***The following is an excerpt from a weekly note sent out to members of our Collective on 9/3***

Let’s start this note off with a story and a lesson from one of my all-time favorite trading related books, John Percival’s The Way of the Dollar. John writes (emphasis by me):

“There is another description of the consensus-that’s-not-confirmed-by-price. It consists of two images that have become part of the ancient lore of Wall Street, the Wall of Worry, and the River of Hope. A bull market we recall, “climbs a wall of worry” ; and “a bear market flows down a river of hope”. In point of fact, the description normally only applies to the early and middle stages in bull and bear markets. So we can be very comfortable when we diagnose a wall or a river — assuming we’re climbing and flowing respectively.

“In the later stages of the trend, things change. The worriers capitulate to the up-trend; and the hopers throw in the towel and give up the fight against the bear. At this stage, in a bull market, we find die-hard bears saying that, well, we are heading for a collapse, but prices are going to go up further before they head down. And in a bear market, die-hard bulls assert that prices are far too low — but they can go lower still. The conversion process is nearing its end.

“Now we have to get a little wary, for obviously we are in the region of consensus. And this is a very dangerous region because nobody on earth can tell how far things can go. Currencies, stocks, commodities — it makes no difference. In this respect, they’re all the same.

“It is said of Joseph Kennedy, father of President John Kennedy, that when he was having his shoes shined one day in autumn 1929, he was astonished to hear the shoeshine boy tip him a hot stock that was sure to go from 160 to 2000 or whatever. That was all Joe K needed. If shoeshine boys (or elevator attendants, or hairdressers, the cover of Newsweek or whatever) were tipping stocks, it was time to get out. So Joe K started selling short and thus laid the foundation of the family fortune — so the story goes.

“But if it’s true that Joe K went short at that moment then he was lucky. The sucker buys at the top of the market; geniuses and liars sell at the top of the market; but the super-sucker sells short at what he thinks is the top of the market.

“In 1979, the then financial editor of Britain’s Daily Mail newspaper, Patrick Sargent (later to be a founder of Euromoney), called the top of the gold market at around $450. It was a perfectly sound call, in the light of the speculative heat in gold at the time especially from one who had been bullish of gold for a good time. Yet gold was to climb a further $400 by early 1980, when speculation turned from red-hot to white-hot. Imagine being short at $450! As I say, no-one on earth knows where a speculative trend will end — except with hindsight…

“This brings us to the question of how you can distinguish a minor multi-week extreme from a major multi-month or multi-year extreme. The late stages in that great dollar bull market of 1980-5 provide a clue: you watch the way the conversion process trickles down through the different categories of currency observers. In mid-1984, the world was still full of die-hard dollar bears who had considered the currency overvalued ever since 1981. Who were they? It wasn’t the dealers, who are not and do not need to be overly concerned with underlying value; nor was it the trend-followers. It was the value-oriented analysts — researchers and economists by profession — with a long-term orientation.

“What happened was that sometime during the autumn of 1984, the bearish consensus among this category turned round; and it happened relatively suddenly. You will see it quite clearly if you go back over the research material turned out by major banks at the time. “The dollar is grossly overvalued at DM 3.00, but we think it will head further up before it collapses”, that kind of thing.

“In other words, it’s just as you would expect. When the long-termers who were formerly skeptical at last capitulate to the trend, then you have a total consensus and the end is nigh for the major multi-month / multi-year move. Nigh, but not necessarily over. At this point, one of our sentiment gauges comes into its own. We have to watch market action: the way the markets react in relation to the background and to news events.”

Consensus conversion… no-one on earth knows where a speculative trend will end… and total consensus...

Some valuable lessons from John… These are things we should keep front of mind as we navigate a bull volatile market through the worst period of seasonality (September) for markets.

The Nasdaq sold off as much as 6% at one point today. Giving it its largest single-day decline since March. This action shouldn’t surprise any of us since it’s typical volatility following a major buy climax, along with the increased trend fragility and sentiment/positioning headwinds we’ve been noting these last two weeks.

The Nasdaq sold off as much as 6% at one point today. Giving it its largest single-day decline since March. This action shouldn’t surprise any of us since it’s typical volatility following a major buy climax, along with the increased trend fragility and sentiment/positioning headwinds we’ve been noting these last two weeks.

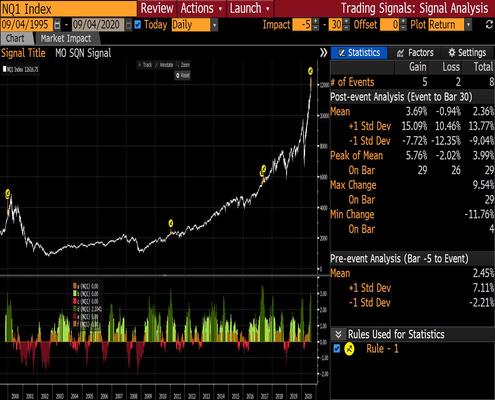

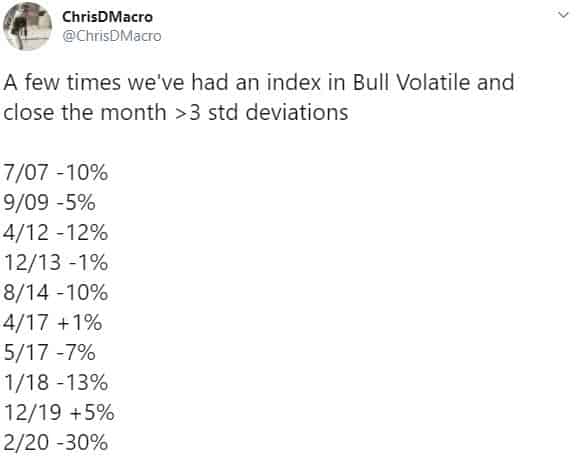

The Nasdaq SQN closed last month over 3std in a Bull Volatile regime]. My bud Chris D lays out in this tweet what has happened historically following similar readings.

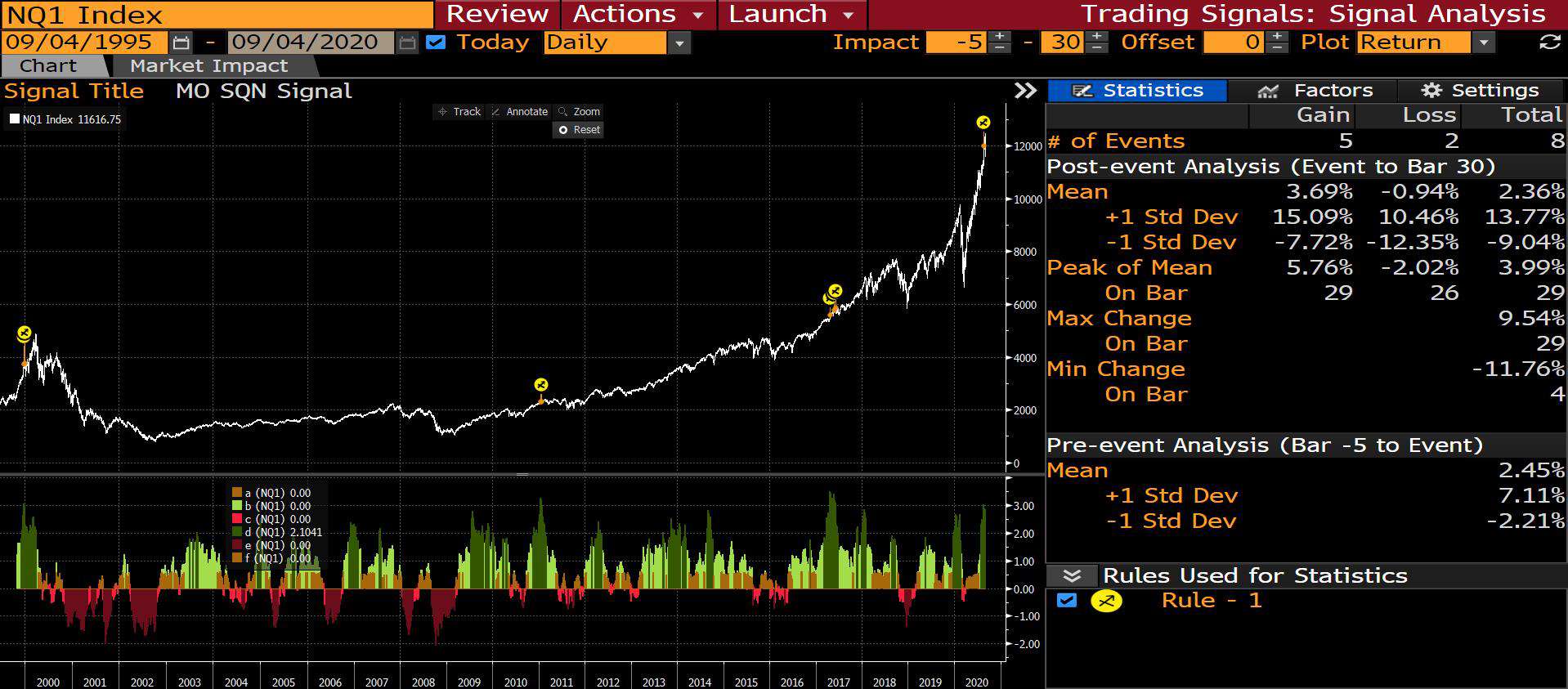

The outcomes are a little better when looking at just the Nasdaq during the following 30-days after an SQN reading above 3.

Here we get 7 instances over the last 25-years with 5 gains and 2 losers. The average gain is 3.69% and the average loss was 0.94%. But the peak-to-troughs moves show a much wider dispersion of outcomes.

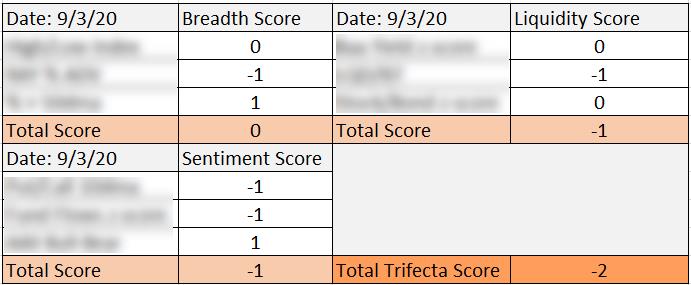

Our Trifecta Lens gives the market a current score of -2, which is the worst reading since before the March low. It’s still far from the -6 readings that have marked past major tops, such as the one we saw in February. But it could quickly get there if we see the market move down to its lower Bollinger Band. On the other hand, it could flip back to positive.

Buy climaxes such as these are notoriously difficult to play. Speculative momentum could easily reverse this market back up tomorrow. Bears want a negative weekly close, giving them a weekly sell signal. And bulls want a reversal. This 3,510 level on the SPX will be acting as a magnet tomorrow. Seeing as how this is a 3-day weekend, I have a feeling we might see further selling tomorrow as people look to lighten up their books.

Normally we wouldn’t even consider cutting/hedging risk at this point since the indices are still well above their lower Bollinger Band Setups. But the overextension of the tape from their 20-day averages means the market could fall a good deal before hitting its lower bands. And considering the extreme sentiment/positioning, I’m more willing to proactively hedge out some of our risk.

If today was the start of a broader 10-15% pullback, then that would put the 3,200 and 3,000 levels into play on the SPX.

So this is what we’re doing for now. We flattened out our Core 25% SPX position and put on a 25% of NAV equivalent short in the Nasdaq (NQZ2020). We also have our bond position which is acting as a counter-balance. But if this ends up being more of a reflation rotation type move, then bonds may not give us as much negative downside capture as we’d like.

We’re keeping the remainder of our positions on for now and will honor existing stops, of course. We’re going to be nimble and adjust fire as this move progresses. We don’t want to overreact and get treed nor do we want to under prepare and get caught flatfooted. We’ll send out updates as we make moves.

My base case is that this ultimately ends lower, in the 10-15% range. And I suspect we’ll start to hear the narrative of “failing CARES 2 stimulus talks” come to the fore. Congress is back in session soon and talks have reportedly hit a wall. I ultimately believe we get a bill passed, likely closer to the Dem’s target range of $2trn — nothing like a market selloff to instill some fear, do a little arm twisting, and get our valiant leaders to act!

Plus, there’s still a large amount of big hedge fund money that has sat this entire rally out (as I pointed out in this week’s Monday Dozen). I assumed they’ll use any 10-15% dip to come in and buy hard, especially if it looks like a solid CARES 2 will get passed.

Basically, my current base case is what I tweeted yesterday (below). This is just speculation of course and there are a lot of moving parts, so opinions weakly held and all that.

~~~~~~~

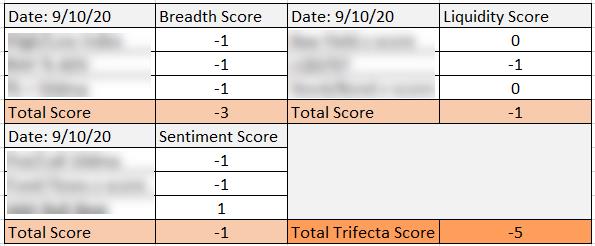

This note was sent out to Collective members on the 3rd. Our TL Score is now -5 for the market. That’s the most bearish reading since the start of the late February selloff, where we saw a consecutive string of -6s (which is about as bearish as our scoring gets).

This means that trend fragility is high and we should expect continued vol and further downside in the near-term until some of the negative marks in the TL score can be corrected.

Our doors are open until the end of day Sunday. At which point we’ll be closing the enrollment period and won’t be opening back up for some time.

We offer differentiated research, theory and education resources, plus a killer community (Slack) filled with some of the smartest Operators from around the world. Our members are predominantly professionals but we also have a number of highly motivated retail players. The one thing we all share is a deep love for the game and an unquenchable thirst to get better.

If this sounds like you then consider signing up and checking us out. I look forward to seeing you in the group! And as always, don’t hesitate to shoot me any questions.