The following is an excerpt from our weekly Market Brief. If you’re interested in learning more about Market Briefs and the Macro Ops Hub, click here.

Here’s an interesting question: Is the Trump administration’s erratic policy and governing style bullish or bearish for stocks?

Lately, I’ve read a number of analyst notes talking about how the current political uncertainty spells trouble for the stock market. They all include the line “…if there’s one thing markets don’t like, it’s uncertainty about the future.” I think that’s lame thinking.

I would argue that this “uncertainty” is bullish for equities, at least over the short-term.

I say this because this “uncertainty” is feeding into the Fed’s rake hiking decisions. Remember the hawkish tone coming from Fed members back in December? That seems to have been reversed since Trump took office and started significantly shaking things up. Fed members have cited the uncertainty over future fiscal policy as a key reason to err on the side of caution in raising rates.

FOMC member, Neel Kashkari, wrote a post this week explaining his reasoning for voting to keep rates steady at last month’s meeting. The whole post is worth reading (link here). but here’s Kashkari’s concluding remarks:

We are still coming up somewhat short on our inflation mandate, and we may not have yet reached maximum employment. Inflation expectations remain well-anchored. Monetary policy is currently somewhat accommodative. There don’t appear to be urgent financial stability risks at the moment. There is great uncertainty about the fiscal outlook. The global environment seems to have a fairly typical level of risk (though that can change quickly). From a risk management perspective, we have stronger tools to deal with high inflation than low inflation. Looking at all this together led me to vote to keep rates steady.

Fed President James Bullard, also cited fiscal uncertainty in a speech he gave this week saying “It is unlikely that fiscal uncertainty will be meaningfully resolved by the March meeting… We don’t have to move. We have a lot of fiscal uncertainty. Why not wait until that is more clearly resolved?”

So Trump’s unconventional governing style is creating uncertainty over the future which is making the Fed step back from its rate hiking path. This is supportive of equity prices over the short-term. The breakouts this past week in many of the indexes seem to confirm this.

This creates the unusual situation where a more steady governance and a clearer picture of future fiscal policy would likely lead to faster rate hikes and thus be a net-negative for markets.

The Fed conducts a Senior Loan Officer (SLO) Report every quarter. In this report they survey roughly 60 large commercial banks and up to 24 large foreign banks with branches in the US. The survey is intended to provide a quarterly update on credit availability and demand as well as developments in lending standards. It’s a good barometer of the overall credit market and provides us useful insight into how the credit cycle is developing.

The most recent SLO came out this past week and the data confirms our belief that we’re in the later stages of the current business cycle.

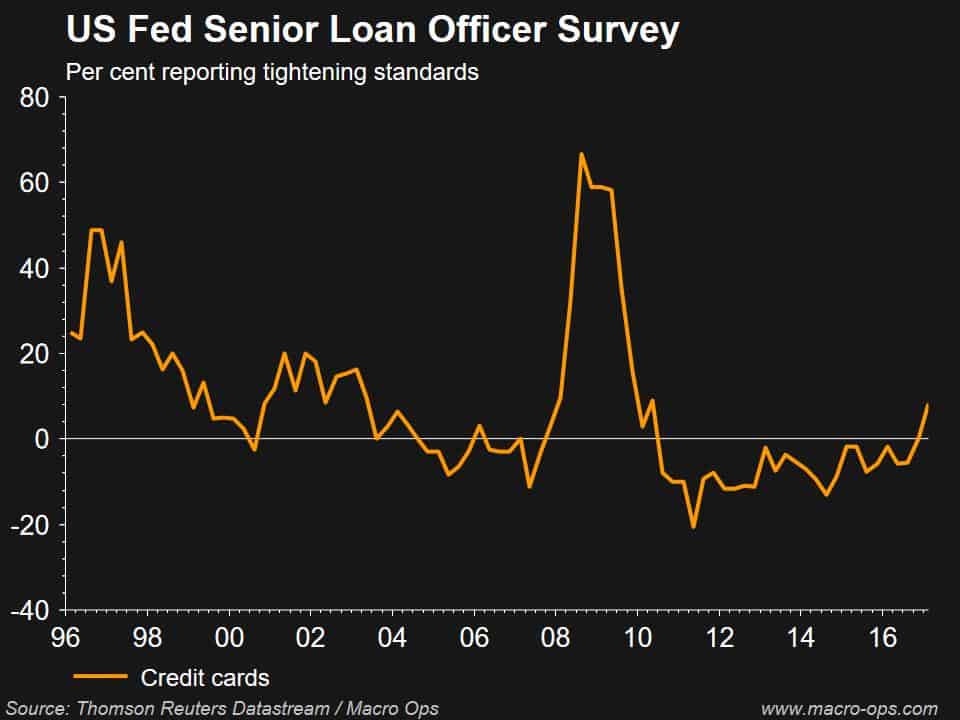

The below chart shows that loan officers are reporting an acceleration of tightening lending standards for credit cards (above zero means tighter credit).

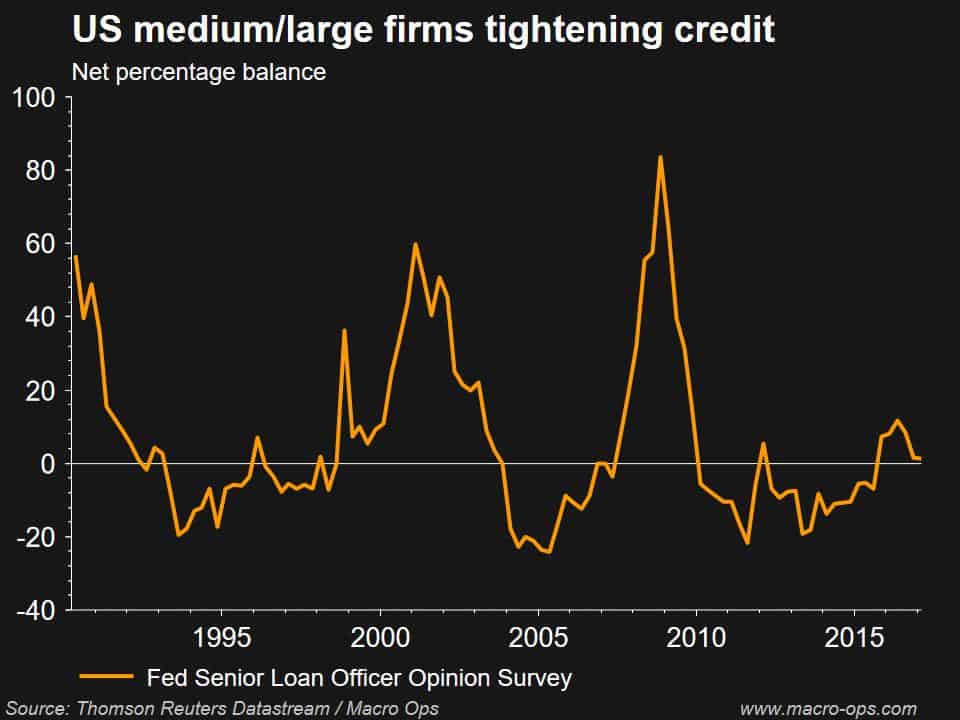

The same is true for medium to large businesses.

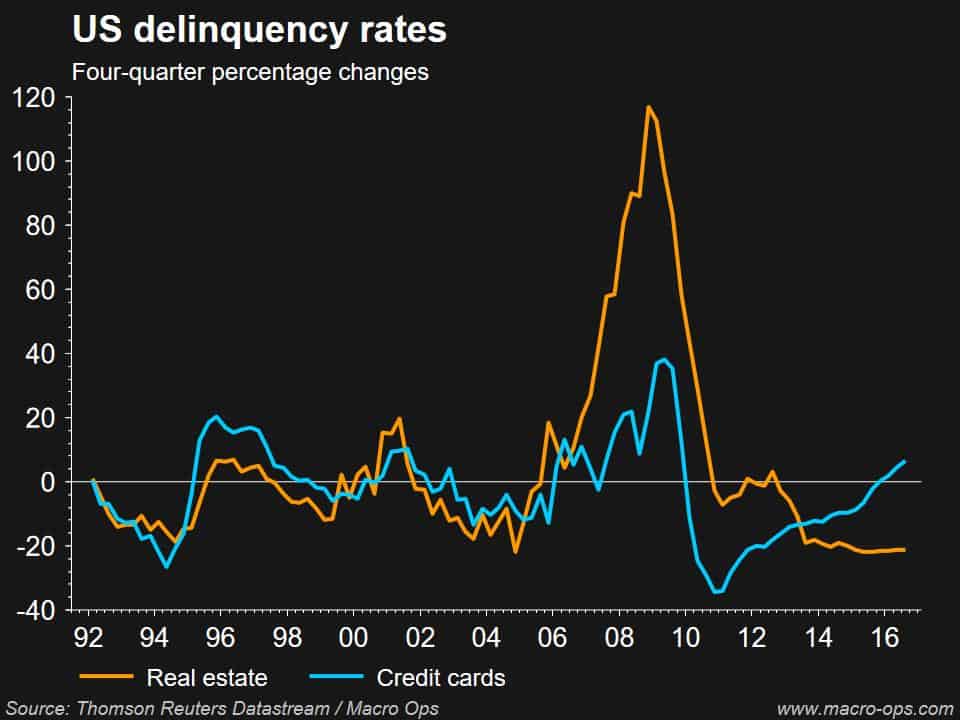

Some of this tightening is being driven by rising delinquencies on credit card debt and as interest rates tick higher we should see that trend spread to other areas like mortgages as well.

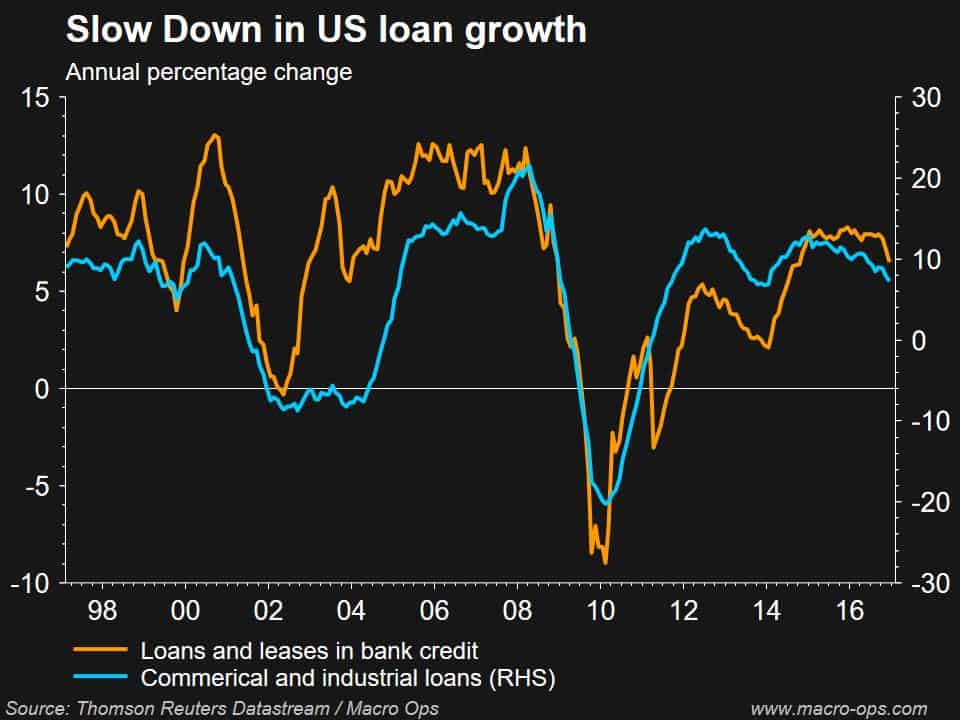

We can see the impact this slight tightening is having on loan growth which has slowed and appears to be turning over. Another sign that is typical in the later stages of a credit cycle.

So though credit is still extremely loose and capital is easy to come by, the beginnings of a reversal in that trend are appearing in the lending standards and delinquency data. That means we should see this weakness begin to be reflected in the credit markets in the coming months and things like high-yield debt will start to roll over.

The above is an excerpt from our weekly Market Brief. If you’re interested in learning more about Market Briefs and the Macro Ops Hub, click here.