morris First Value Hive Podcast

- Alex’s Investment Newsletter

- Alex Morris Podcast Appearances (here, here)