Prabowo Subianto will most likely win the Presidential election in Indonesia. He will take over after a ten-year run by highly popular president Joko Widodo (80% approval rating).

Why does this matter? The guy who Joko endorsed just won with Jokowi’s son as VP.

One of Joko’s last requests as president was a critical minerals export ban. Now that Joko has his man in office, we believe the export ban will happen and Indonesia tin exports will grind to a halt.

Indonesia has done this before, with great success, and it looks like they’ll doing it again with tin and other critical metals. The country is responsible for 20% of global tin supply. This will rock the already fragile tin market.

We’ve been pounding the table on Resource Nationalism at Macro Ops. I wrote about this potential tin catalyst for Collective members back in November 2023. Now that it’s here, I want to share the report with you.

If you’re interested in tin and haven’t read my Tin Industry Primer, do that first. Then come back and read this piece.

Indonesia’s Resource Nationalism Plans

Imagine you’re a lemon salesman. You go around the country and sell fresh lemons to lemonade stand entrepreneurs. You have no control over lemon prices. You simply sell at the last quoted price.

It isn’t a great business. And after a while, you realize that the lemonade stand is where the real money’s at. It has the distinct advantage of charging a premium on the sum of its commodity parts (lemons, sugar, water).

Eventually, you say, “screw it, I’m getting out of the lemon business. I’m selling lemonade now!”

That’s basically what Indonesia is doing with its critical minerals.

Indonesia will choose a new president in a few months as Joko Widodo completes his second term. The current frontrunner is Defense Minister Prabowo Subianto. Whoever wins has big shoes to fill.

Widodo will finish his 10-year term with an 80% approval rating (not a typo). In other words, if you’re the new president and want to make a good first impression on the country, you probably shouldn’t change the policies.

One such policy is an export ban on critical minerals (emphasis added):

“Widodo has led efforts to promote export restrictions on raw minerals while advocating for ‘adding value to resources.’

Beginning with a ban on exports of raw nickel ore in January 2020, Widodo has expanded restrictions to other metals, imposing an export ban on bauxite, the ore used to make aluminum, in June this year. The list will grow next June after the country adds five more items, including copper concentrate, tin and gold.”

Indonesia doesn’t want to sell lemons. They want to sell lemonade. And it’s worked very well for them (emphasis mine).

“The ban on nickel ore exports has been a big success. According to the Jakarta Post, nickel-related exports, which amounted to 17 trillion rupiah ($1.1 billion) in 2017, rose 19-fold to 323 trillion rupiah last year as key export items shifted from raw metal ore to products with higher unit prices.

Those products include ferronickel, an alloy containing iron and nickel, and nickel matte, which is used in the processing of nickel ore.”

When asked about Indonesia’s history as a raw material exporter, Widodo said, “For years, we have always exported raw materials. This is a mistake that we must not repeat.”

Before we explore the consequences of Indonesia (and other emerging countries’) shift from raw materials to value-added products, we should ask ourselves how we got here.

For a while, developed economies like the US had all the leverage in the raw material relationship. The West was like, “hey, we’re making all these cool toys that need your raw materials. Why don’t we cut you in on the action and allow you to export that stuff to us?”

This wasn’t the worst deal for emerging markets. They received foreign investment, international credit, and state revenues in exchange for their raw materials.

The “problem” occurred when the West got drunk on its NIMBYism. Yes, the US cares about the environment, and we don’t want to drill mega-holes on our soil. Instead, we’ll farm off CO2 emissions and environmental destruction to some jungle in the Congo.

Eventually, the US/West stopped investing in raw material production. They didn’t need to because they sold high-margin value-added products.

The tide is turning.

“For a long time, developing countries have had no choice but to accept the terms of industrialized powers, which have capital, technology and markets. But the picture has begun to change, with an increase in the economic power and influence of emerging and developing countries, collectively known as the Global South.

Some are now “in rebellion” against the system which, under the name of free trade, has long constrained their efforts to develop domestic industries.”

From lemons to lemonade.

But it’s not just Indonesia and China. Mexico and Chile are nationalizing lithium production. With all the money flowing into EV production, why should Mexico and Chile be content selling lemons? Even the Philippines is considering an export ban on nickel.

Resource Nationalism is staring us in the face, yet nobody seems to care or notice. We will care only when commodity prices skyrocket in response to a massive supply shock.

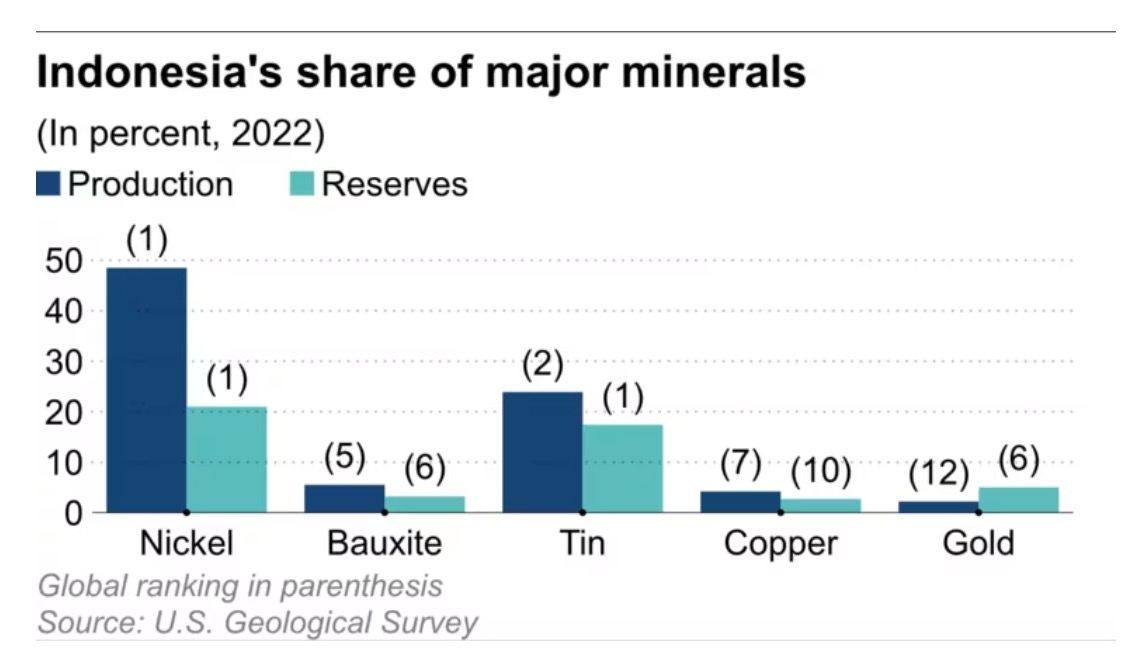

Let’s use tin as an example. Indonesia will likely place some export ban on tin next June. The country is responsible for over 20% of global production and ~18% of global reserves.

What happens if they use 25% of production on value-added products instead of raw materials export? Who’s picking up the slack in a market where the world’s third-largest tin exporter loses money at $27K/ton?

The bear case for tin (and every other base metal) is that we’ll eventually have a recession. That recession will crush demand and balance the already supply-constrained market.

But there’s no supply/demand model for “what happens if Indonesia takes 25-50% of its supply offline to make its own widgets instead?”

And so you have this setup where the baseline price to bring new supply online is ~$3K higher than the current spot price in a market where 20% of the world’s supply might take 50% of it offline.

And AFM’s stock hasn’t moved in two years. It doesn’t make sense.

When things don’t make sense, especially in commodity markets, it’s best to KISS and focus on changes in supply and demand. The demand story, barring a global recession, remains unchanged. The supply story, however, looks more bullish with each news release.

Also, it looks like tin prices are inflecting (see below).

We own a lot of Alphamin Resources (AFM.V) and will look to add on technical confirmations. That said, none of this is investment advice. Please do your own research. This is mining after all. Everything that can go wrong probably will go wrong. Position size accordingly.

Tin is now a Trifecta Lens trade. Fundamentals, sentiment/positioning, and technicals are all aligning for a massive move higher. All we can do is place our bets, monitor the situation, and enjoy the ride.