Think of all the news that has come down the pipe over the last two weeks…

We had the elections where it looked for a moment like Trump would stage a surprise upset (again). The tighter than expected race has left the Senate up for grabs, though Republicans should take it giving us a divided government.

The election is being contested and Trump is, despite all the evidence to the contrary, claiming victory as well as widespread voter fraud. His moves in recent days of firing the Secretary of Defense, Deputy USAID Chief, top climate scientist, and Energy Regulation Commission Chair, refusing to allow the start of the transition process with the President-elect, pushing Barr to break precedence and open a federal investigation into voter fraud, etc… Doesn’t exactly instill confidence we’ll see a smooth transfer of power.

Then there’s COVID making waves… literal waves, as in its 3rd wave here in the US. This one much bigger than the others in the level of new cases. And it’s projected to get much worse in the coming months. Countries in Europe, including the UK, are enacting various levels of lockdown, again.

All in all, we ended up with a contested election, disorderly transfer of power, a divided government, accelerating COVID cases forcing lockdowns… oh, and no second round of fiscal stimulus.

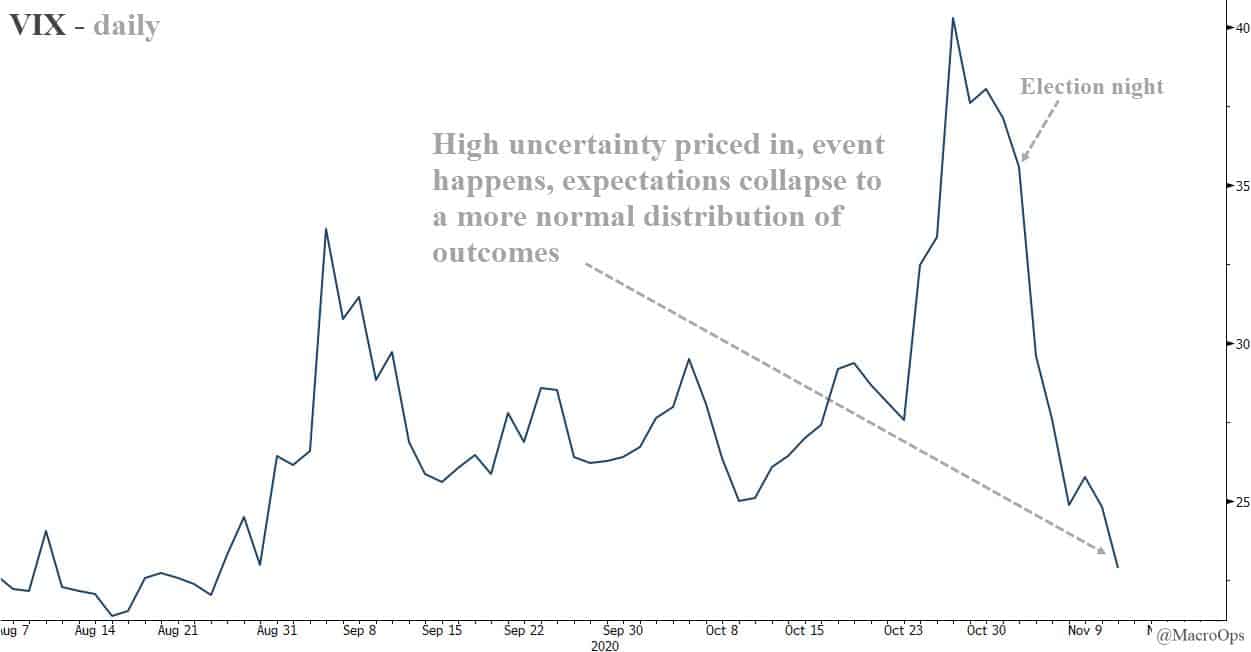

The market’s fears have been realized. This exact scenario is what drove investors to begin bidding up vol in early October. And yet, here we are… At the top of a four-month range. Just a freckle and hair from all-time highs.

In the Marine Corps, this would receive a loud “Whiskey-Tango-Foxtrot, over?!”

Most can’t grok the counterintuitive nature of markets. They may theoretically understand that public information and aggregate opinions are immediately embedded into the price. But they don’t actually get what that means from a practical standpoint, let alone have a process that harnesses that truth.

Luckily for us, the MO approach is built around Playing the Player and not arguing with the tape. We simply compare what markets are doing relative to the sentiment and positioning at the time.

This is what we were talking about when we wrote in “Sitting On Hands” the night before the election that:

…this is a known-known. Everyone is expecting an ugly contested election, so this is likely already in the price. And any outcome where, say, we get data indicating a clean sweep by either party/candidate, would positively surprise and therefore be good for short-term price action.

The VIX is already juiced up at 40. So while we could see a brief spike higher, it’s much more likely that we’re near max uncertainty and we’ll see vol compress as the results start coming in.

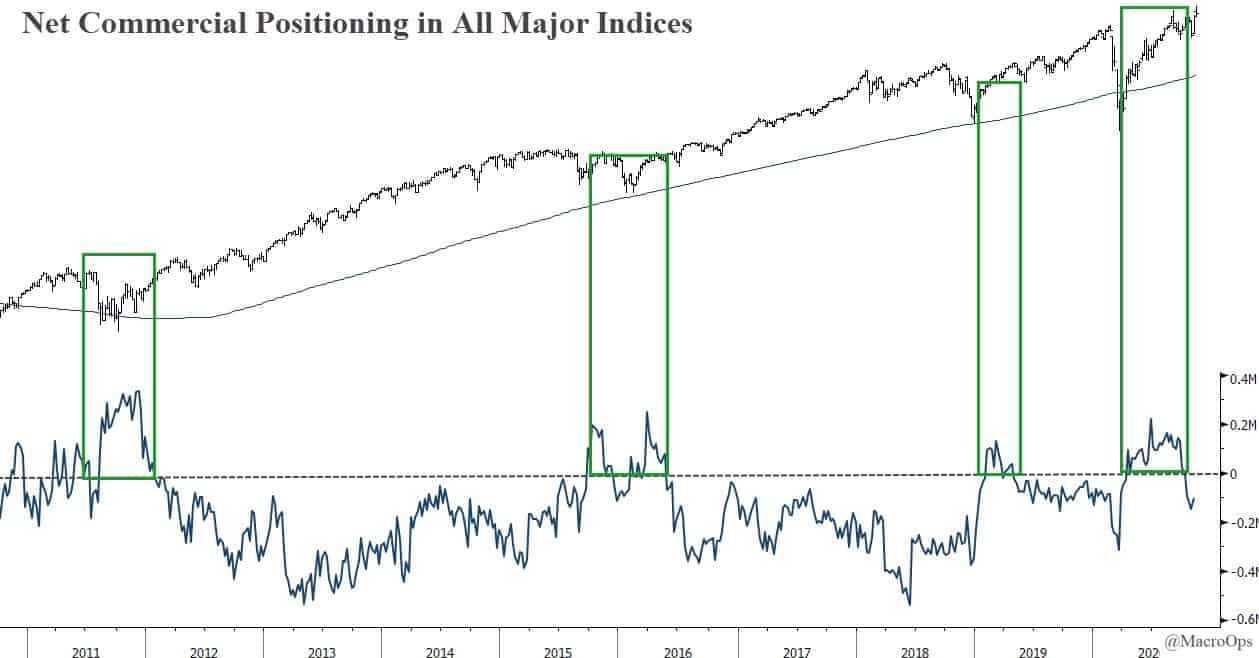

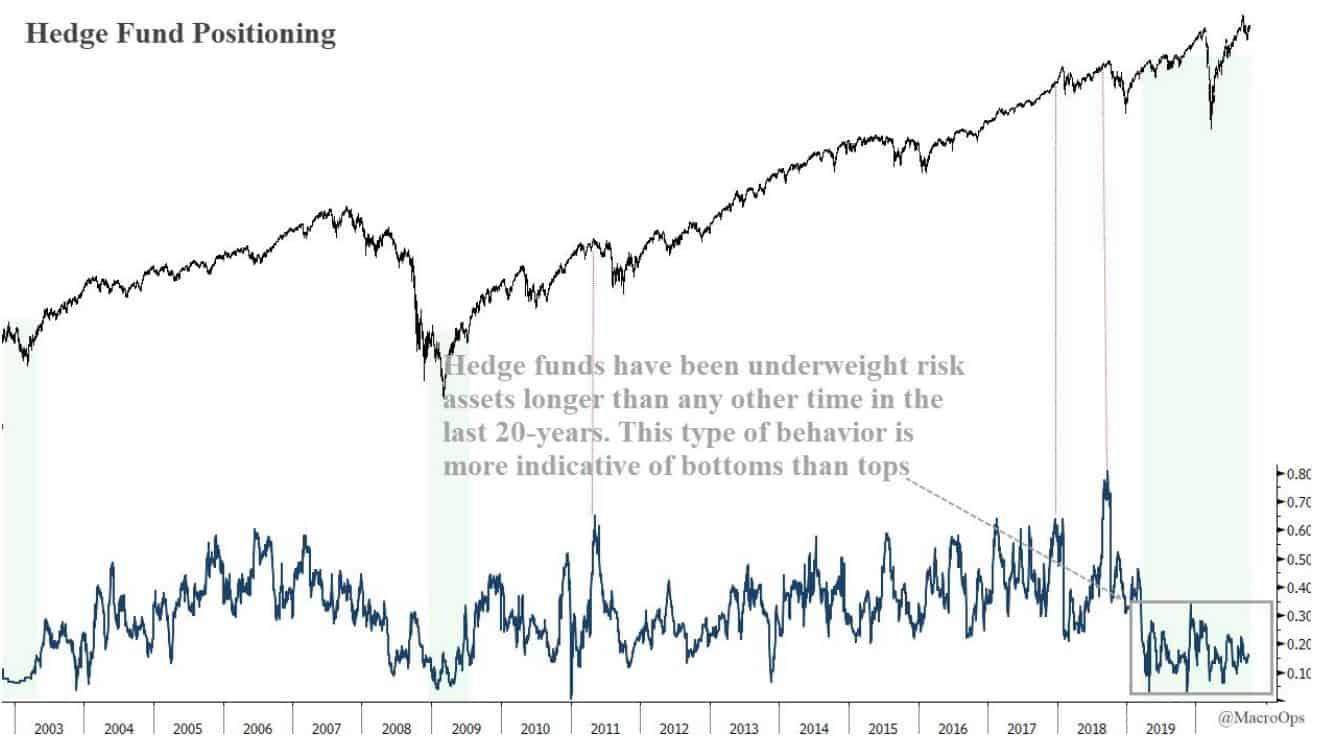

The fact that markets are rallying in spite of all that is happening is a signal in and of itself. It’s telling you that participants are coming to the realization that they’re too underweight on risk. The large cash piles carried by institutions that we talked at length about in our early October writeup “Sleight of Hand” are only starting to be put to work.

This approach to markets is pretty liberating — not to mention more profitable — compared to the alternative, which consists of being bludgeoned by the 24/7 news noise cycle and reacting to every dip and jump on the screen as if any of that stuff matters.

I’m reminded of the section from Livermore’s book “How To Trade In Stocks” when he shares the story about the successful speculator who lived in the mountains. Here’s that bit with emphasis by me:

Remember this: When you are doing nothing, those speculators who feel they must trade day in and day out, are laying the foundation for your next venture. You will reap benefits from their mistakes.

Speculation is far too exciting. Most people who speculate hound the brokerage offices or receive frequent telephone calls, and after the business day they talk markets with friends at all gatherings. The ticker or translux is always on their minds. They are so engrossed with the minor ups and downs that they miss the big movements.

Almost invariably the vast majority have commitments on the wrong side when the broad trend swings under way. The speculator who insists on trying to profit from daily minor movements will never be in a position to take advantage of the next important change marketwise when it occurs.

Such weaknesses can be corrected by keeping and studying records of stock price movements and how they occur, and by taking the time element carefully into account.

Many years ago I heard of a remarkably successful speculator who lived in the California mountains and received quotations three days old. Two or three times a year he would call on his San Francisco broker and begin writing out orders to buy or sell, depending upon his market position. A friend of mine, who spent time in the broker’s office, became curious and made inquiries. His astonishment mounted when he learned of the man’s extreme detachment from market facilities, his rare visits, and, on occasions, his tremendous volume of trade.

Finally he was introduced, and in the course of conversation inquired of this man from the mountains how he could keep track of the stock market at such an isolated distance.

“Well,” the man replied, “I make speculation a business. I would be a failure if I were in the confusion of things and let myself be distracted by minor changes. I like to be away where I can think.

I like to be away where I can think…

I love that.

It pays to overweight the tape and underweight the news. We want to be long technicals and short popular narratives. Long trend continuation and short top callers.

The market’s equivalent to the Call of the Sirens is to over-intellectualize this game which just doesn’t pay. That’s because most of what people intellectualize over is already in the price. Like Odysseus, we’re better strapping ourselves to the mast, less we get drawn to the “smart” theories and opinions that populate the ether.

So what’s the play going forward?

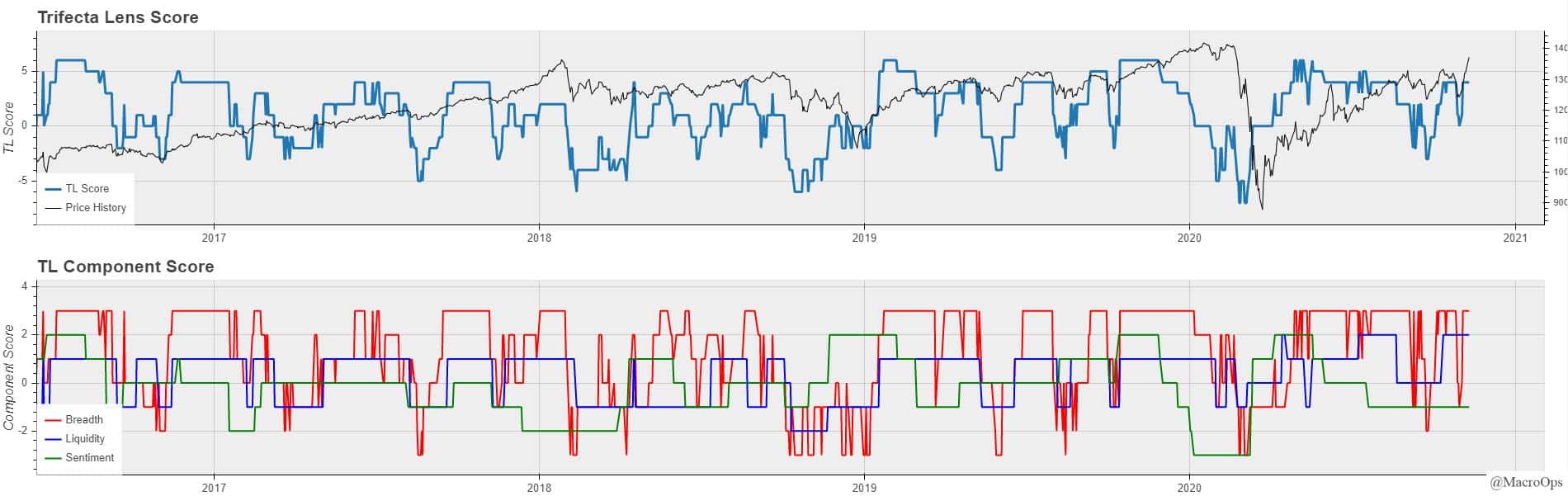

Well, we’re in a Bull Quiet regime in a primary uptrend and the TL Score is a +4. This means we want to be long and buying (which we are).

You can see the breakdown of the TL Score on the bottom graph. It shows that both breadth and liquidity are currently supporting the bull, while sentiment is slightly negative at -1 (the sentiment score is likely to drop to a -2 to -3 in the coming days).

I expect we’ll soon punch through the upside of this trading range, likely after one more tiny dip to put people offsides.

That’s going to suck in a lot of sidelined cash which could potentially send the market on a strong run into the end of the year, which happens to also be strongly supported by seasonality (SPX = orange line, 30yr average = white line).

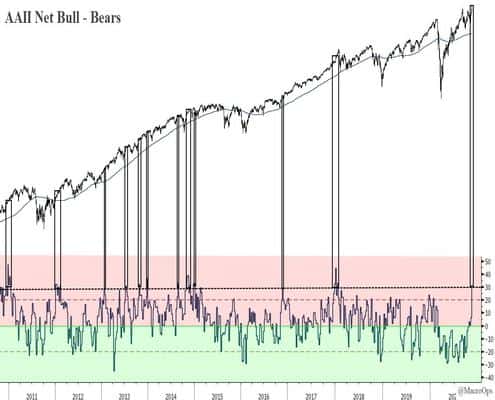

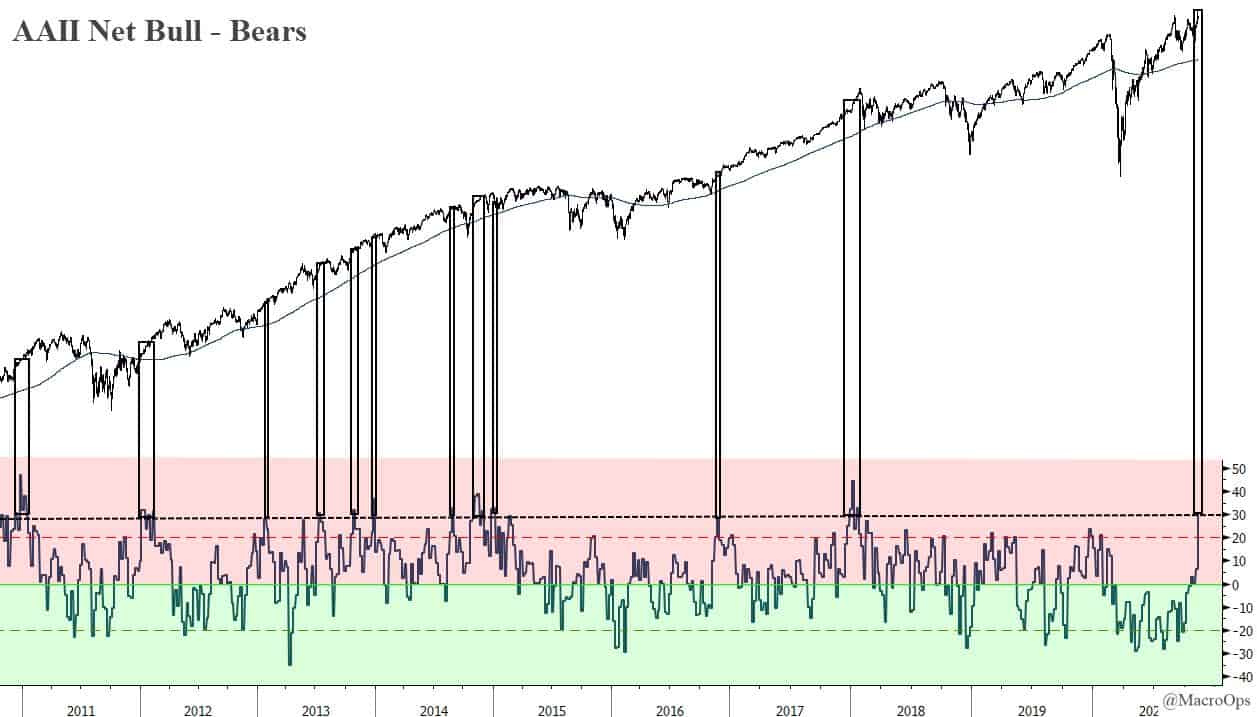

Sentiment and positioning are the things to watch here as it’s starting to heat up to a boil. Take Net AAII for example, which is now above 30. This doesn’t necessarily mean weakness is coming. As we can see on the chart there are numerous past instances where an elevated AAII preceded more gains.

What matters though is how quickly this bullishness leads to over positioning. Luckily, we don’t have bearish signals on that front yet so we should expect more upside in the interim until that changes.

The broader macro backdrop is improving with the obvious caveat of COVID.

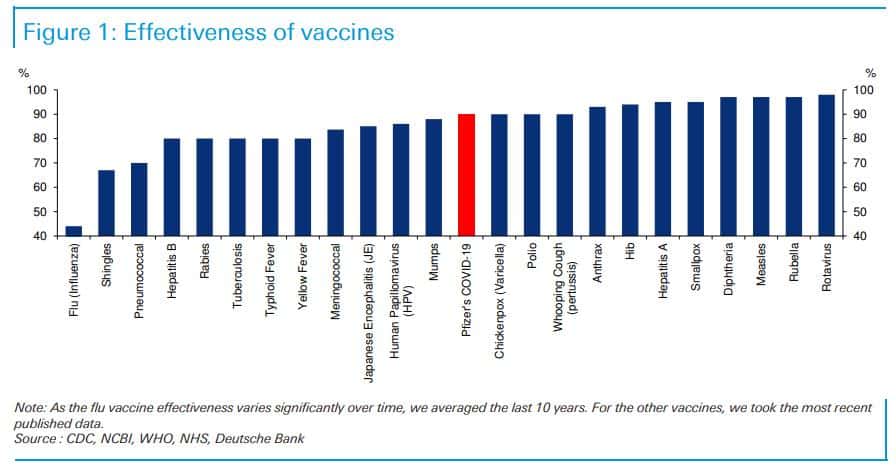

A vaccine is coming.

Pfizer announced the results of their COVID vaccine and the data is promising The vaccine is showing interim efficacy results that are in the 90% range, which is excellent if true.

And Pfizer is far from the only one in the race. There are currently 9 candidates in phase 3 trials globally. Pfizer’s success bodes well for a number of the others as they use a similar bio-pathway.

The Super Forecasters over at the GoodJudgement Project assign roughly an 80% probability that we’ll have enough doses of FDA-approved COVID-19 vaccine(s) to inoculate 25 million people in the US by May 31st.

This is excellent news as it gives us a viable path out of this mess. And from a narrative perspective, it may allow the market to sidestep the very bad COVID data that’s coming this winter, which is important.

One thing I wonder about though is, will the positive vaccine developments make governments more likely to enforce harsh lockdowns this winter? I’m not sure what the answer to that question is but it could have implications for the market.

Stimulus is coming but maybe not till early Spring.

Shortly after the election, Senator Mitch McConnel signaled he’s ready to get to work on passing stimulus before the New Year.

While this is promising we can’t take his words to the bank. With the all-important run-off election in Georgia that has two seats and control of the Senate up for grabs, McConnel is likely to defer to the two Georgia Republicans. We’ll get fiscal if they deem it will help their election odds and we won’t if they don’t.

An economy on the rebound.

Building permits are at new cycle highs which bodes well for construction activity going into next year.

Inventories are still nowhere near where they should be despite the rapid build we saw in Q3. So there’s still significant room for inventories to contribute to GDP growth going forward.

The labor market is staging a broad-based recovery and household balance sheets are actually stronger than they were pre-pandemic; thanks to stimulus, reduced spending, and rising stocks and home prices.

And lastly, we have incredibly supportive demographics, which we’ve talked about here. Millennials are just entering their prime homebuying years and will soon be in their peak earning years as well.

Will Small-caps and Value finally shine?

It typically doesn’t pay to try and call the turn on major macro trends. Newton’s Law of Inertia reigns and a trend in motion is likely to stay in motion, statistically speaking. Same goes for sideways regimes where mean-reversion dominates.

Growth and tech have been the leaders all cycle and we should expect this to remain so until there’s a clear reversal.

Above is the relative performance of Small Caps versus the Nasdaq. Relative performance has been sideways for roughly 7-months.

But we need to keep this relative performance in perspective. Below is the longer-term chart showing that we’ve seen a number of these sideways relative performance regimes over the last decade only to have tech and growth reassert its dominance.

With that said, there are some notable differences this time.

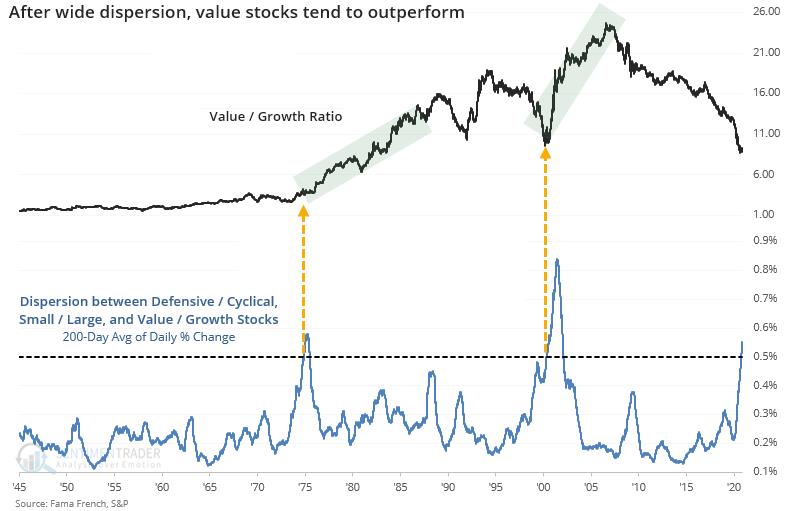

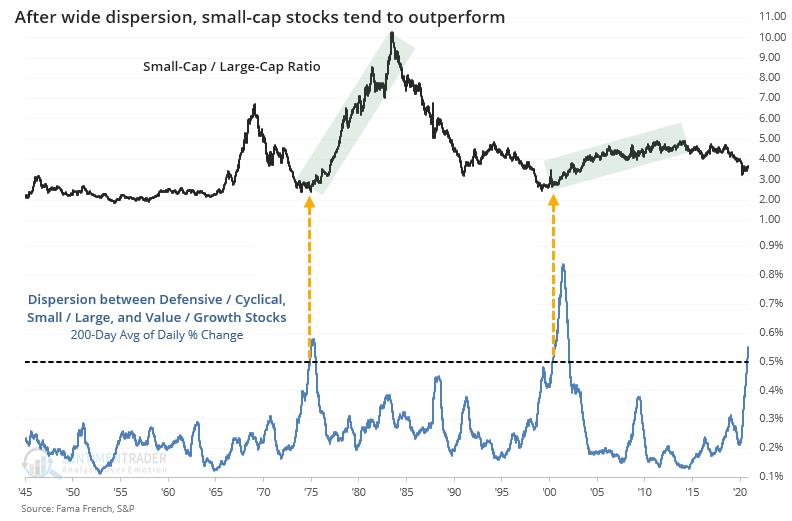

Check out these charts from SentimenTrader showing the recent extremes in factor dispersion.

SentimenTrader notes (emphasis by me):

The two periods with dispersions as great as they are now both led to extended periods of smaller stocks doing better than larger ones.

The same pattern holds true for value versus growth stocks. By the time dispersion among the factors reached the current level, value stocks were about to embark on multiple years with massive outperformance relative to growth.

Investors have been looking for a turn in these relationships for years, and yet in most respects, they just keep getting more extreme. It seems like Monday’s shock, building on the massive differences in positioning for most of this year, is enough to equate to some of the most notable changes in 75 years, and that has been a very good relative sign for small and value stocks.

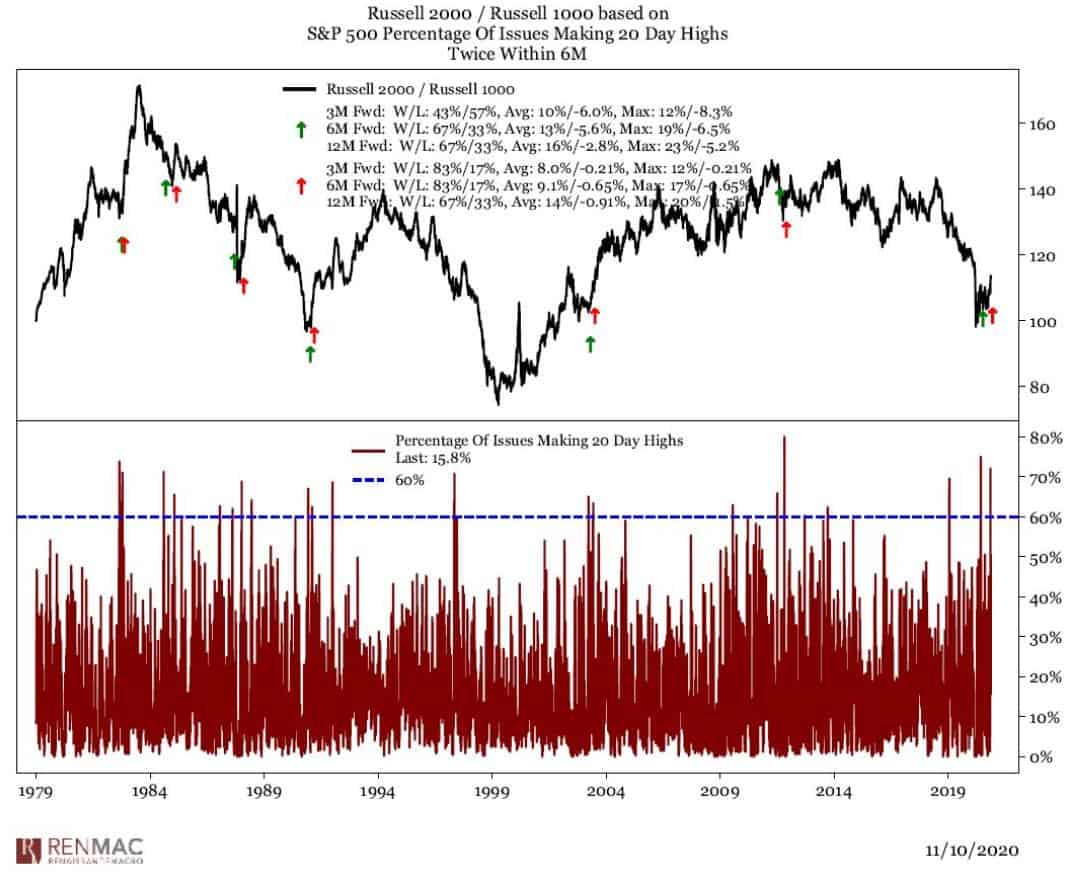

In addition to the extreme factor dispersion, we just saw a degraaf Thrust signal. This is when over 60% of issues make 20-day highs. Green arrows mark past instances below. Monday’s trigger marks only the 10th time history that this indicator has spiked above 70% according to RenMac.

RenMac points out the other instances where we’ve seen a deGraaf Thrust signal trigger twice in a six-month span. Past instances have historically led to small-cap outperformance.

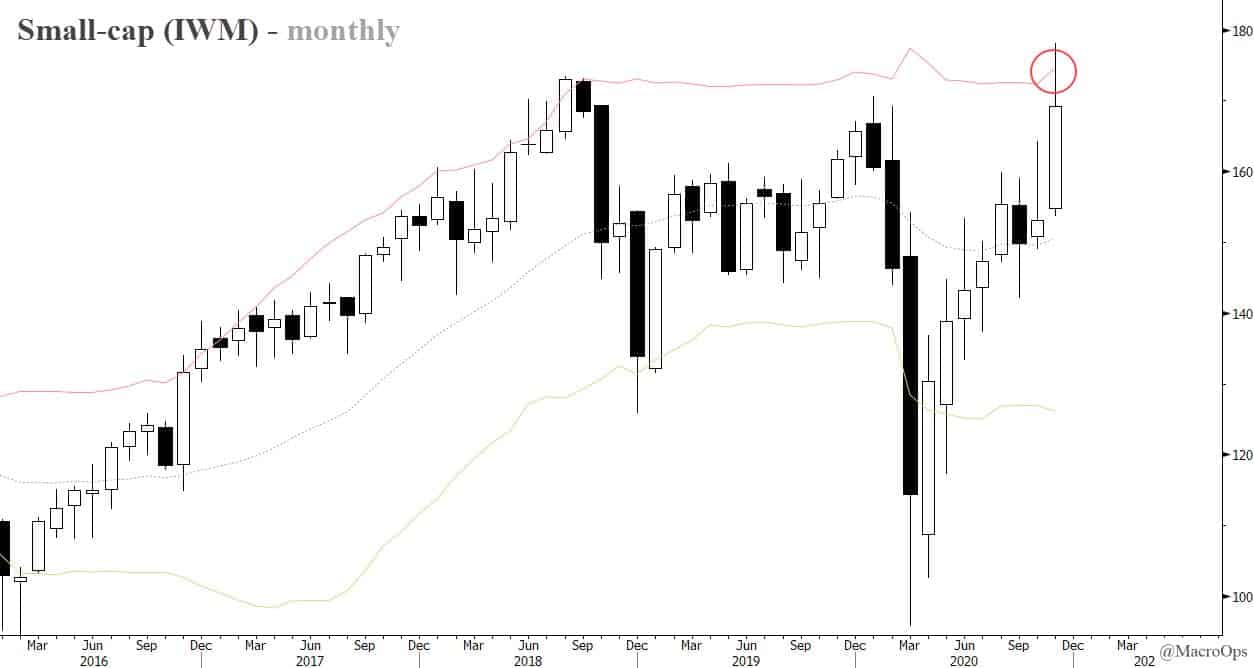

Small-caps (IWM) are currently banging against their upper monthly Bollinger Band and are so far being rejected. We may or may not see a dip here. With sentiment turning up, we shouldn’t be surprised if small-caps just punch straight through.

A few of the names we’re looking at are energy plays like Geopark (GPRK) and Antero (AR), the Jones Act shipper Overseas Shipholding Group (OSG), and container shipper Danaos Corporation (DAC), the Argentinian ag play Cresud Sacif ADR (CRESY).

If you’ve got some names that you like, please shoot them our way.

Our position in the Grayscale Bitcoin Trust (GBTC) is up a little over 50% since we bought in last month. The monthly chart is below.

This remains a high-conviction position for us. Negative real rates, expensive equity markets, an incoming fiscal wave, and underwater pension obligations are going to drive more and more institutions to add Bitcoin to their portfolios. First as a steady drip and then as a flood…

No belief in Bitcoin or crypto as a tech or store of value is required to get this bull thesis. It’s a simple supply and demand equation.

Bitcoin’s share of global liquid markets is a rounding error. Its market cap would have to rise 10x just to match the total private sector investment to gold. Demand is driven by a whole lot of cash and not a lot of places to put it with negative real rates forcing investors to step well outside their comfort zones.

I expect Bitcoin to easily clear its previous all-time high of 19,650ish within the next 6-months.

Lastly, how about those Micron DOTM Calls? They’ve already doubled and still have a looong ways to go. You gotta love mispriced optionality…